YWR: Friday Money Maker(s)

The market may have given us a gift.

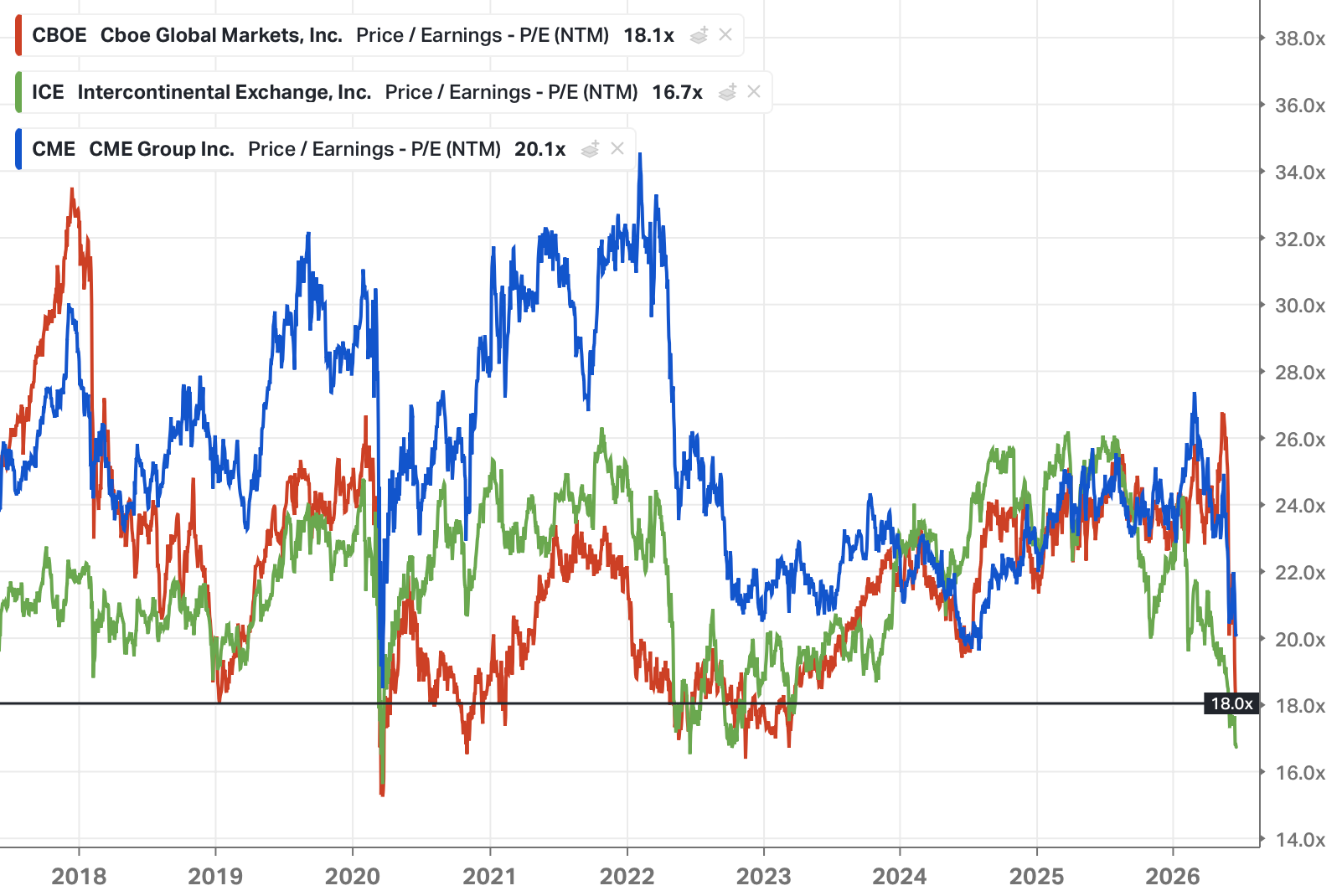

CME, ICE and CBOE are down 25% from their highs.

There are two issues.

First, is concern the CFTC’s approval of Kalshi’s perpetual future’s contracts might be a competitive threat to these established futures exchanges.

The second concern is that with the signing (?) of the Iran peace deal the Q1 surge in Iran War volatility was a one-off.

Forward P/E’s are back to trough levels for these businesses, which is sub-20x. Traditionally, this is a good entry point.

We probably don’t need to go over why these are great stocks to own. They grow in line with capital markets activity, have virtual monopolies in their products, high operating margins and minimal capex.

Perpetual Futures Threat

The fear with Kalshi’s new Crypto perpetual futures is whether these monopolies are under threat. It’s crypto today, but tomorrow it could be commodities and the S&P 500.

First let’s understand the real moats around these derivatives exchanges, because they aren’t really monopolies, they just naturally evolve this way.

#1 Liquidity network effects. This is the most obvious. Liquidity begets liqudity. It would be hard for a new exchange to compete with the CME’s flagship S&P 500 contract, ICE’s Brent contract or CBOE’s S&P options contract. Although you can see how CME also offers options and competes with CBOE, and why ICE has a competing WTI contract. But it’s really hard for a new entrant to get started.

#2 Collateral efficiency. A diversified derivatives exchange can reduce a client’s margin requirements by considering offsetting contract positions (long June - short September) as well as highly correlated contracts (long Brent - short WTI) when calculating collateral. This is a strategic benefit for a one-stop shop like CME (interest rates, equities, commodities, FX). This is also why traders might want to trade WTI on ICE for the margin benefits even if CME is more liquid.

#3 Back office clearing and settlement relationships. CME, ICE and CBOE own their own clearing houses and this is the key market structure. It’s hard to set up back office settlement relationships with all the major banks, commercial traders, futures clearing merchants, and market makers. Everyone is already ’set up’ with ICE, CME and CBOE. There would be huge inertia to setting up a new derivatives exchange and getting all the market participants connected.

This is different from cash equities settlement which is why cash equities isn’t very profitable for exchanges. US cash equities settlement is through the DTCC, a public settlement system everyone is connected to. Effectively, anyone can create a cash equities exchange. The settlement is a public good through the DTCC. Which is why exchanges make ‘billions’ trading futures and ‘hundreds of millions’ trading cash equities.

Rule of thumb: He who owns the clearing house makes the money. It’s why SGX and HKEX can make a lot of money in cash equities.

Perpetuals vs Futures

A traditional futures contract is tied to the underlying spot market through periodic delivery. Usually, quarterly. The requirement for future delivery means spot and futures market are highly connected through arbitrage.

Perpetuals are a crypto market invention where the contract is never delivered and has no connection to the underlying spot market. Instead there is a ‘funding rate’ which is meant to keep the perpetual tied to spot. If the price of BTC on a perpetual has pushed up to $70,000 because everyone is super bullish BTC and wants to be long with 20x leverage, while the spot is $60,000, there would be a 16% funding cost which gets paid to holders of the short BTC contracts. Effectively, compensating them for the contract deviating away from spot.

The perpetual structure kind of works as a way to trade things on a website without having settlement. But it’s like Automated Market Making, another crypto invention. It works (kind of), but it’s shaky and it’s not the same as being connected to the actual liquid underlying market.

Pushback on Perpetuals

#1 Retail product: It’s hard to see perpetuals as something institutions are going to use. American Airlines, Vitol, and Morgan Stanley want to trade energy contracts with deliverability of the underlying commodity. Real commercial traders who touch both the spot and futures market are the core to a contract’s liquidity. The pure play speculators are layered on top and chase after real world liquidity. I’m trying to keep an open mind of how the market might develop, but perpetuals are probably going to remain a fringe retail product for traders who want extreme leverage (>5x).

#2 Regulatory Review: CME is pushing back heavily on this CFTC’s decision to allow onshore regulated trading of perpetuals. On June 18th they sued the CFTC that perpetuals do not meet the Commodities Trading Act definition of a future contract, which clearly states the contract has to have a delivery date. If perpetuals have no delivery then they are ‘swaps’, which are regulated differently. The CFTC has responded that they will open up the matter to a wider industry consultation, which is what the CME wanted. CME Executive Chairman Terry Duffy gave a great 25 min fireside chat on this topic (as well as his positive outlook on CME’s growth). I recommend giving it a listen.

My guess is the futures industry is going to drag Kalshi through the regulatory mud and make it really hard to offer a regulated perpetual futures contract. And in the end if they do get it approved, the existing exchanges CME and ICE are well positioned to counter with products of their own if they want to.

Interestingly, Duffy thinks perpetuals futures are insane and the current retail speculative trading fever is the equivalent of subprime mortgages in 2007.

Why derivative exchanges are good Project Zimbabwe plays

The fear over perpetuals contracts provides us an entry point to businesses which are aligned with our Project Zimbabwe outlook. Earnings have been surging for the exchanges recently, and here is why it is likely to continue.

#1 Rise of retail speculation. The lesson from all inflationary periods is that trading and speculation increase as nominal assets rise and everyone flees cash. Duffy worries this is a short term cyclical trend. Project Zimbabwe says this is going to go a lot further.

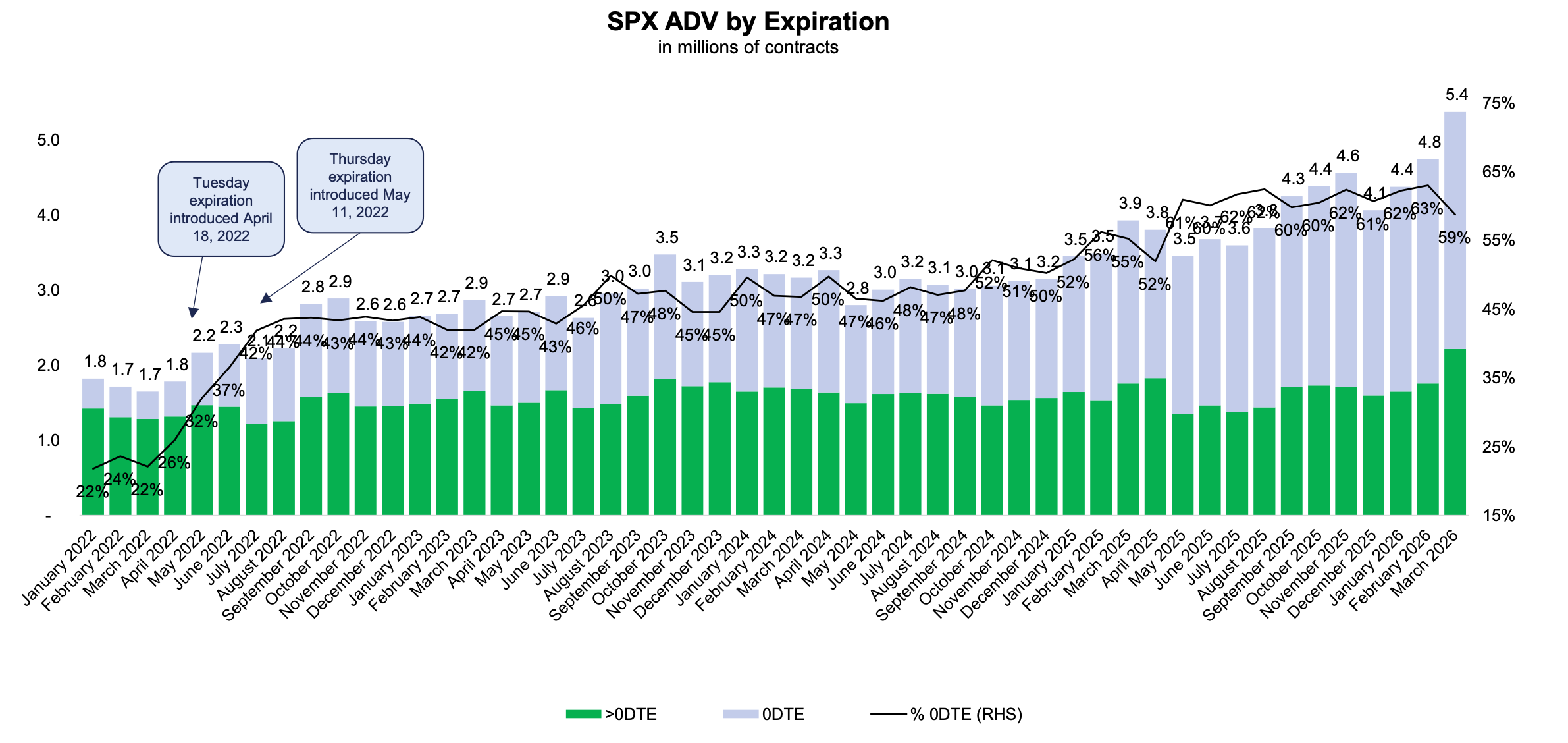

Project Zimbabwe is why hyper volatile short dated options grew gone from 22% of CBOE volume in 2022 to 60% in 2025.

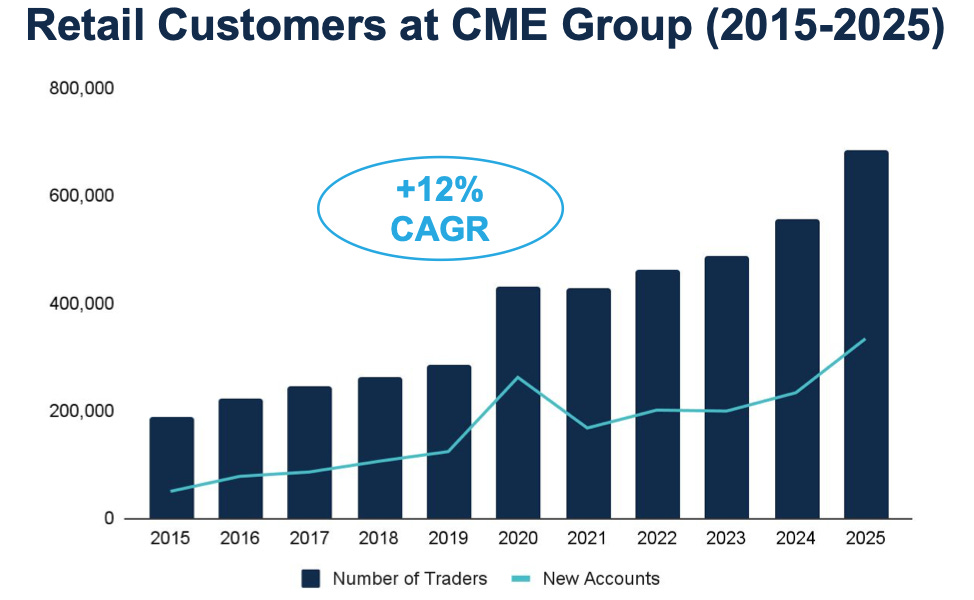

CME is also seeing a surge in retail trading.

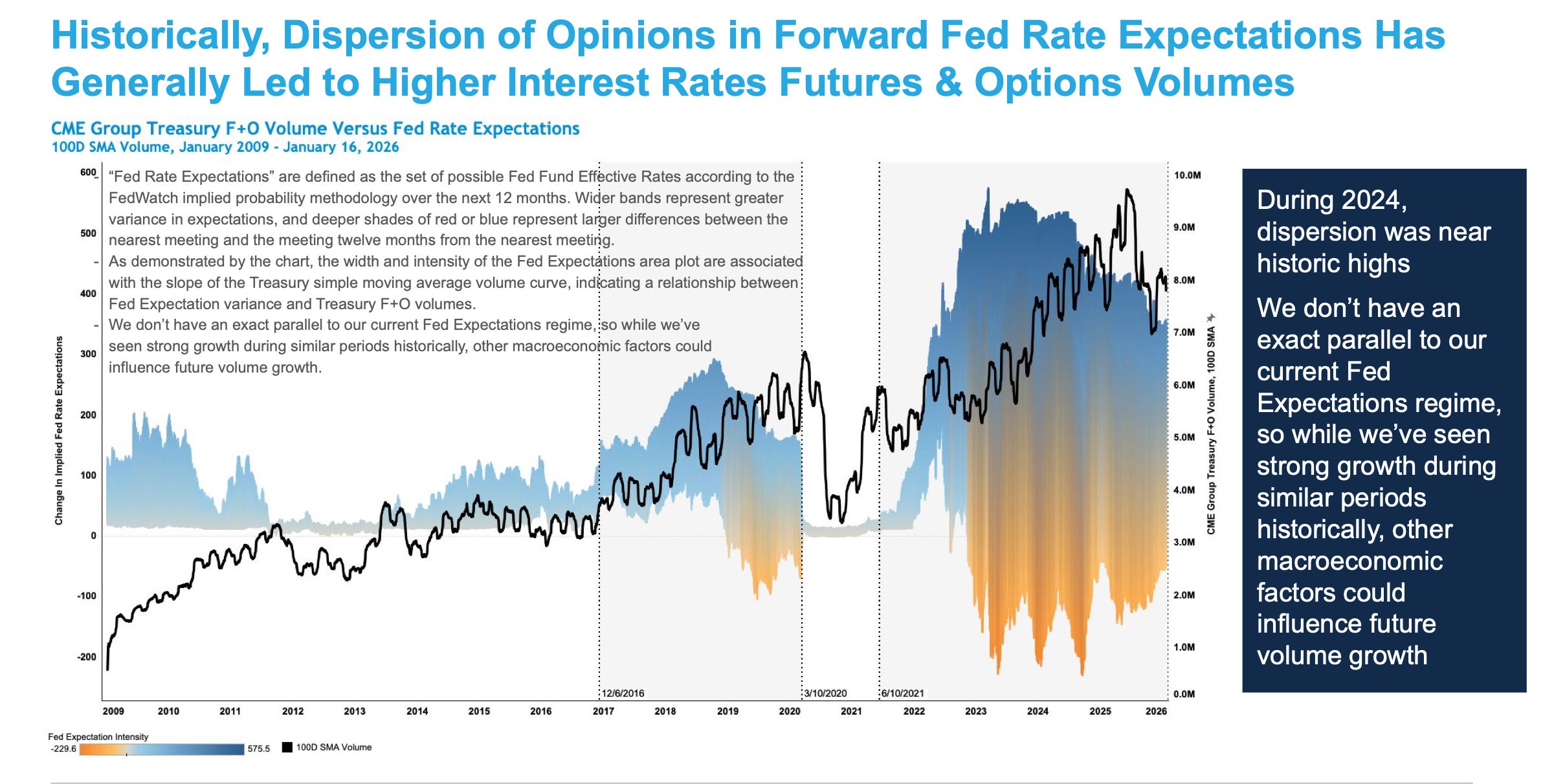

#2 Rise in interest rate volatility.

The biggest complex at CME is interest rates and it’s becoming a big product for ICE too. Interest rate contract volumes are growing rapidly which seems to be tied to our new environment where rates are higher and no-one knows if interest rates are going higher or lower from here. For the exchanges this uncertainty is great.

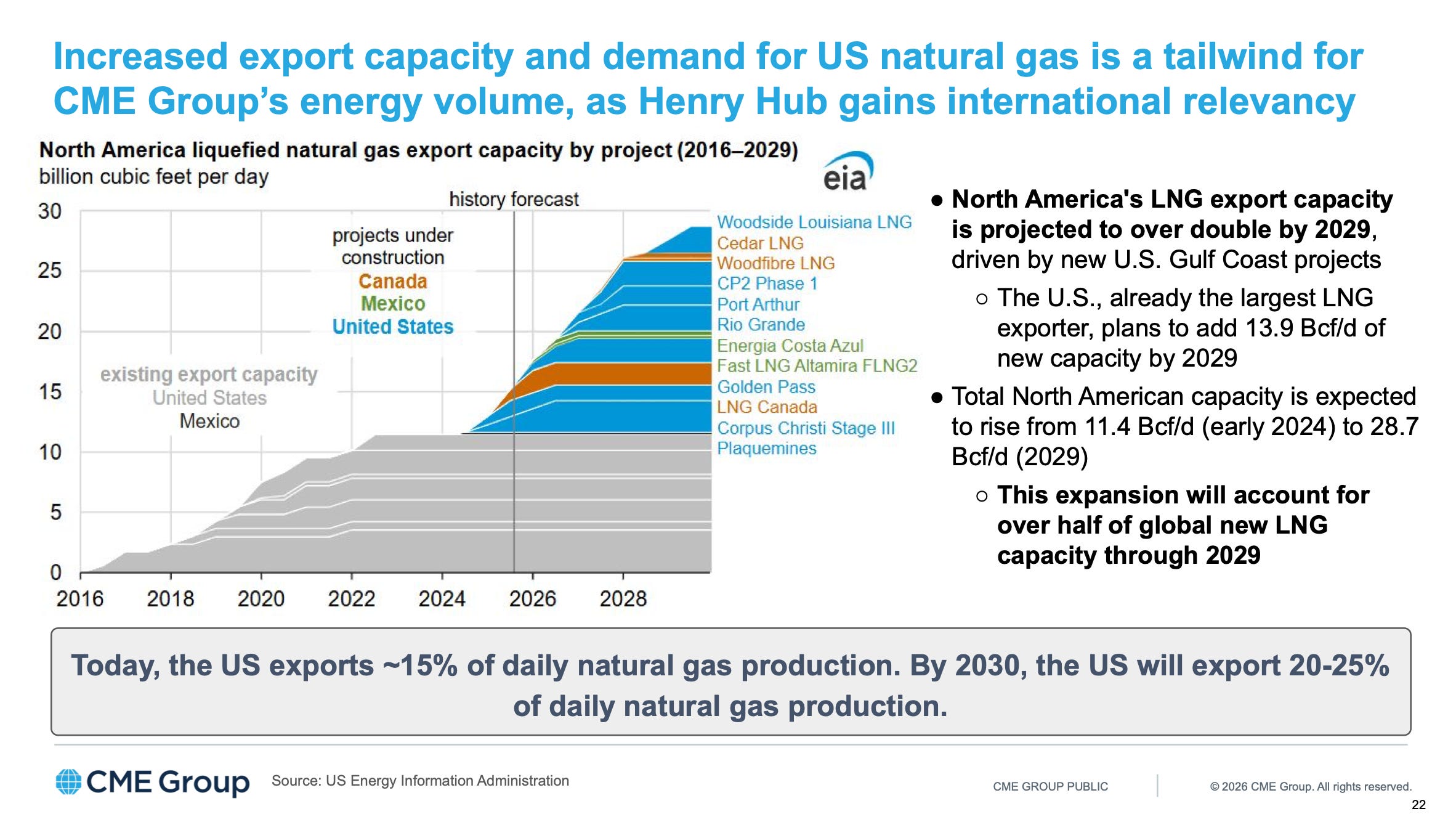

#3 Growth of US Energy Exports

The US is becoming the trusted, reliable supplier of world energy, especially for gas and LNG. Counterparties around the world will need to hedge their US supply with US energy futures contracts.

#4 Geopolitical uncertainty.

Covid, Ukraine War, Tariffs, Iran War.. .what next?

The world is increasingly uncertain and volatile. Which is great for hedging volumes in interest rates, metals, energy and equities.

Risks and Timing

I could be wrong, and this isn’t the best entry point for the derivatives exchanges, but I think with a long enough time frame these are good businesses to own. The other challenge is that it is hard to predict quarterly volumes. They can surge and then flatline, and it’s frustrating to wait around when things are quiet not knowing when the next volatility surge will hit.

You just have to know you own great businesses and also track all the initiatives they have to launch new products and data sets.

Below are my earnings models for CME and ICE.

Have a good weekend!

I’m going to go watch the HSBC Championship Cup tennis.

Erik