YWR: 1H Performance Review

Disclosure: These are personal views, not investment recommendations to buy or sell a security.

It’s fun to talk about stocks and have views on things, but we also have to a) eat our own cooking and b) report the results.

Dirty Dividends

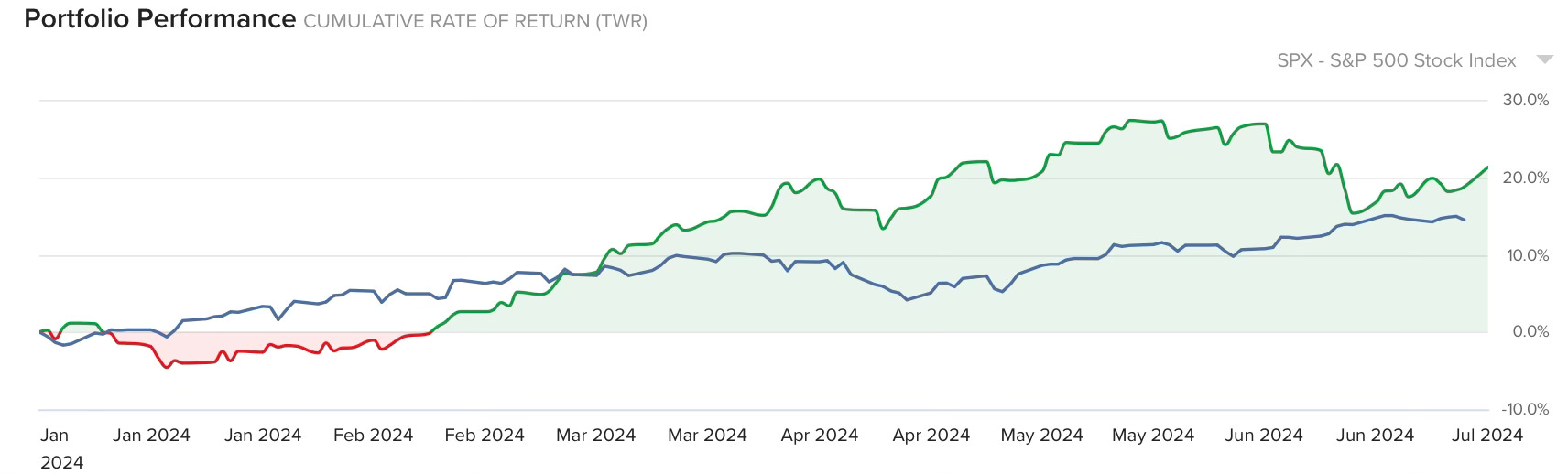

Performance

Dirty Dividends has had a good 1H, but then so has everything.

Positions

I rarely trade and the only change is that I used some of the year-end dividends in Europe to start a position in Vinci. I bought most of the position at 115/share and added again at 100. The dividend yield looks low at 4.8%, but I forecast Vinci is generating almost EUR 7bn of free cash flow (operating cashflow - taxes - interest payments) which they can use for dividends, share buybacks or acquisitions. So far Vinci been using this cash to buy more airport stakes (50% of Edinburgh Airport, and 20% in the Budapest Airport) and buying back EUR 40-145 mn of shares each week.

Underperformers

Total Energies +2.6% YTD

BP +1.3% YTD

Glencore -1.2% YTD

TSLA - 15% YTD

The energy related positions have been underperforming, but I don’t spend time worrying about them. Total and BP are generating good cash flows at current energy prices, paying dividends, buying back shares and getting ready for the big squeeze.

You know…rising non-OPEC oil demand in the years ahead, but with no change in investment. That squeeze.

Glencore shares aren’t doing much. They are taking this year and next to pay down their Elk Valley met coal acquisition. Meanwhile, copper prices have been healthy.

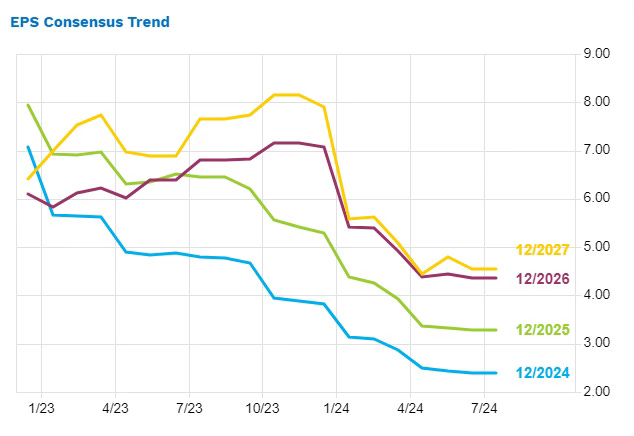

Tesla has been the stinker. Previous forecasts that Tesla would make $4/share in 2024 have fallen to just over $2/share. Previous estimates of $7-8/share in 2027 are now $4.

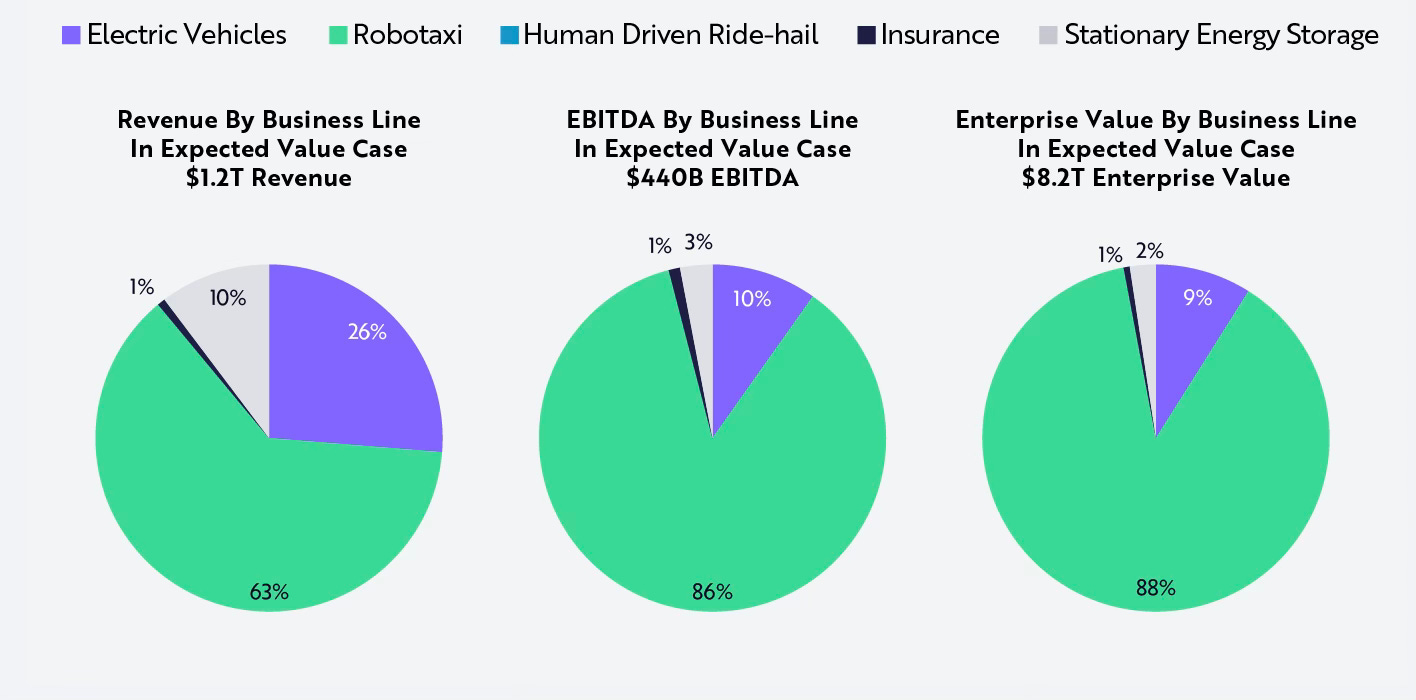

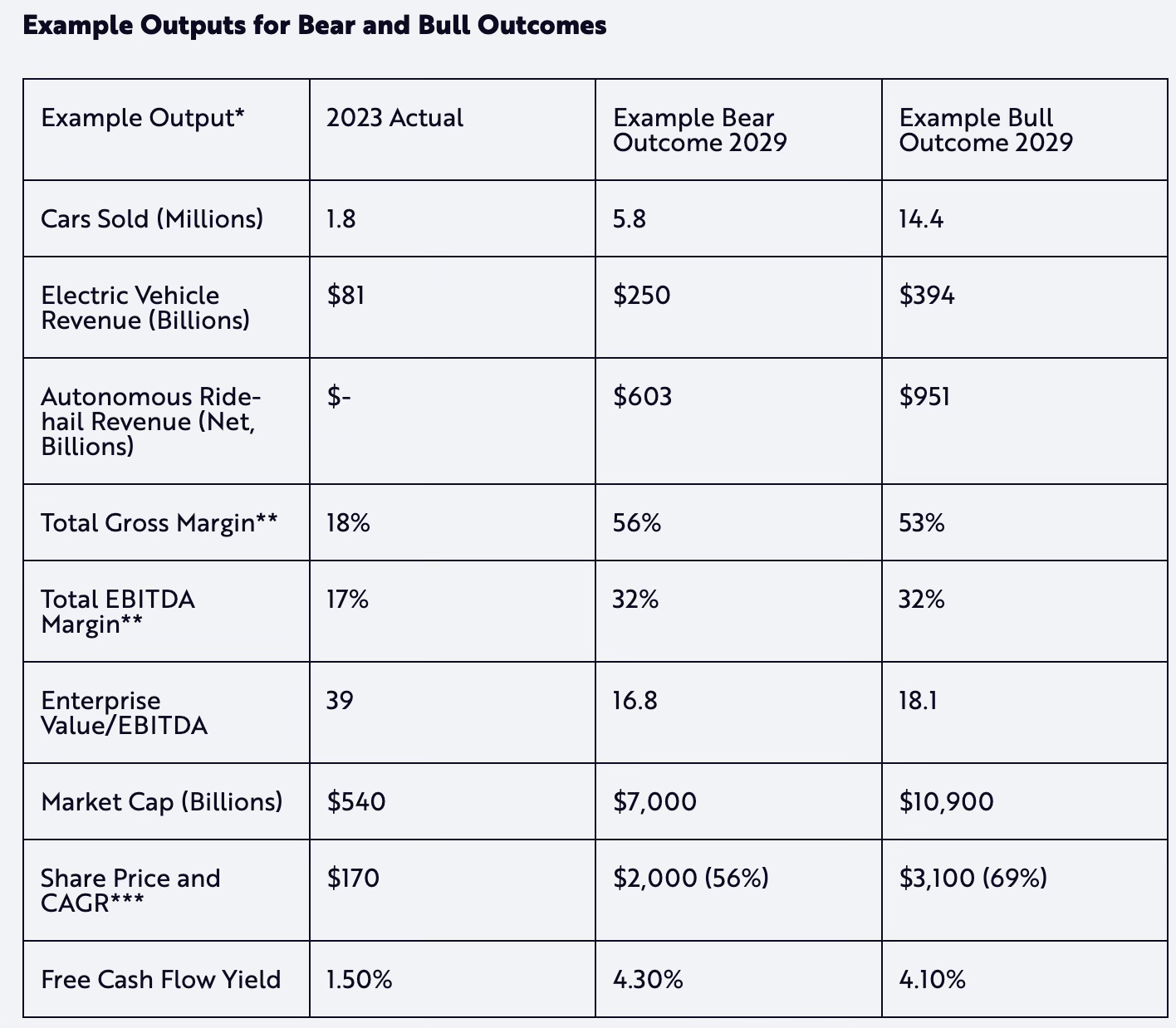

The good news is Cathie Wood says if I’m patient I will make over 10x when Tesla shares appreciate to 2,900/share. Sales of EV’s will be irrelevant because the real money making business will be robo-taxis. Robo-taxis will be 88% of the value of Tesla.

Her full Tesla report is in the reference section at the bottom of the post.

Cash Dragons

In April we launched a new theme, the Cash Dragons, and so far it hasn’t been so hot.

Positions

We’ve discussed Chinese tech stocks, LVS and Swire Properties, but so far I only have 4 positions. The valuations are less attractive than the Dirty Dividends, but these stocks are supposed to be growthier.

Baidu has been the worst performer, but to me it seems the most interesting. It has a market cap of $30 billion, is trading on 10x earnings with half its market cap in net cash. Yes, I don’t know how much of that cash they can get out of China, but still….

Baidu’s Ernie 4. 0 Turbo AI model supposedly has over 300 million users and Apple is going to use Ernie for AI in their Chinese iPhones. Meanwhile, OpenAI says they have over 100 million users….and is valued at $80 billion. They are almost paying you to own the OpenAI of China. I’ll put the Baidu model in the reference section. The negative is their internet search business is ex-growth.

The Third Plenum

Every five years China holds a Plenum, their conference to finalise economic policy . On July 15-18 China is holding its Third Plenum and Xi is promising a series of ‘major measures’ to improve growth. There is even talk that this will be a historic plenum, along the lines of the 1978 plenum.

But, as usual nobody cares. Another gradualist Chinese economic policy that might be sensible, but does nothing to move the stock market.

Still, it’s interesting. We have Chinese stocks at historically low valuations, a major policy meeting in 2 weeks and signs of economic momentum.

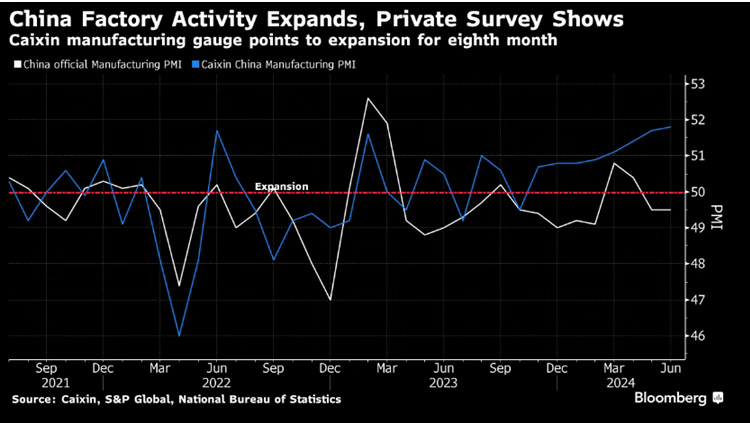

The number of China stocks scoring highly in the YWR Factor Model has jumped dramatically.

A potential improvement in manufacturing sentiment according to Caixin.

Macau gaming 1H revenues are +41% yoy, although June was +17% yoy, which was seen as slightly disappointing. Gaming revenues are still tracking below 2019 levels.

Also some signs of improvement in secondary sales of Chinese real estate as the stimulus measures and lower interest rates take effect.

‘Big wave’ of buyers: China’s property market sees signs of recovery

Real estate experts say the government’s recent stimulus measures are taking effect, at least in the megacities of Shenzhen and Shanghai

Some property developers have stopped offering special incentives to buyers, thanks to a surge in demand

https://macaonews.org/news/greater-china/china-property-market-recovery-shanghai-shenzhen/

Have a great 4th of July for me. I’ll make my famous burgers, but it won’t be the same without bottle rockets and jet skis at the lake.

Erik

Reference Material