YWR: Gold and Gold Miners Update

An update on the multi-year bull market in gold and gold miners.

Gold and the gold miners have taken a pause here while we Make America Great Again. And Bitcoin hits $100,000.

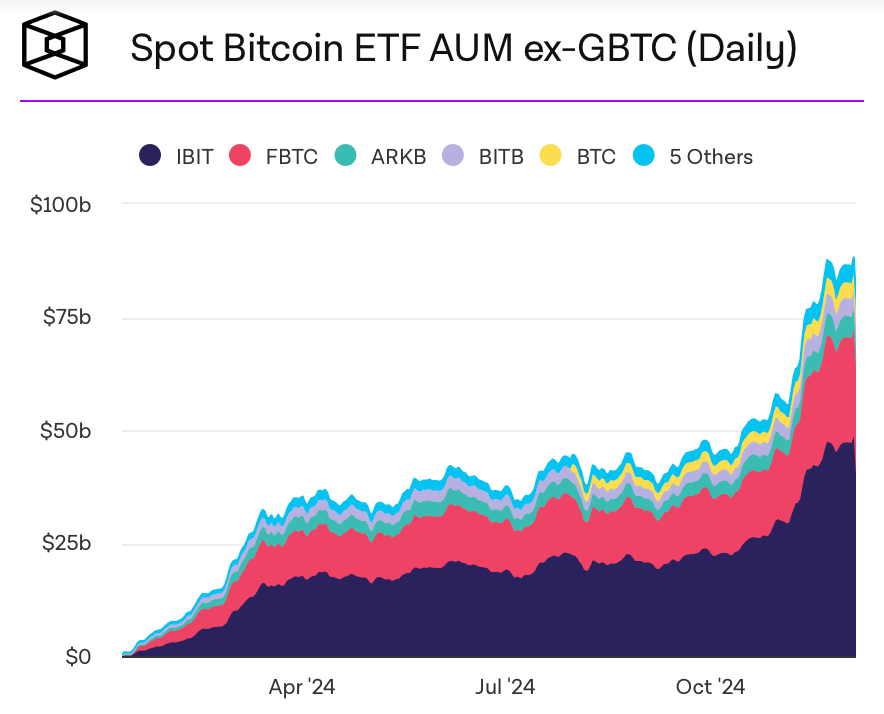

Bitcoin ETF’s were approved in January and already the AUM are over $75bn.

Meanwhile, despite the move up in the gold price there has been no increase in ounces held by gold ETF’s.

So what’s up with the gold rally? Is it still happening?

Contrarian Positive

Actually, the set up is great. I love that retail is chasing BTC ETF’s at $100,000 and has no interest in the steady climb in the gold price.

Meanwhile, the world’s Central Banks are quietly buying more gold than ever. And you notice how this trend kicked off in 2022 after the US and Europe confiscated $300bn in Russian assets.

The consequences of that decision are under appreciated and will continue to reverberate. US$ Treasuries are no longer a risk free asset. If you want to own them, fine but make sure you never get in a disagreement with the US about anything, or they will be zeroed.

What if the Best is Yet to Come?

Gold’s climb to $2,700 has been a series of gradual ups and downs, but what if 2025 is a lot more explosive? What if the real move is still to come and gold makes a move to $4,500?

Markets love to make idiots out of everyone and this would fit perfectly. We all forget about gold right when it’s positioned on the launchpad. What if by June 2025 retail investors are scrambling to sell Bitcoin ETF’s and Hawk Tuah coins so they can chase the gold market?

It’s hard to have the imagination to see these things, which is why I encourage you to listen to our talk with Jeremy Gray ($4,500 gold with Jeremy Gray). Jeremy says despite a gold price over $2,500 nobody trusts the gold bull market, nobody wants to get sucked in, and nobody wants to invest in the gold mining sector. He knows because he meets with all the funds and they don't care about gold mines at any price.

He sees gold making new highs in 2025 while industrial commodities languish.

“I genuinely believe, most in the market don't believe this rally. And that's why I'm so bullish.”

“No one wants to get sucked in, right?”

“Don't want to get sucked in. They've lost money on the sector. They made money on Apple and Nvidia and Bitcoin. They just are nervous to get involved. And that's why we called for a $2,800 gold price by the end of this month and $3,500 within six months. And $4,500 by next year.”

Jeremy’s Gold Price Forecasts

What about the Gold Miners?

The miners have been a mixed bag. Earnings results for Agnico, Kinross, and Royal Gold have done well, while others like Newmont and Goldfields have been a bit disappointing. And the headwind for both miners and royalty companies has been a steady derating of the sector. EPS is rising, but P/E’s are falling. For example, it’s rare to see Barrick and Newmont on P/E’s of 10x 2025.

I’ll get into some company specific thoughts below, but I want to lay out more general sector comments first.

There has been criticism that the gold mining results are disappointing. Costs keep rising too much. There isn’t as much operating leverage as expected give the move in the gold price. The miners are giving too much away in higher costs.

OK. But for all the criticism that results aren’t good enough, earnings estimates for the miners are rising. Apparently, for all the supposed disappointment they are still better than expected. Statistically, this combination of positive earnings revisions and low valuations looks good.

I also think that to some extent we shouldn’t be too nit-picky about the 2024 results. When a sector has been in a bear market for a long time the companies are not in great shape. They’ve been hanging on by a thread, trying to scrape by and make numbers each quarter. When things finally improve and they are making decent money there is a lot of catch up to do. There is machinery which needs to finally get fixed. There are employees who have patiently stuck around and need a raise. All these built up expenses come through just as we investors are looking for the operating leverage come through. So we get disappointed and throw in the towel.

The reality is after you’ve been in the desert for 10 years it takes longer than you think to get things patched up. Management has to run a balancing act of showing some operating leverage, while also fixing things in the background that were in worse shape than you realised. This was a comment Jeremy made from his experience running gold mining businesses. And it’s why I take the cost increases in 2024 with a grain of salt.

It was also the same with the European banks in 2022. The bull market had started (higher interest rates), but there were annoying extra loan provisions to make and net interest margins were slow to adjust upwards. There were fixed income assets and hedges on the balance sheet which management had stupidly invested at 0% interest rates and took 2-3 years to roll off before they could be reinvested at higher rates. And all the while, even though profits were recovering, management was continually fearful there would be a recession next year, so they didn’t want to pay out big dividends. I had to stay patient and remind myself that this was a multi-year bull market. Let the companies work through their issues. The profits would come.

Where are the network effects?

One negative comment on the miners though. Businesses and business models evolve. The modern day investor is looking for network effects. Yes, I get you are a miner, you need to do a good job at mining, and that is the priority, but also don’t be a dinosaur.

None of you (I’m talking to the mining CEO’s) had the imagination to widen your scope that you were in the wealth preservation asset business, and that it would make sense to diversify into mining digital assets. Why not mine Bitcoin too? Gold and Bitcoin. Everyone missed that, but wouldn’t it have been brilliant?

OK. Maybe Bitcoin is too mind blowing for a crusty miner from Vancouver, but you can also be thinking how to build a jewellery brand, or mine financing, gold refining or a trading business. Dont’ be one dimensional. “We only build gold mines.” Investors don’t put much value on that. They don't want to hear about your geology reports and mine projects for the rest of their lives. It’s boring. It’s part of the reason the P/E is derating. Investors have moved on from that model, but the gold CEO’s haven’t.

It’s why I like Total and Glencore. I like how they are evolving. I like the network effects which come out of Glencore’s physical commodity trading business and asset financing (loans to Tullow for example). With Total I like the Integrated Energy business where they discovered the synergies (and profits) from mixing renewables with gas turbines with power trading. Total is an oil company, which is learning how to be a new era utility.

Sibanye is also thinking creatively with their PGM and battery metal recycling businesses. Maybe the metals of the future don’t just come from mines…

So that’s my advice. When the profits start flowing in 2025 try to think a touch creatively about what you do with the money. If Bitcoin is in the toilet buy a digital asset miner.

Gold Miner valuation and estimate summary

This valuation and estimate table is also available under the ‘Data and Models’ tab on www.ywr.world.

The consensus estimates are as of Dec 2, 2024.