I spent a lot of time on payment companies this week.

I didn’t find the stock idea I expected.

I was rewarded with 3 realisations instead.

Stocks need ‘communities’

Dividends might be better than buybacks

All roads lead to BlackRock, and maybe we should buy it.

Let me explain.

Two weeks ago I joined a London ideas dinner and was blown away by all the great ideas. We enjoyed great food, wine and war stories of undiscovered stocks from the past which had 5x’d. At the end of the dinner we were discussing what might be ‘the next thing’.

Which beaten up sector, or stock could be the next AST SpaceMobile?

In the end we came up with this former darling which has completely fallen from grace and is now massively hated.

Payment companies: Paypal, Fiserv, Remitly, Adyen, Global Payments, Western Union, Fidelity Information Services

So this week I spent some time looking at their results and presentations. In the end Global Payments (value play) and Remitly (still growing) looked pretty good. They will probably do well. Uzo Capital was at the dinner and is the real expert on them.

But I struggled to get excited.

I was thinking of that Buffet quote if you only had 10 stock investments you could make in your life, would this be one of them?

Not really.

It caused me to reflect on why I couldn’t get myself excited about them. Because the management teams were saying all the things you are supposed to say.

And here is what I came up with:

The whole thing sounded ‘corporaty’, all about sales channels, routes to market, returning capital, and nothing really about innovation. Nothing interesting.

No cool founder/leader. If the CEO is great, I’ll kind of invest in anything.

No macro variable which was going to change everything, like interest rates for banks, or the oil price for energy stocks. The one possibility is that the upcoming inflation surge boosts the payment volume growth temporarily from 1-3% to 3-5%.

And playing 3D chess, I was worried the rest of the US retail army wasn’t going to care about this financial sub-sector either.

Which made me reflect on what things the US retail army cares about. And you realise attention is a scarce thing and you need a dedicated constituency of investors who still care about a sector even after it falls out of favour. Tech has its Silicon Valley groupies. Mining stocks have the Vancouver Mafia. The energy sector has Texas. Cryto has its hodlers. There is even a community of investors who like investing in shipping stocks. For international stocks in smaller markets the dedicated constituency is the domestic investor base.

But who cares about mid-cap payment companies fighting for their life in a market like the US when you have stocks like Nvidia? You realise that in a market with so many choices, and the best companies in the world, payment companies fall through the cracks.

And if the US retail trader isn’t going to care about struggling payments company, then who else will?

Maybe a smart ‘value investor’ at a mutual fund? But then you realise she is getting redeemed in favour of an index ETF and doesn’t have any money to invest.

Maybe a cunning PE fund will swoop in an take these undervalued gems private. Then you realise the PE funds own a whole portfolio of similar companies and rather than buy more, are struggling to get liquidity so they can return money to their investors.

And this is where I came to my three realisations.

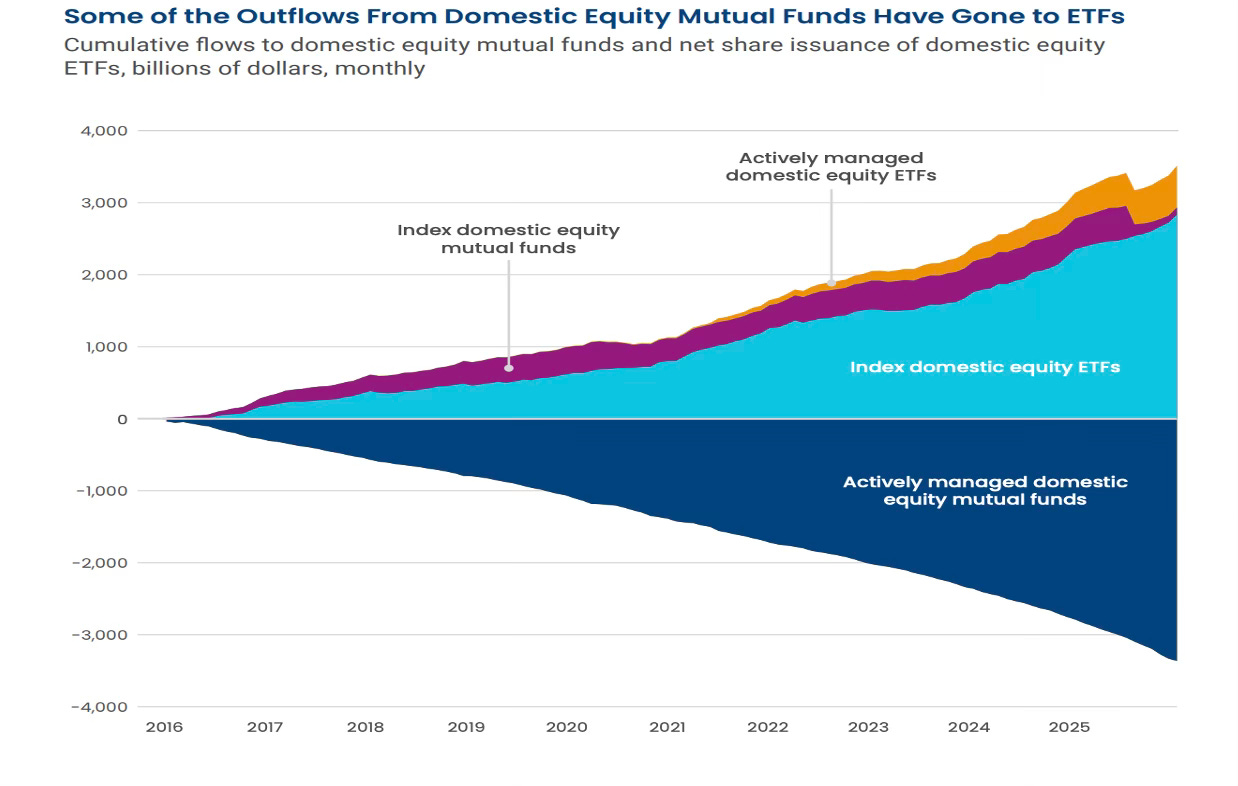

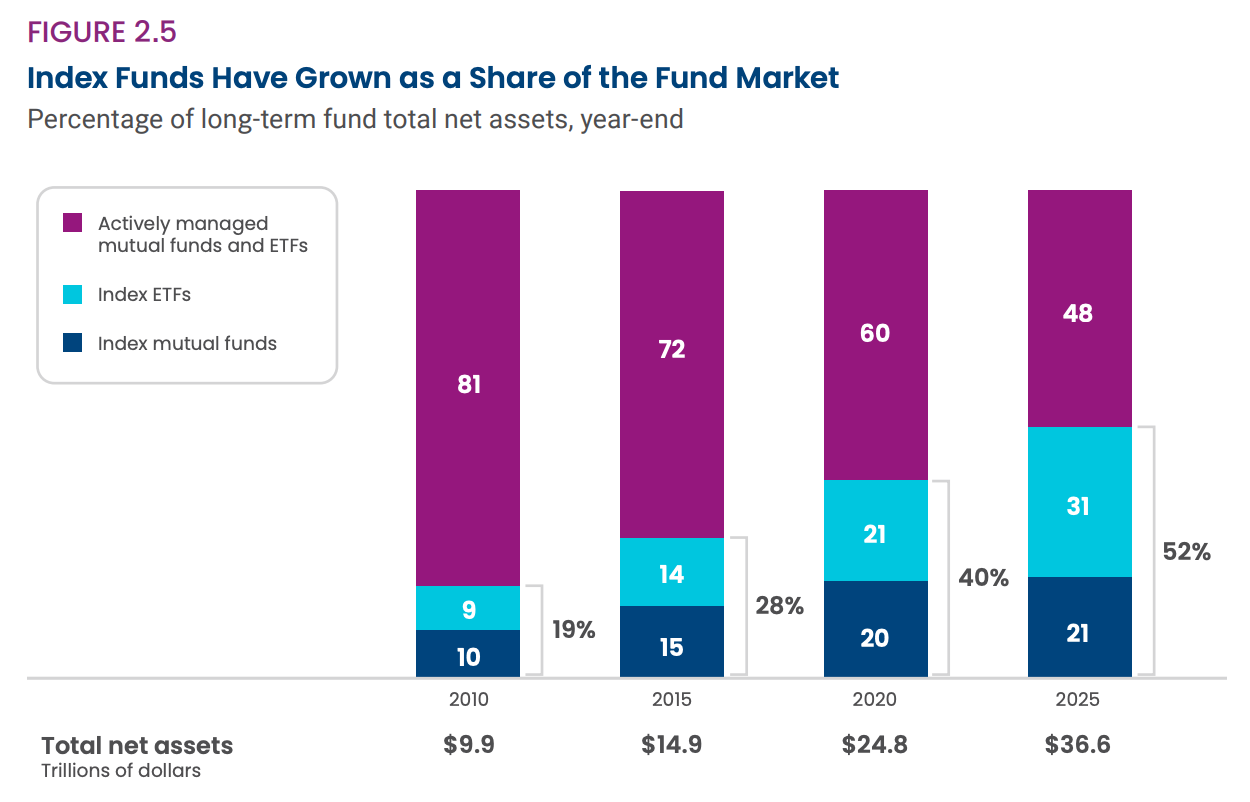

Realisation number #1: Stocks need to build ‘communities’: The active management community in public markets is under a lot of pressure. Over the last ten years $3 trillion of funds has exited active managers to buy index ETF’s.

Which means companies can’t assume there is some smart analyst at a big fund co with lots of screens and tools who is going to do the work, figure out their company is a great opportunity and buy hundreds of millions of $’s of their stock for the long-term. They can’t trust the markets will automatically be efficient. What is replacing the active manager is a thriving retail trading community. But their attention span is fickle.

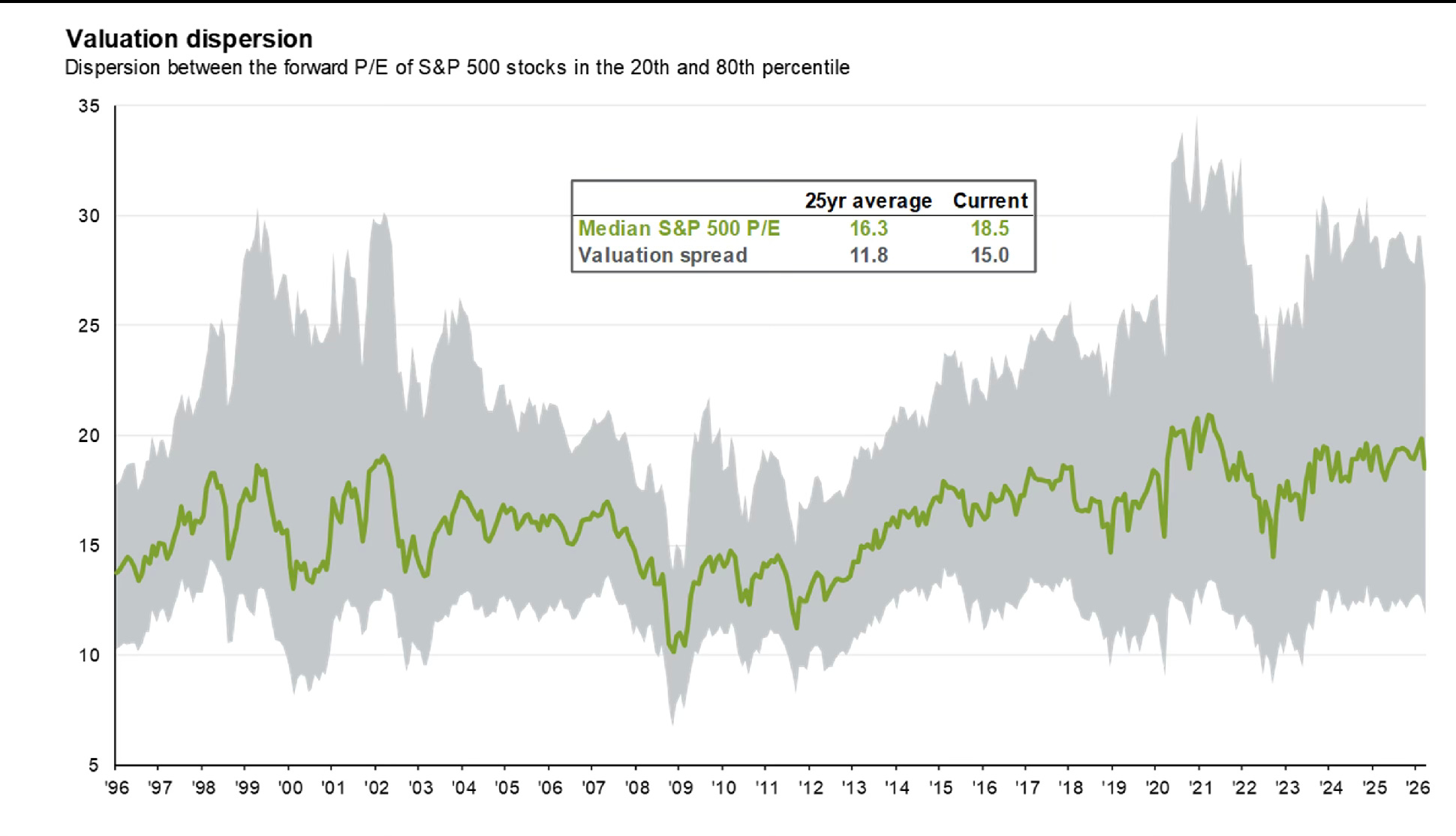

So there is this sad state of affairs where there is an attention span cliff. When stocks fall out of the narrow band of investor interest (high growth, innovation, high-vol) they quickly become worthless because there aren’t any active investors to save them. It’s why there is such a wide dispersion in valuations. The 25 year average P/E multiple spread between the 20th and 80th percentiles is 11.8x. Currently, it’s 15x. You are either interesting, or you are not.

Which means in this new normal companies have to build up their retail investor base. It means they have to go to smaller conferences, meet smaller investors, use social media, go on podcasts, etc to build a retail following. The crypto world has learned this.

Realisation number 2 is that when stocks become ‘no-growth value traps’ maybe they should pay out the cash as dividends instead of buying back shares.

If you are a dying star, that’s fine, but give us the cash so we can milk it and use the money to reinvest in something else, like Buffet did with Berkshire Hathaway. Take Paypal. They say they are going to return $6bn in share buybacks when the market cap is $45 billion. Which sounds great, but what if they are just shovelling more cash into the furnace? What if the stock price still goes lower despite all the buybacks because they are losing market share and payment volumes aren’t growing? If Paypal paid $6bn out as dividends at least we would have the cash.

The second benefit for a company from paying dividends is that it shows up on dividend screens. Lots of investors screen for stocks for dividend yields. And a company with a high enough dividend yield might even get picked up by a dividend ETF. There is a home for stocks with double digit dividend yields, but not for stocks which aren’t growing and have dividend yields of 1%

The market structure has changed.

What you realise is the market structure has changed. It used to be that financial advisors allocated money to the institutional active fund managers who had good access to the companies, were relatively long term and had a value bias. The analysts at the active fund managers would build their spreadsheets and identify which company in the sector had the best ROIC, and pick that one, even if it wasn’t the most liked. They would never buy a stock like Tesla for example. Meanwhile, the financial advisor would sit back and leave the stock picking and tough decisions to the active manager.

But with the rise of ETF’s for every possible sector, country, index and theme that structure has changed. The investment decision shifted back to the advisor. The advisor now became an asset allocator. And ETF’s are the lego blocks they use to build their client portfolios.

The financial advisor doesn’t care about some one-off aircraft part company in Wisconsin which is cheap. Or, a cheap payment company. The advisor cares about sector and country beta. They need to make sure they don’t miss the hot ‘themes’. They can’t be the advisor who missed ‘EM’ or ‘Korea’ or ‘Semis’. It’s why so many financial advisors read YWR.

This is how ETF’s changed the game. We went from stock picking to theme picking.

And it’s why the more I looked at the dying payment companies and the appreciated the challenges they would have in attracting investors, the more interested I became in BlackRock. Because the death of the payment company share prices is directly related to the success of BlackRock ETF’s.

If you aren’t big, aren’t liquid, aren’t growing, and aren’t in the ETF’s, and there isn’t some retail community which cares about you, you don’t exist.

Realisation #3: If BlackRock ETF’s are a Death Star taking over the market, shouldn’t we own the Death Star?

Is the big takeaway from analysing the payment companies, that we should be buying BlackRock?

You thought we were going to buy the small, edgy undervalued stock with 5x upside? Nope. Fake Left. Go Right.

We are buying the Death Star instead.

Bam!

Could BlackRock be on the verge of an earnings acceleration and a move to $1,700/share by 2030?

Platform as a Service

The NYCERS Insight

More Legs to the ETF Story

YWR EPS Estimates and Earnings Model

Risks

Platform as a Service

The thing about great entrepreneurs like Larry Fink, and why you want to invest in them, is they never stop thinking about the next thing. They are always moving the goal posts. So while the rest of the asset manager community is finally getting around to launching their own ETF’s, Larry is turning BlackRock into a platform which they call 1BLK.