YWR: Anatomy of a Private Equity Train Smash

The more I look at Private Equity the more I think the most important driver of investment returns for the next 10 years will be avoiding the PE/VC train smash and all its 2nd derivatives.

Look at the growth of this industry. As recently as 2017 it was only $5.4 trillion. Then it rockets at an 18% CAGR for the next 6 years to almost $15 trn.

Returns boom which causes more money to flood into the asset class.

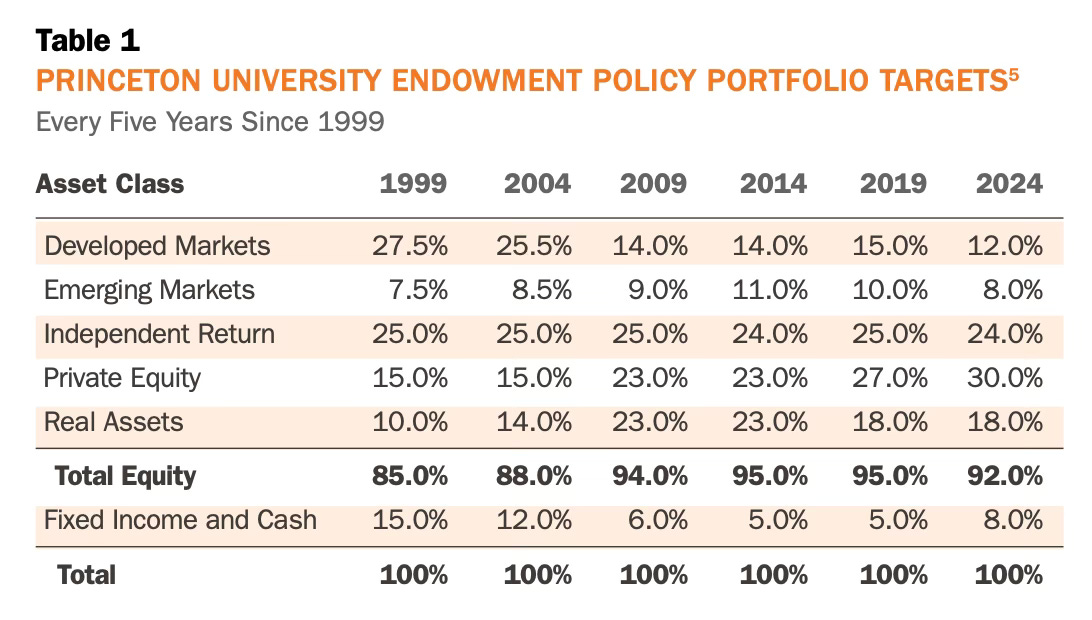

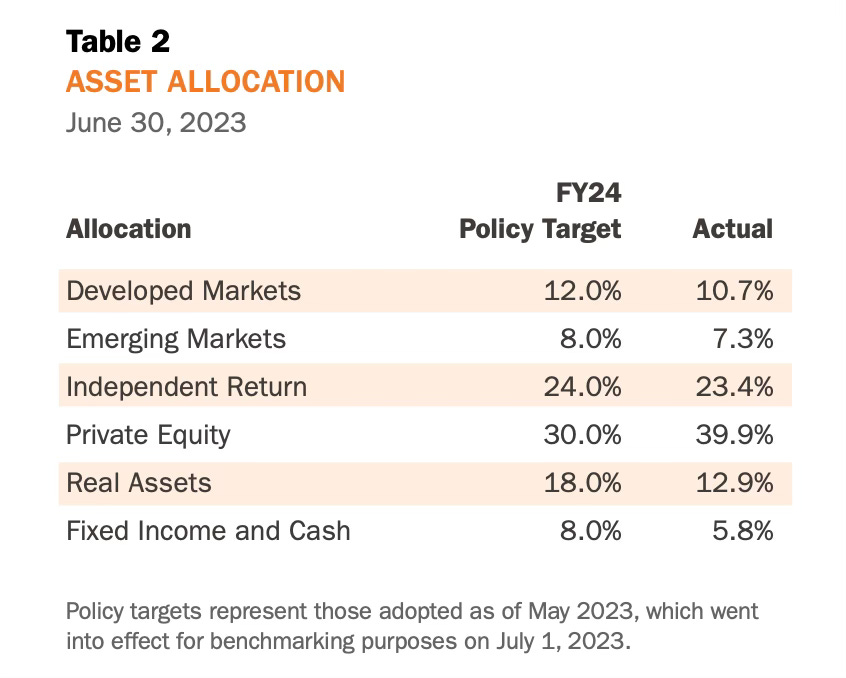

Endowments like Princeton eagerly increase their PE allocations from 15% in 1999 to 39% by 2024.

Dry powder reached $3.9 trillion!

Buyout funds accounted for 31%

of all dry powder in 2023

3.9

3.5

3.2

3.0

2.5

2.3

2.0

1.7

1.5

1.4 1.4

Other

Distressed PE

Secondaries

Direct lending

Infrastructure

Growth

Real estate

Venture capital

Buyout

2005 06 07

08 09

10

12

14

16

18

20

22

11

13

15

17

19

21

23

Notes: Buyout category includes buyout, balanced, coinvestment, and coinvestment multimanager funds; other category includes fund-of-funds, mezzanine, and hybrid; discrepancies in bar heights

displaying the same value are due to rounding differences

Source: Preqin")

But like all trends, there are cycles and I see the set-up for a big unwind which will play out for years.

Live by Zero %. Die by Zero %

The Rate Pin

The Snake eats its Tail

From $14 trillion back to $10 trillion

This is Africa

Beware the Second Derivatives

Is your Life Insurer a PE Fund?

Reference Documents

The Key Assumption: Before I go further, I want to stress my key assumption in this outlook is that interest rates are more likely to rise than be cut. US 10 years go to 5-5.5%

And if so, this is how it likely plays out for Private Equity. Alternatively, if you think US 10 years go back to 3% this will all seem too negative.