YWR: 6% 10 yrs

I attended a macro ideas call last week with my peers and it left me thinking there was something wrong with me. Like I was from Mars.

There were six of us. And I’d say where we differed most was on China and Interest Rates. On China I see a beast in the making. Everyone else saw it as an uninvestable mess which would perpetually disappoint.

Then on rates I said 10 year yields are going higher, while the consensus view was interest rates will fall. And the only question was how fast the Fed needs to cut.

So why am I 180 degrees the opposite of sensible fund managers?

Here are 6 reasons I think 10 years are going to 6% and will be the surprise of 2025.

Let’s start with a simple one.

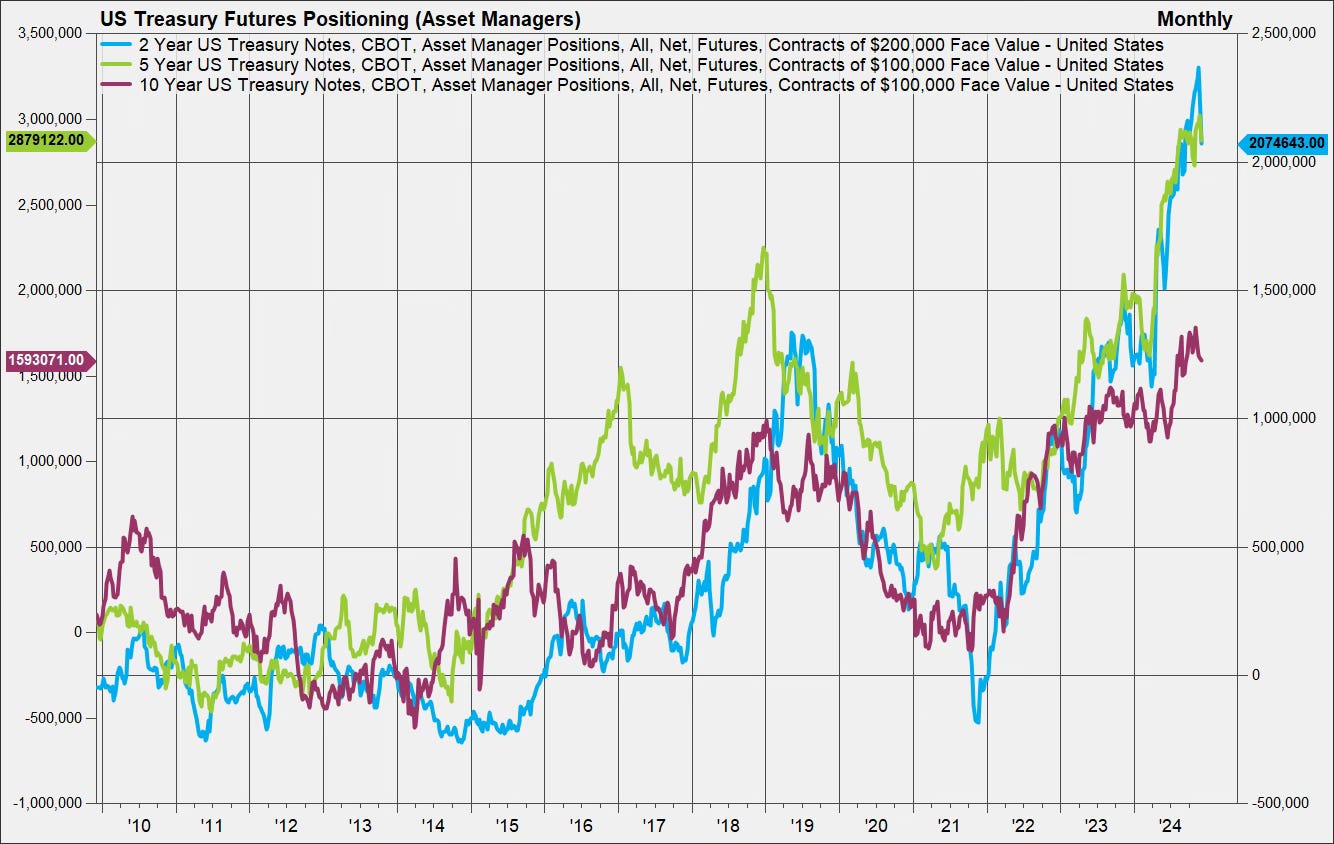

#1 Positioning

According to CFTC data asset managers are record long Treasury futures. Positioning in 2’s and 5’s are at especially high levels, but it’s in line with the view the Fed will cut rates. 10 yr futures positioning is also high.

Yes, I’ll take a grain of salt that it’s CFTC data, it’s hard to classify all the players correctly, and there is always someone on the opposite side of every trade (all positions net to zero). And I’ll give you that asset manager positioning could have an upward bias over time as the industry grows, managers use futures more, and investors are attracted to higher rates.

I’ll give you all that. But it still looks like everyone is positioned one way on this debate. The macro call was the same way. The contrarian call is asset managers are positioned exactly the wrong way.

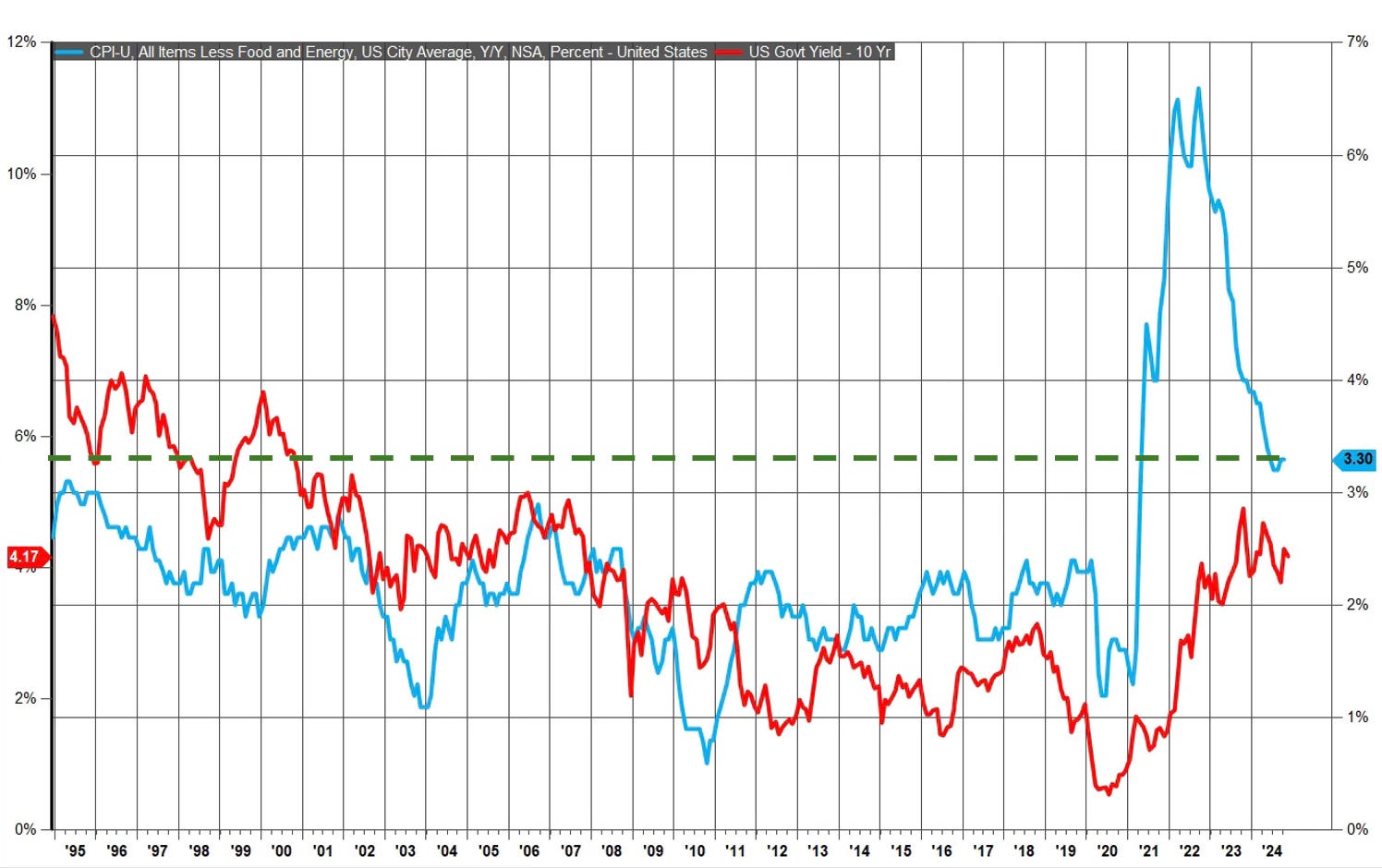

#2 10 year yield - CPI relationship

This isn’t super scientific but it’s a chart of 30 years of the relationship between 10 year yields and CPI (less food and energy). Note the scales are different. CPI on the right, yields on the left.

Look back to the late 1990’s when CPI was in the 2.5% range (Blue-line, RHS). 10 year yields were in the 5-7% range (Red-line,LHS).

If we go back to that relationship where 10 years return 3% above inflation (is that called term premium?) it gives us a 6% target yield. Not so crazy. And yes, it assumes 3% CPI is sticky.

We’ll get to the Dickersons in Boise and why they drive 3-5% inflation.

#3 Equities are pricing in a 6.6% 10 year.

There is a view ‘the bond market is always right’ and equities are the dumb money.

We look at the S&P 500 at $6,000 with a 4.6% earnings yield and think it looks crazy.

Why take all that risk for 4.6% earnings yield when you can get 4.3% on a 10 year?

I think it’s the opposite. I’m going to flip it around and argue equities have it right.

Bonds are the dumb money. Let’s look at the math.