YWR: Bad News, Good News in the European Banks Trade

In 2023 we said the European Banks trade would have 2 stages.

At the time the Ukraine War had just started and European bank CEO’s anticipated a recession in Europe. They were worried about high energy prices and the effect of higher interest rates on their loan books.

Our view was these CEO’s were being way too bearish and didn’t see how much money they were about to make. Net interest margins would expand and the loan book would be fine.

This would be Stage 1.

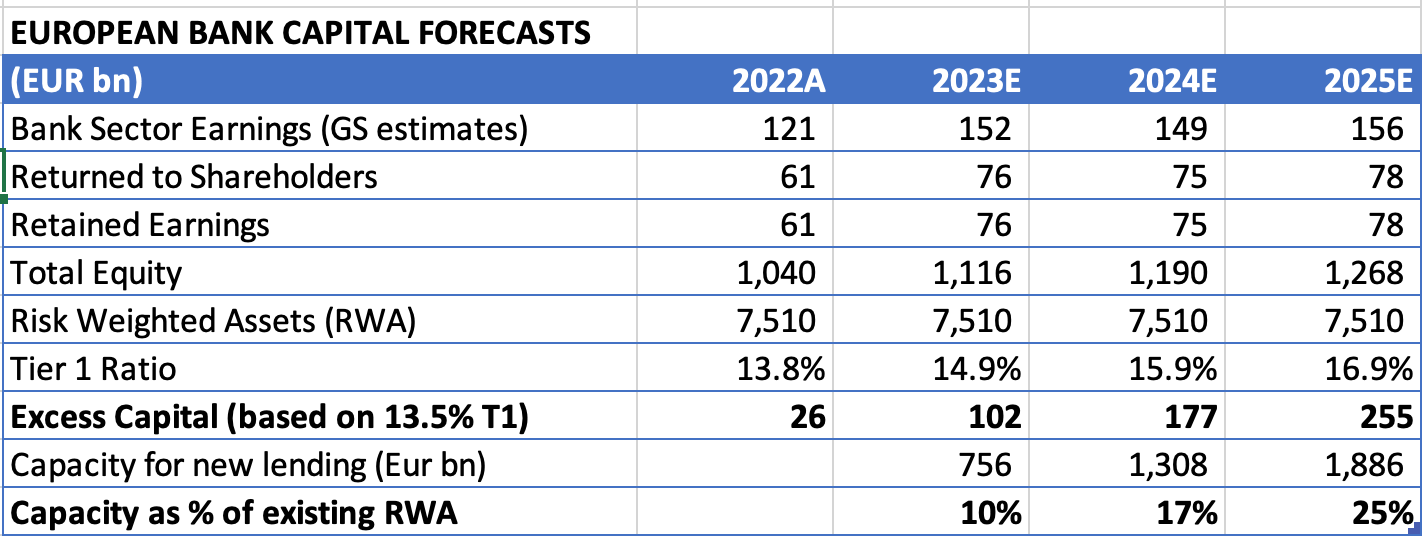

Later, sometime around 2025, after several years of record profits these bank CEO’s would get bullish again and start to lend. Systemwide bank lending would be positive for European economic growth. We called this What do you do with EUR 250 billion? (in excess capital).

The switch to loan growth would be Stage 2.

We bought Barclays, Santander, Commerzbank and Unicredit.

So it’s 2025. How’s the view going?

Mixed.

Let’s do the ‘Bad News’ first.

The ‘Bad News’

The bad news is European bank CEO’s have become too comfortable with a banking version of Conoco’s ‘shrink to grow’.

The model of the last 3 years, which they are all doing, is to be super stingy with lending to customers, keep the balance sheet flat, and milk the customers for lots of fees instead. Also, keep costs flat to get operating growth without much top line growth.

This nice thing about this combination is it generates lots of money without using regulatory capital. You also don’t get loan losses. Next take the cash flow and buy back shares to turn 2-3% growth into 10-15%. Grind it out over years with super strong cost control, capital management and share buybacks. Low volatility, and low risk with lots of capital returns. Shareholders love it.

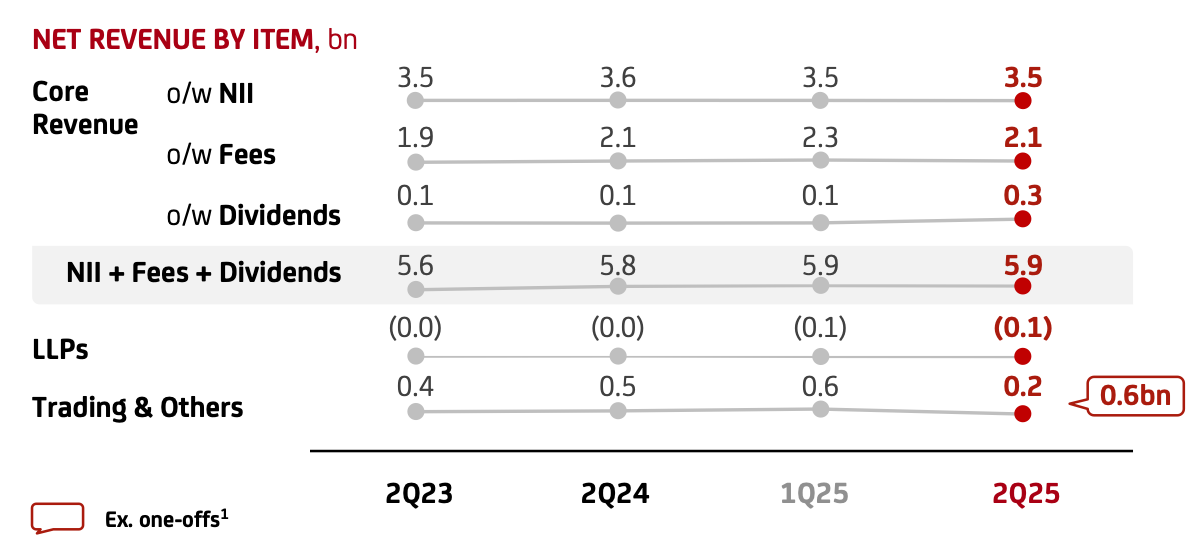

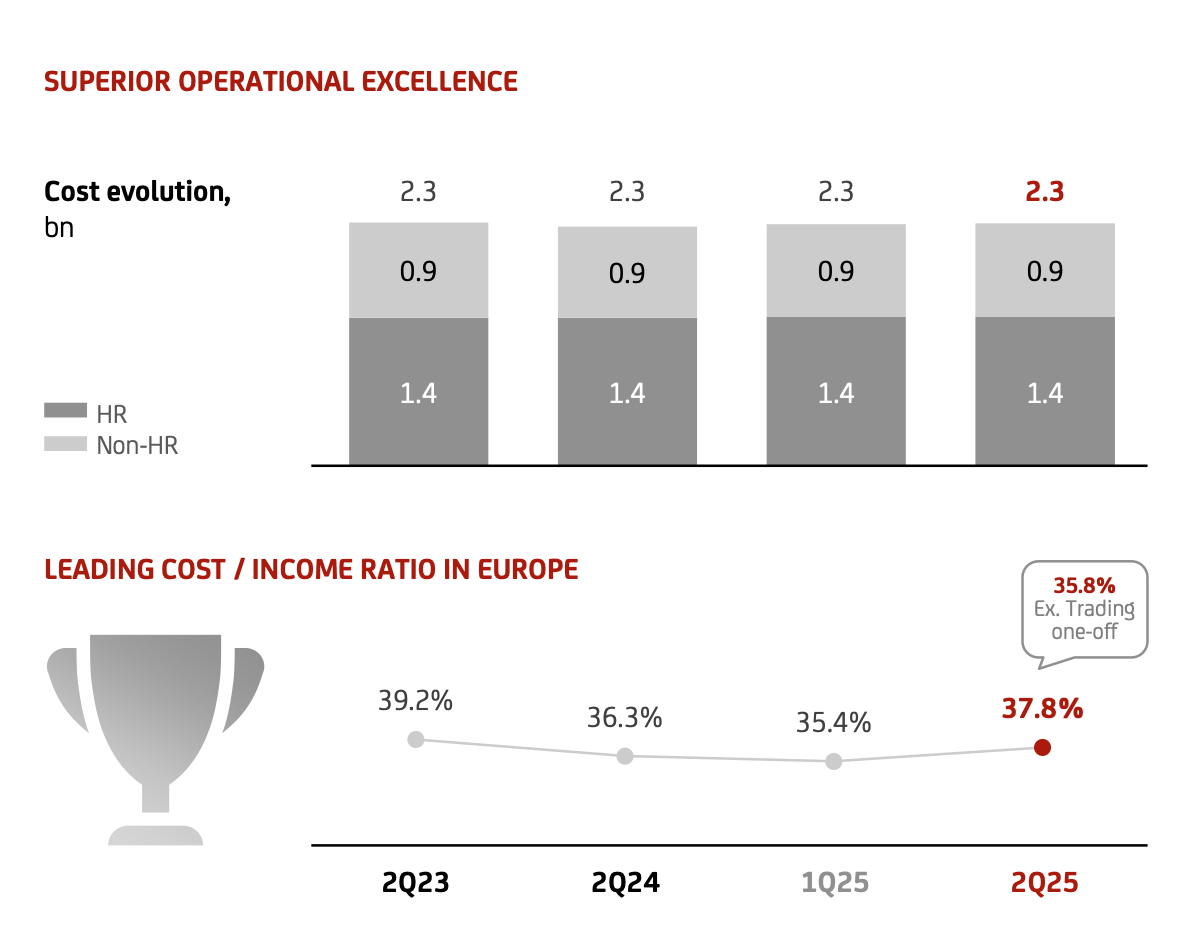

Here’s Unicredit’s version of this.

Only EUR 300mn of revenue growth over 2 years (NII+Fees+Dividends)

But costs flat and an amazing sub 40% cost income ratio.

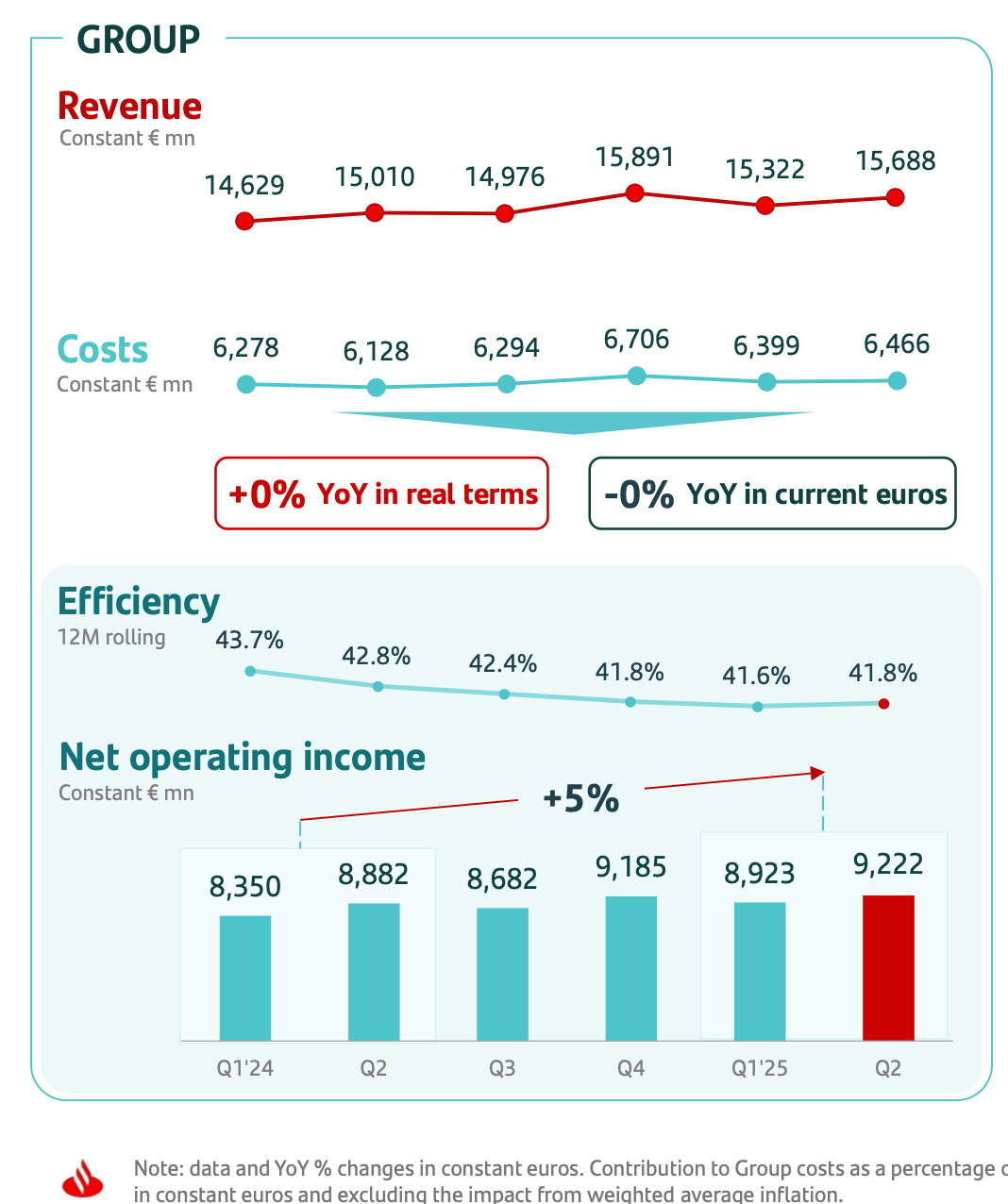

Here is Santander’s version.

7% revenue growth over 5 quarters with 3% cost growth = 10% operating profit growth (Q1 2024 to Q2 2025).

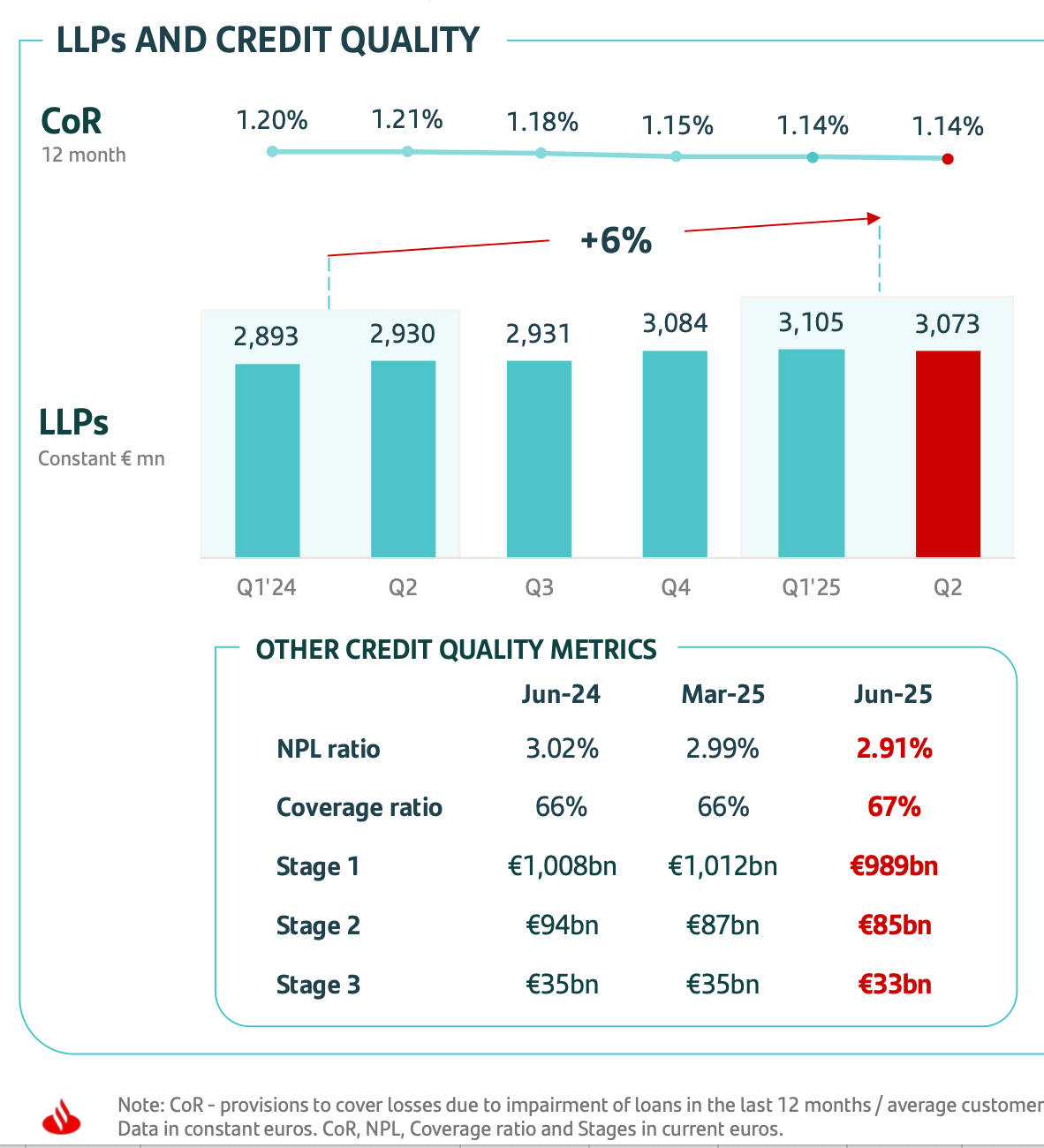

Credit costs in this model stay low, which has been the big surprise for the sell side which had been modelling in a recession.

Because loans aren’t growing and Tier 1 Capital Ratios at 14-16% are above the regulatory requirements (10-12%) you can distribute all these earning as share buybacks, which manufactures more EPS growth, and makes the share price go up.

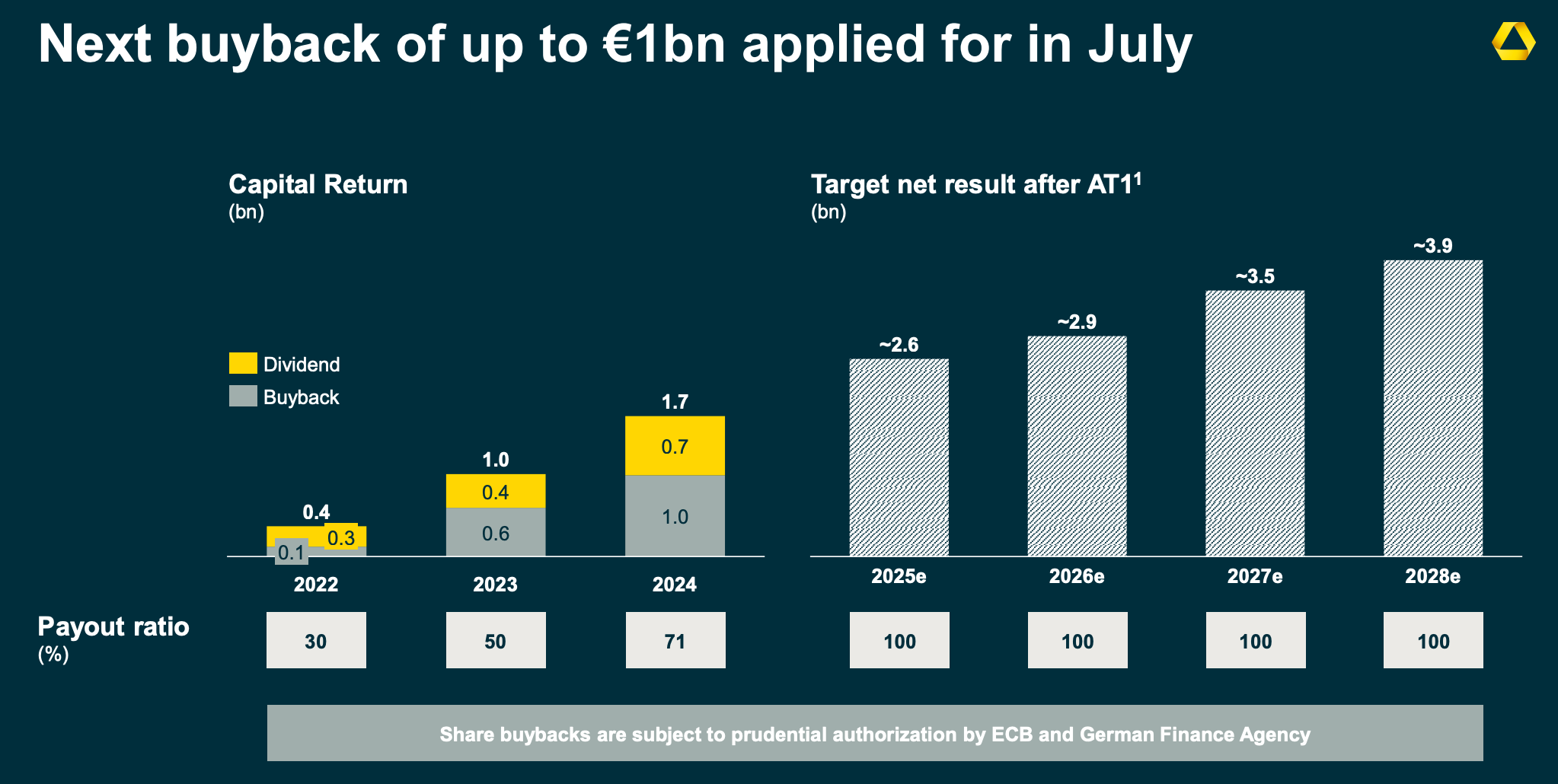

Commerzbank went from a 30% payout in 2022 to 70% of profits in 2024, and plans to payout 100% of profits for the next 4 years (2025-2028).

And that’s the problem.

That’s the bad news.

The banks have gotten too comfortable with Stage 1.

They don’t see this stage has run its course.

The net interest margin expansion is over.

And the run up in bank share prices means the share count won’t decline as much in the future. Buying back shares at 9x earnings is a lot less accretive than buying them at 5x.

And you remember the EUR 250 bn in excess capital we were supposed to have for loan growth? They paid much of it out in dividends and buybacks.

The irony is everyone is piling into European Banks right as this model is reaching a dead end.

And is the Stage 2 European growth story over too?

What’s the good news?

The Good News

Good news #1. The share prices have gone up a lot and we’ve made money.

Good news #2. People change their minds.

It’s the secret to sales.

Yes, bank CEO’s are thrilled with this capital light model of consistently grinding out earnings. Their share prices are going through the roof. They tell us this is the model for the future.

And to some extent it is. The scars from the post-GFC regulatory torture run deep.

But I anticipate the banks will change their minds and start to get more interested in loan growth and risk taking.

There are already signs of this.

I see in the slide decks much more optimistic outlooks on the European economy. They’ve upgraded their GDP forecasts. They aren’t predicting recessions anymore.

And the CEO’s are brimming with confidence. You can see it in how they present. The banks are humming and loan losses are surprisingly low.

But in the background I imagine the CFO’s with their spreadsheets doing the numbers and realising share buybacks are not going to drive growth from here. I imaging these CFO’s quietly tapping their CEO on the shoulder and showing them they need to grow the balance sheet too.

So the math says balance sheet growth needs to happen.

Also the tone from the Central Banks is changing. For the last 15 years the message from the regulators was how much they hated the banks and how they could never take risk again! It was one new capital requirement rule after another. But times are changing. Memories fade. A new tone is emerging. Maybe everything isn’t about ‘regulations’. Maybe the economy needs to grow too.

From the Barclays call:

And then on capital, as I said, that is part of growing the economy and growing the banking system. Now, the Bank of England Governor made another point last week at the Treasury Select Committee where he said there's no trade-off between financial stability and growth. He's absolutely right. Financial stability is a necessity, but not all regulation necessarily contributes to financial stability and that's where the debate is to be had. Which regulation is excessive, superfluous, gilding the lily, in the whole capital framework? And can you relax some of that regulation and improve growth? I'm optimistic for those outcomes.

That’s central bank double talk for maybe we over did it on regulations and killed economic growth. Maybe it’s actually a good thing if banks lend more.

And I see the green shoots of growth and risk taking in the presentations.

Barclays is targeting £30 billion in asset growth in the UK specifically in business loans and mortgages. Not a big number, but the first time I’ve seen a loan growth target.

Commerzbank is talking about 8% loan growth in German corporates.

Santander is ready to grow their European auto loan book if rates decline further.

Unicredit is making acquisitions (Alpha Bank and Commerzbank).

In summary, if the ECB or Bank of England reduce interest rates further the banks are teed up to lend.

I’ve moderated my expectations for asset growth, but am modelling in that bank balance sheets start to grow slightly in 2026.

Where do we go from here?

Do the banks still look interesting?