YWR: HKEX,our China FOMO Play

Disclosure: This is market commentary and definitely not investment advice. Always get professional investing advice.

Is AI a bubble? Or, is it not?

So many good reports on this topic. Is it telcos 2000? Or, do Musk Zuckerberg, and Altman know what they’re doing better than the peanut gallery?

Tough to know.

One thing is for sure. If you’re trying to figure whether something’s a bubble, it has probably already moved A LOT.

Maybe a more profitable use of your time is to find a new bubble/bull market in the making. Find the new, new.

Like China.

I love that the HSI is +23% YTD and everyone is fading it.

‘The stimulus isn’t enough. Nothing’s changed. etc.’

Guys… fade it?

The party hasn’t even started. IMHO this move is going to go mental and will last years.

Earlier this year we put on the Cash Dragons + LVS. We were a bit early, but now it’s working.

But there was always another trade I knew I should add, but it was risky. It’s the real bucking bronco.

If this China move is going to do what I think it can, it’s the mega way to play it. HKEX (388 HK). So I bought it too.

The China Bull Market (2024-2028)

I’ve been trying my best to tell the China bull case, but maybe I haven’t been doing a good job.

Fortunately, I recently met someone more articulate and experienced,

from Gavekal Research in HK.Louis is cool and I give him the YWR Approved Service Provider certification.

Take it away Louis.

Thank’s Erik. I’ll keep it brief and highlight a few slides, but the full presentation is available at the end of the post.

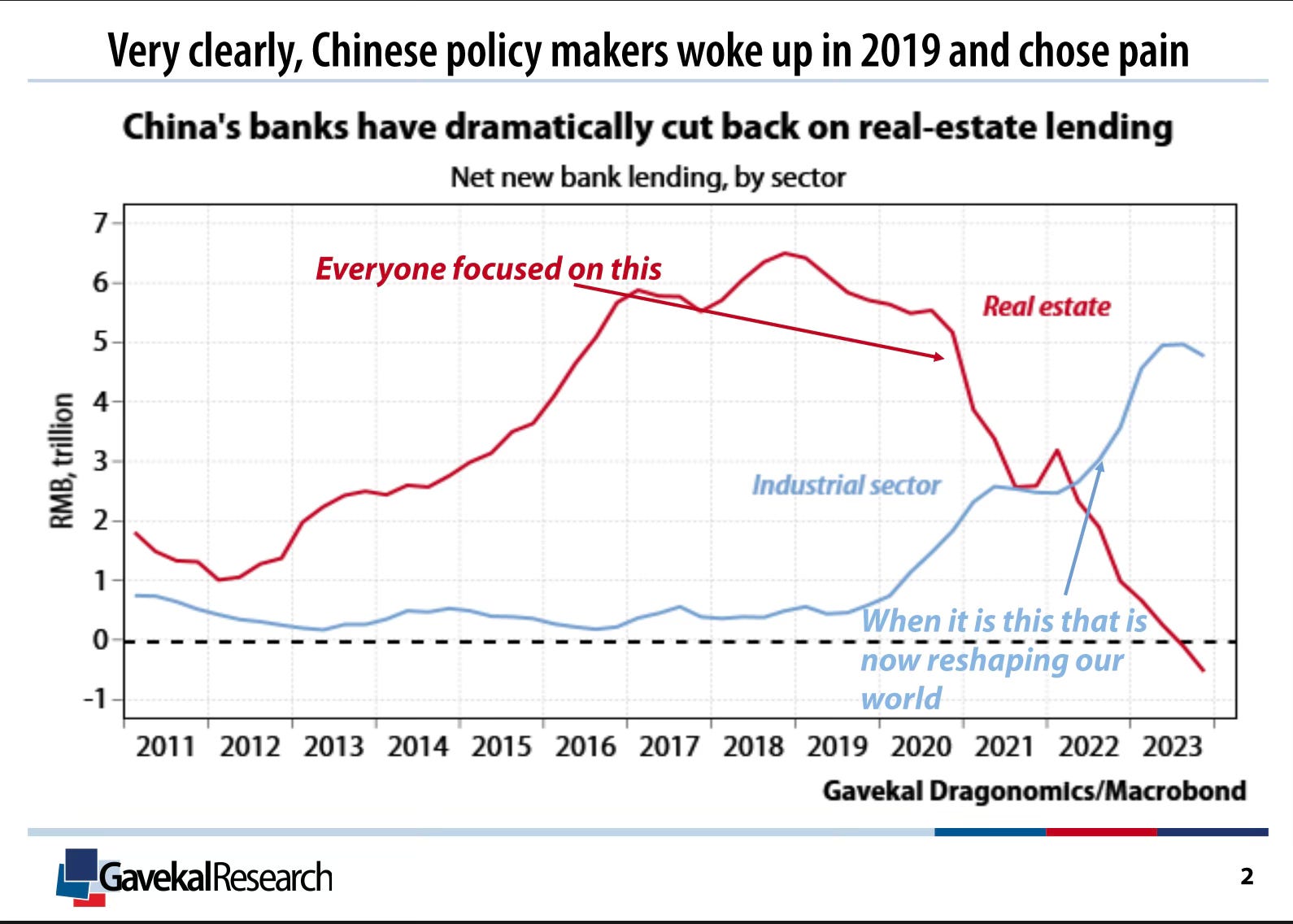

Everyone is overly focused on Chinese real estate lending, but this isn’t the full picture. They are missing how much Chinese banks have reallocated lending to industry. This is where China is growing.

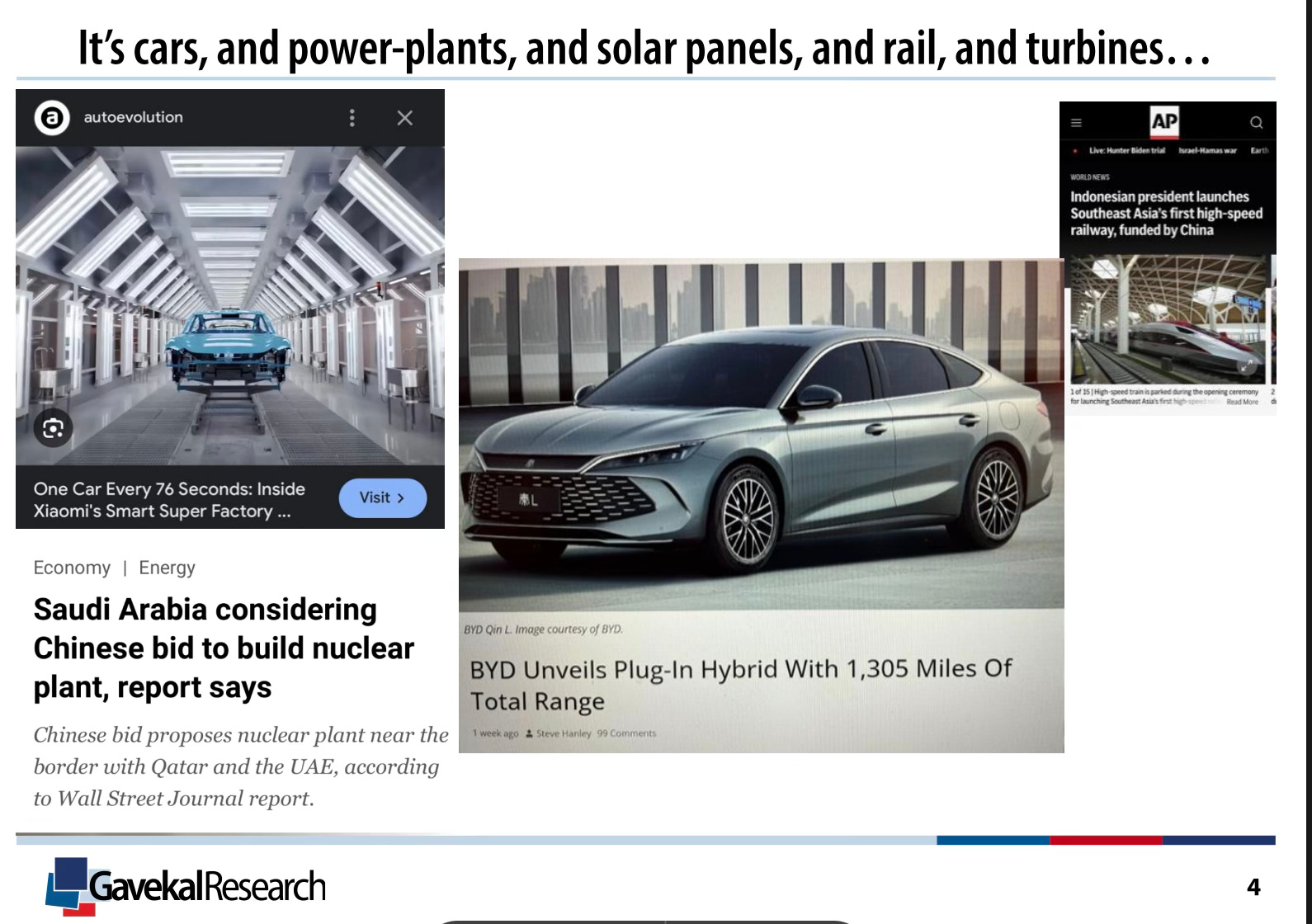

China is dominating one industry after another. Their competitiveness is startling. First it was solar panels, then wind turbines, then trains, now cars and even nuclear reactors.

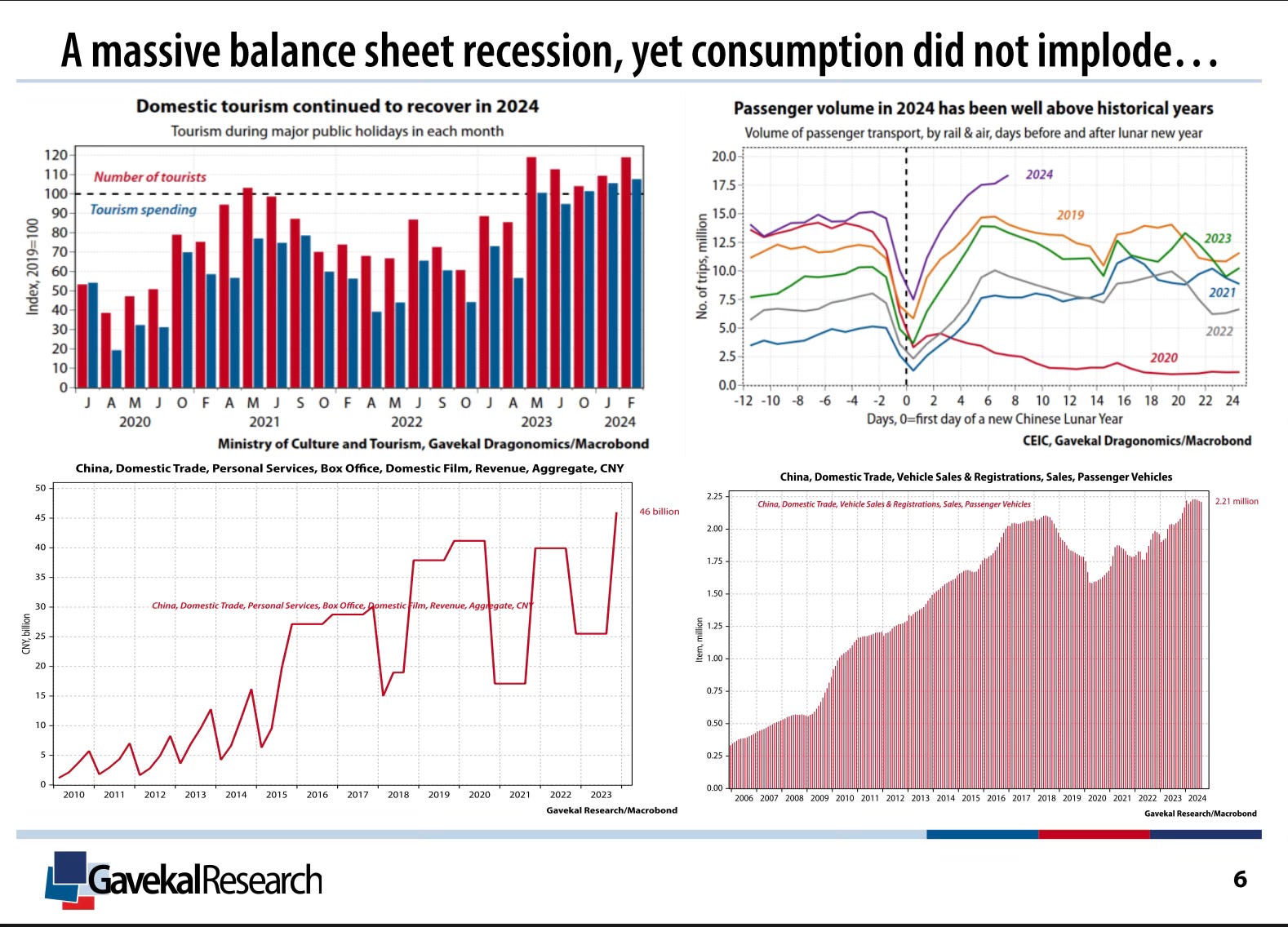

Yes, real estate prices have declined, but the Chinese consumer was never over levered and Chinese consumption is making new highs. You see it in domestic flights, Macau gaming, and vehicle sales. When European car companies complain about their China results it’s because they’re losing market share, not because the market is weak.

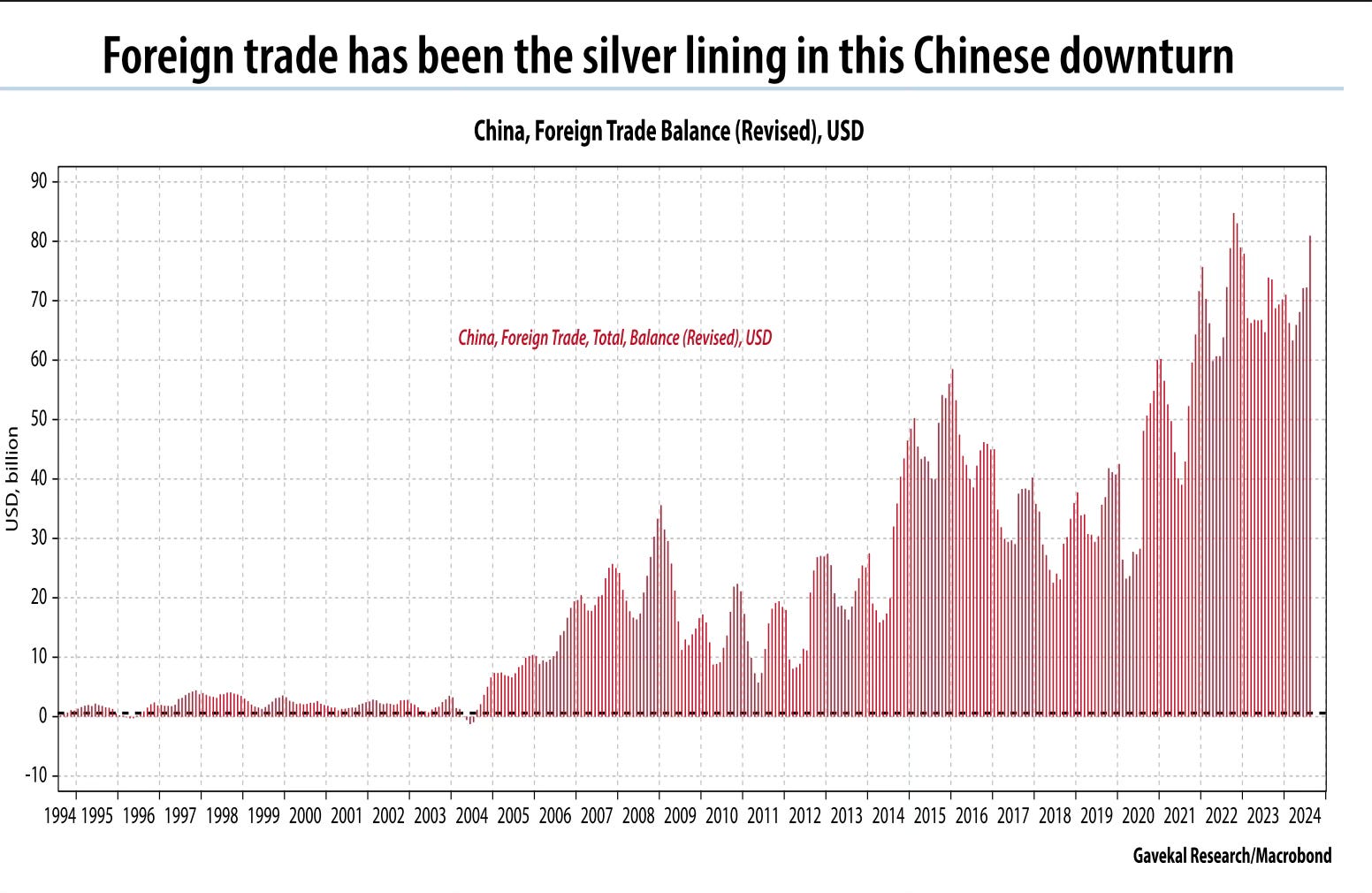

And then you have this record trade surplus. China is running a surplus of $80bn/month. It’s a tidal wave of dollars.

Normally, this $80bn/month would cycle back into China, the FX would strengthen, asset prices rise, domestic consumption increases, and gradually the trade surplus reverses and becomes a deficit, which weakens the currency. That’s a normal cycle.

But this cycle Chinese companies and entrepreneurs are too bearish about their own market to bring the money back, so it’s parked in US tech stocks, US real estate or gold. If they do bring it back into China they put it into Chinese government bonds.

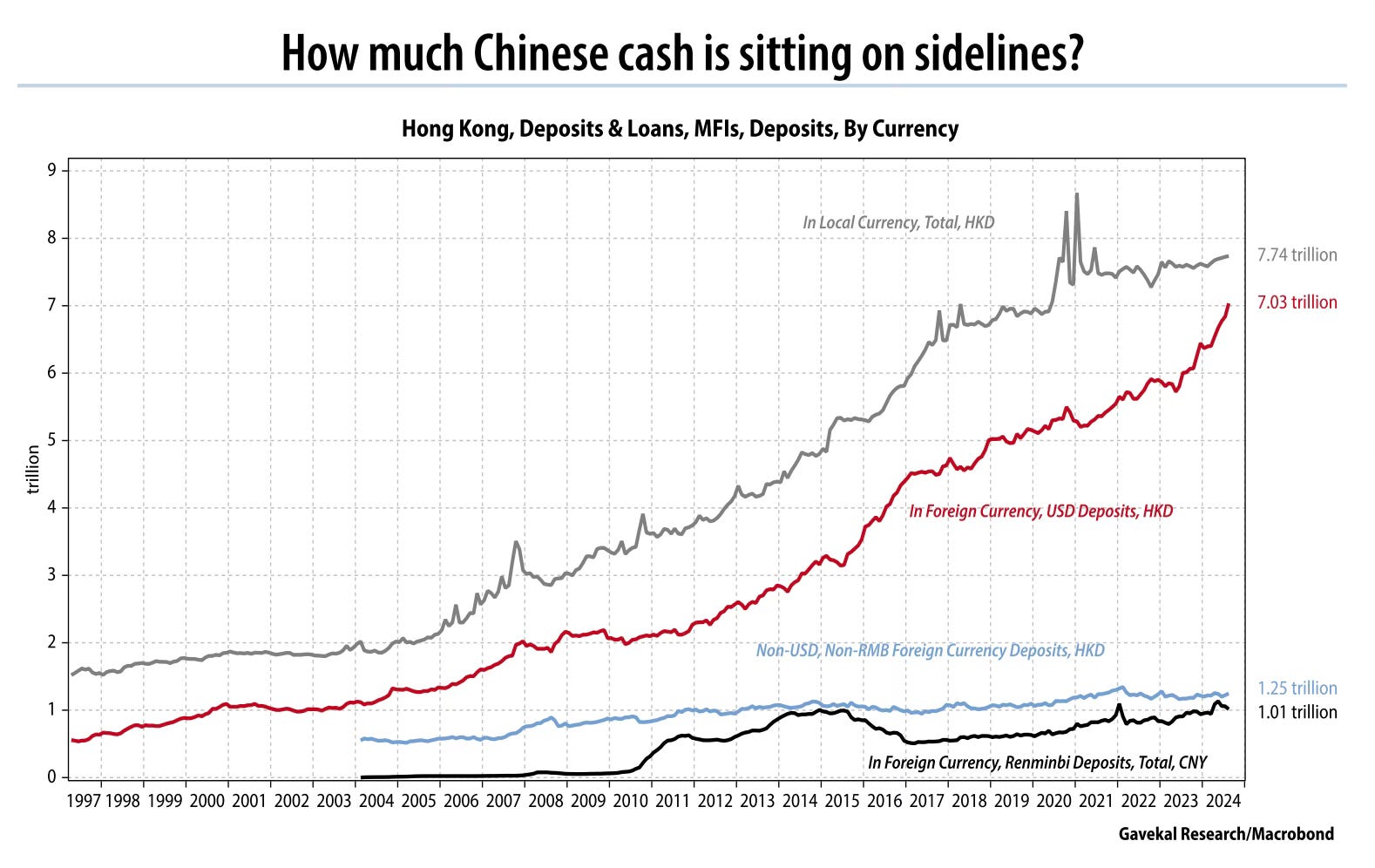

The dollars from the trade surplus show up as a surge in US$ deposits at Hong Kong banks. Now $7 trillion.

So Louis… where do you think this goes from here?

There are two main scenarios. It’s possible the status quo continues. The dollars keep piling into US assets and tech. But that’s not our house view.

We think it’s more likely we are on the verge of US$ weakness (which will align with Trump’s policies) and as soon as Chinese see any $ weakness these US$ deposits are going to suddenly flow into Chinese equity markets.

Wow. So you’re saying some of this $7trn parked in the HK banks could flow into the stock market?

That’s all we need to know.

If Louis is right, it’s time for HKEX, our China FOMO play.

Hong Kong Exchanges is the ultimate way to play a China bull market. Cash equity trading picks up, companies want to IPO, and futures and options activity surges. Meanwhile the cost base is relatively fixed. It’s the leveraged way to play a China bull market.

And because HKEX expenses everything and has no capex, the dividend payout ratio is 90%. It’s a pure flow through of China capital markets revenues into DPS.

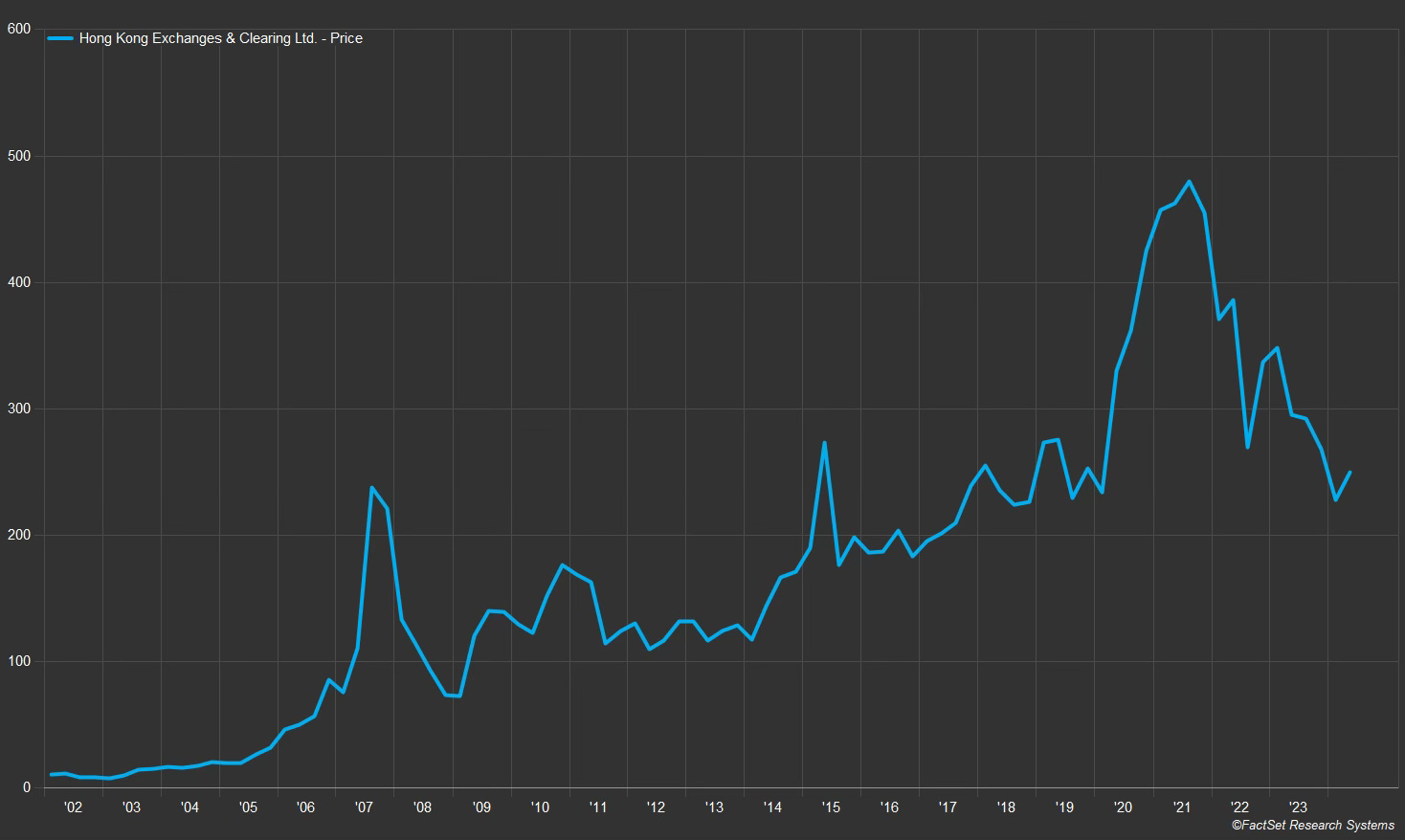

And the share price?

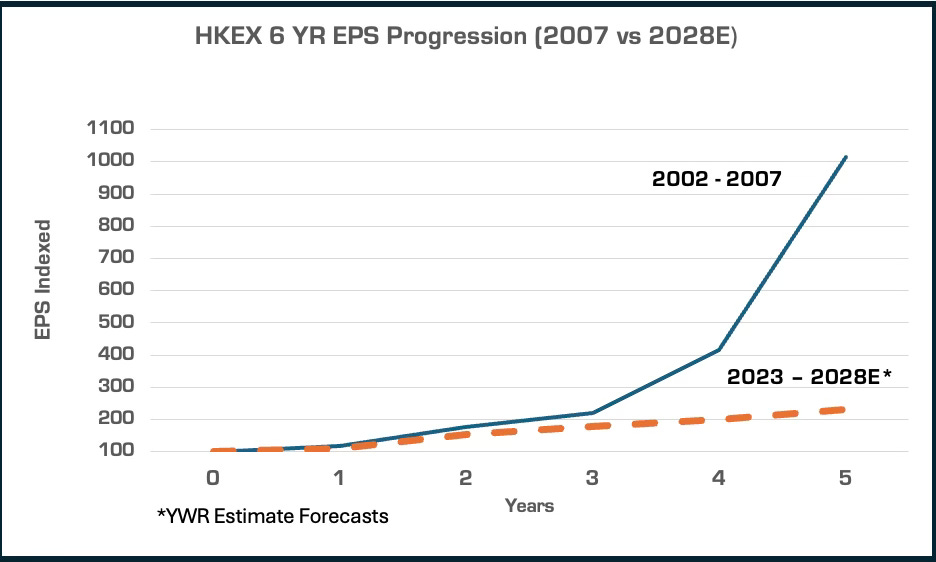

During the last China bull market (2003 to 2007) the share price went up 14x from (HK$15 to HK$ 230).

Full disclosure. I’m more bullish than any analyst on where Chinese stock markets are going to go. China and the HK market are highly undervalued and global investors have zero exposure. The Chinese themselves have almost no exposure even though it’s a national priority to stimulate the stock market.

I predict this is going to get mental.

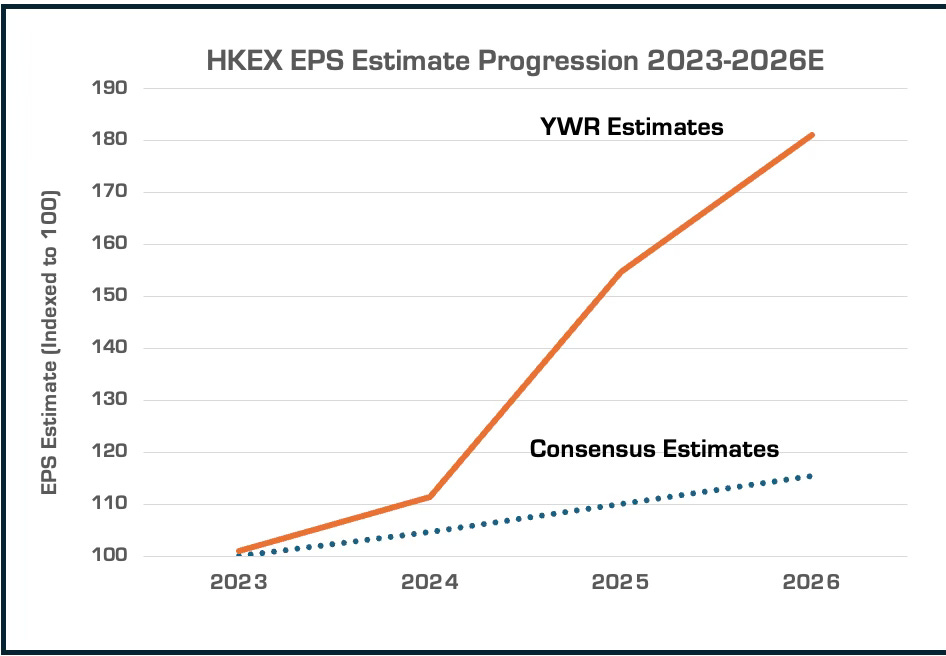

I also lived through 2003-2007 and painfully underestimated the upside in HKEX earnings. This time I’m trying to not make the same mistake.

Consensus estimates expect HKEX earnings growth between 2023 and 2026 of 16%. I forecast it to be +80%.

I’ve attached a link to my HKEX earnings model at the bottom of the post along with Louis’s presentation.

I’m trying to be bullish, and I’m 80% ahead of consensus on how this plays out over the next several years, but I’m probably still too low.

During the last bull market (2002-2007) HKEX earnings increased 10X (HK$ 0.57 to HK$ 5.78).

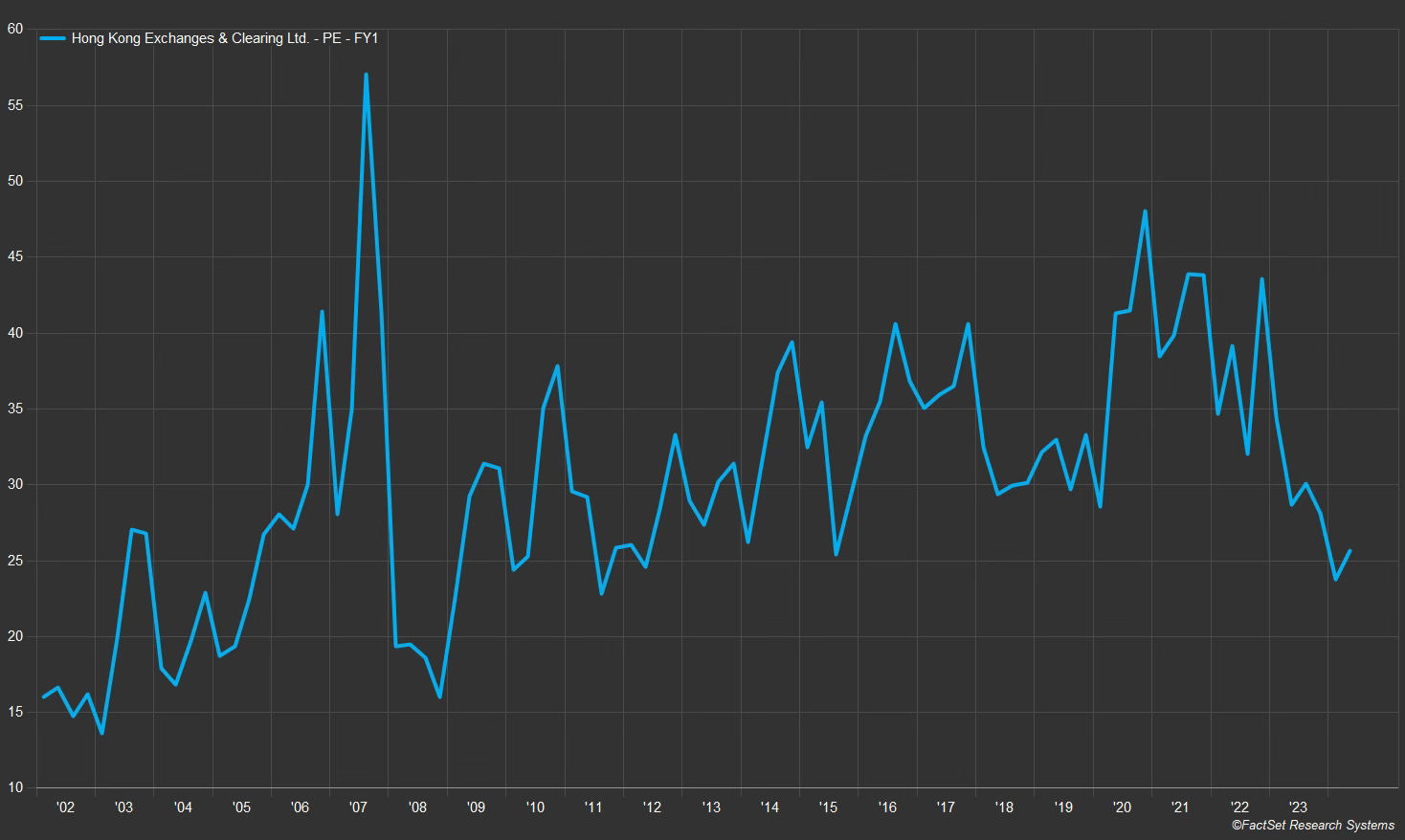

HKEX isn’t cheap. It’s trading on a P/E of 30x 2024, but to some extent it deserves a high P/E. It’s a massively cash generative business which pays out 90% of earnings, so the dividend yield in 2024 is 3%. A company which can payout 90% of its earnings and still grow multiple X is worth something.

We’ve talked about the upside optionality from EPS growth, but when the animal spirits are pumping we’ll probably get some multiple expansion as well. More likely HKEX will trade on a 35-40x P/E. The main kicker though is the earnings leverage from more market cap, and more trading activity in cash and derivatives.

Feel free to play around with the model and add your own optionality of where things can go.

Obviously, the downside risk is that it is a stock exchange and has a 1-1 correlation to the HK market. Too the downside too.

Below are links to the YWR HKEX Model and the Gavekal China Quandary presentation.

Have a good weekend!