YWR Bank Masterclass

You should be proud.

Word is spreading that YWR investors are some of the best.

It’s great we’re getting recognition, but if we’re going to be the elites of investing, we need to up our game. We can’t always talk ideas. Periodically, we need to train and build our skills.

Which is why this week we are going to do a mini bank analysis class using the Unicredit Q1 2024 results as a working example.

This is a ‘mini’ class. We are not going into everything and not covering US bank reporting. The business model is the same, but the reporting is more complicated with mark to market of everything (mortgage servicing rights for example). To me this just adds confusion.

There is a quiz at the end. I’ve also provided links to the reference material.

And if you are a bank expert and want to add comments or critique anything please do. It makes us better.

Lesson 1: Modern Banking Balance Sheets

The modern bank’s balance sheet is complex with a greater proportion of marketable securities than in the past, where bank primarily just made ‘loans’.

As we see below loans are only 488bn of Unicredit’s 811bn balance sheet. Loans includes loans to customers interbank loans, deposits at central banks and repurchase agreements.

Then on top of loans there are trading assets (Financial Asset at Fair Value), cash and other assets.

You can think of a bank buying a corporate bond for its balance sheet as kind of the same as making a loan, except that the loan is a tradeable security. In a way all of the assets are loans. Cash deposits at other banks are loans too.

On the liability/funding side of the balance sheet there are customer deposits, deposits from banks and repurchase agreements. Banks also fund themselves by issuing debt instruments.

Finally, banks are funded with equity. For Unicredit equity is EUR 66bn or 8.1% of assets.

Retail deposits are generally less expensive and stickier (ie slow to move if they is a banking problem), which is nice. But retail deposits are more work to attract and often come with the cost of running a retail business. Wholesale deposits are nice in that you can borrow in large size without a branch network, but the negative is they are highly price sensitive and move quickly at the first sign of problems. Leasing companies are often 100% wholesale funded, which is why they can quickly blow up.

Loan/deposit ratios are not as important as they used to be although you still like to see them at less than 100%.

Lending spreads are also important, but not the whole picture the way they used to be. The bank earns net interest income on everything (loans, bonds, trading book assets, deposits). And they pay interest on all the different ways they borrow money.

Net interest margin is the key metric for this and changes here have massive effects on bank earnings.

net_interest_margin = (interest_income - interest_expense)/(avg_assets)

There is no interest expense for equity. This is one of the ways banks benefit from higher rates. Banks also don’t pay interest (or very little) on current accounts (US term is checking accounts). So at least 2 of the liability items have no interest expense.

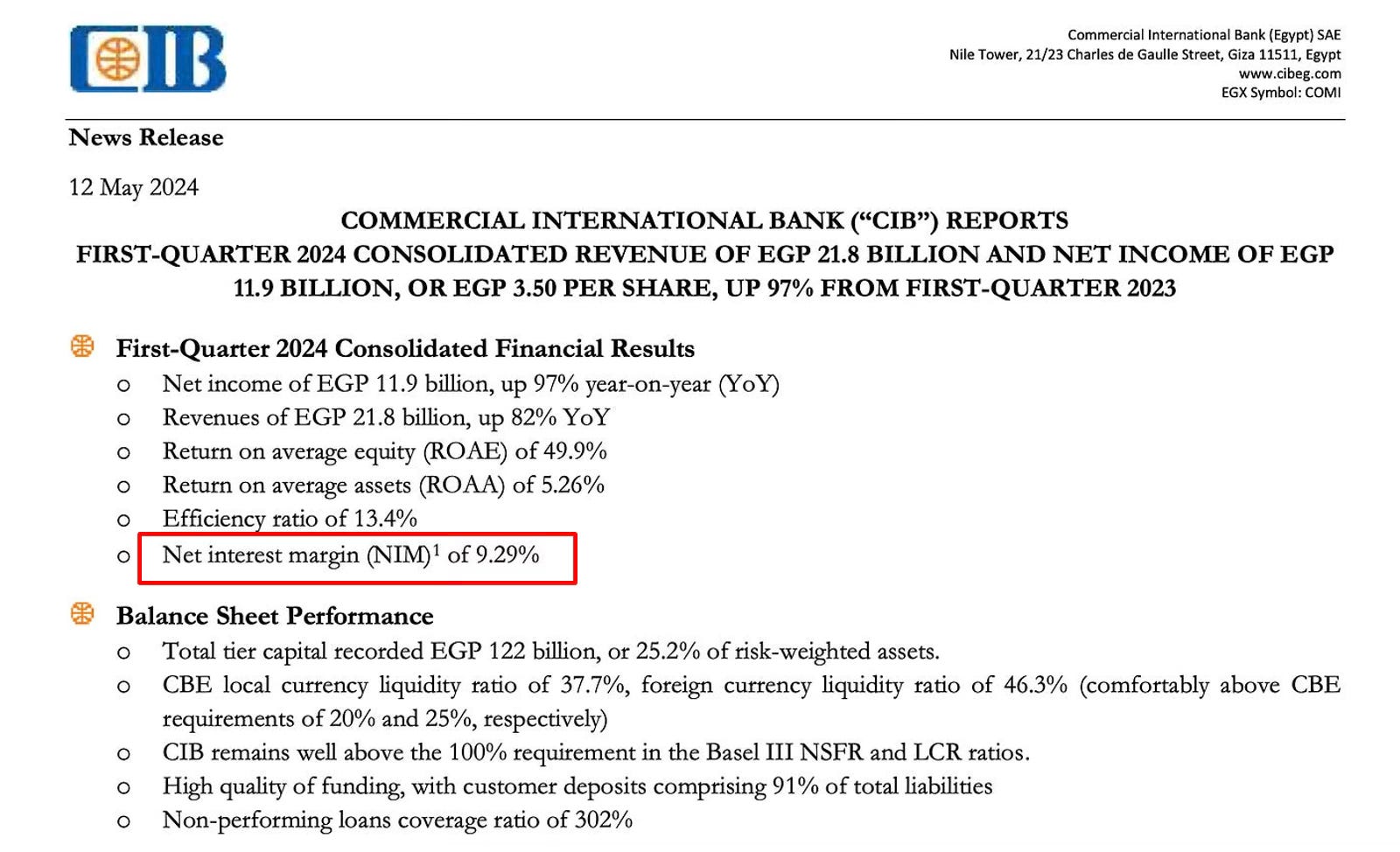

If someone wants to debate you on whether high interest rates are good for banks point them to CIB in Egypt where interest rates are 27%. CIB is earning a NIM (net interest margin) of 9.29%. And the ROE is 49.9%. That is literally a money machine.

Unicredit has a net interest margin of 1.75%

Lesson 2: Capital Ratios

Capital ratios at banks have been a big topic since the GFC, but the issue is pretty much put to bed. If anything regulators see they might have overdone it and there is room to loosen the requirements.

The most important capital ratio for banks is the ‘Tier 1 Ratio’ or ‘Core Tier 1 Ratio’. ‘Core Tier 1’ is the most important and is shareholder’s equity. Tier 1 can include preferred shares or highly subordinated bonds (AT1’s).

The Core Tier 1 Ratio, (sometimes abbreviated as CeT1) is Core Tier 1 capital divided by a bank’s risk weighted assets (RWA). We will explain RWA’s below.

Core_Tier1_Ratio = shareholder_equity/risk_weighted_assets

Pre-GFC the minimum Tier 1 ratio was 4% and banks generally carried 6-7% Tier 1 ratios (see chart below). Then post GFC there were multiple revisions to the appropriate capital requirements for banks and how to calculate all the ratios (BIS II and BIS III).

Post GFC the required Tier 1 ratio is now 10-12% with most banks holding 12-14%. Technically, the required Tier 1 ratio is 6%, but there are multiple buffers which get added on depending on the complexity of the bank and whether it is considered ‘Globally Significant’. Plus, banks are nervous of getting involuntarily put into receivership, so while the official number is a 6% Tier 1, in practice it’s at least 10%, and Europeans operate like 12% is the number.

Lesson 3: Risk Weighted Assets (RWA)

Unicredit has EUR 811bn in assets but EUR 280bn in ‘risk weighted assets’. Each of the EUR 811bn in assets has a risk weighting depending on the class of asset, the level of risk, and the counterparty. It can get complex, but here are some examples.

Cash at a central bank and OECD government bonds (Italian government bonds for example) have a risk weight of 0%. So they add nothing to Unicredit’s RWA.

A $10bn deposit at a AAA rated bank might be risk weighted at 20% (EUR 2bn).

EUR $10bn loan to a BBB+ weighted corporate would be risk weighted at EUR 7.5bn (75%).

These risk weighted assets are added up to create a total risk weighted assets (EUR 280bn) and Unicredit has to have equity > 12% of this number (EUR 33bn).

Below is a table or risk weightings from the BIS.

Banks grow their RWA’s when they add more loans or trading assts. Unicredit is a unique case where the are reducing RWA’s (EUR 299bn down to EUR 280bn). This can also be done by switching assets into lower risk buckets (for example sell corporate bond, buy T-bill).

One of the BIS III reforms is additional RWA’s for operational risk and market risk, which you can see in the slide below. Basically, BIS hits you with extra capital requirements if you are an investment bank trading a lot. Another post-GFC innovation.

Risk Weighted assets can change because of the bank adding or selling assets (portfolio management), but also due to changes in economic outlook (probability of default). RWA’s also change due to regulatory rule changes.

Because a negative change in economic outlook can quickly increase a bank’s RWA’s and therefore its required capital, banks like to run big buffers so they don’t get into regulatory trouble.

Lesson 4: Asset Quality

A Non-Performing Loan (NPL) is a loan which hasn’t paid interest for 90 days. If a loan isn’t paying interest a bank should make a loan loss provision against it.

But ‘NPL’ is not an IFRS accounting term.

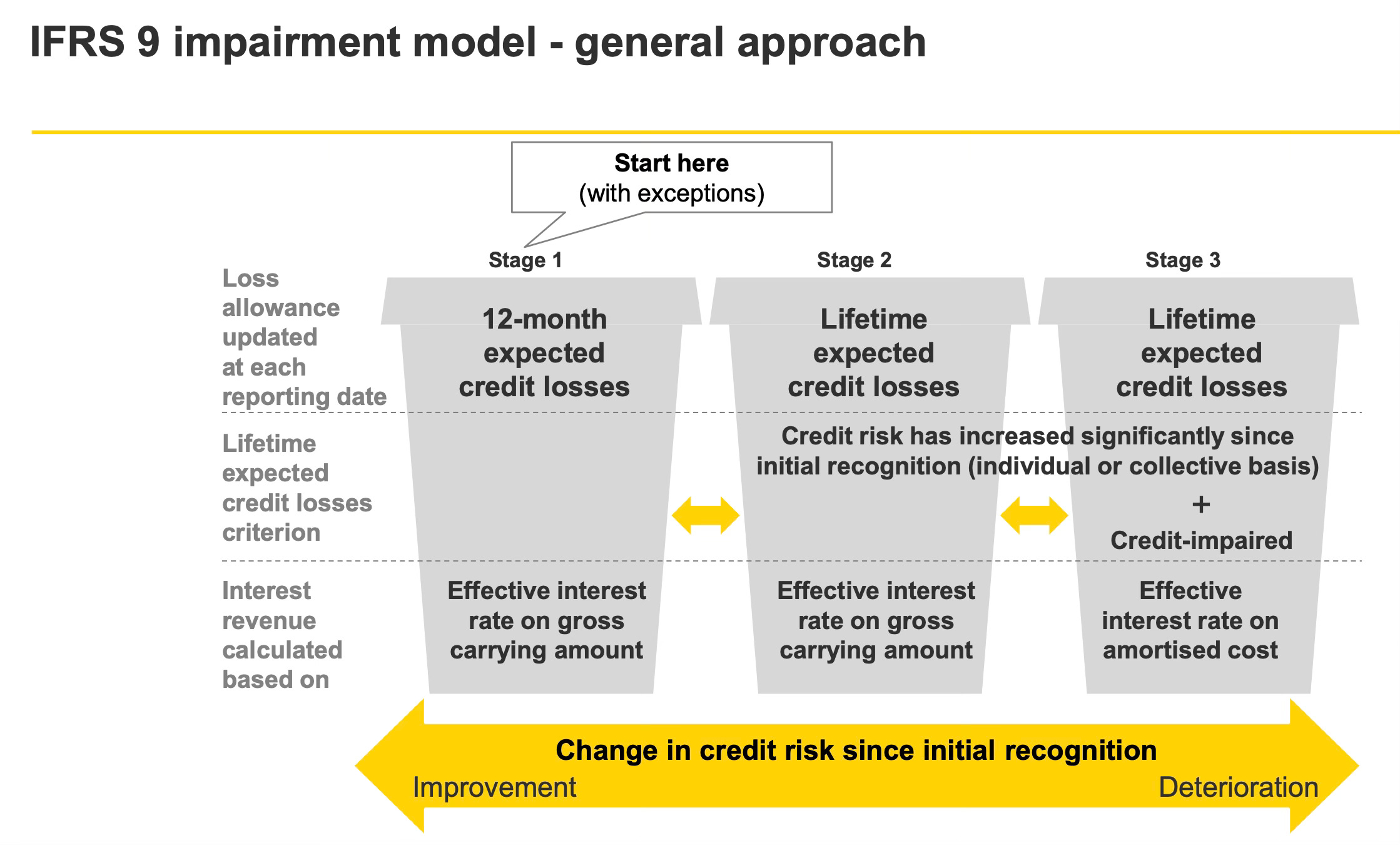

In 2018 the IASB implemented IFRS 9 for the valuation of financial assets. It’s a different methodology and it took some getting used to.

TLDR. IFRS 9 segments assets into Stage 1, 2, 3.

In Stage 1 there is no problem and the loan is performing as expected. The bank makes a small provision when they first put the loan on their books.

In Stage 2 there has been some development and the expected credit loss from the loan (or asset) has increased. Now the bank has to make an estimate of any future losses and take an extra provision. The initial Stage 1 provision was too low.

In Stage 3 there has been a credit event and the loan is impaired. A higher level of provisioning is required.

IFRS 9 came about partly as a result of the financial crisis. Regulators thought banks were waiting too long to take provisions. Technically, as long as the bank was still receiving interest payments on a loan the bank could claim nothing was wrong, even if the entire loan was on the verge of default.

With IFRS 9 the process is more forward looking, and subjective.

With IFRS 9 banks are continually estimating the future losses of their loan book (expected credit loss or ECL) and provisioning proactively. This results in large changes in provisioning if the economic outlook suddenly changes, like with COVID.

In a case like COVID or the Ukraine War, the banks go through all the loans and all the buckets, change their GDP assumptions and massively increase the entire provisioning requirement for the entire bank. In the next reporting period they report large loan losses reflecting these changes in assumptions, even if all the companies are still paying and nothing has happened yet. The bank proactively provisions for the impending crash.

Unicredit for example still has EUR 1.8bn in general provisioning overlays for COVID which it hasn’t used. FYI, banks are quick to make these provisions and slow to reverse them.

While ‘NPL’s as an IFRS accounting term doesn’t exist, banks still report ‘NPL’s’ or ‘NPE’s (non-performing exposures) because it’s a concept we are all familiar with.

NPL’s are reported as both ‘gross’ and ‘net’ as a % of loans. ‘Net’ is after provisioning. Usually, gross NPL’s should be under 5%.

As a rule of thumb banks in the US will provision 70-100% of NPL’s while Europeans are usually lower (40-50%). US bank analysts often criticise European NPL coverage ratios as too low. European banks will say there is real estate collateral behind the loan or some other reason why the loss on the loan isn’t going to be 100% and so that’s why the 40-50% is good enough.

npl_ratio = non_performing_loans/avg_customer_loans

Lesson 5: Income Statement

The revenue lines for a bank income statement start with net interest income, followed by net commissions and fees followed by trading income.

This is followed by operational costs. A cost/income ratio below 40% is good. Unicredit is at 36%.

Below the operating profit line are changes in provisions for loan losses or changes/impairments in the value of bonds held to maturity (changes in bond values can also show up in the trading line if they are mark to market, but it depends on the accounting games they are playing).

Note Unicredit is reporting ‘Return on Tangible Equity’ and Tangible Book value per Share

tangible_bvps = (equity - goodwill)/end_of_period_shares

There are regulatory reasons for reporting this way, but I think ‘net of goodwill’ calculations get confusing and unless it is a special case I use stated ROE and book value per share. We will address how to use these for valuation below.

Lesson 6: Free Cash Flow

Free cash flow doesn’t exist for banks the same way it does for other sectors. Or, it kind of does, but it gets confusing.

A more important concept is the capital being consumed to grow the balance sheet, which is capex for a bank.

If a bank earns a net income of $10bn in a year, but also grows its balance sheet from $100bn to $150bn in that same year, and those new $50bn in assets require an incremental $10bn in regulatory capital (at 20% risk weighting) then the free cash flow of the bank in that year is $0. +$10bn in net income, but -$10bn in regulatory capital for the new assets.

In the following year, the free cash flow will presumably be $10bn + whatever they are earning on the $50bn in assets. If the balance sheet hasn’t changed during the year there is no incremental capital requirement.

Lesson 7: Capital Efficiency

The key to being a profitable, resilient bank is to be stingy with the balance sheet and use just enough of it to bring in the customers (because money is what the customers want), but then do an excellent job of cross-selling the customers fee driven products which don’t use the balance sheet. It’s hard to achieve, but banks would love for fee revenues to be equal to the net interest income (or 30-50% of total revenues).

For retail customers this means offering a low-risk mortgage, but then also getting the customer’s deposit account (with monthly account fees) and also selling mutual funds to get asset management fees.

Side note: If rates are super high (like in EM) you can stick all your deposits in 0% risk local government bonds and generate 20-30% ROE’s and not worry about all this cross selling stuff.

For a corporate account it means giving out a loan, but then also getting all the treasury management, payment and FX business which generates fees, but has no risk, and doesn’t require any capital. Unicredit calls this ‘Client Solutions’

Sometimes banks try so hard to chase fees that they give away the balance sheet too cheaply, which comes back to bite them during the next crisis.

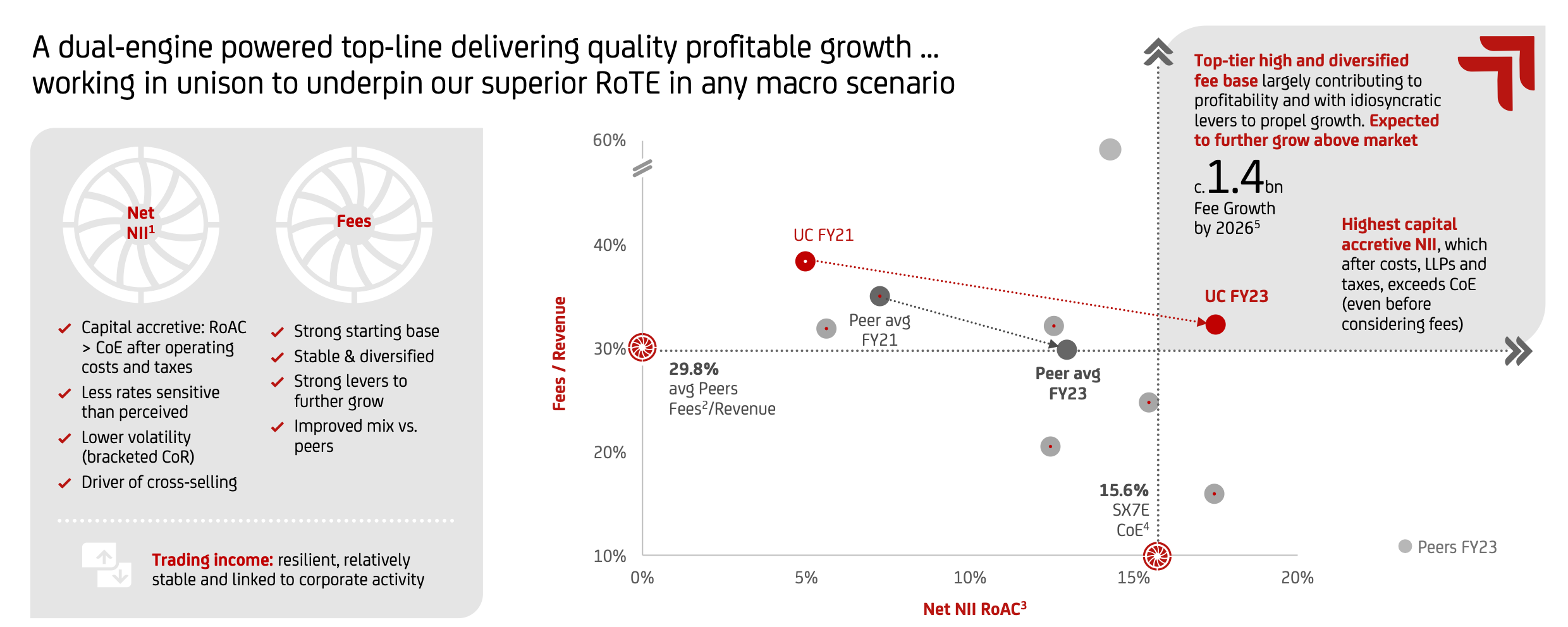

In the chart below Unicredit is demonstrating it has a good mix of fee revenues (30%) but is also using the balance sheet effectively.

The y axis shows Fees/revenues is over 30% which is high relative to other banks. The x axis is the ROE the bank is generating from the balance sheet (Net NII RoAC) without fees. So being up and to the right shows Unicredit is earning a good ROE on lending (charging sufficiently for use of the balance sheet), but also generating a high level of fees. It’s a complex calculation and I’ve never seen a bank show it like this before. It’s good.

Lesson 8: Valuation and Investing

To value a bank stock I look at a mix of P/E, Price to Book and dividend yield.

You know how P/E’s work. They aren’t super technical. Or, they could be, but in practice are not. The P/E where a bank stock trades depends on the growth, where the peers are trading, excess capital etc. Bank P/E’s generally range between 5-14x. Sometimes you will find an EM bank where the locals think it’s worth a P/E of 20x, but I find those to be anomalies and I’m never interested in them.

The more technical approach is price to book where the fair value is the based on ROE relative to cost of capital. The ‘cost of capital’ has a finance book definition, but in practice changes day to day depending on people’s animal spirits. For banks operating in countries with 10 year government bond yields in the 3-5% range I use a 10% cost of capital. So a 15% ROE bank should trade at 1.5x book.

price_book_ratio = roe/cost_capital

We could/should add a growth rate component to the equation (cost_capital - g), but the fair values you get are beyond the market’s imagination.

While roe/cost_capital is the textbook price/book valuation for a bank, in reality valuations wander all over the place and it’s hard to tell why. It often depends on investor’s outlook. The bank might be earning a great ROE, but investors are sure next year there will be a recession. Kind of like how things are now.

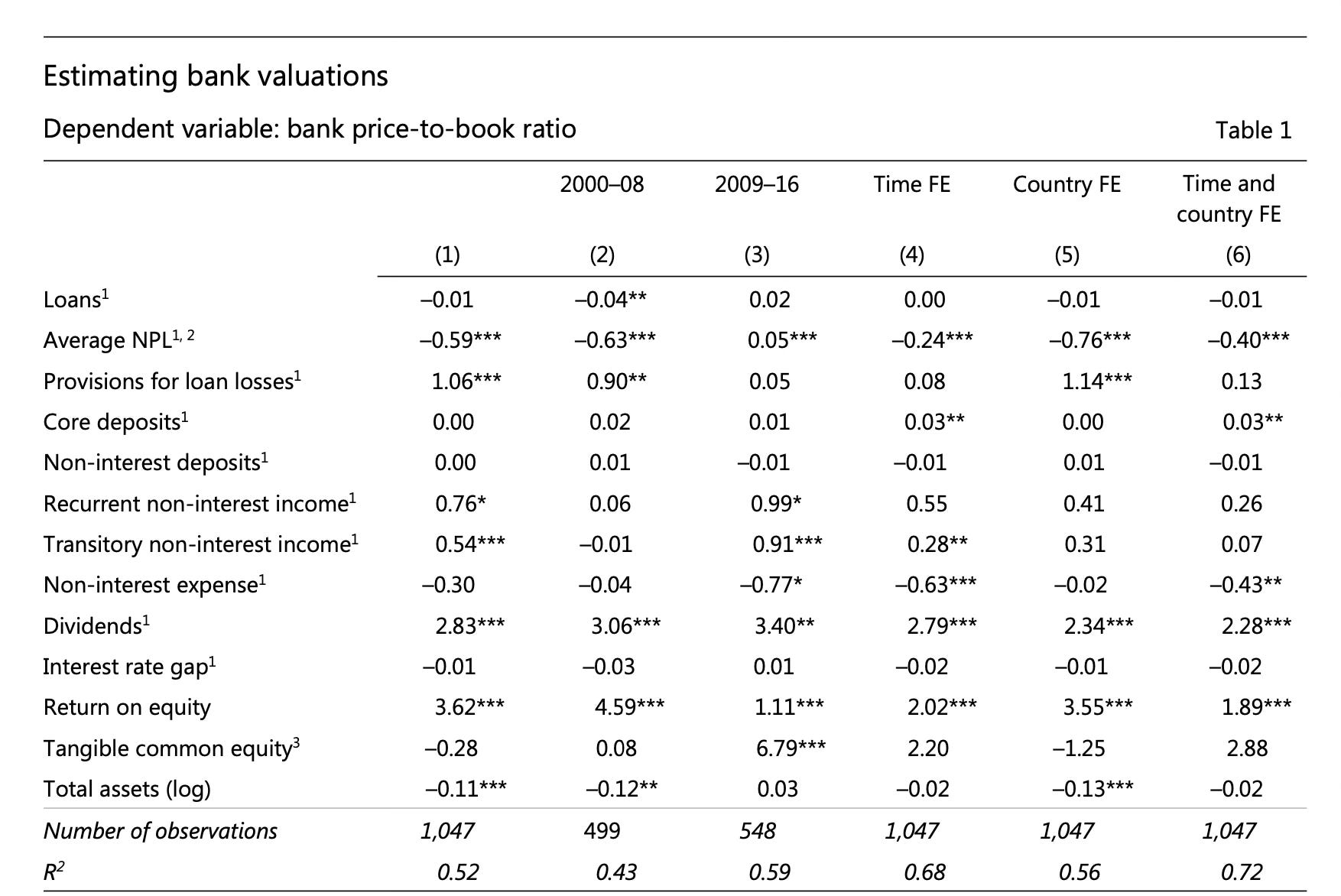

Below is a regression analysis of price to book valuations by the BIS. They find that ROE is the biggest coefficient for price to book ratios (fits the textbooks), but ‘Dividends’ is another, which kind of makes sense. Dividends imply capital adequacy.

The chart below from Unicredit is unique because it is mixes ROE (or Return on tangible equity) on the X axis with P/E on the y-axis. Note the footnotes for the ROE. Unicredit has too much capital (Core Tier 1 ratio of 16%) so they are adjusting their ROE to use less capital in the denominator (using 13% Tier 1 instead of 16%) which makes the ROE higher.

On stated YWR 2024 numbers (no adjustments) Unicredit earns an ROE of 14% and trades on a P/E of 6x.

Quizz Time

At the bottom are links to the YWR Unicredit model as well as the reference documents we used in the class.

Close your books.

4 questions. Let’s see how you do.