YWR: EuroBanks 1H Earnings Review

Disclosure: What follows is not financial advice or an offer to sell a security. Get financial advice from a professional.

European banks are our biggest theme and 50% of the Dirty Dividends Portfolio. Let’s do a quick 1H earnings review.

First some summary takeaways then we’ll get into the details of each result.

For YWR subscribers links to the updated earnings models are at the bottom of the post.

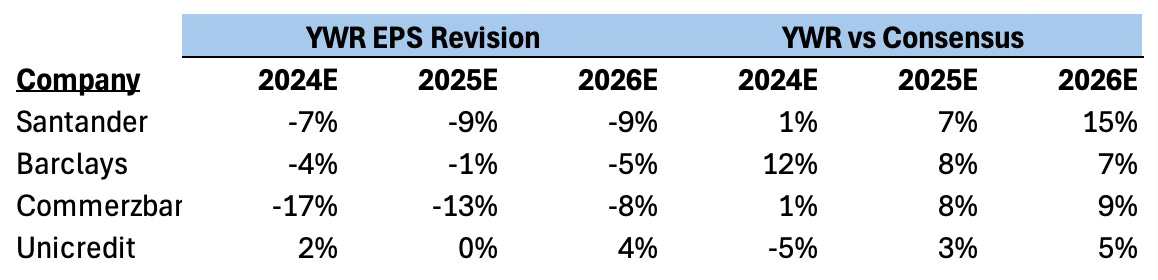

I’m still ahead of the consensus on European bank earnings, but after the 1H results I had to cut my estimates by -6% on average.

Asset growth is coming in lower than I expected (<3%). The banks are well capitalised and profitable. And I thought they would be lending by now, but the problem is corporates and retail don’t want to borrow at the higher rates. With the higher capital requirements and regulations the banks are also more careful about lending and pricing. They would rather buy back shares than do stupid loans at the wrong price.

Net interest margin expansion has been lower than I expected at Barclays and Commerzbank. They have been giving away more of the rate increases to depositors than I expected.

Loan loss provisioning has been surprisingly low and this is a positive offset to the lower revenue growth. I had expected that with a lag there would be higher loan losses, but so far it isn’t happening. The whole European recession story isn’t playing out.

Cost control has been better than expected. I thought costs would be growing 3-4% in line with inflation, but cost growth is basically 0%.

The ‘Shrink to Grow’ strategy is in full effect. Banks are focused more on the share price. They realise top line revenue is not the only way to grow the EPS. Because the loan book isn’t growing the improved free cash flows are going into share buybacks.

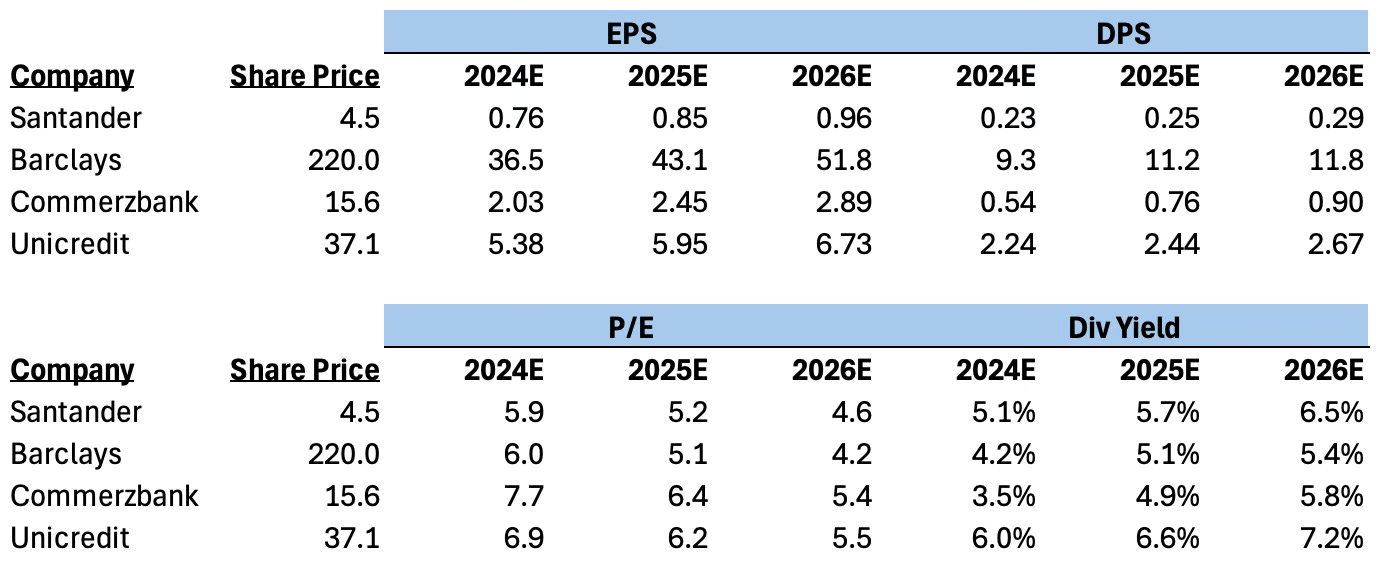

Post 1H results Santander looks like the best set-up. Despite good results and earnings upgrades, the share price has gone nowhere. The street under estimates the long-term growth through 2026. Santander trades on a P/E of 4.6x 2026 (on YWR estimates).

Valuations look great. Soon we will be rolling forward to 2025 earnings where despite the good share price performance the banks are still on P/E’s of 5-6x.

Dividend yields are 5%. The banks all have share buybacks on top of the dividends, but I’m capturing that through the growth in EPS and DPS.

It’s annoying the shares aren’t rerating more quickly. On the positive side it gives management more time to buy back shares at 5x earnings, which improves the longer term upside.

Santander

I think I love Ana Botin. She’s doing a great job with Santander and her father would be proud.

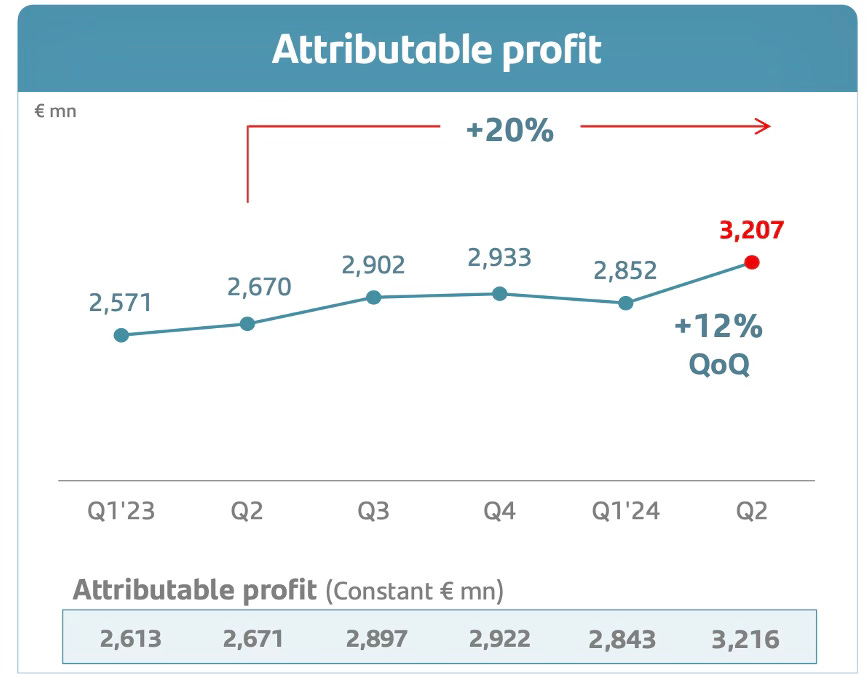

Really good growth in net interest income (+12%), 10% revenue growth with 3% cost growth = + 15% in operating profits.

The South American business did really well and offset the UK which was weak. Brazil was especially good.

, time deposits and mutual funds

• Greater profit and profitability YOY, driven by NII (volumes and cost

of deposits) and efficiency gains, more than offsetting lower gains on

financial transactions and higher LLPs (growing less than loans)

Profit rose QoQ, with better NII and fees and controlled costs

Loans

€99bn +10%

Efficiency

32.4% -2.7pp

Underlying P&L*

Nil

Net fee income

Total revenue

Operating expenses

Net operating income

LLPs

Attributable profit

(*) mn and % change in constant euros.

(1) % change in current euros.

Deposits

€86bn +14%

CoR

4.77% +3bps

Mutual Funds

€50bn +22%

RoTE

15.9% +3.8pp

HI'24 % HI'23 % HI'231

2,605

888

3,477

-1,109

2,368

-1,158

580

3.3

9.3

3.4

0.1

5.1

3.9

7.7

5,235

1 ,734

6,984

-2,265

4,719

-2,322

1,141

22.4

3.8

11.4

2.8

16.1

7.6

39.0

22.2

3.6

11.2

2.6

15.8

7.3

38.7")

Santander is trying to grow everywhere, but a big focus is OpenBank in the US. They see a big opportunity to grow corporate banking and advisory in the US given their strong linkages with Mexico and South America.

In the interview with Ana Botin you realize you have a multi-generational family of bankers running Santander with a good balance of stability and growth.

Why can’t Santander trade at EUR 7/share?

Barclays

Profit before impairment

Credit impairment charges

Profit before tax

Tax charge

Profit after tax

Non-controlling interests

Other equity instrument holders

Attributable profit

Half year ended

30.06.24

Em

3,713

877

632

6,347

1 ,678

30

13,277

(7,997)

(120)

(64)

(8,181)

16

5,112

(897)

4,215

(892)

3,323

(26)

(510)

2,787

30.06.23

Em % Change

3,922

935

558

6,312

1 ,593

202

13,522

(8,030)

(32)

(8,062)

(2)

5,458

(896)

4,562

(914)

3,648

(30)

(507)

3,111

(5)

(6)

13

5

(85)

(2)

(1)

(6)

(8)

2

(9)

13

(10)")

Cost: income ratio

Loan loss rate (bps)

Basic earnings per ordinary share

Dividend per share

Share buyback announced (Em)

Total payout equivalent per share

Basic weighted average number of shares (m)

Period end number of shares (m)

Period end tangible shareholders' equity (Ebn)

11.1%

50.1

62%

45

1 8.6p

2.9p

750

c.8.0p

14,972

14,826

50.4

13.2%

47.2

44

19.9p

2.7p

750

c.7.5p

15,645

15,556

45.3

(4)

(5)")

Great cost control, loan losses are fine, and good buyback execution, but no revenue growth.

I cut my expectations for net interest income. Deposit competition has taken away much of the rate increases and the structural hedge is not offsetting this as I expected.

Barclays UK is doing really well. The drag is BarCap. It’s been an anchor. Barclays has 58% of their risk weighted assets in Barcap where it is generating a 9.6% return on tangible equity.

1'4

1,869

Q222

CIR

6.5%

200

Q124

57%

Barclays Q2 2024 Results

August 2024

Yoy

22

RoTE (0/0)

Q222

Income by business (Em)l

Banking fees &

underwriting

Intermediation2

Financing3

International

Corporate Bank

2,924

554

1,435

747

188

Q222

2,743

472

937

812

522

Q223

3,328

617

1,587

700

424

Q124

Yoy

+44%

-2%

-5%

1,814

Q223

66%

12.0

Q124

1,999

Q124

60%

5.9%

203

Q224

58%

1,903

Q224

63%

Risk weighted assets (Ebn)

9.6

Income/

Average RWAs

Period end

RWAs

Q223

Q224

1B RWAs as % of

Group RWAs

5.70/02

208

Q222

60%

3,019

679

1,051

794

495

Q224

5.5%

197

Q223

59%")

If Barcap can start to grow consistently, it’s a massive kicker for the stock.

I’m frustrated by the lack of revenue growth, but I’ve decided I should be patient. I’ll let Venkat keep plugging away and turning things around.

Consensus estimates at 40p for 2025 are quite conservative. I’m at 43p.

If Barclays can improve its revenue growth and earn over 40p in 2025 the stock has a shot at £3/share so I’m keeping it.

Commerzbank

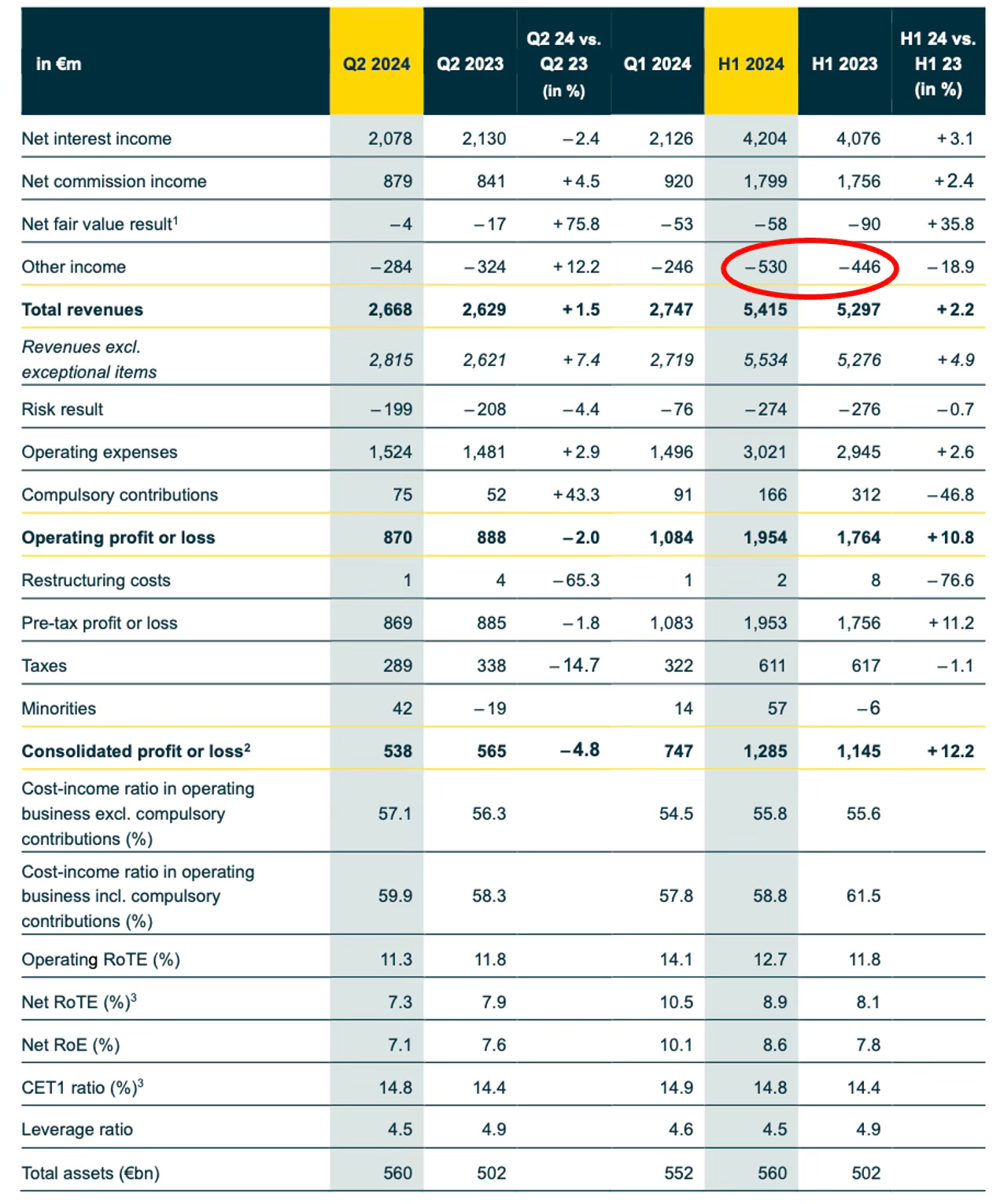

Do you see the -530mn in that ugly red circle? Those are one-off costs for Russia and Polish mortgages. Those were not supposed to be there in 2024 and it was going to be a big kicker for the shares. Pre-tax should have been 40% higher. Everything else was good, but Polish mortgages won’t go away.

Despite all the negativity about Germany NPL’s are non-existent at 0.8%.

Like every bank in Poland, Commerzbank’s mBank originated mortgages to Polish retail in CHF. Borrow at a lower rate, but take the CHF risk. Yes, everyone signed and said they knew the risks, but then when the CHF appreciated 40% against the zloty the lawsuits and consumer protection investigations started. The provisions for settling disputes over CHF mortgages has been going on for years. I thought this issue was put to bed, but there was a new court ruling which opened up thousands more settlement cases. Maybe it will be put to bed in 2025. The big lesson is there is no way to innovate in retail banking. If you offer a new product and the consumer loses money no matter what they said they knew you are fried as a bank. So stick to plain vanilla products and bash you brains out offering the same thing as the competition.

Commerzbank made a provision of EUR 95mn for guarantees provided to Gazprom. Linde was supposed to build Gazprom a chemical plant in Russia, so Gazprom made a deposit for the construction with bank guarantees from Commerzbank, Deutsche and Unicredit. Then Linde had to stop construction because of European sanctions and Gazprom naturally wanted its money back. The European banks weren’t sure they should pay Gazprom and if that would go against European sanctions. Gazprom then got a Russian court to order the banks to repay them. The European banks were caught in an impossible situation with two opposing laws. The point is it’s increasingly difficult to operate in these environments with geopolitical sanctions. Russia is an extreme case, but I bring it up because I think China is turning into a version of this. For companies operating in the middle of a Cold War it might be easier to pull out of China rather than get caught in between local court case rulings on the one side and international sanctions on the other.

There is a silver lining though. Unicredit surprised the market by announcing they bought a 9% stake in Commerzbank. Maybe it will be acquired at a premium. Unicredit CEO Andrea Orcel sees the value in Commmerzbank once the Polish mortgage provisioning is finished and how he can merge both the German and Polish businesses with Uncredit’s Hypvereinsbank and Bank Pekao. YWR will keep the shares and see how it plays out.

Unicredit

Unicredit is 1 year ahead of everyone else (except maybe Santander). The Tier 1 ratio is in surplus, they’ve cut costs, the loan book is clean, commissions are growing, and they’re buying back shares. Now they are moving to offence and acquisitions.

As mentioned above Unicredit secretly built up a 9% stake in Commerzbank. It's a great fit and would be accretive.

Unicredit’s move will get the other bank CEO’s in Europe thinking about what moves they should be making. After the long bear market of 0% interest rates investors have been happy so far for CEO’s to cut costs, increase dividends and buy back shares, but now we want growth. If the loan books aren’t growing, and net interest margin expansion has peaked (for now) how can you grow the bank in other ways? Unicredit has opened up the whole kettle of fish around cross border M&A, which has been dormant in European banking for years.

Andrea Orcel keeps exceeding my expectations and shows he is thinking years ahead. It doesn’t seem extraordinary for Unicredit shares to trade to EUR 50/share over the next 15 months. So we’ll sit tight.

Below are links to the YWR earnings models. They are also available on www.ywr.world under Data & Models. Always look at the most recent tab.

Have a good rest of the week.