YWR: 10 Secrets to Stock Investing

Disclosure Alert #1. Not financial advice. Always get advice from a professional.

Disclosure Alert #2. This is not for professional investors. Or, maybe it is.

This week Ana Jones a 41 year old Ukrainian mom, single, with 2 girls, and YWR reader, built a stock market portfolio for the first time in her life.

She allocated

76% to the Vanguard S&P 500 Index Fund.

23% to the ishares Emerging Markets ETF

Plus some cash to buy on dips

Her friends think she’s crazy and want to see what happens to her.

If you’re also curious what happens Ana is writing about it on Substack (The Money Affair). A real life laboratory experiment.

Ana describes the instability growing up in the Ukraine. Nobody invested in stocks, only in paper $’s. The saying was ‘In US $’s we Trust’. Don’t trust anything. Don’t trust the economy, don’t trust the banks. Only trust US$’s hidden in a rice jar or a CD case.

Now she lives in Germany with a good job and things have settled down. For the first time in her life she can take the plunge and invest a little money in equities. Even if it’s terrifying.

She questions herself.

“You and stock investments? Hello! It is too complicated, risky, and requires too much money.”

“Yeah right, go invest your hard-earned money, let them disappear. Most of it is a scam.”

But I am curious and want to learn about it. If others can, why can’t I? I allowed myself to open up to this idea.

Which made me think how many other people around the world don’t invest in stocks, are intimidated by them, confused by them, or getting really bad advice.

Ana’s story reminds me of a taxi driver I met in Africa. He was taking me to the airport and we were making chit chat. He asked me why I had been in Zimbabwe and I said it was for business meetings and that I worked in the ‘stock market’. I asked him if he invested in the stock market and he said ‘No.’ and acted like that was a surprising question. He said the stock market was for rich people. For smart people. Not for him as a taxi driver. He wouldn’t know where to start. In a country where the stock market is the only way to protect your wealth that surprised me. ‘Stuck with me’ I should say.

My daughter goes to a University in London where all the CompSci and Physics majors are dying to get jobs at JPM, Jane Street or Blackstone. They say ‘EBITDA’ a lot, brag how many Excel shortcuts they know, and dream about being a Finance Bro. But according to my daughter few of them invest in stocks. They are mostly from India, China and SE Asia. Desperate to make money in ‘finance’ managing other people’s money, but have never invested themselves. To be fair they are students, who perhaps don't have money to invest in stock portfolios. Still I’m surprised.

As Americans we take investing in stocks for granted. It’s second nature. It’s our culture. We are practically forced to invest in the stock market by our employers. The company opens a 401K account for you and matches your savings every month. There are 1000’s of investment choices and you have to figure it out on your own. The company says “Here’s $10k to invest for your retirement. Hope it goes well.” So we’ve all gone through this experience and learned the hard way about investing for retirement.

Now US retail investors are the best in the world. They have built tremendous wealth and out invest the pros. It’s amazing.

But we don't realise how intimidating investing can seem for people in the rest of the world.

So for the single Ukrainian Mom’s, African taxi drivers and wanna be Finance Bros… this post’s for you.

It’s a list of common sense investing tips from someone who has spent a career in the investment management industry, invested everywhere in the world through all the cycles, managed other people’s money, managed my own money, and wasted years making tons of mistakes.

This isn’t get rich quick advice. It’s advice to have a positive outcome and make money instead of losing it. Let’s start with that. If we achieve a 9% CAGR over long period of time, and keep adding to the pile with savings, that’s a win.

My advice:

#1 Build your fortress. Step back. Why are we doing this? You are building your multi-income stream fortress. You have your day job, or your business. That’s your #1 income stream. Now we want more income line items. And the stock market is a big one. We want the biggest most profitable companies in the world sending us checks while we sleep. You most won’t get rich just from owning stocks, but it’s an important part of a wider strategy. Cash Flow Quadrant is your Bible on this.

#2 The Real Crash is Missing Out. Stock market experts are always warning about crashes and recessions. It creates a lot of fear. Yes, those happen and stocks might go down for a few years, but that isn’t the real risk. The real risk is more subtle. The real risk is that the price of everything goes up, and your income doesn’t keep up. Your lifestyle declines. The vacations and dinners get fewer, and farther between. And you get angry about everything. That’s the real crash that happens over time. It’s inflation. And investing in the market, sensibly, is one of the best ways to fight back. Don’t be the Zimbabwean taxi driver.

#3 Think 5 years at a time. The stock market is safer than people realise, as long as you invest for longer durations. Over 1 year it’s a risky crap shoot and anything can happen. But stretch your time frame to 5 - 10 years and the total return with dividends has almost no probability of being negative. Key point. If you put money into the market kiss it goodbye for 5 years at least. That’s the key to success. If you think you are going to make a quick buck in the market and then you need the money back in 1 year to pay down a loan or something else, that is almost guaranteed to be a disaster.

#4 Keep bonds to a minimum. This is going to be controversial, but I increasingly think there is something wrong with bond returns. I don’t get it. If stocks have outperform bonds by millions of % and have done so consistently for hundreds of years, why don’t bond prices adjust? I mean who would buy bonds if they always underperform? In an efficient market bond prices (and yields) should adjust and outperform. But they don’t and I think it’s a behavioural anomaly. I think it’s because people are more cautious and bearish than they need to be. And that is why they allocate more to bonds than they should.

My advice; use bonds for money you need in under 3-5 years. Use it as a liquidity pool. Everything else should be in stocks. I’m 99% stocks.

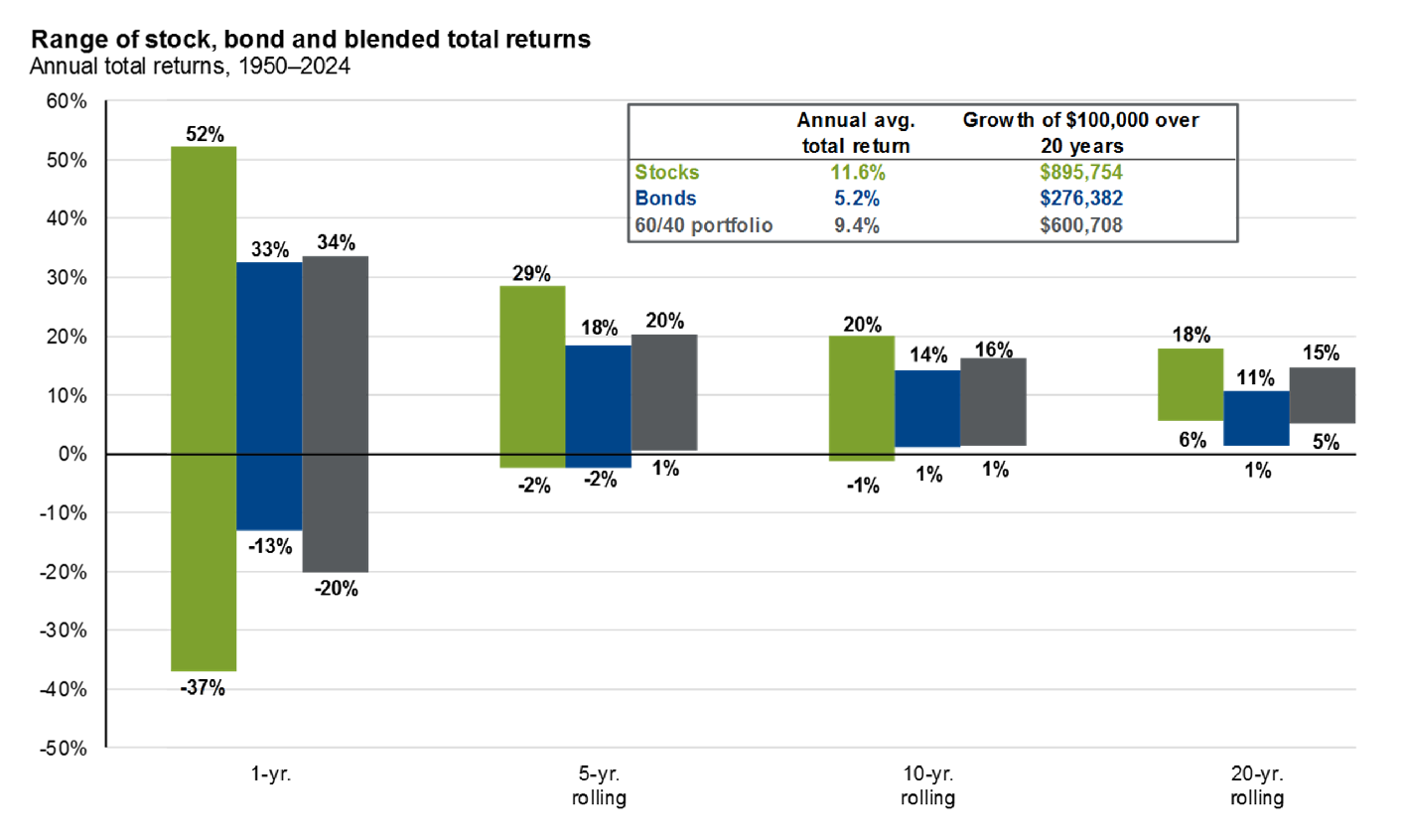

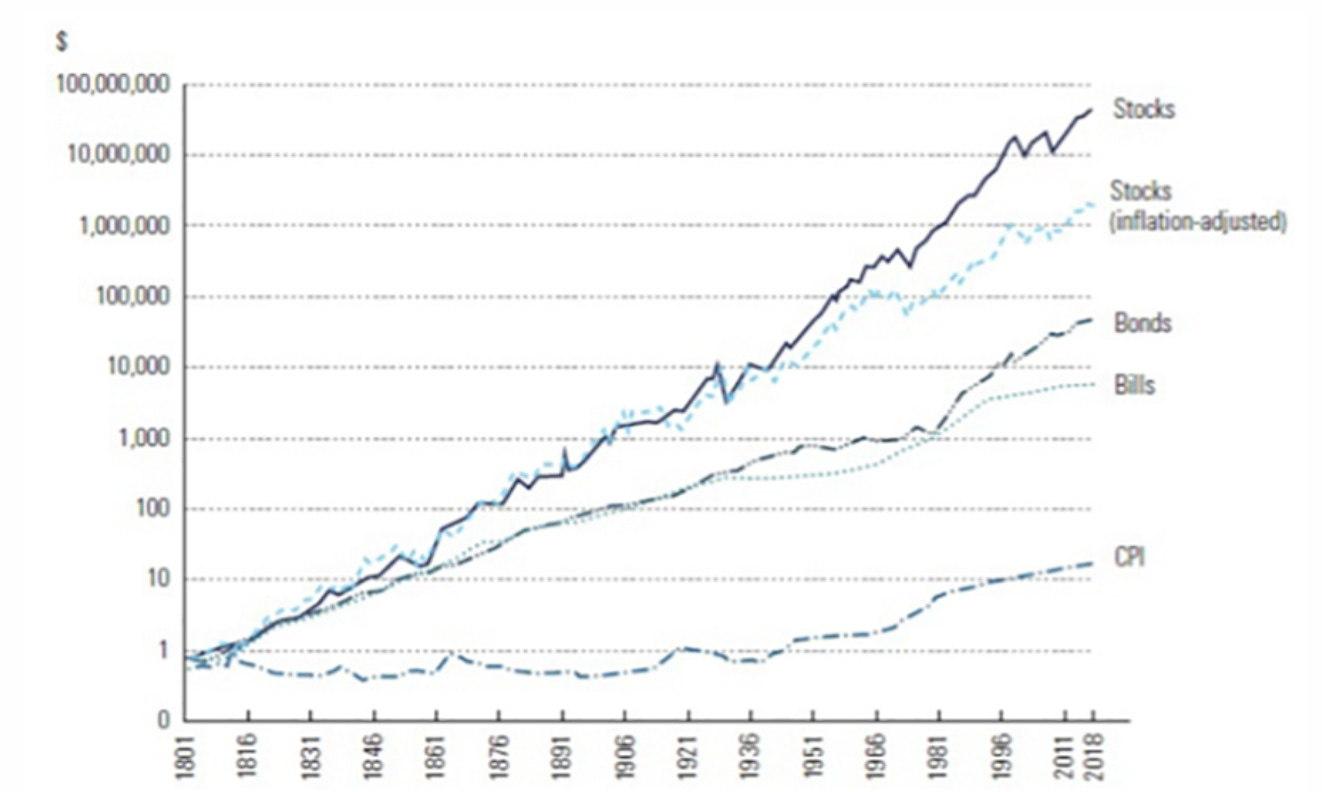

Long term returns of stocks and bonds (1801-2020)

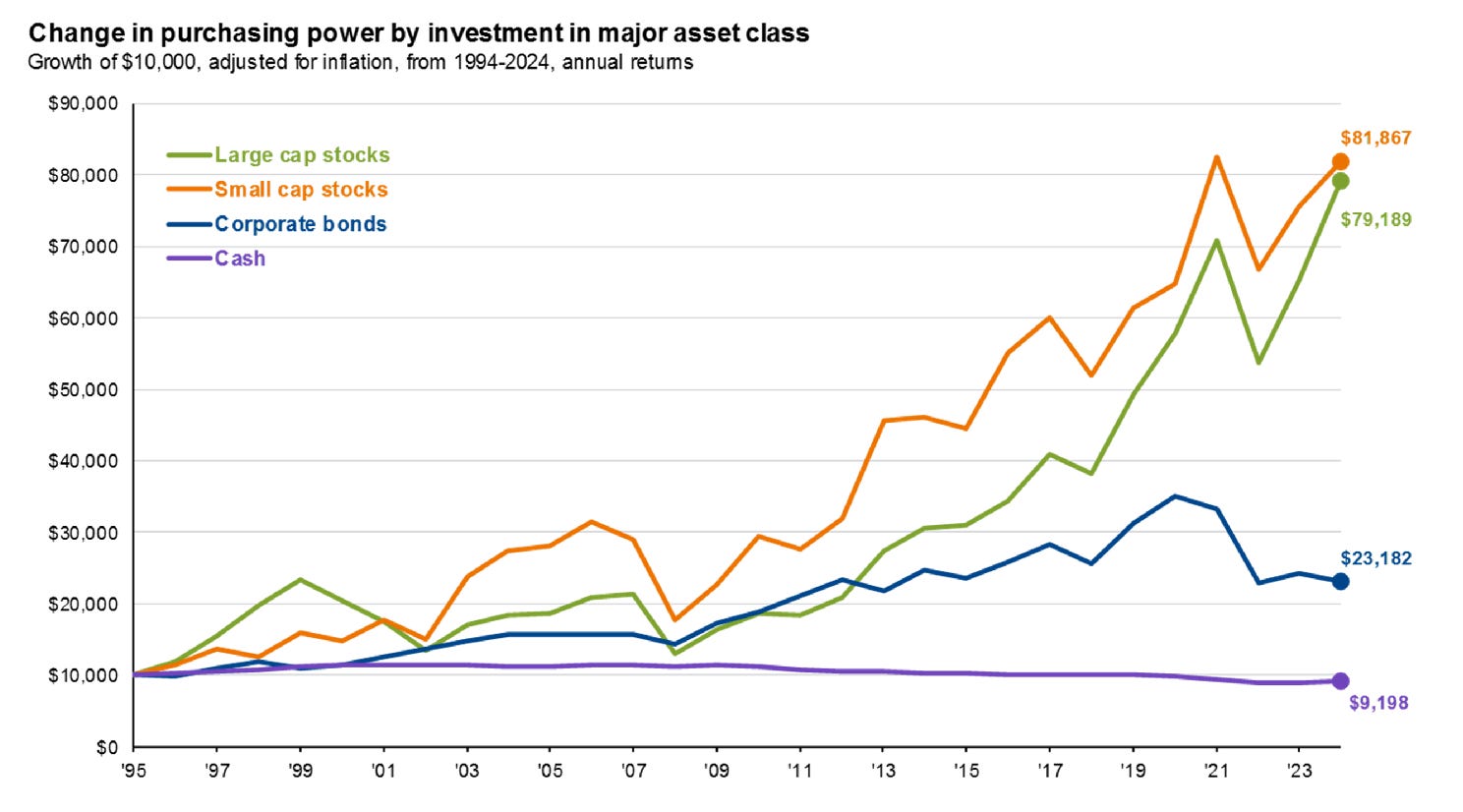

More recent returns of stocks and bonds (1995-2024)

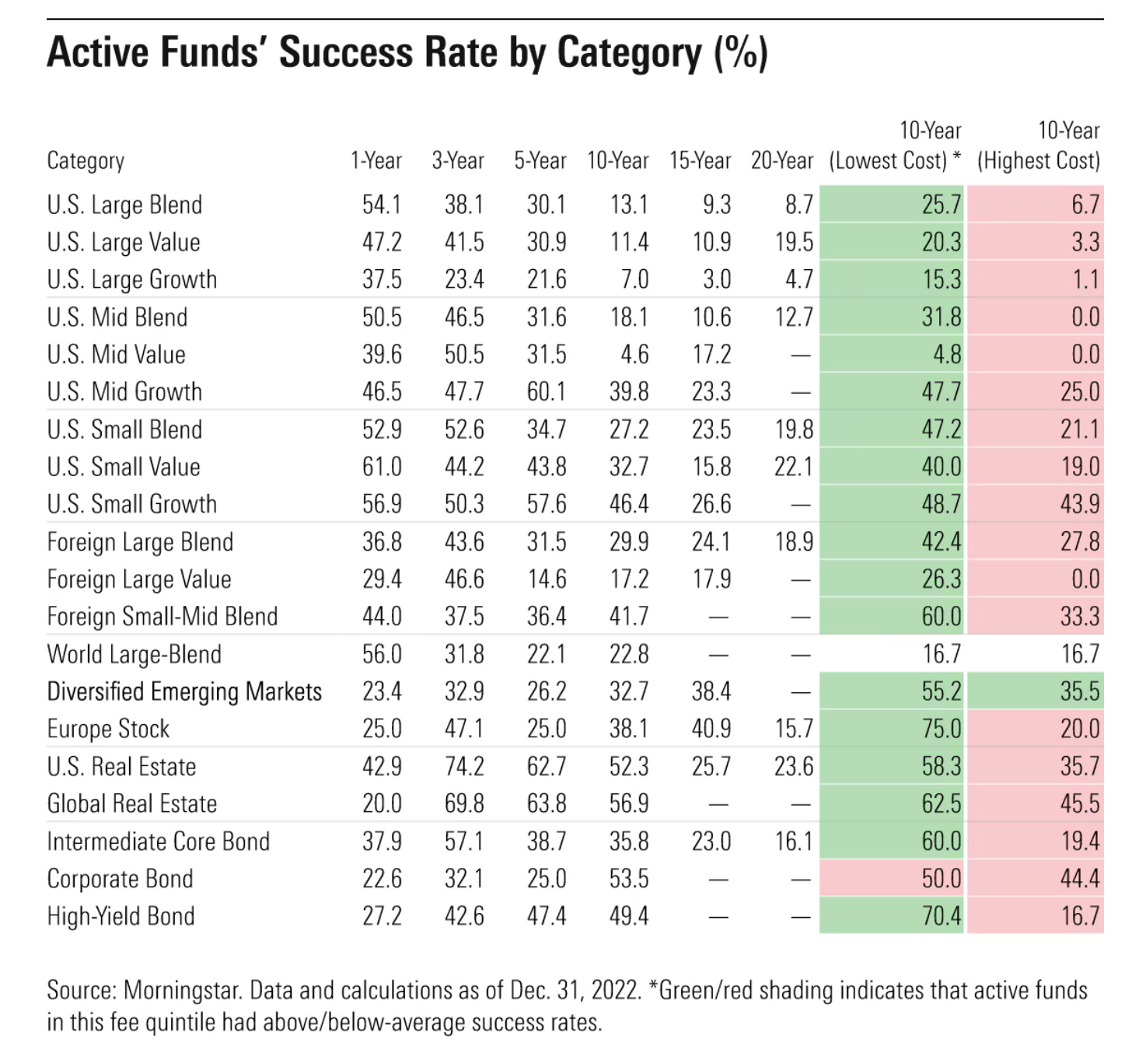

#5 Just Buy the Index. The investment industry should make the chart below illegal. Because what it shows is that over any period of time a simple low cost index fund is likely to outperform an active fund manager. Yes, there are great fund managers, but not many. That’s what the numbers show.

If you buy a simple S&P 500 index fund you aren’t missing out on anything, and actually probably doing better.

#6 The Dirty Business of Complexity. We just figured out that owning an equity index fund and doing nothing for long periods of time is your best investment strategy. Buffet says the same thing.

But if you did that, we the investment industry, would be out of business. We need you to be active so we can make fees. If you do nothing we all die. That’s why there always has to be new products, new strategies, new investment views to get you trading and generating fees. We make everything more complex than it needs to be to make money. Everyone is in on it. The fund consultants (Russell, Cambridge Associates, Albourne), the academics, the strategists, the Substack writers (even me). Understand the incentives.

#7 Avoid Gimmicky Trading Strategies. This goes with point #6. I see so many advertisements on TV for strategies to trade futures and options. It’s always some guy sitting at his computer in a nice house explaining how he spends 1 hour day on his option trading system, which sends him alert, he clicks a button, makes money, and then spends the rest of his day on his yacht.

It is so stupid and such complete garbage!!

Please don't get sucked into this. Or if you have to, just keep your losses to a minimum while you learn your lesson the hard way. Think about it. If the guy’s strategy actually worked, he would not need to make $20/month selling it to you. All these products are get quick rich distractions which don’t work.

And can I say another thing?

I have worked on several trading desks at firms over the years with many professional traders running books. And the great thing is the portfolio management software lets you see what every other trader has in their book, what they are trading, and their P&L. Not the P&L they tell you about at cocktail parties. The real P&L with every trade, good and bad. And you know what? Most of them are super mediocre, especially the longer the track record. Yes, there are exceptions like John Burbank, but overall it’s mediocre. I’m not saying good traders don’t exist, but all the data, and my personal experience say the same thing. They are rare. And if they exist, they don’t need to talk to you and sell you their strategy.

Stick with the Index funds. At least in the beginning. Master the basics. Like Mr. Miyagi.

A related post on this theme is How Conoco Changed My Life.

#8 Avoid leverage in stocks. Your big bet is to be overweight equities. That’s enough. That’s the bet. Don't add to it with leverage by trading on margin. Stocks are super volatile and the leverage is going to trip you up if there is a crash. Leverage will force you to sell, when instead we want you on offence buying. Leverage is how you have the real life ending train smashes. Stay away from leverage, stay diversified, reinvest your dividends, and your worst case scenarios aren’t that bad. Make use of leverage instead in your real estate holdings where it’s harder to get a margin call.

#8 Allocate 60—70% to US Equities. I love investing globally. I love travelling around the world and finding opportunities. It’s so much fun. But if I had to give a single mom from the Ukraine advice, I’d say allocate 60-70% to the US and don't rebalance. If the US part outperforms, which it probably will, and becomes 90% of your portfolio just leave it. Let it grow. There is a lot of inherent diversification in owning 500 of the largest, most profitable companies in the world. There is a reason they made it to the Top 500. They have a good businesses. Have some Asia and some Gold so you don’t go crazy if the S&P goes flat for 8 years (which is possible), but over longer periods of time there is something special about the US which nobody has replicated. I live in Europe and I see the difference. The US is wired differently. More aggressive, more entrepreneurial, more hustle. If you are young and ambitious go to the US. You will love it. And that’s why stock-wise it will outperform over the long-term. Asia’s also good too. I’m adding more to it. And if the US does crash, reinvest the dividends and buy more.

#9 Being in the Game is the Game. Your strategy isn’t complicated. You are going to own equities through the ups and downs and keep reinvesting your dividends. You are never going to sell. You will hear clever sayings like “You never go poor taking a profit.” But you kind of do. There are exceptions to everything, but for our diversified index portfolio we aren’t selling because here’s the problem with selling. It’s really hard to get back in. You feel clever at first, then you get frustrated and anxious as the market goes back up and you get left behind. I know. I’ve done this mistake tons of times and it’s super annoying. That’s why now I say a better strategy is to just take the beating, let the market decline (if it does), and buy more on the lows.

#10 Pay Yourself First. This goes with Pt. 9. I know how it feels when money is tight and as soon as you get paid all your money goes to paying bills. But we are trying to get out of that situation. And one part of it is making a small allocation to your investment portfolio. Even if it’s $50 it’s fine. Pay that $50 to your investment account first. And make a habit out of it. And remember you won't get that money back. It’s gone. Off to stock market land to compound. So only invest money you don’t need, which is why it’s fine if you need to make it super small. The key is your equity account is always getting inflows. These inflows plus the dividends you are reinvesting act as automatic stabilisers when the market sells off. If everything sells off 30% and you are fine. You knew it could happen, you expected it. You don’t need the money, and now you take the opportunity to get on offence and make a small buy instead. Then next week the market goes a bit lower, but a dividend comes in from your index fund and that is also reinvested at these low prices. They call this Dollar Cost Averaging. I call it always being on offence. But it helps if you pay yourself first. And yes, this comes from ‘The Richest Man in Babylon’. Another book you should read.

Oh shoot... I’m at 10 Secrets already. I still have more.

What do I do?

Let’s keep going. Here are 5 bonus secrets.