YWR: Global Factor Model

It’s Global Factor Model day where we review the global trends in estimate revisions, valuations and price momentum.

As a reminder, the YWR Global Factor Model ranks stocks on earnings estimate momentum (relative to entire universe of 3,300 stocks), valuation (relative to sector) and price momentum (relative to universe).

YWR Global Top 40

Usually, I just show the Top 20 ranked stocks, but I have to admit… I didn’t find the Top 20 very interesting. Many of them have run too much for my taste. This is a symptom of the high level of momentum in the market right now. It’s harder to find stocks with rising estimates and good valuations that haven't already had a strong move.

So I expanded the list to the Top 40… and that did the trick. It brought up some gems. Corebridge and Eurazeo look interesting, and we own Unicredit in Dirty Dividends, but then right at the bottom..

Emaar and Saipem.

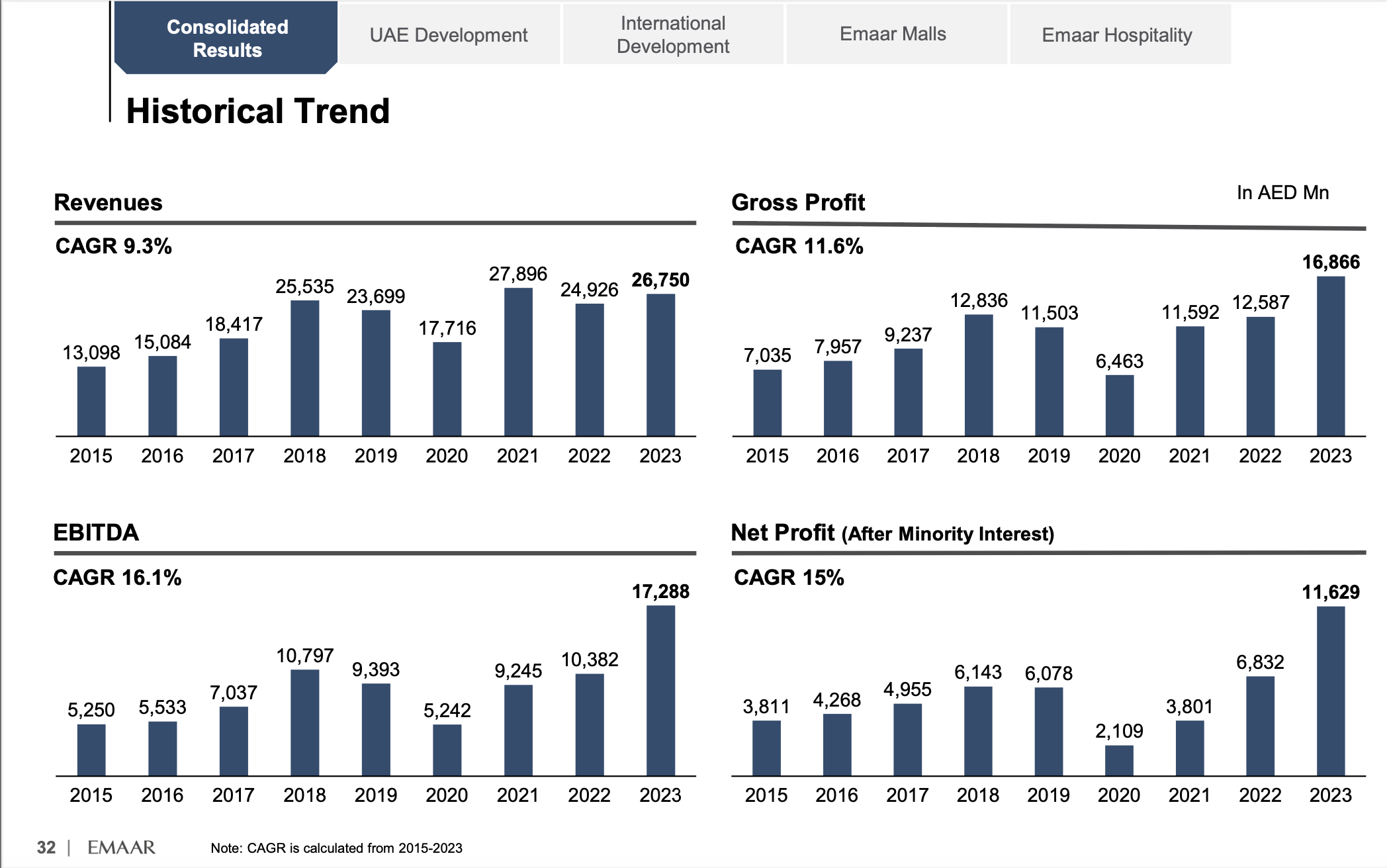

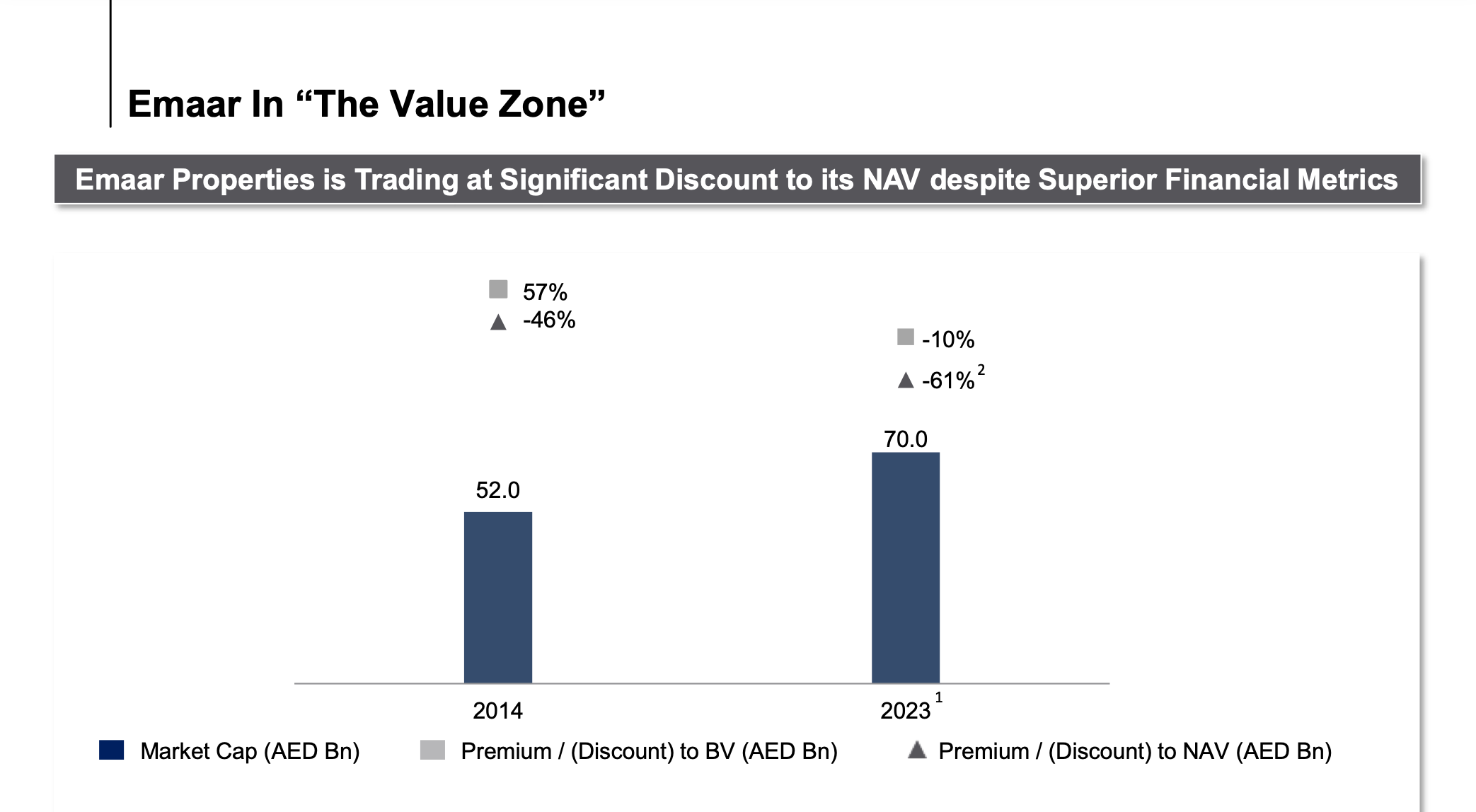

Emaar

Dubai is one of the most dynamic cities in the world and it’s a great deal to be able to buy its biggest property developer and owner of shopping malls and hotels for 6x earnings. Emaar IS Dubai. Their signs are everywhere.

As the world fragments, Dubai will continue to grow. It’s one of those frontier bridge cities which will be of increasing value in the future. These are the cities where you can do business across different geopolitical spheres. Singapore is another.

After a 14 year bear market in Dubai the shares are finally back to the previous 2014 highs and yet the business is 3x larger in terms of EBITDA and Net Profit.

Back during the last bull market EMAAR traded at at 50% premium to book value per share. In 2024 the share price has recovered, but is severely lagging the fundamentals.

And Emaar is not just property development, which is highly cyclical and unpredictable, it also has stable earnings from the malls, hotels and leasing, which contribute 48% of EBITDA. Dubai Mall at 6x earnings is a steal.

But maybe you aren’t set up to trade Dubai.

In that case… we have something special on our radar...

Saipem…

Welcome my friend. We’ve been waiting for you.

After years in the desert it appears Saipem is turning itself around. Revenues, EBITDA and free cash flow are increasing. The backlog is growing too.

Offshore drilling and construction has been a highly depressed sector for years and much of the sector went into bankruptcy. Few investors even look at this sector anymore. The consensus view was that offshore drilling was an industry with no future. On the path to Net Zero, we will just run off the existing fields and have very little need for new field development.

But the positive of this widespread distress, and lack of new investment, is that there will be capital discipline even if things start to improve and all the players are making lots of money. It will extend the cycle.

And as we will see below, Saipem isn’t the only driller starting to show momentum.

Industry Trends

We’ve had a real shift in momentum. Banks are still the most represented sector in the YWR 300 top ranked stocks, but semiconductors and Pharma are catching up quickly.

Top 5 Industries

I don't know what to do with semis. I got negative on them because of the enormous capital cycle underway, but maybe it is justified. I think we all need to understand this sector better.

But I don’t like to chase, so I look for other trends which could be interesting.

Aerospace and Defence sticks out.

Aerospace first came up in January in How Consensus is your Hedge Fund when we noticed Chris Hohn had blasted his Microsoft to buy GE. We noted his very high level of Aerospace exposure and remarked that he has traditionally been good in this sector and must have a strong view. Then Aerospace came up again in 7 reasons interest rates go higher when Eaton’s CEO was saying it is one of their best industries.

At the bottom of the post is a link to the full YWR Global Factor Model results. Go in and filter for Aerospace and Defence and tell me what you like.

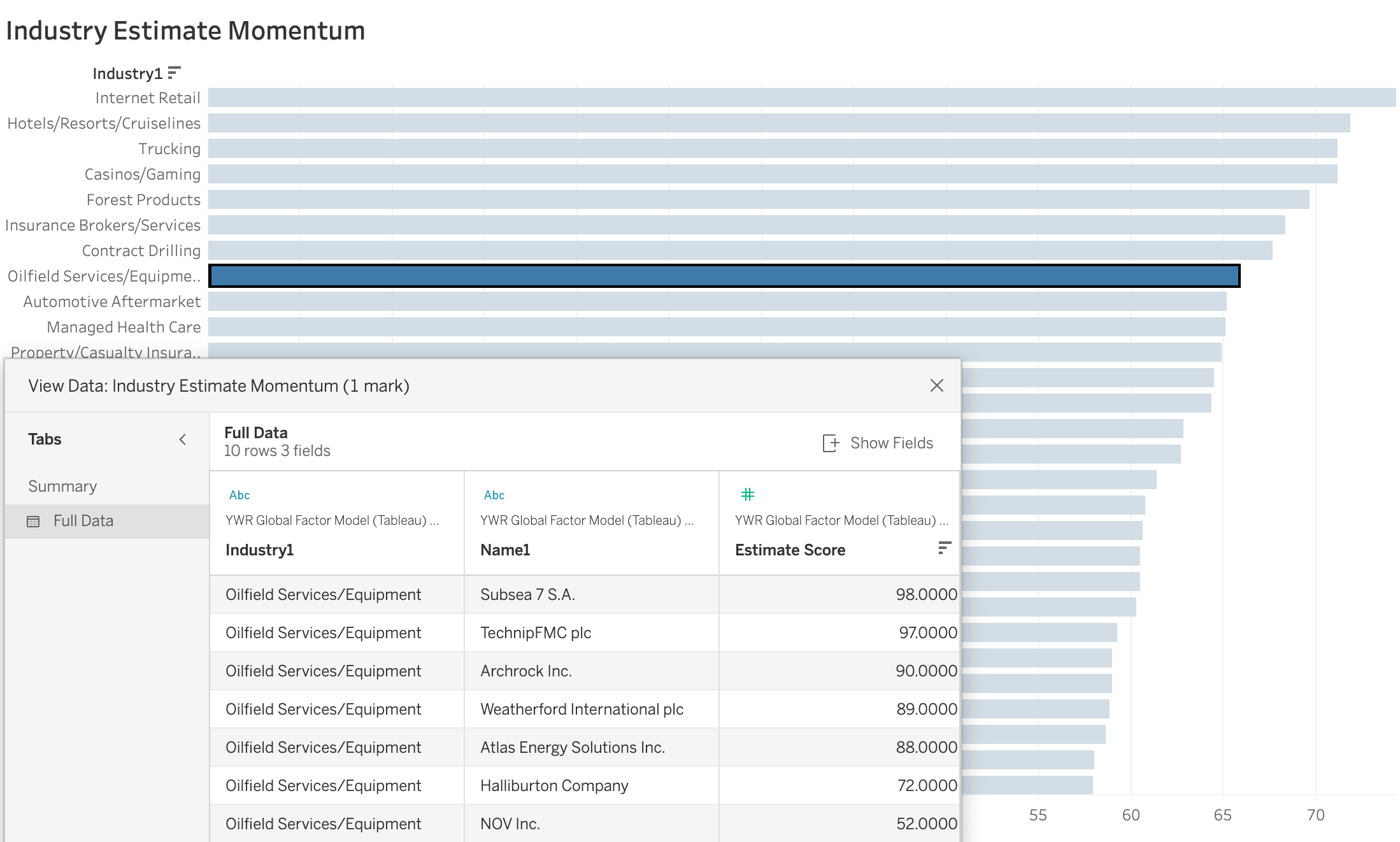

But back to offshore drillers.

If we use the YWR Tableau Dashboard (link at the bottom) and ‘drill’ into just the estimate revision factor we see Contract Drilling and Oilfield Services have some of the best earnings estimate momentum in the entire market.

It’s Valaris, Transocean, Noble and Baker Hughes.

Then in Oilfield Services it’s Subsea 7 (competitor to Saipem) Technip, Weatherford and Halliburton.

Alert!

Drillers and Oilfield Services…

What we have here is a sector showing strong earnings momentum, which hasn’t had a big move and which few people own.

Put that on the buy list.

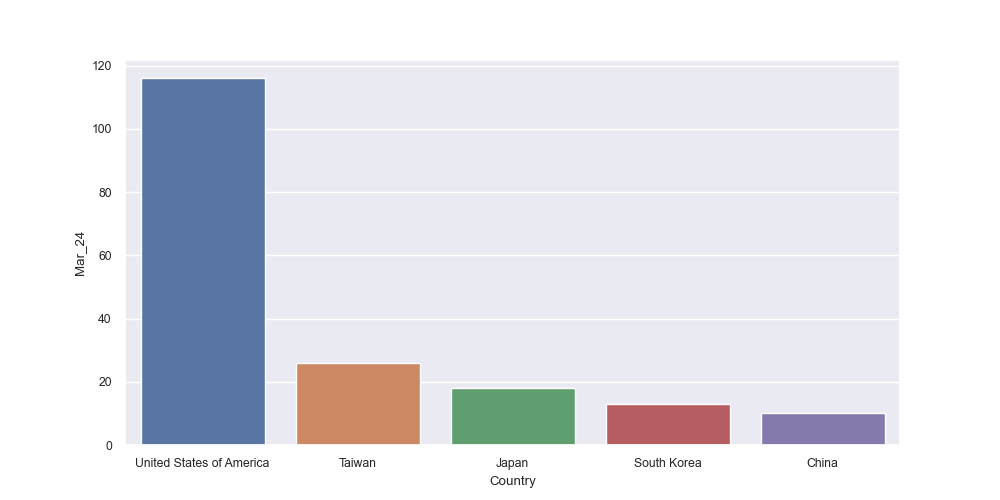

Country Trends

Two trends stick out at the country level.

The complete dominance of the US.

Asia is the new Europe.

I don't like that when I go through the Top 20 list I don't really know all the South Korean and Taiwanese companies. It’s a gap for me. And you probably have it too. We’ve all spent too much time looking at the US and Europe. We need to up our game on Taiwanese electronics companies.

Below is the full factor model with rankings for over 3,000 stocks.

Also is a link to the Tableau Dashboard which is a visual representation of the date.