Jason addresses head on the big elephants in the room around hyper competition, token governance, token economics and privacy.

This is part two of a three part series on Chain Street.

I encourage you to start with Part 1 which you can find here.

The Shift from Counterparty Risk to Technical Risk

Why the Hyper Competition of Crypto is Good

Token Holders vs Equity Holders

ZK Privacy and why we need Blockchain Identity

The Shift from Counterparty Risk to Technical Risk

Legacy finance relies heavily on trusted intermediaries such as banks, brokers, custodians, and clearinghouses to facilitate transactions and enforce agreements. This introduces counterparty risk to everything we do with our money, the danger that one party defaults on its obligations, whether due to insolvency, fraud or mismanagement. Enforcement depends on social processes like legal contracts, regulatory oversight, and human-led dispute resolution, which can be slow, costly, and prone to bias or corruption.

Blockchain technology, which we described as Trustware in Chain Street Part 1, fundamentally reorients this dynamic by replacing human intermediaries and social enforcement mechanisms with cryptography, economic incentives and consensus protocols. DeFi protocols like lending platforms (e.g. Aave) or decentralised exchanges (e.g. Uniswap), let users interact directly with smart contracts (self-executing code on blockchains like Ethereum. Trust in these interactions is minimised in that no single entity holds custody, and outcomes are determined deterministically through game-theoretic incentives (e.g. staking penalties for misbehaviour), and network consensus (e.g. proof of stake validators agreeing on transaction validity and guaranteeing finality). These new rails eliminate counterparty risk, as it allows us to transact without the need to trust an intermediary and the social processes holding that intermediary to account.

Blockchains essentially transform counterparty risk into technical risk, which is not risk-free. Once deployed, smart contracts are immutable, meaning bugs and vulnerabilities can lead to irreversible losses. This is another important distinction. In a blockchain world, we don’t have recourse when something goes wrong, you can’t call up Vitalik Buterin and say, “Hey man, I messed up with that last payment and sent it to the wrong person. Can you roll it back for me?”

While audits, formal verification and bug bounties mitigate some of these issues, they cannot eliminate them entirely. Code afterall, is written by humans and unforeseen risks exist. This is an obvious barrier to adoption, as legacy finance relies on safeguards such as recoverable human processes and recourse in the event that something doesn’t go as planned.

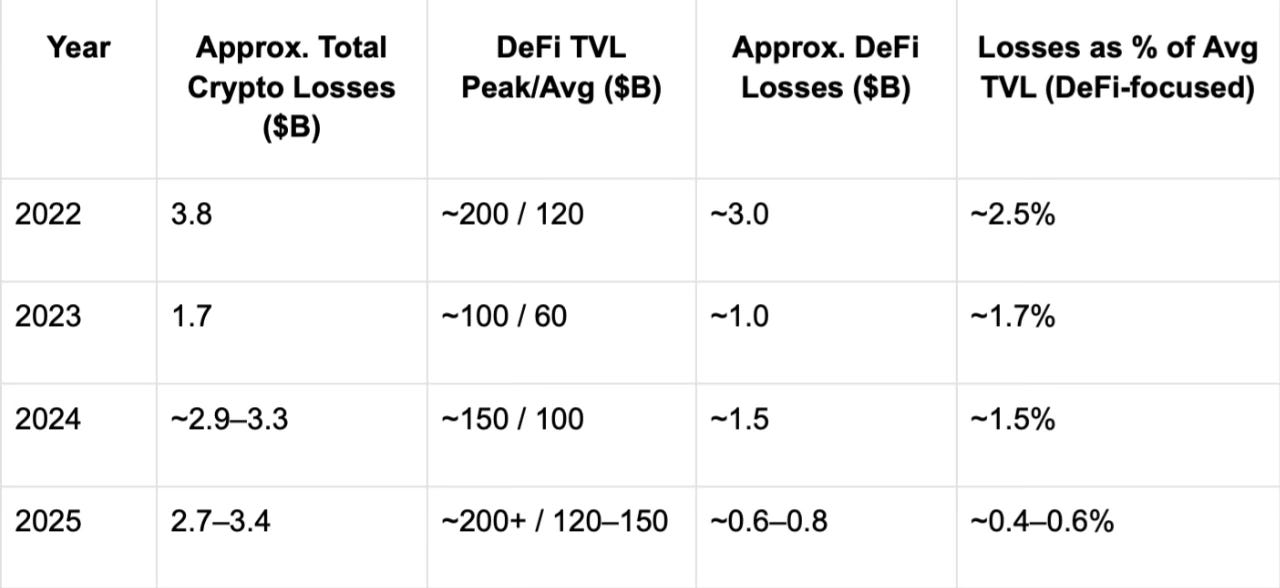

Persistent Exploits with Declining Relative Impact

Technical risks remain a persistent threat in crypto. According to Chainanalysis and TRM Labs, in 2025 alone, total losses from hacks, exploits, and theft ranged from $2.7 billion to $3.4 billion. Interestingly, the majority of losses were driven by centralised exchange breaches ($1.5 billion Bybit hack) and social engineering rather than pure DeFi smart contract vulnerabilities. Even as Total Value Locked (TVL) has rebounded significantly, DeFi-specific losses were notably suppressed compared to prior cycles.

As of January 2026, global DeFi TVL stands at around $100-130 billion. Exploits resulting from smart contract bugs accounted for a smaller share of losses in 2025, while most exploits occurred via offchain vectors such as private key compromises and phishing attacks. Smart contracts are evolving and maturing to risks. In earlier years saw exploits scale with TVL growth, but improved tooling, better formal verification, timelocks and multi-signature wallets have broken this relationship.

As a percentage of TVL, exploit losses have trended downward over time. While absolute figures remain high due to larger ecosystems, relative risk (losses/TVL) is lower than in DeFi’s early days.

One of the beautiful features of blockchains open source nature is that many eyes can tame complexity, and risks are constantly being identified and resolved. However, it’s worth acknowledging that, for some, technical risks remain a deal-breaker. Whether it’s the bearer nature of cryptoassets or outsourcing the management of those assets to smart contracts, these risks are scary and require vigilance.

This gives us two paths forward: we either throw our toys out of the cot at an emerging technology with enormous potential because there are risks, or we keep working toward making wallets, custody and DeFi safer. As an optimist, I believe we have the human intelligence and ingenuity to lower technical risks to parity with counterparty risks, and eventually reduce them to the point where interacting with a counterparty no longer makes sense.

Why the Hyper Competition of Crypto is Good.

Banks, payment networks, and custodians operate closed, permissioned systems protected by regulation, licensing requirements, and decades-old trusted relationships. A startup cannot simply “plug in” to Fedwire; it needs approvals, capital reserves, compliance infrastructure, and political connections that take years (if ever) to secure. Gatekeeping and high barriers to entry are a consequence of trust maximised legacy finance. For users, switching costs are punishing. Changing banks or brokers means time and money spent opening new accounts, setting up direct debits, credit history checks and KYC paperwork. The result is clients locked into entrenched monopolies or oligopolies that extract rents far above what would be possible in a more competitive environment. These problems are amplified in the developing world.

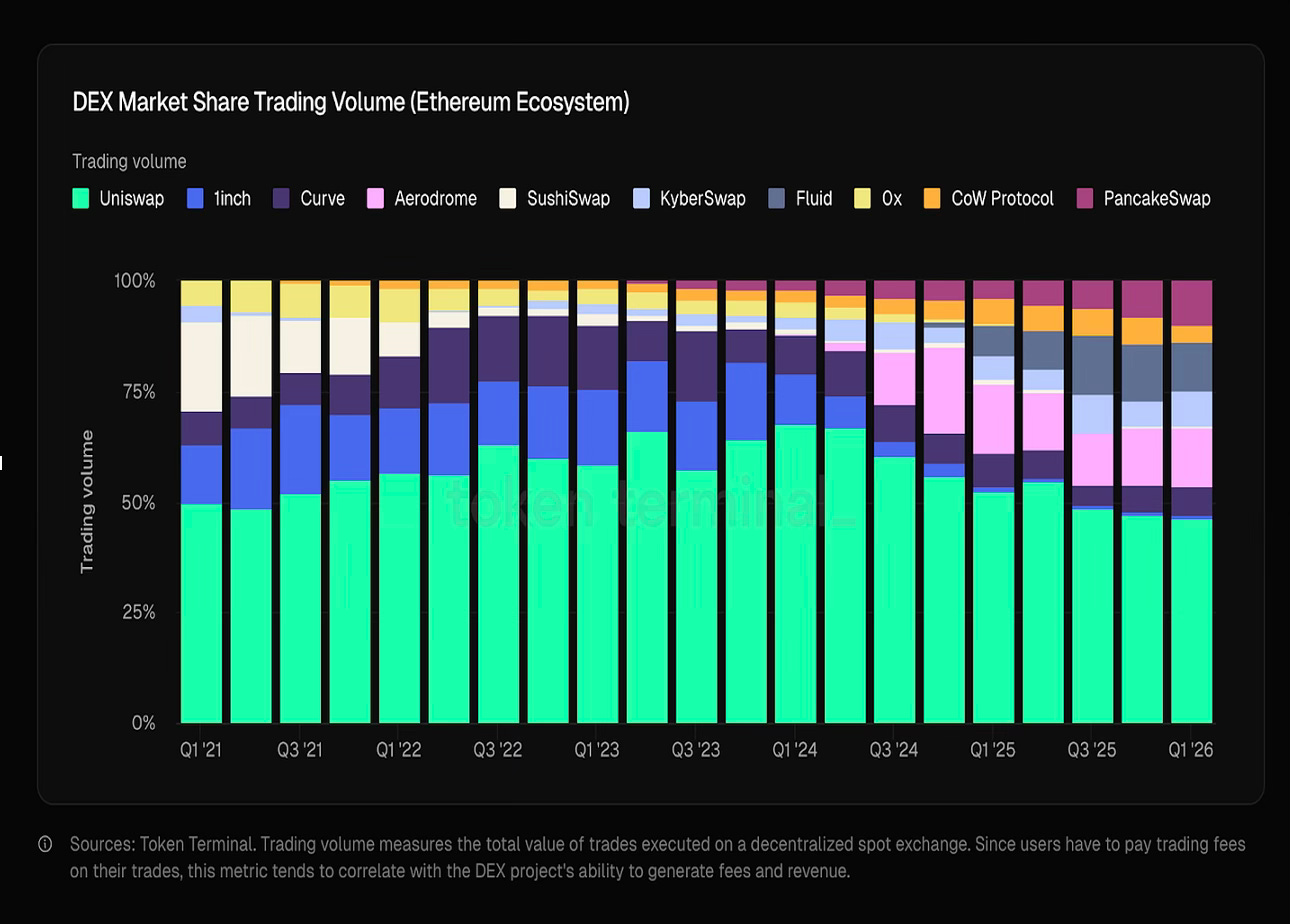

Crypto turns this model upside down. Core DeFi protocols are open source, composable and permissionless. Anyone can fork Uniswap or Aave in an afternoon and offer the same functionality with a few tweaks. Users face near-zero friction (assuming they stay on one chain), a wallet connect, a couple of clicks, and they can be routed to the best price via a decentralised exchange aggregator. This is hypercompetition, far more intense than anything in traditional software, let alone finance.

For users, the outcome is unambiguously superior. Capital can flow to the most efficient venue in real time, fees compress quickly, and low barriers to entry spur constant innovation. New capabilities pop up regularly because no one needs permission to build on Ethereum. This mirrors the early internet’s triumph over corporate intranets as open protocols eat closed gardens because developers and liquidity naturally gravitate to where friction is lowest.

Investors, however, face a challenging environment. Moats are shallow and temporary. Clever token incentive programs can cause liquidity to migrate from venue to venue. Valuation remains difficult and feels speculative because sustainable technical competitive advantages are rare in a world where code can be copied, and users are mercenary.

Surprisingly, even in the face of hyper competition, winner-take-most dynamics still emerge. Uniswap, for example, has been forked thousands of times (Sushiswap, Pancakeswap, Quickswap, Aerodrome) but still commands 40%+ of Ethereum DEX volumes.

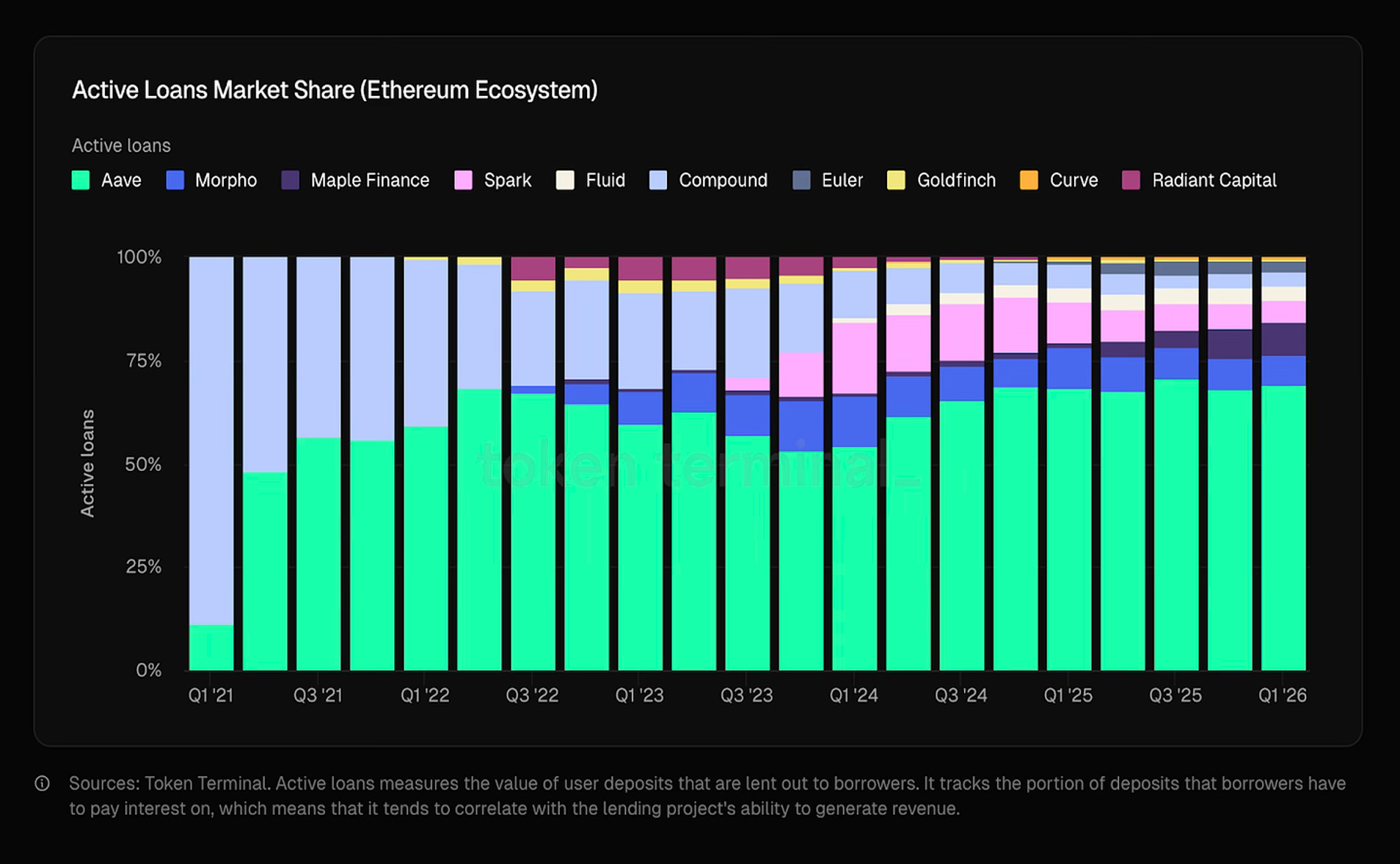

The same is true for Aave’s core lending logic, which has been replicated and tinkered with endlessly, yet it continues to command 50%+ of active loans.

It seems evident that network effects can take hold in DeFi, especially around liquidity and integrations. The best DeFi protocols quickly become infrastructure that developers build on top of rather than replace.

Token Holders vs Equity Holders

The reality is that tokens are new, unique assets we have never seen before. Tokens can encapsulate multiple functionalities (Service provision, Governance, Value distribution, Membership, etc). I discussed this in the Art of Crypto Economics. Our friends at Just Cryptoeconomics have a brilliant dashboard that displays these functionalities for over 50 cryptoassets. This innovation is simply incompatible with existing securities laws. Ideally, 10 years ago, regulators and industry participants would have sat down together and had a conversation to lay out the rules of the road, this isn’t how things played out.

The situation reached a climax during the Gensler era at the SEC (2021-2025). Gensler led an openly hostile regulatory environment for US-based crypto projects, forcing a stark separation between equity holders (typically in entities such as Uniswap Labs or Aave Labs) and token holders. The fear of tokens being classified as securities led teams to structure protocols in such a way that minimal value generated by the protocol would accrue to tokenholders, while equity captured upside from valuable IP, siphoning of fees and side hustles. Bad incentives bred bad outcomes.

Venture funds and Founders of DeFi protocols reaped the benefits of these poor incentives through salaries, advisory contracts and various forms of offchain revenues. Leaving many DeFi tokens as speculative bets without claims on cashflows. These claims don’t need to be legal in nature, they can be programmatic (either via a dividend or buyback) or captured and allocated via governance of the protocol, often a decentralised autonomous organisation (DAO).

Addressing this requires regulatory clarity for the crypto industry and its builders. The CLARITY Act will be a good first step in cleaning up token holder rights. Companies like Blockworks are also doing great work with their minimum disclosures framework and investor relations platform, something I think is integral for crypto to step into adulthood. There is no reason why DeFi protocols should not be able to follow similar value accrual methodologies as companies to maximise token holder value. They provide a service, charge a fee for that service, build up residual interest, and have governance structures to decide how that residual value is allocated. But incentives are key, and the separation between development labs and the DeFi protocol itself needs to be more clearly defined and aligned.

Why the token crash is at an inflection point.

| A guest post by

|