YWR: Global Factor Model

Great pianists practice scales to keep sharp.

For us its the monthly review of our global ranking models (GFM and QARV).

And today is Global Factor Model Day!

At the bottom of the post are links to all the data and the data tools.

Rankings Sheet with scores on Estimate Momentum, Value, and Price Momentum for over 3,000 global stocks.

Tableau Dashboard with Estimate/Price Scatter and Sector Level Data.

Retool Data App for screening and sorting the Global Factor Model rankings. Plus a useful visualisation of each stock’s estimate revisions.

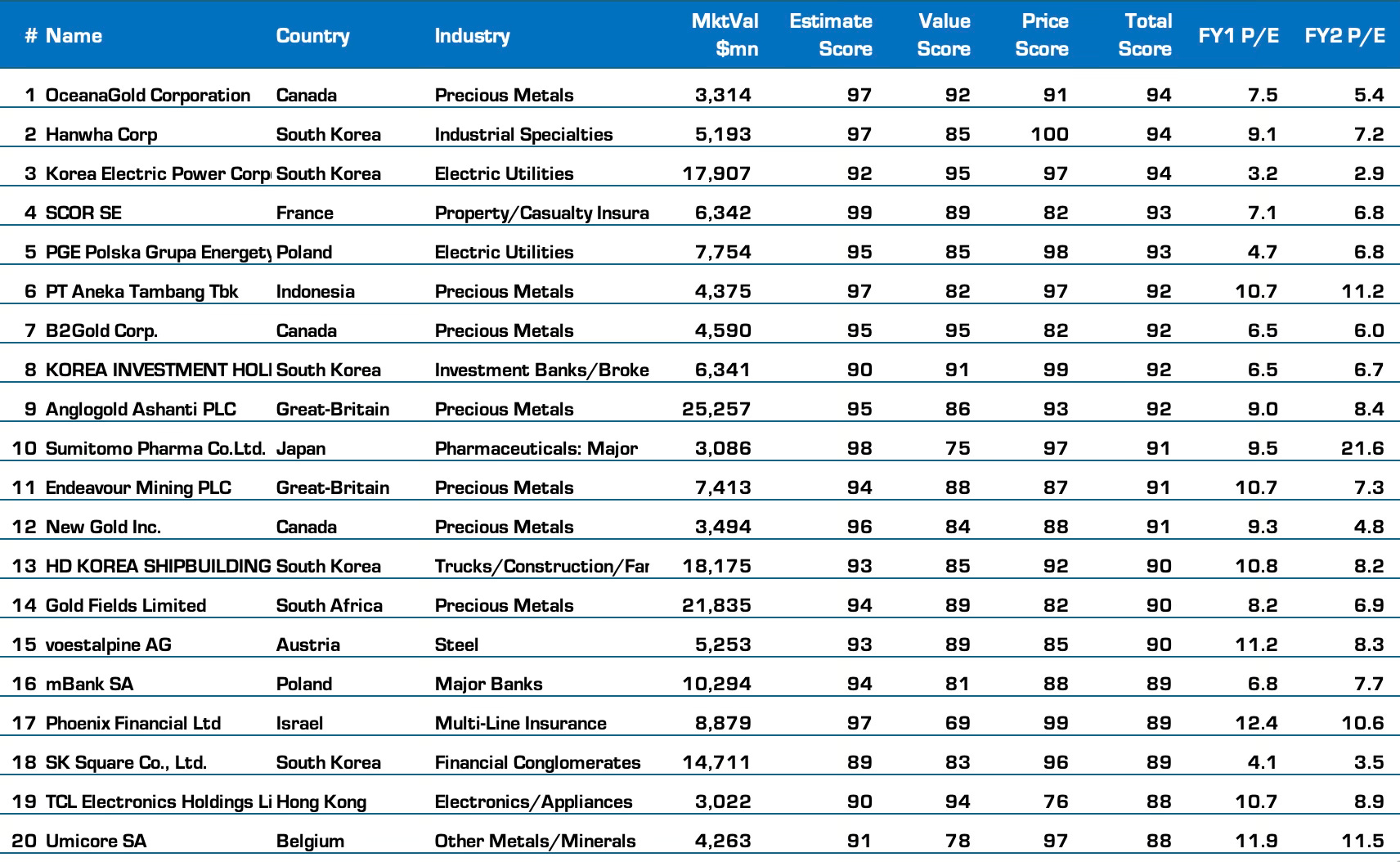

Let’s start with the top ranked.

BTW, I’m filtering out Chinese stocks, because there are so many…. China is actually the #1 ranked country in the world. But we’ll get to that later.

Top 20 Ranked Stocks *(Ex-China)

What do we see?

Lots of gold miners. Gold mining.. the Number #1 ranked high momentum sector hedge funds don’t own. Nice.

Then lots of South Korea. We love South Korea.

We’ve flagged Korea Electric Power before at 3x earnings. It even has an ADR KEP 0.00%↑. The story is that the South Korean government is allowing KEPCO to raise prices in order to earn higher profits so it can deleverage from the COVID period when it kept rates stable and lost a lot of money. The government also realises if Korea is going to lead in AI, power generators need to be able to make money. So earnings are surging at KEPCO and the market isn’t sure what P/E to put on it. The concern is what if there is pressure to lower power prices again.

But there is an interesting new angle which will appeal to the nuclear bulls.

KEPCO might be a key contractor for new US nuclear power plants.

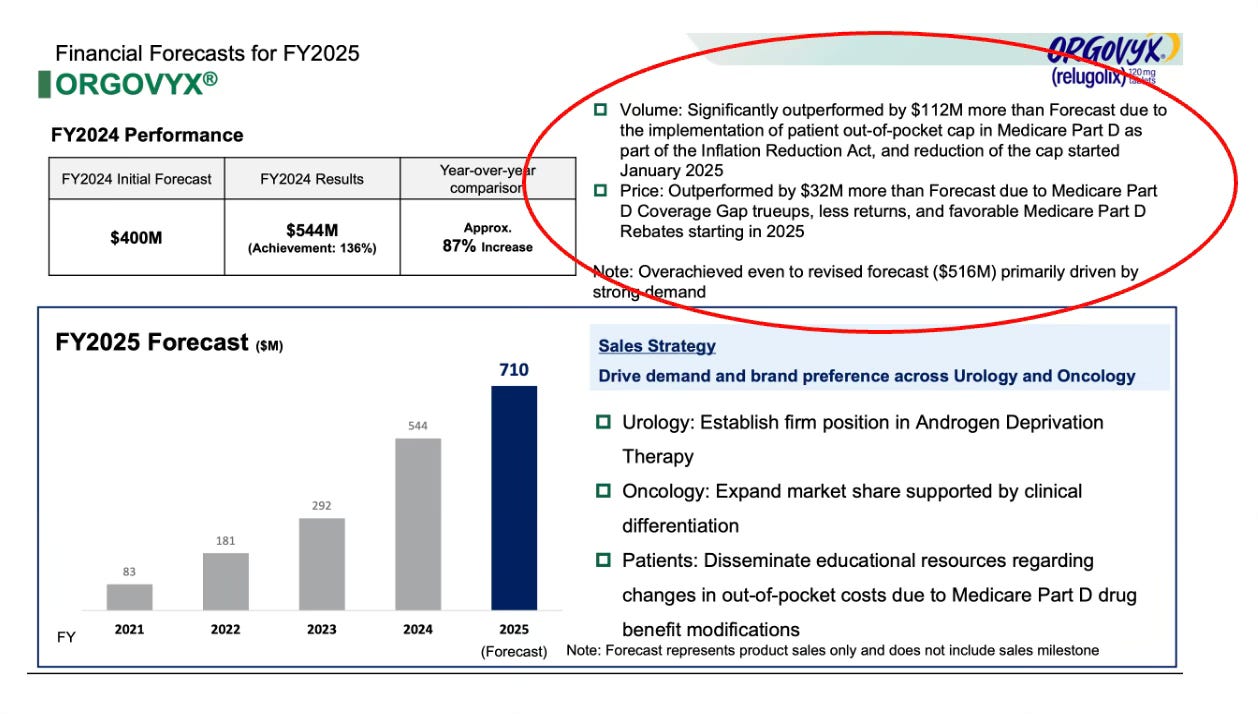

At #10 Sumitomo Pharma is worth flagging because it’s the first time I’ve seen a company confirm our thesis why specialty drug volumes are surging.

Back in April we noticed the surprising surge in earnings momentum for specialty pharma stocks (Factor Model Mystery). We thought it strange these niche drugs were suddenly exploding in use. No one was saying this on the conference calls, but our guess at the time was that it had to be insurance related and most likely due to the changes in out of pocket expense for patients enrolled in Medicare which kicked in this year as part of the 2022 Inflation Reduction Act.

Sumitomo Pharma confirmed this is what is going on. They have a March 2025 year end, and so they reported ‘2024’ sales of their advanced prostate cancer drug grew +87% yoy. They confirmed this was due to changes in Medicare Part D out of pocket expense. Their forecast is that March 2026 sales will grow another +30%. That’s 143% growth in a prostate drug in 2 years.

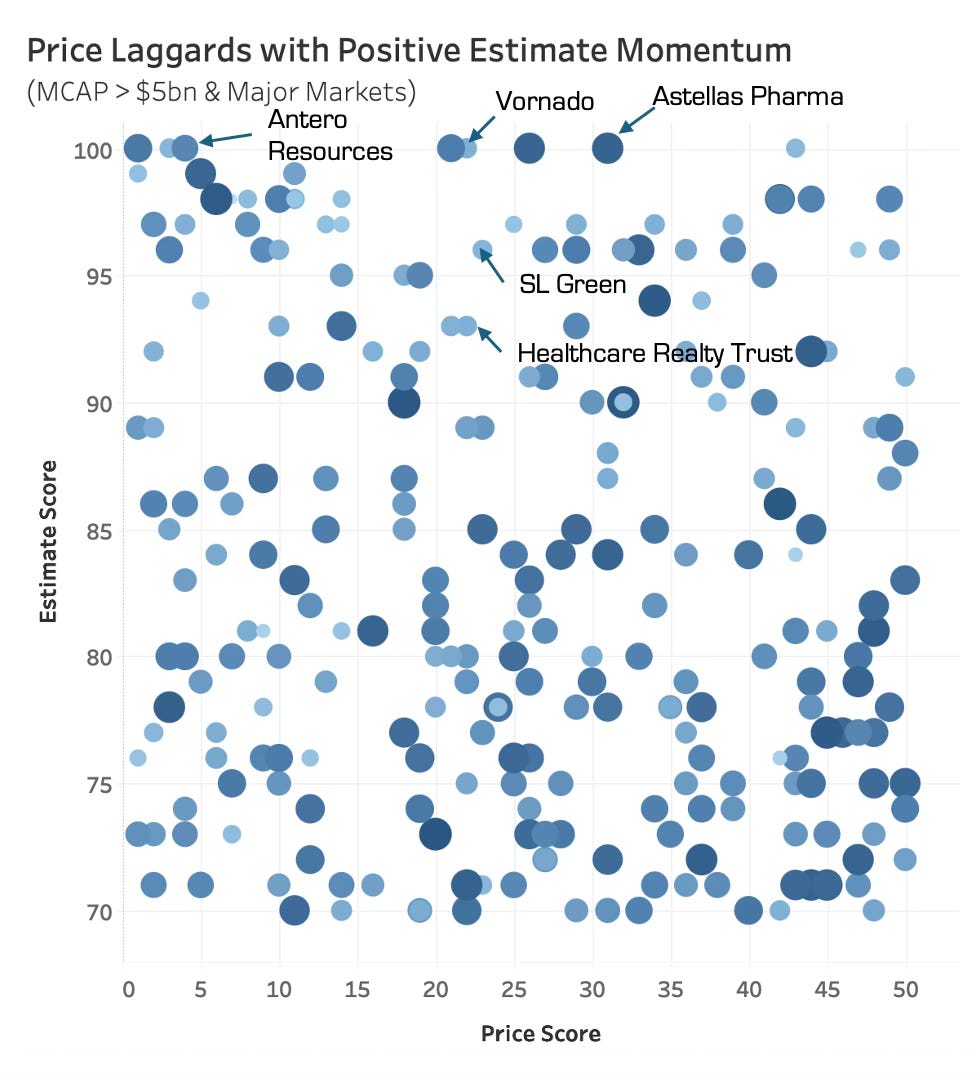

Strong estimate momentum with Low price momentum

I created a useful scatter chart for you in the Tableau Dashboard.

It screens for stocks with strong estimate momentum scores, but low price momentum.

You have to always double check the actual data with each stock, but it is meant to flag interesting improvements in estimates where the stock hasn’t moved yet. These good be good set-ups.

And you know what is showing up on the estimate/price scatter?

REIT’s.

It’s the most hated, underweighted sector, along with energy, and yet estimates for several of the REITS are gradually rising. Estimates are rising, but without much change in price relative to the market.

In the Tableau Dashboard you can hover over all of the dots, but I flagged a few for you. Vornado, SL Green, Healthcare Realty Trust. Kite Realty and EQT also show up.

It’s interesting because in Time for a Garbage Rally we flagged REIT’s as a potential sector which could benefit from a Fed rate cutting cycle.

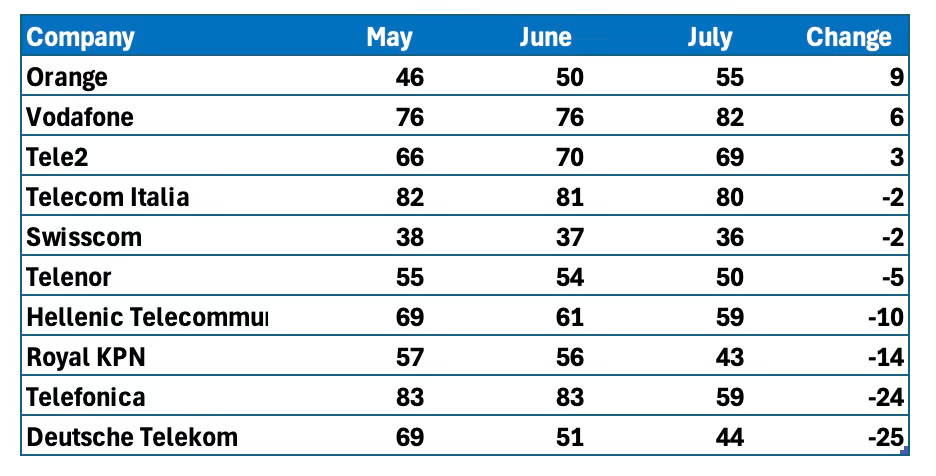

Telecom Momentum Update

We’ve been keeping an eye on the European Telcos because of two potential inflection points. 1. Rising free cash flow driven by falling 5G capex and 2.support for higher European Telecom profitability from Mario Draghi (A Secret to Making Money)

Despite the interesting big picture, signs of improvement within European telecoms are minimal.

And when we look at the trend in the factor model scores over the last 3 months a totally different story emerges.

And not the story anybody is talking about.

Why are the rankings for Orange and Vodafone improving while the others are declining?

What is the common feature to Orange and Vodafone?

Africa. They both have good sized Africa businesses.

Africa growth is saving them.

Look at the 1H results for Orange. Where is the growth?

Then look at the results presentation for Vodafone.

African data usage and mobile money usage are booming. It’s why the pure plays MTN and Airtel Africa are also top ranked stocks.

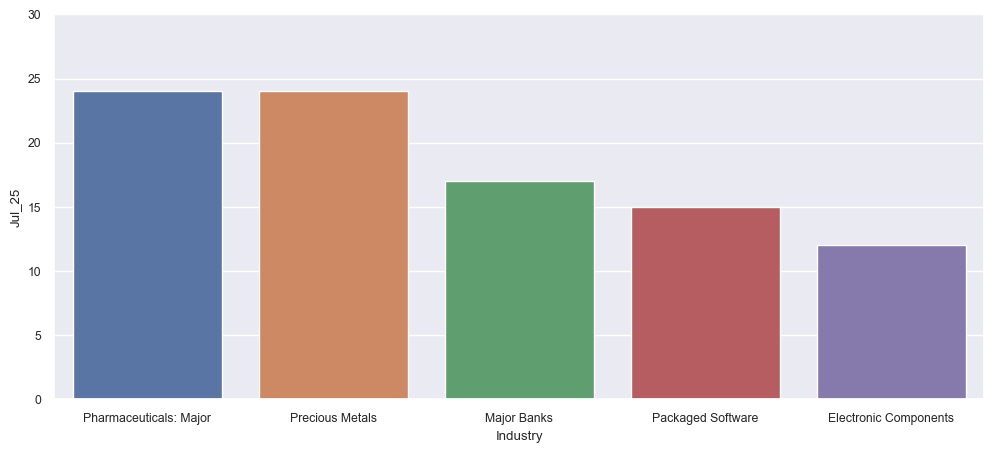

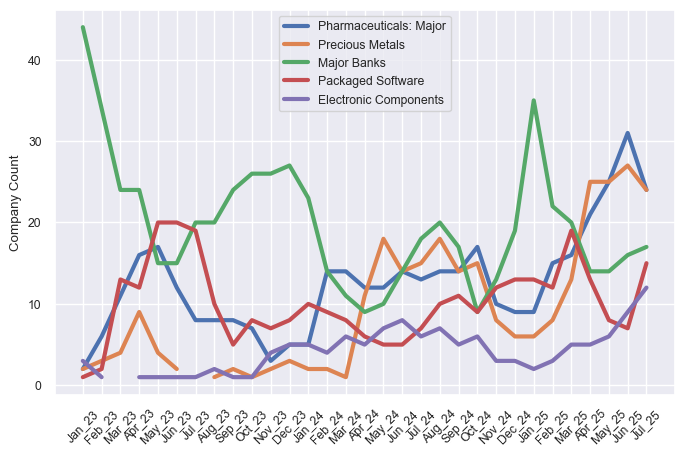

Sector Level Trends

We’ve said before Pharma is the biggest estimate momentum story nobody is talking about. It ranks even better than the gold stocks.

The Packaged Software trend is mix of gaming stocks from Korea (Netmarble, NCsoft), but then quite a few Chinese software companies.

Then the electronic components stocks are a lot of semi-conductor supply chain companies in Taiwan, China, South Korea and Japan. In the US TTM Technologies (TTMI 0.00%↑) and Amphenol ($APH) rank well. On of our views-in-progress is that hard tech is taking over software and internet services as the new momentum sector in technology.

Pharma has overtaken leadership from the Banks as the top ranked sector.

You see the monthly rise in the rankings of Electronic Components companies.

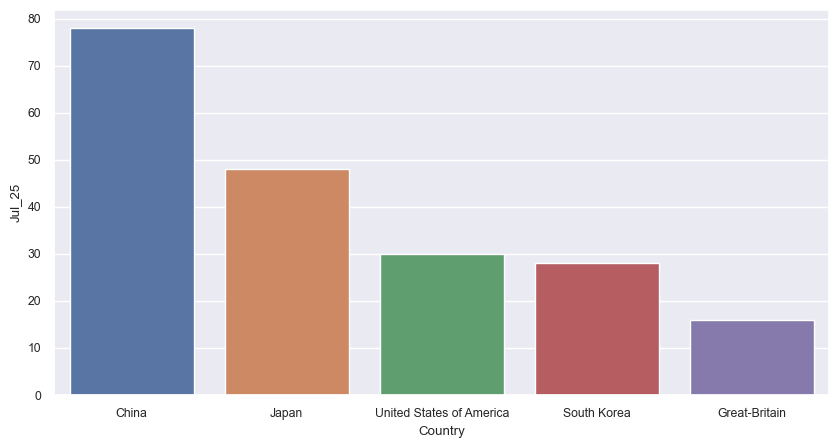

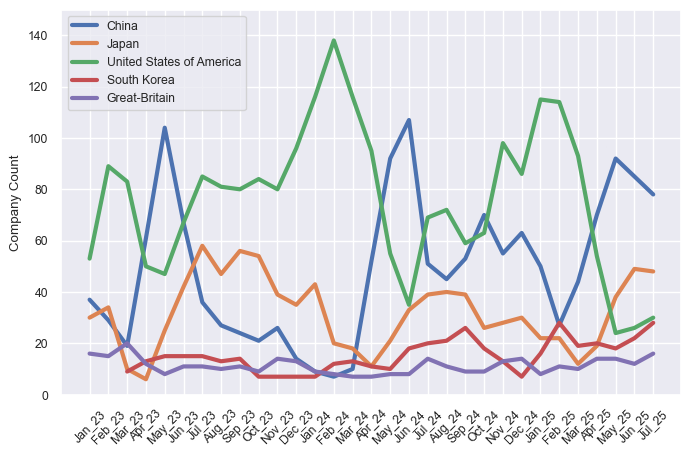

Country Level Trends

The top 3 podium is the same as last month. #1 is China (biggest market nobody owns), followed by Japan (another not well owned market), followed by the US.

South Korea (another market nobody owns) is still #4, but Great Britain overtakes Canada for the #5 slot.

At YWR we are pivoting to Asia. Focusing on it more, going there more, investing more.

The Korea momentum is widespread, but we also got some helpful news for Korea’s biggest stock, Samsung. Samsung has been struggling to get any momentum in their foundry business and lost Apple as a client, but this week Tesla announced they are going to produce their new AI chips using Samsung’s fab in Taylor, TX. It’s a $16.5 billion contract and a massive vote of confidence for Samsung. The market didn’t react as much as I think it should have. This is going to play out well for Samsung in the years ahead. In YWR Portfolios we own the ishares Korea ETF and Samsung has a 21% weighting.

Those are my takeaways, but there is so much data, I probably missed lots of good ideas.

Please use the links to the tools below to uncover your own insights and let us know what you find.