YWR: Global Factor Model

Let’s do it.

Let’s get into the data and make some money.

Like before we’re going to move through the usual charts quickly and get to the inflection ideas.

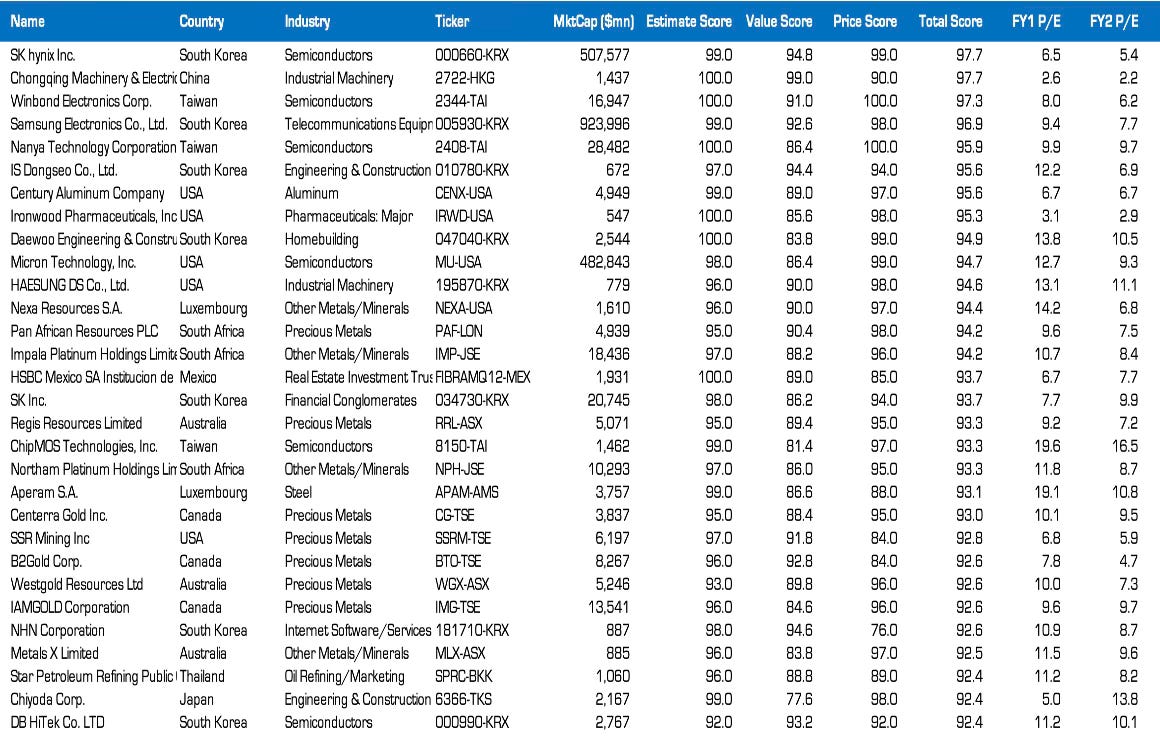

The YWR Global 30

The top 30 is everything we know.

Our themes are going mental.

Memory, Korea, gold, platinum, copper.

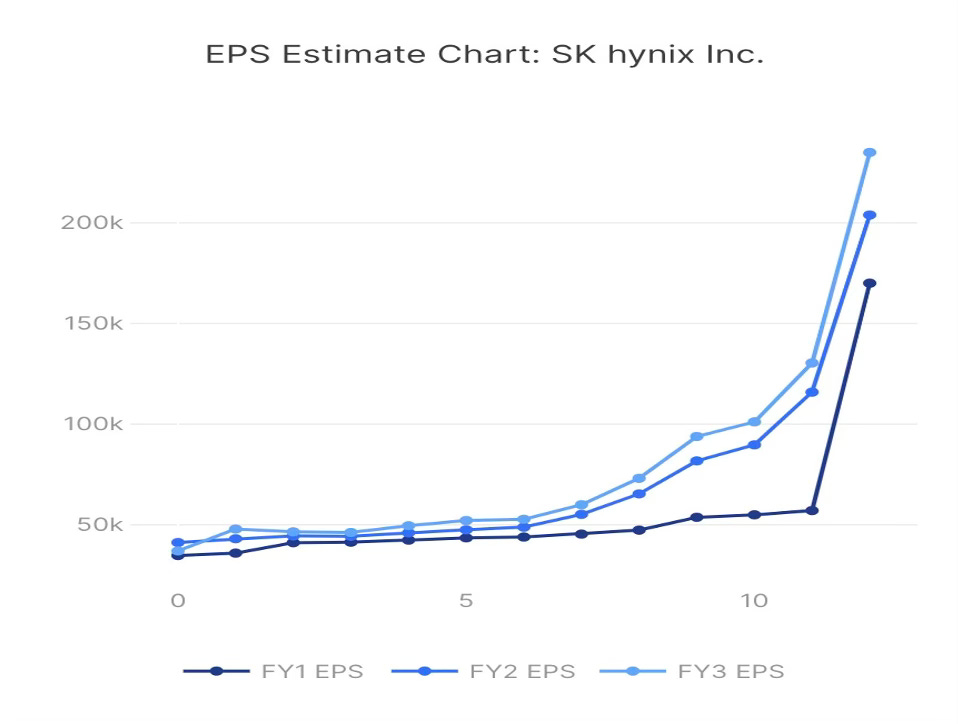

On memory, look at the estimates for SK Hynix!!!

My original forecast last August in Nvidia on 7x was that by 2027 Hynix might earn KRW 58,000/share. We took an optimistic view versus consensus, which was that 2027 earnings would be 20,000-30,000, a decline from 2026.

‘Commonsense wisdom’ at the time was that 2025 earnings were a bubble and would collapse by 2027. The view was always that memory was a bubble, with no appreciation for how incredibly complex HBM4 was becoming and how, far from becoming a commodity, it was becoming a one player game where only SK Hynix could reliably make them. Over the last 12 months that ‘memory is a bubble estimate’ has been revised up 5x to KRW 200,000/share.

The best thing is SK Hynix is still on 5.4x 2026 estimated earnings because.. you know… it’s a bubble. I own the SK Hynix GDR. I guess one man’s bubble is another man’s pay check.

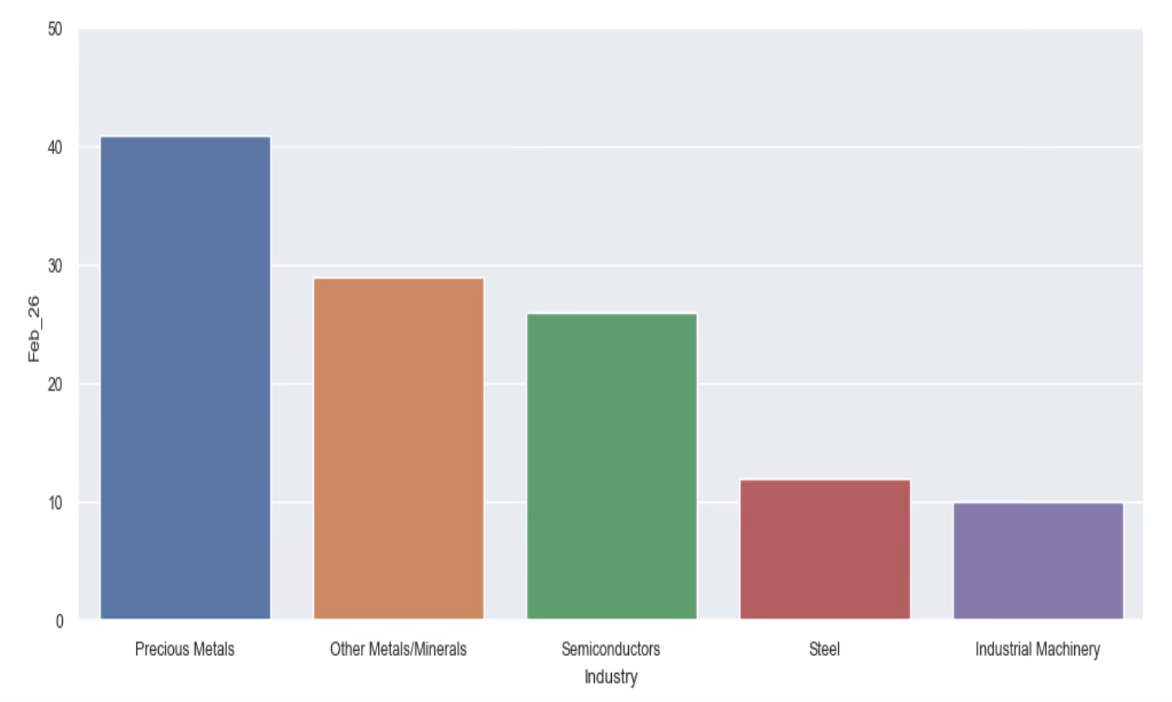

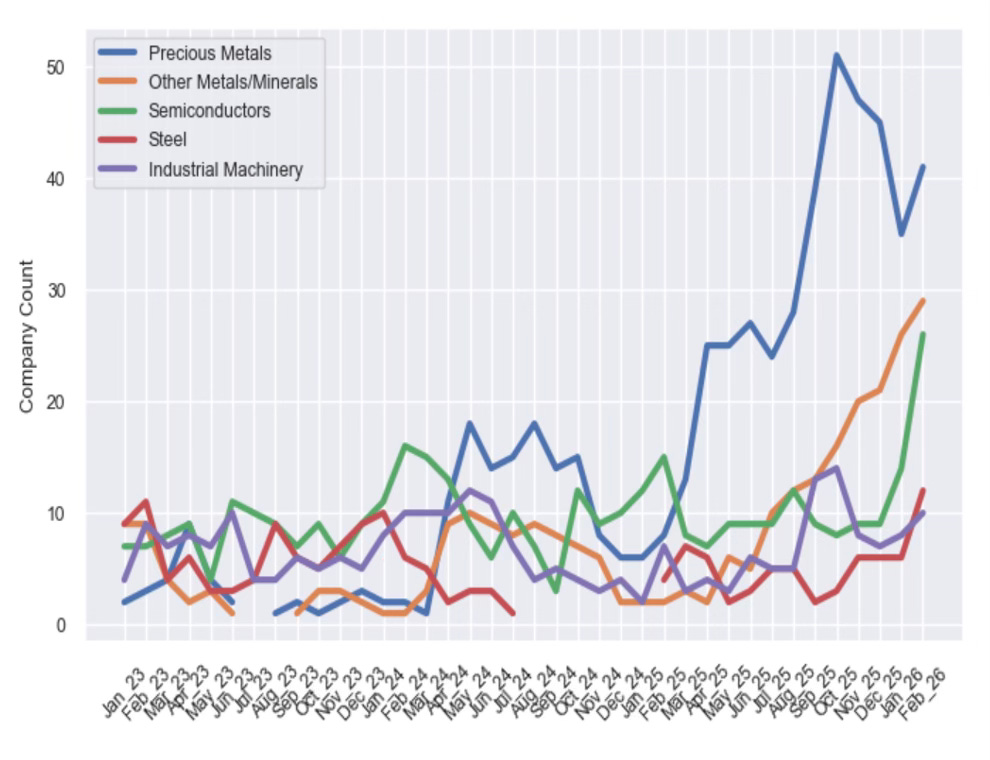

Top 5 Ranked Industries

Look at the best ranked sectors in the world. This has to be a bloodbath for the large hedge funds and family offices. Aside from semiconductors there is no tech here.

We will talk more about steel below.

Semiconductors and everything to do with them continue to be in ascent, which makes sense. I see lots of people buying new super spec’d out computers and MacMinis to run their Clawdbots. A new hardware cycle is underway.

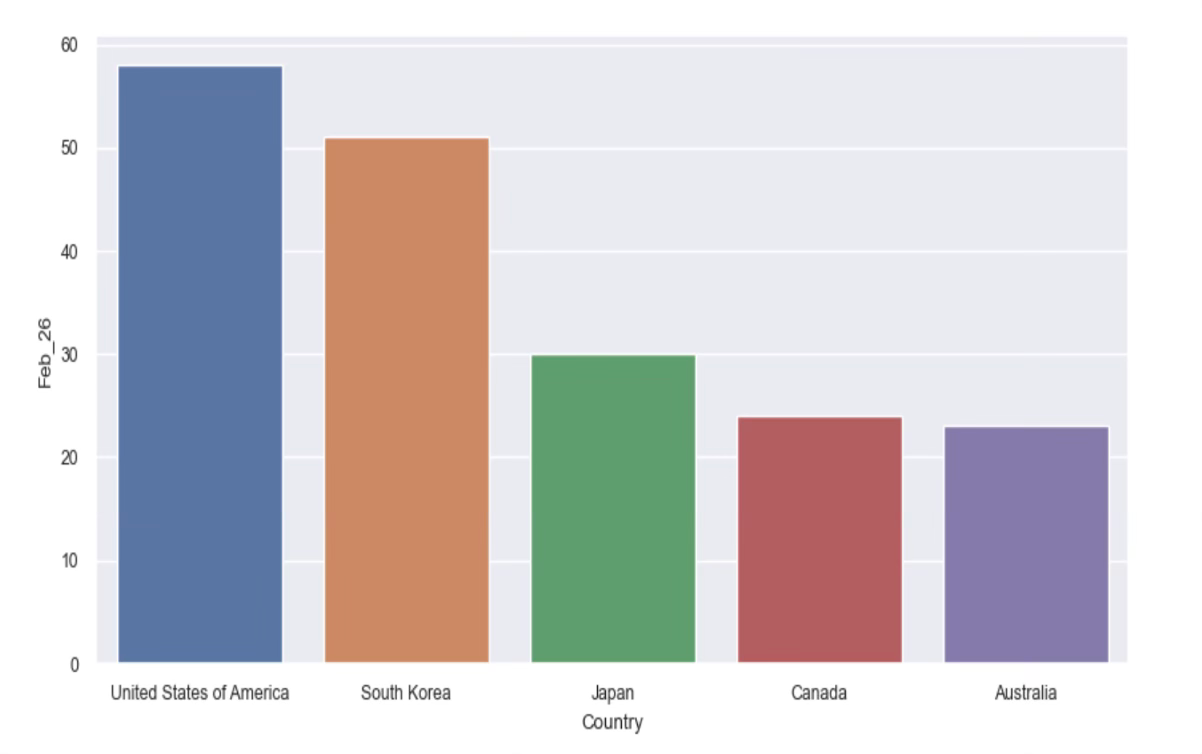

Top 5 Ranked Countries

Korea. I see you. I love you.

But what really needs more attention is Japan. Massive market, in all the indices, super liquid, performing well and you never get the impression people are involved. The BofA Survey shows the same thing. Probably everyone worried about bond market and not realising rising yields are a good thing. It’s a sign of growth.

It’s also notable that China dropped out of the top 5. First time I’ve seen that happen. I’m quite sure it’s just resting and will be back.

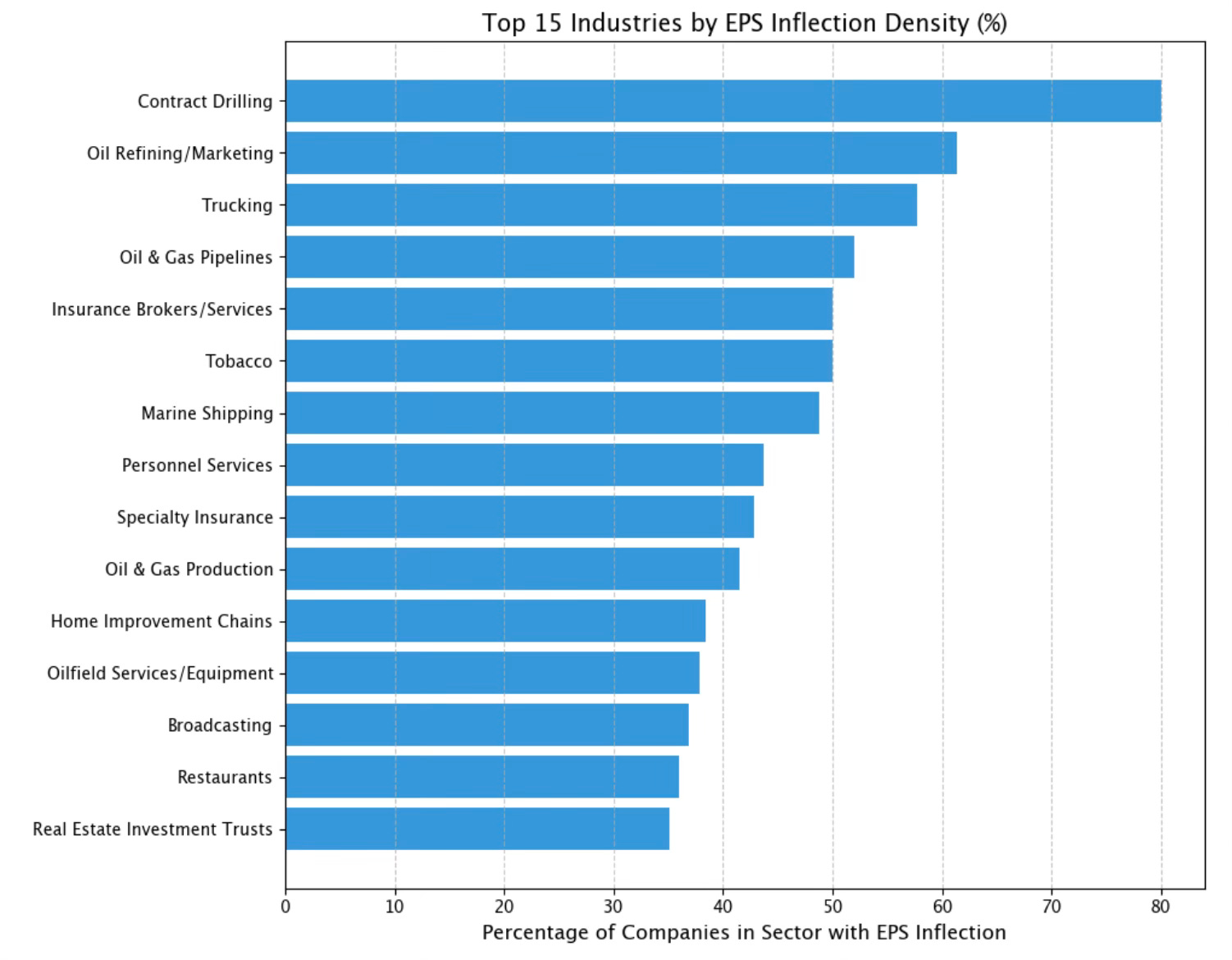

Top Inflection Industries

The problem is our trends are all working too well.

We need to find fresh meat.

Which is why in December we started searching for earnings inflections (Global Inflections). Where have earnings estimates been in a down turn, or flat, and recently turned upwards?

When you quantitatively screen for these earnings inflections what do you find?

It’s almost all heavy industry. Contract drilling, refining, pipelines, trucking, shipping, oil and gas exploration. HALO.

I included a worksheet at the bottom with the top 4 inflection companies for each of these industries.

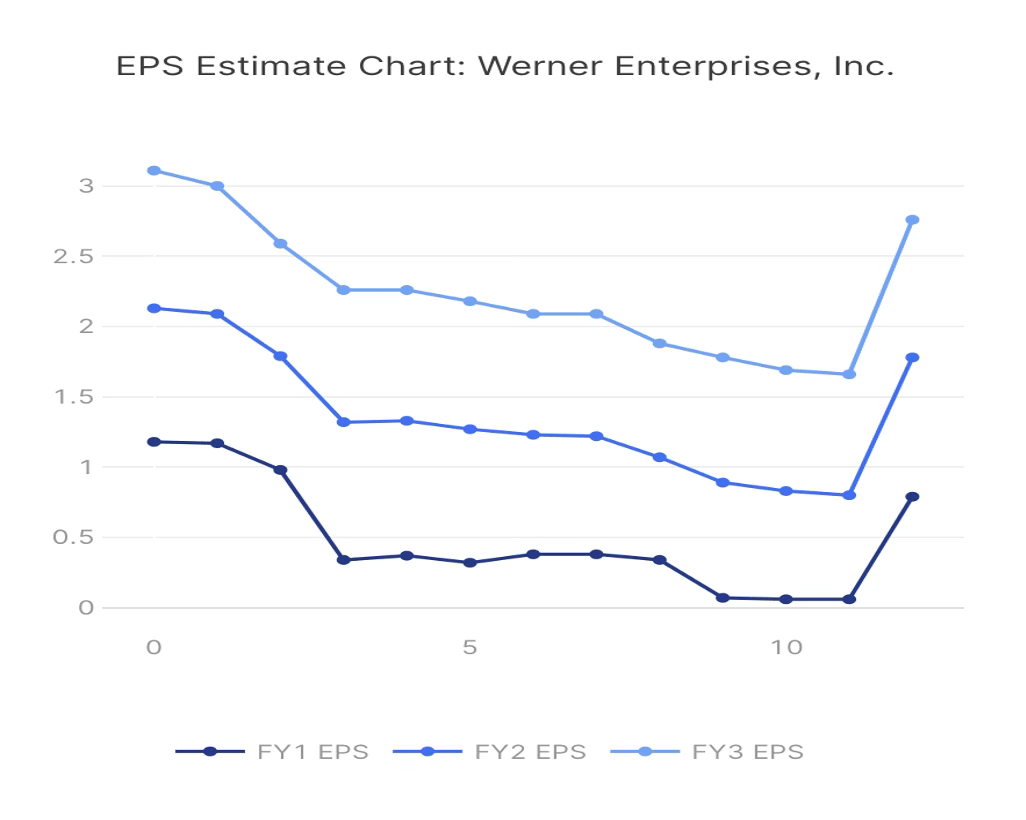

But first, what’s going on with trucking? Werner, Knight-Swift, Heartland. Earnings all inflecting at the same time, for all years.

My guess was Trump’s enforcement of immigration law and English proficiency for commercial drivers licenses is taking drivers for 2nd tier companies out of the industry, tightening capacity.

That was my guess, so while I wrapped up something else I asked Stevie (@stevie_ywr_bot on Telegram) to go read the WERN and KNX transcripts and tell me if this was the case.

Turns out it is.

We are in the early stages of a bull market for trucking.

1. English Proficiency Rule: Nearly 12,000 drivers put out of service since June

2. California Non-Domicile CDLs: 17,000 potentially expiring in March

3. New York: Similar “17,000 expiring soon”

4. School Closures: 3,000 schools recently removed for non-compliance, 4,000 more on notice

5. Temporary Protected Status (TPS) Ending: Multiple countries (Somalia, Ethiopia, Haiti) = trucking population reduction

Adam Miller at Knight-Swift.

“Regulatory enforcement of qualifications and safety standards was arguably the most welcome development in 2025 for our industry.”

“The influx of capacity from 2021 to 2024... has distorted pricing behaviors and cyclical patterns. The ongoing efforts of the FMCSA and DOT... should have an outsized impact on the lowest priced capacity in the one-way truckload market.”

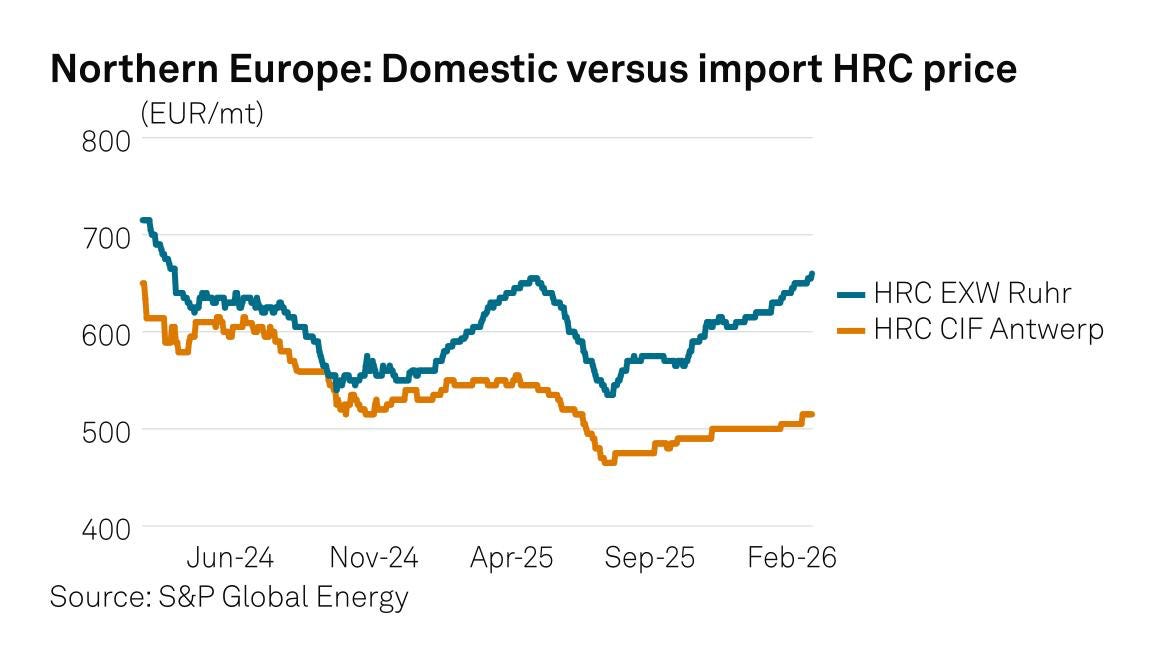

Buy Steel, Sell AI

Regulatory changes are also creating a bull market in Steel.

For decades Western steel mills were crushed by cheap Chinese capacity. But now the walls are going up. The US imposed 50% tariffs on steel and aluminium. Europe, which loves to criticise US tariffs, enacted their ‘Carbon Border Adjustment Mechanism’ in January.

Which is why you are getting a bull market in US and European HRC, while Chinese steel is flat on its back.

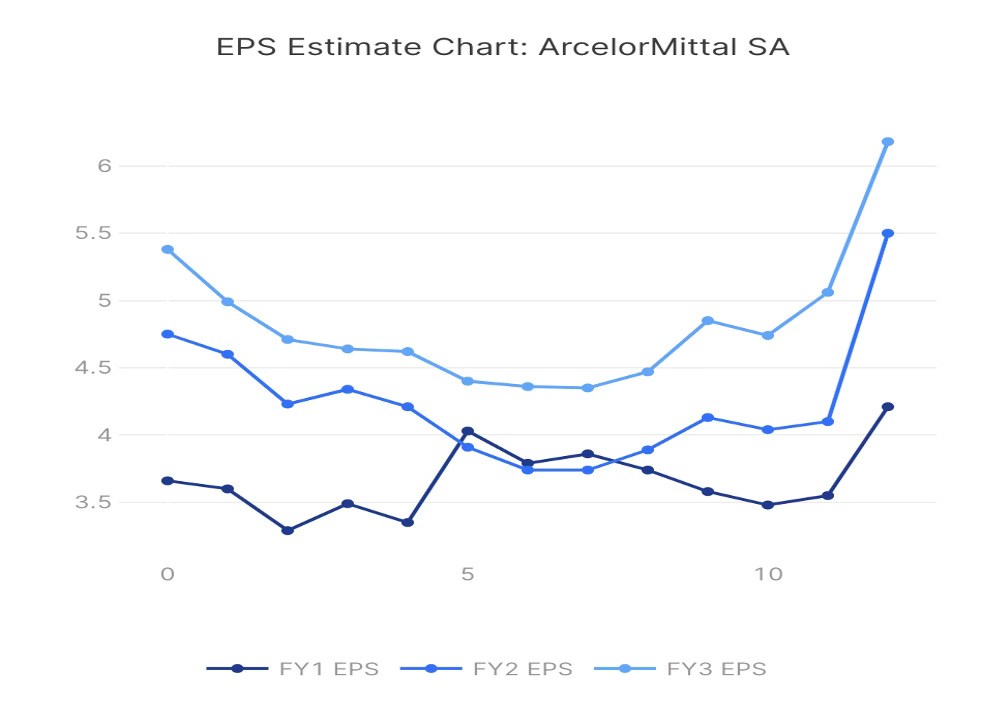

And steel EPS estimates are rising.

Connect the dots. We have severely retrenched domestic steel capacity in the US and Europe, which is now protected by high fences of tariffs and carbon border adjustments while demand is picking up. We have defence spending, stimulus, and banks lending again (It’s happening), plus a record average vehicle age.

Could this be a once in a generation bull market for beaten down US and European steel companies?

While all the supposedly smartest investors in the world are masturbating about AI on WhatsApp, should we be out buying Nippon Steel, Aperam, Cleveland Cliffs, Arcelor Mittal, Outokumpu and ThyssenKrup?

This is the great age for active investors (Untouchable #9). The whole world is getting turned upside down and few see it. Thankfully we have our data tools to keep nudging us in the right direction.

Below are all your data tools:

Global Factor Model rankings sheet

Global Factor Model Data App with AI reports and Estimate revision charts.

Factor Model Tableau Dashboard for sector level data.

New! Top Inflection stocks by industry.

February Bonus!! Top Inflection stocks by Country. Find out why Finland could be the new Korea.