YWR: CBK's Cashflow Pile Up.

Disclosure: What follows is personal commentary. It is in no way meant as an investment recommendation or advice. For investment advice and guidance seek professional help.

From: Paul Rillo <prillo345@gmail.com >

Date: 02 September 2023 at 17:42:44 BST

To: Erik @ YWR <erik@ywr.world>

Subject: Money Maker?

Hey Erik,

Been loving all these posts on how to allocate my $50 billion endowment, but can we get back to business?

Do you know what I need out of you?

Three letters. A ticker.

Give me a ticker to buy and no more wonking on about the yield curve or the economy.

Thanks.

Paul

From: Erik @ YWR <erik@ywr.world >

Date: 02 September 2023 at 19:25:10 BST

To: Paul Rillo <prillo345@gmail.com>

Subject: Money Maker?

Dear Paul,

Thanks. You remind me of someone I used to work for.

This is supposed to be market commentary… but I’ll give you 3 letters. Well 5 actually.

CBK GR

Commerzbank in Germany.

But it could also be Unicredit, Santander or most banks in Europe. The investment case is similar.

It’s a good investment idea, but it might be challenging.

Do you know why?

Because it requires you to do nothing for 2 years.

Can you resist trading Nvidia after the close?

Can resist watching CNBC all day and buying 2 day call options based on your latest stochastic indicator?

If so, there is a good investment case in European banks, but it will be highly boring. Let me explain.

The backdrop is that there has been a paradigm shift in the investment return for shareholders of European banks and the market is slow to recognise this.

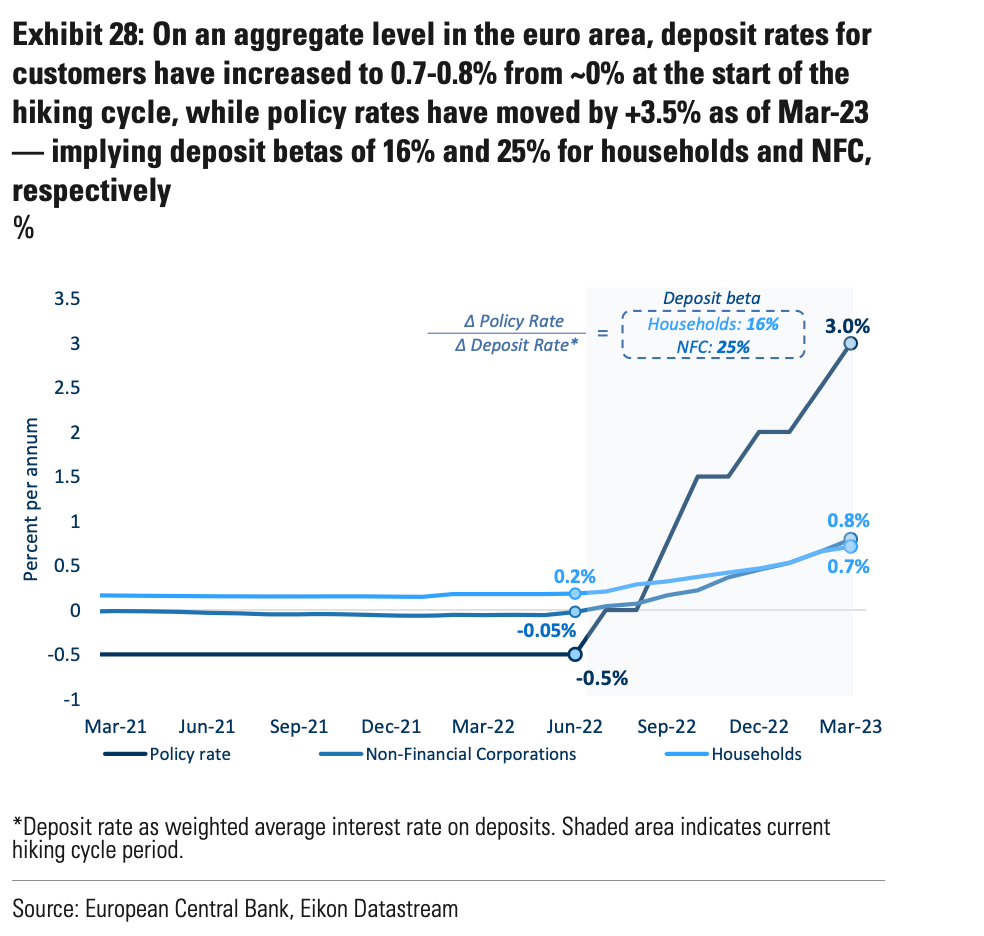

The paradigm shift has 2 parts. The first is the move in ECB deposit rate from -50bps to 3.75% (chart below). The second shift is the current over capitalisation of the European banks after 12 years of deleveraging. Regulatory Capital ratios are now too high.

Summary: There is a cashflow pile up underway at European banks and there is nowhere for it to go but to shareholders.

Bank net interest income is complicated and people get confused because of all the moving parts; lending rates, deposit rates and the timing and sensitives of all the different assets and liabilities. The big picture is that is orders of magnitude easier to make a lending spread when interest rates are 3.75% than when they are -0.5% and that is what is happening.

This chart from Goldman tries to capture how banks are raising the rates on deposits, but more slowly than the rise in the ECB policy rate, which is why profitability is exploding. Note this chart is out of date. The policy rate is now 3.75%.

Another point to remember is that it takes time for banks to reprice loans. It also takes time for older low interest bonds on the balance sheet to mature and for the bank to reinvest the funds into higher yielding securities. This is why the net interest margin and profit increases are only just starting and will play out over 2023 and 2024. The ECB rate increases started at the end of 2022 and we have only seen 1H 2023, so the profit growth is happening, but we still haven’t seen the full effect. I think the market is not looking ahead to where earnings will be by the end of 2023 and especially 2024.

Let’s talk specifics and because I just updated my Commerzbank model let’s use that. The current share price is EUR 9.1.

If you’ve been following Commerzbank over the last several years the earnings have been a mess. The bank has taken large restructuring provisions to lower the number of staff and branches in a move to be more digital and more profitable (-7,500 FTE by 2024). It’s good long term and is benefitting costs currently, but it butchered earnings in 2020 and 2021 by EUR 800 mn and 1.1bn.

Then there was the EUR 1.8bn impairment of goodwill in 2021.

Then there were the problems with the CHF mortgages sold through their Polish bank, mBank. This dates back to the early 2000’s when Polish banks were originating mortgages in CHF because Swiss interest rates were lower. There was always the risk to borrowers of being short the CHF, but they did it anyways.

Even though the Zloty did blow up vs the CHF it still worked out for the consumer (mortgage borrowers) because for some reason the European courts have decided this is the banks’ fault and the borrowers can be reimbursed for their losses. Commerzbank has taken EUR 1.7bn in provisions against EUR 2bn in CHF loans in Poland. Commerzbank took additional provisions for this in 1H 2023 after a recent court ruling reaffirmed Polish consumers were misold the mortgages and didn’t understand what they were doing. So this has been a drag on the earnings, but I think we are finally done with it.

On top of this Commerzbank has been worried about the German economy and pre-emptively taken an additional EUR 475mn in provisions for their overall loan book in case NPL’s increase (currently at 1.1%).

So you see, it’s been one thing after another but we’ve taken care of Poland, paid for laying off German employees through 2024, made extra provisions for the upcoming recession (which may or may not come). And now, we’ve eaten enough vegetables and it’s time for desert.

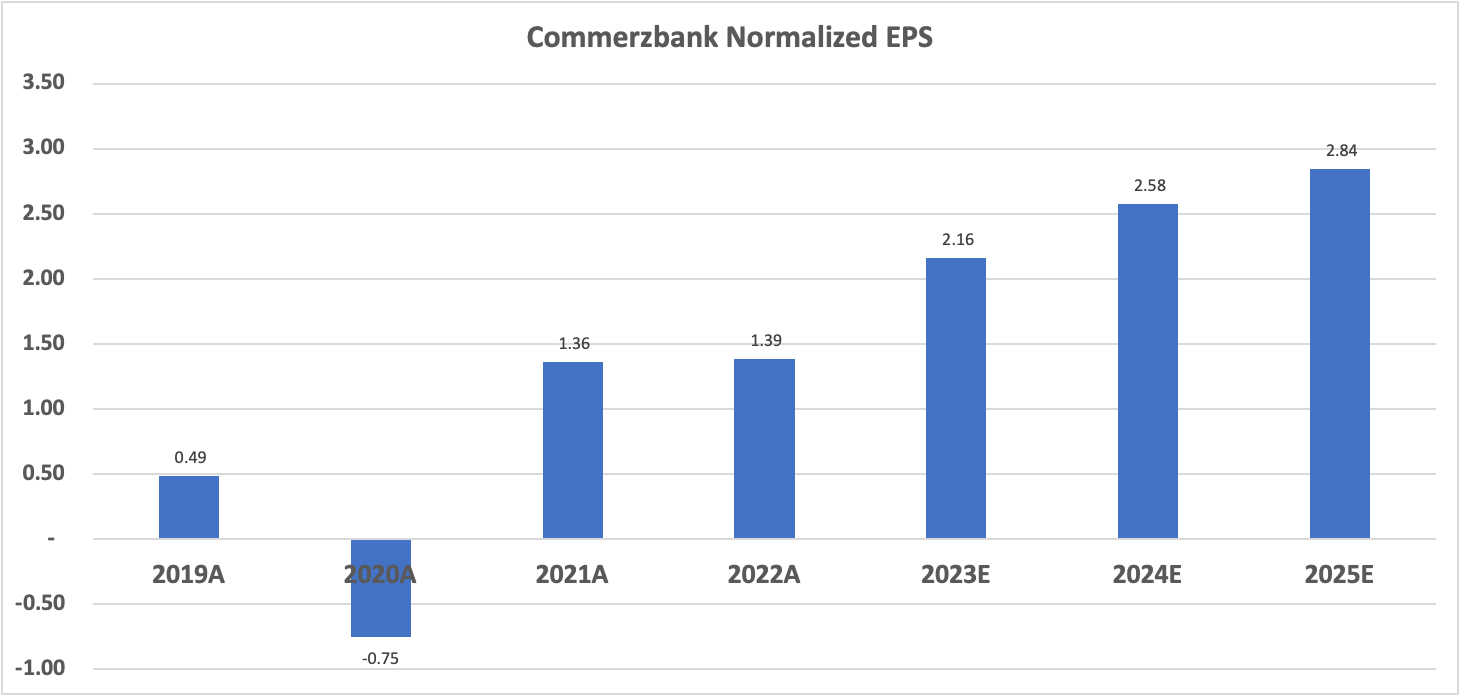

Look at the earnings per share progression from here.

I’ve made the chart nicer by using ‘normalised earnings’ which strips out all the past restructuring charges in 2020 and 2021, so you can see the growth in the underlying business of the bank.

Earnings growth is nice, but the real desert is in May 2024. After full year 2023 earnings are published and the board has had their meeting I expect Commerzbank will pay a 70ct dividend on 2023 profits. So wait 9 months and you get a check for 7.7%.

Paul, this is where you have to wake yourself up from your slumber, log into your brokerage account, take that 70cts and reinvest it into more Commerzbank shares, because there is another payday coming in May 2025. That’s when you will likely receive a dividend of EUR 1.1 share. After you have done the reinvestment trade you can go back to sleep again. I told you this would be boring.

It’s boring but by May 2025 (21 months from now) your CAGR from the dividends is 11% assuming no movement in Commerzbank’s share price. But then look where you will be in May 2025.

Let’s say Commerzbank shares have done nothing and are still trading at EUR 9.1/share because people are worried about the economy, they are bearish on Europe, they don’t want to own banks and would rather own Nvidia, bla, bla, bla.

Then you are sitting on shares that will likely pay a DPS of EUR 1.25 in May 2026 which means a dividend yield of 13.6%. Even though people don’t like banks it’s unlikely the share price is going to still be EUR 9 when the company has now established a track record of paying out large dividends of over 1 Euro per share.

Here is the dividend share progression.

There is also probably 40-50% upside in the share price assuming the shares trade on a 7% dividend yield in 2025 (1/0.07 = 14.2).

You’ve got your EUR 1.8/share in dividends(0.7 +1.1) and now maybe the share price rallies 50% too.

Furthermore, there is a cherry on top. I’m assuming Commerzbank pays out 40%-45% of earnings and also does some minor sharebuybacks (EUR 600mn/year), but because loan growth is only 3% (‘Europe doesn’t grow..’) there is a massive pile up in excess cash at the bank.

If we assume a 15% Tier 1 ratio is the adequate level of shareholder’s equity then by 2025 there is EUR 5bn in excess capital and the Tier 1 ratio is almost 18%. The market cap today is only EUR 11bn so 5bn in excess capital in 2025 is 45% of today’s market cap. That’s why I call it a cashflow pile up.

And this is all after the EUR 600mn/yr in share buybacks and dividends.

Maybe in 2H 2024 when management is certain the profits are real and the money is ‘in the bank’ Commerzbank has to start doing even bigger buybacks. special dividends or take the dividend payout ratio above 45%.

Who knows, we’ll see what happens when we get there, but it’s an additional cherry on top that should play out positively. But again, it takes time, and at the moment it is impossible for investors to visualise the compounding nature of these rate hikes on earnings and how big an effect this becomes by Year 3.

A quick comment on risks:

Commerzbank owns mBank in Poland so a real drop in the Zloty vs, the Euro is a negative, but it has to be a real move. Turkey style.

Political interference like a special bank profits tax or cap on lending rates, basically ways to stop the banks making money on the higher rates and shielding consumers. Moves like this are already happening in the UK and Italy. This will have some negative effect, but my advice is generally to not overreact and be patient. I have seen this many times in many markets. The banks will say nothing publicly, but behind the scenes they will tweak every charge for customer wire transfers, account overdraft fees, mortgage origination fees, etc. They will find 20 different ways to make their money, but they aren’t going to say in public or on analyst calls that they are doing this. Just be patient.

Fear of recessions. European banks have not been growing the loan book for 12 years (since the GFC) and have already taken extraordinary provisions in preparation for a potential slowdown. So the loan books are mature and with large corporate customers they know well. It will take a considerable crash to shake the earnings picture and a lot of negativity is priced in to both the valuations and consensus earnings forecasts (which are too low).

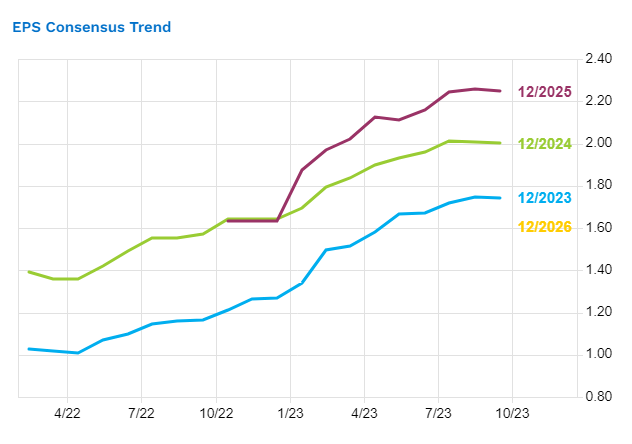

Source: FactSet A drop in interest rates. Again, be careful to not overreact. The banks will quickly cut deposit rates, faster than their lending rates to defend their margins.

Oh, BTW I put my condensed earnings model for Commerzbank in the YWR data section. I also added a tab in the model with charts from the Goldman European banks report from May. Their charts help gives more perspective on the sector, valuations and also commercial real estate. Remember, the model is just my forecasts.

Feel free to change the assumptions on net interest margins, loan losses, expenses, loan growth, or whatever.

Hope this helps!

Erik

P.S my Commerzbank earnings model. See below.