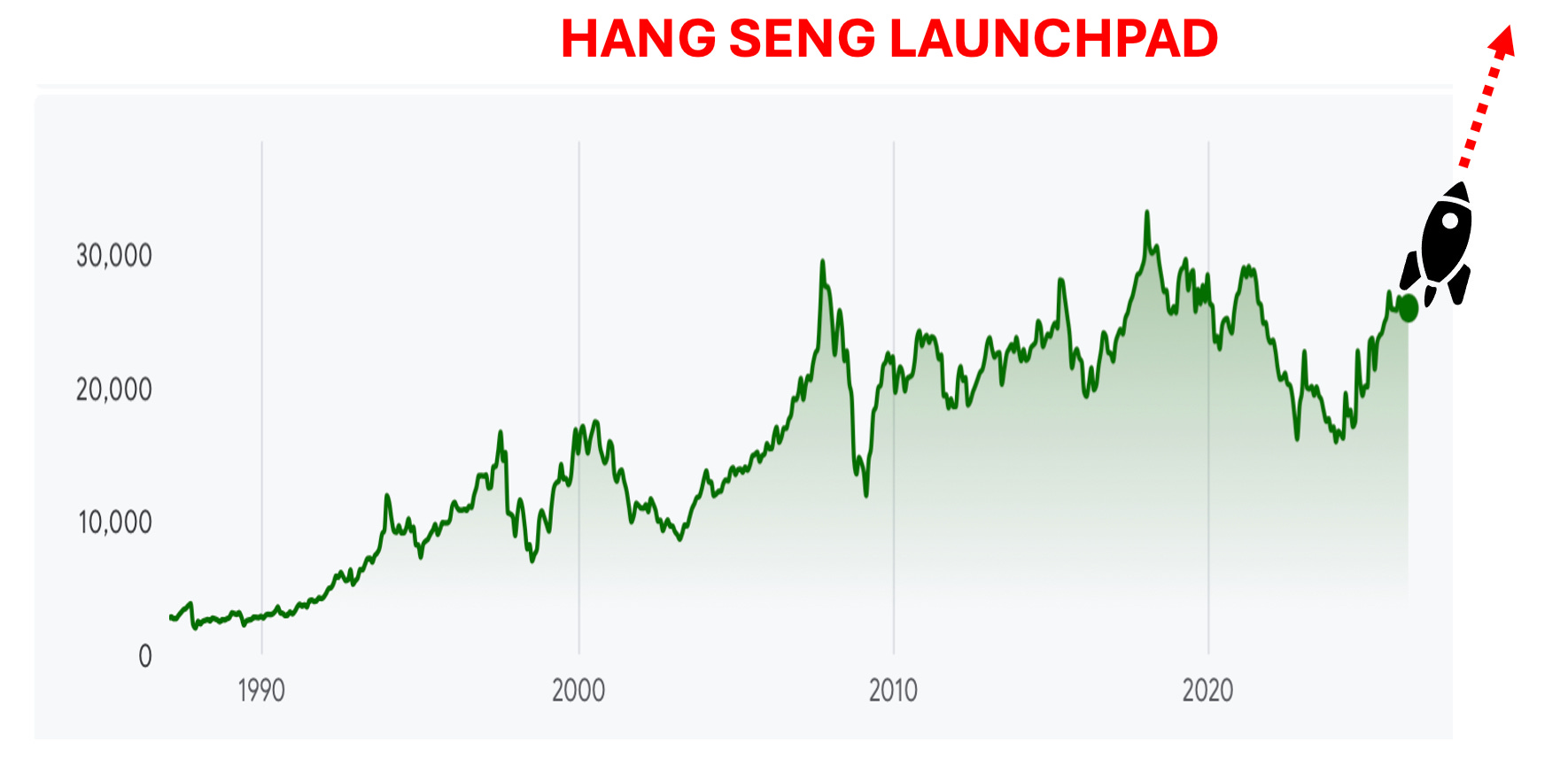

YWR: Hang Seng on the Launchpad

Skate to wear the puck is going to be.

Isn’t that what they say?

Semis and memory have been great, but it’s time to hand the baton to someone else.

Like the Hang Seng Index.

The Hang Seng has had a sluggish start to 2026 (-1.5%), but I think it’s still going to be a great year.

Let’s start with the chart. I LOVE the chart. Where else has a developed market index gone sideways for 15 years in hard currency?

This thing looks like a coiled spring. Which is why I remain patient. Because I think the move is going to be big (IMHO).

35,000 at the index level seems very achievable.

Besides the chart why could the Hang Seng be about to gallop?

Here are 4 reasons.

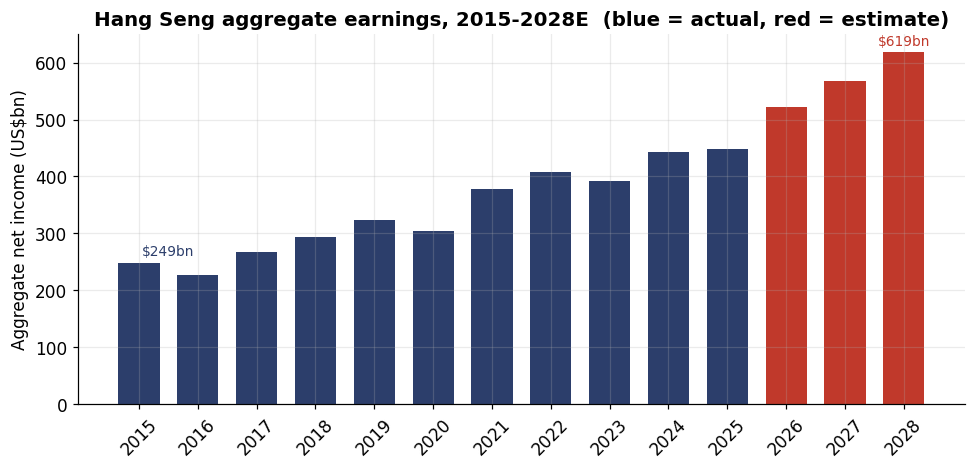

#1 Earnings growth is expected to accelerate from 6% to 11%.

Note: I created my own rough approximation of the Hang Seng Index fundamentals using 89 constituents. So warning, this is an approximation, not the official index.

From 2015-2025 earnings grew at a 6% CAGR, which is slow and caused the index to derate. China and Hong Kong have experienced an epic property crash so the earnings CAGR at the big Chinese banks (ICBC, CCB, BOC), has been just 1-3% for a decade. When you think about it, it’s actually amazing the big banks have been growing earnings at all in the midst of a property crash and falling interest rates. Think back to the Evergrande days. We all expected China would go through their own GFC and these banks would need to get bailed out. Instead they muddled through.

The property problems spilled over into many other Hang Seng constituents like China Resources Land (4% EPS CAGR), China Overseas Land (-9% EPS CAGR), Sun Hun Kai Properties (-5% EPS CAGR), Henderson Land, Wharf, and Hang Lung Properties.

There was also the crash in earnings at Alibaba (3% EPS CAGR),

But that is the past.

Over the next 3 years the EPS CAGR is expected to improve to 11%!

Tencent, the biggest earner, is expected to grow EPS at a 17% CAGR. Alibaba works through the hit to online retail and grows again (+17% CAGR). The Big Banks accelerate to 6% growth (from 3%). PetroChina, CNOOC, China Petroleum & Chemical benefit from the oil price recovery. The New Energy EV stocks, BYD and CATL, also kick in with a 26% EPS CAGR. And the property stocks go from negative EPS growth to positive.

#2 Earnings revisions are swinging positive.

This is one of the most important trends. Earnings are starting to beat expectations. Importantly, the big banks are beating earnings. You have growth accelerating and EPS estimates rising.

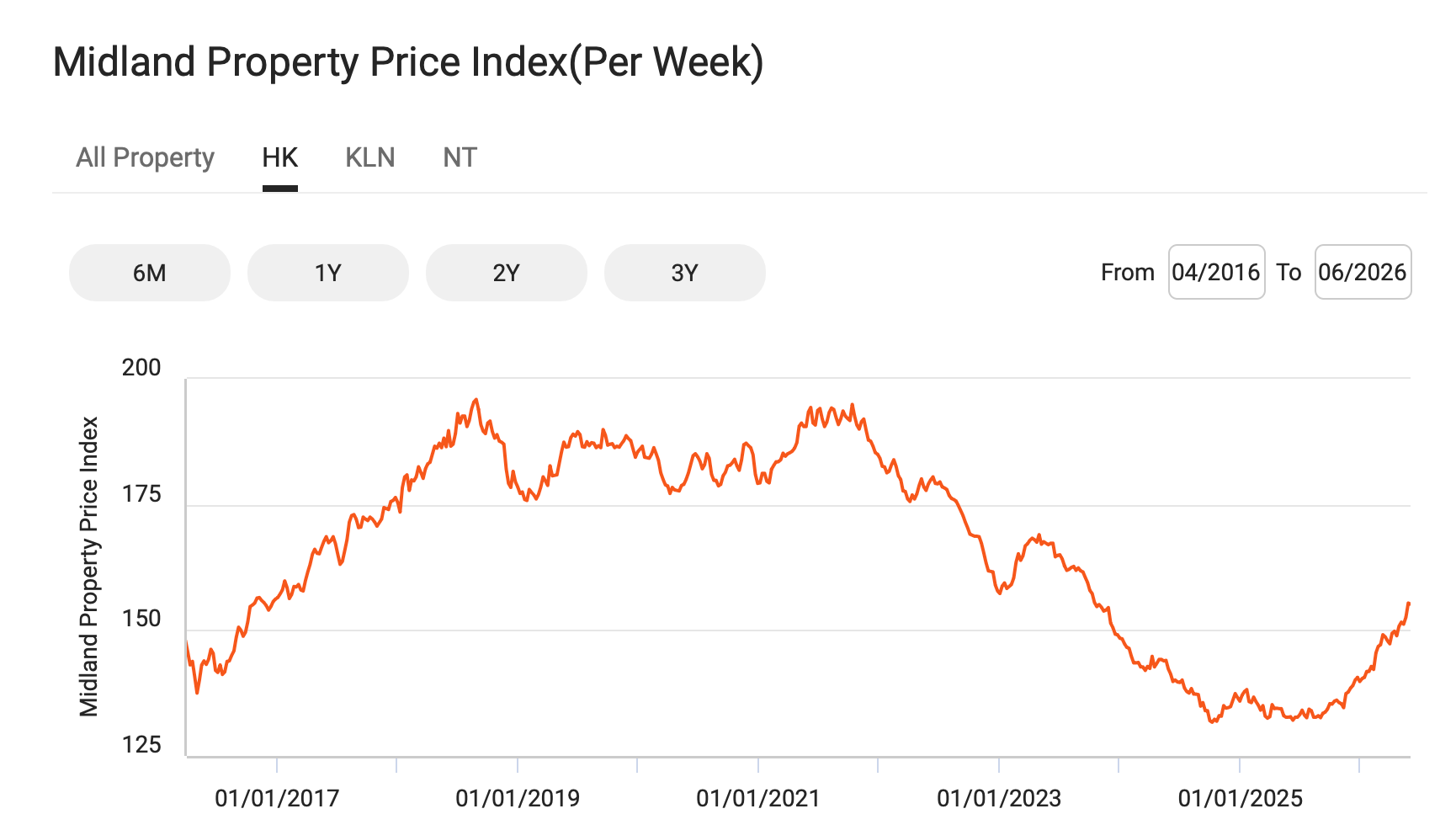

#3 HK Property prices are recovering.

For a city built on property it’s a big deal that property prices are recovering. Rising property prices improves risk appetite and collateral values.

After a gruelling 4 years, Chinese mainland property might be stabilising too.

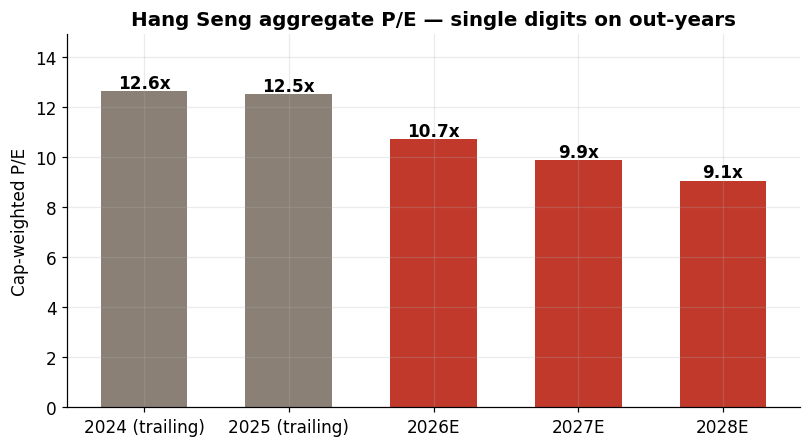

#4 Where else do you find a hard currency index on 10x P/E?

This growth pick up leaves the Hang Seng valuation looking like a dripping roast. If earnings develop as expected the index would be trading on 9x in 2028. Be safe and assume I’m wrong by a turn and it’s 10x 2028 earnings. Again, this is an approximation using 89 constituents and consensus EPS estimates through 2028.

Only a few of us remember the good old days, but Hong Kong investors love to trade, and in a HK bull market this P/E can easily expand to 15x.

Below is the full dataset I used for the analysis if you want to dig in and find the best mix of valuation and expected growth.