YWR: How to make $ from PE Lock-In.

I told you all fun and exciting things I learned in Hong Kong.

But there was also something depressing I learned.

Or, should I say “depressing, but important to realise.”

Then having overcome the depressing part, our mind opens up to how we make money from it.

We were in the Grand Hyatt pitching ideas one after another. China, small cap miners, oil, nickel, SPAC’s, value stocks, shorting restaurants, etc.

The ideas were flying.

It was all good fun.

Then there was a presentation from the head of a large family office. We were excited to hear his great insights on what the most edgy, connected families in the world were doing.

We were on the edge of our seats.

What he would say?

“I thought I’d give you some insights into how the top family offices in the world look at things.”

Wow. Here it comes. Pen ready.

“And I don’t mean this to come across the wrong way, but they don’t care about any of these stock ideas. They’re playing at another level.”

“First, of all they think more in terms of asset classes, not stock ideas. They are looking for the best asset classes into which they can deploy large pools of money. And sorry to say, but when they look at the expected future asset class returns, private equity always comes out looking the best. Higher returns with less volatility.”

He pointed to a slide with a list of over 20 asset classed and the expected 10 year returns.

“That’s how they look at things.”

“While you think of the investing world as stocks, bonds and real estate. They think of the world as Event, Venture, Infrastructure, Distressed, Buyout, Co-invest, Secondaries, RV, CB Arb, ABS, CLO’s, and ILB’s.”

“And you may think the life of a family office CIO is coming up with amazing insights about the world, in reality it’s about managing the mountain of pitch decks they get every day from funds and business opportunities. Not to mention all the pitch decks dumped on their desk from the head of the family because of someone they met at a party the night before. ‘Oh, and can you take a look at this? It sounded interesting.’

Their job isn’t about amazing insights, it’s about filtering and finding ways to say ‘no’ to things.”

As I listened to this an upsetting realisation was sinking in.

An upsetting realisation for the small, struggling equity fund manager, which I had been.

The institutional fund consultants and the PE firms had reshaped the game. It wasn’t about equity funds and great stock ideas, it was about controlling the asset allocation.

They’d taken the traditional equities and bond investment universe and flooded it with new products and asset classes, all of which were private, not indexable, and charged high fees.

They’d also made it confusing. How was a pension fund or family office CIO supposed to have a view on the 5-10 year future return outlook for so many different asset classes? No way.

And think about those future return projections. Think how arbitrary they are. You are comparing a universe of known public equities or bonds, with historical financials and valuations, with ‘strategies’ represented by funds, which may or may not yet exist, and which will make future investments, into who knows what.

Forecasting private asset returns is a total thumb suck.

In this world of confusion, the CIO has two choices. Be like Norges, ignore it all, and stick to public equities. Or, default to the consultant or sell side research firm’s view on the outlook for all these different asset classes. If the CIO goes this route there is a whole industry happy to provide research and views nudging the CIO towards products with the massive fees. Because the great thing about private funds is everyone gets to eat. The banks structuring the deals and lending money, the consultants, and the asset managers.

It’s PE lock-in.

A further realisation was that even if you are a CIO who sees what’s happening you can’t fight it.

It’s too hard, and too risky at this point to take a contrarian view for example that maybe the next 10 years of private market returns will be sub-par and you should switch it all into international public equities.

Or, that you should buy China stocks listed in HK.

It’s too much career risk. What if China invades Taiwan? What would the board think? That would be a career ender. Better to stick with the program and buy Blackstone’s latest fund. Terrible but true.

And to be fair the returns from private assets have been pretty good. I expect those returns to be lower going forward, but it could be that it doesn’t matter. Maybe as long as private assets do 6-8% that’s ‘good enough’.

Private asset managers have created a better mousetrap. Equity-like returns without the sickening volatility. Yes, at times the NAV’s will be wrong, but the customer won’t complain as long markets recover by the end of the fund, which they usually do. The customer actually appreciates not having the extreme mark downs. Ignorance is bliss.

And so I started have this shift in view.

Maybe private market returns aren’t going to be great, but maybe it doesn’t matter (and maximising returns isn’t the only objective). Could it be that pension funds and family offices are on auto pilot and keep allocating anyways?

Had I under appreciated the strength of the business model and the PE Lock-In?

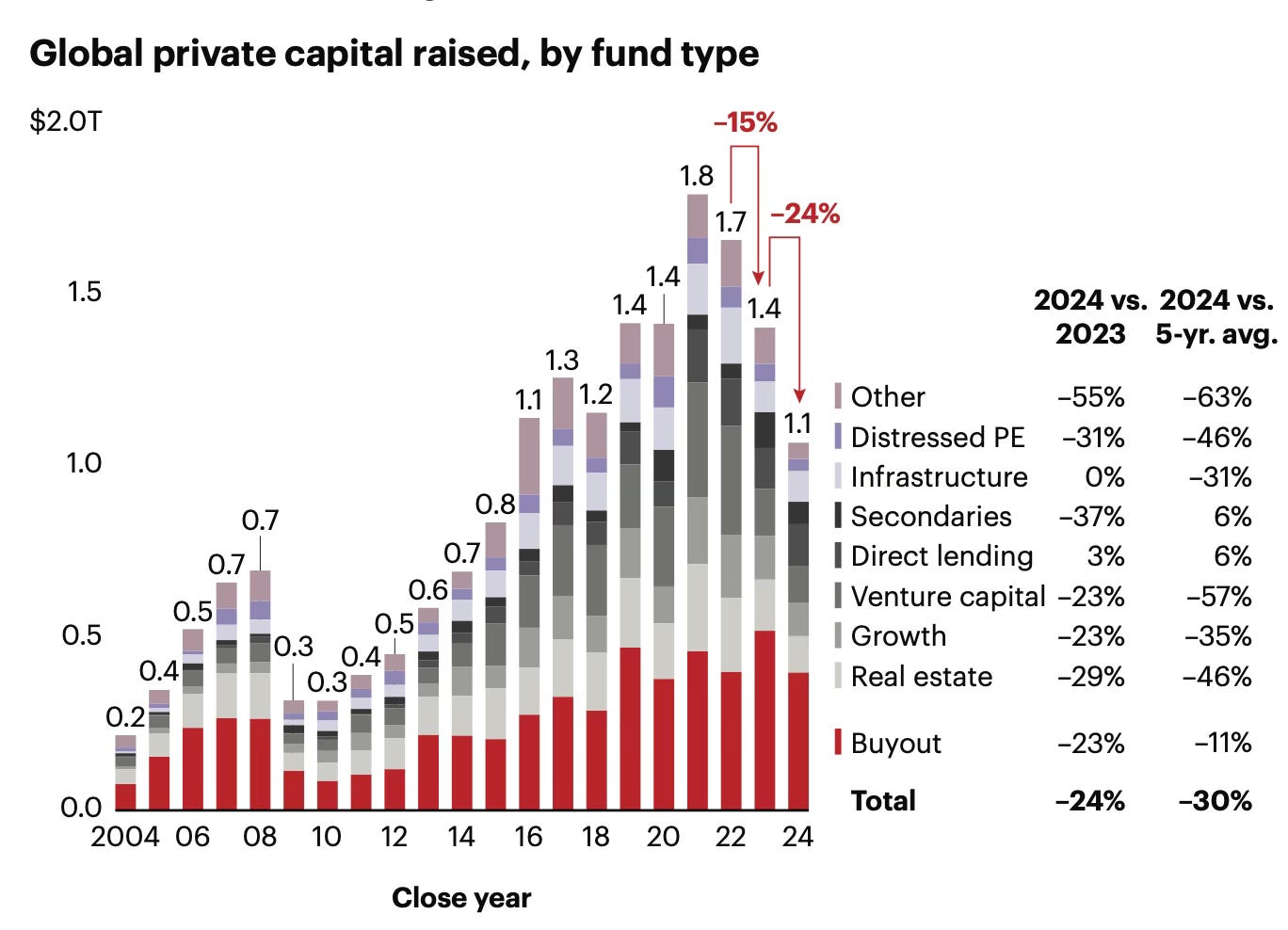

If so, the current dip in private capital fund raising was not going to last for years as funds struggled to get their money back. Instead, the surprise could be that by 2030 fund raising is making new highs. Like what happened in 208-2010.

If that’s the case, then maybe the Private Markets asset managers are good investments, even if private market funds aren’t.

Be the GP, not the LP.

Why do I bring this up today?

Because it’s our monthly review of the QARV rankings.

This is our YWR screen to find companies generating consistently high ROE’s with ‘relatively’ attractive valuations.

Link to the full QARV dataset is at the bottom of the post.

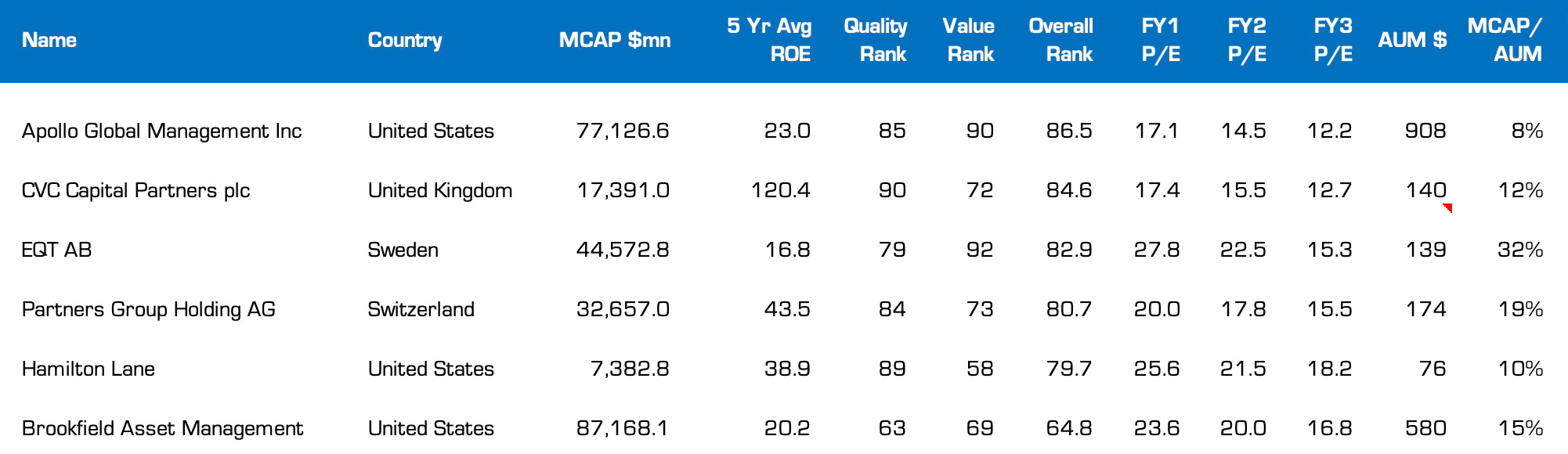

As I was scanning down the list this month, down past all the China stocks and Taiwanese semis, I was surprised to find several private capital managers like Apollo, CVC, EQT, Partner Funds and Brookfield.

Private capital fund managers don’t look screamingly cheap, but QARV loves their super high ROE’s, strong growth over the last 5 years and low debt levels. Valuation wise the P/E’s are < 20x’s and down from their previous highs of 30-40x (low P/E Z-score).

To be clear, these aren’t the best ranked stocks on QARV, those are the Chinese and Taiwanese stocks, but it surprised me to see private capital fund managers in the top decile.

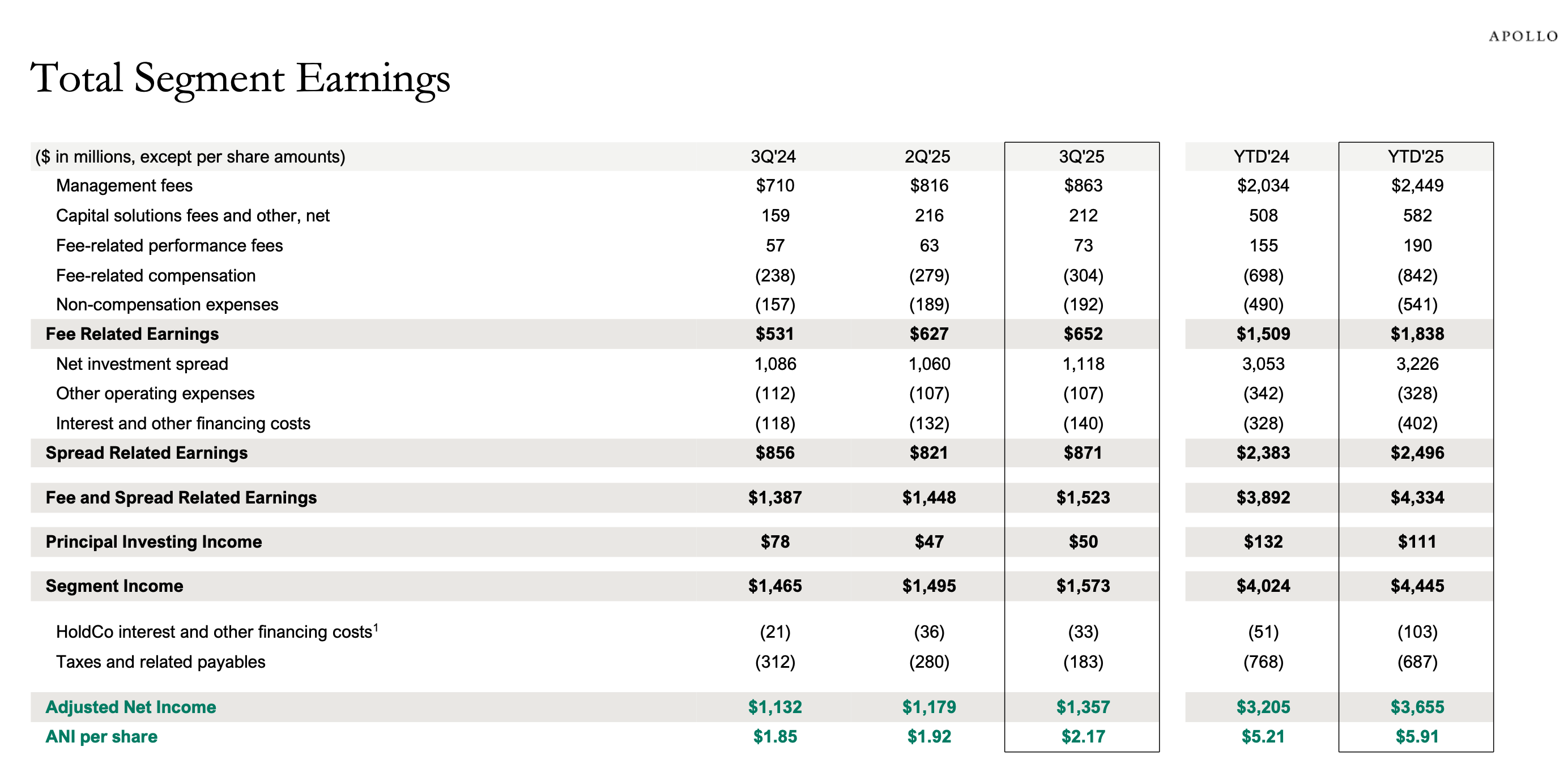

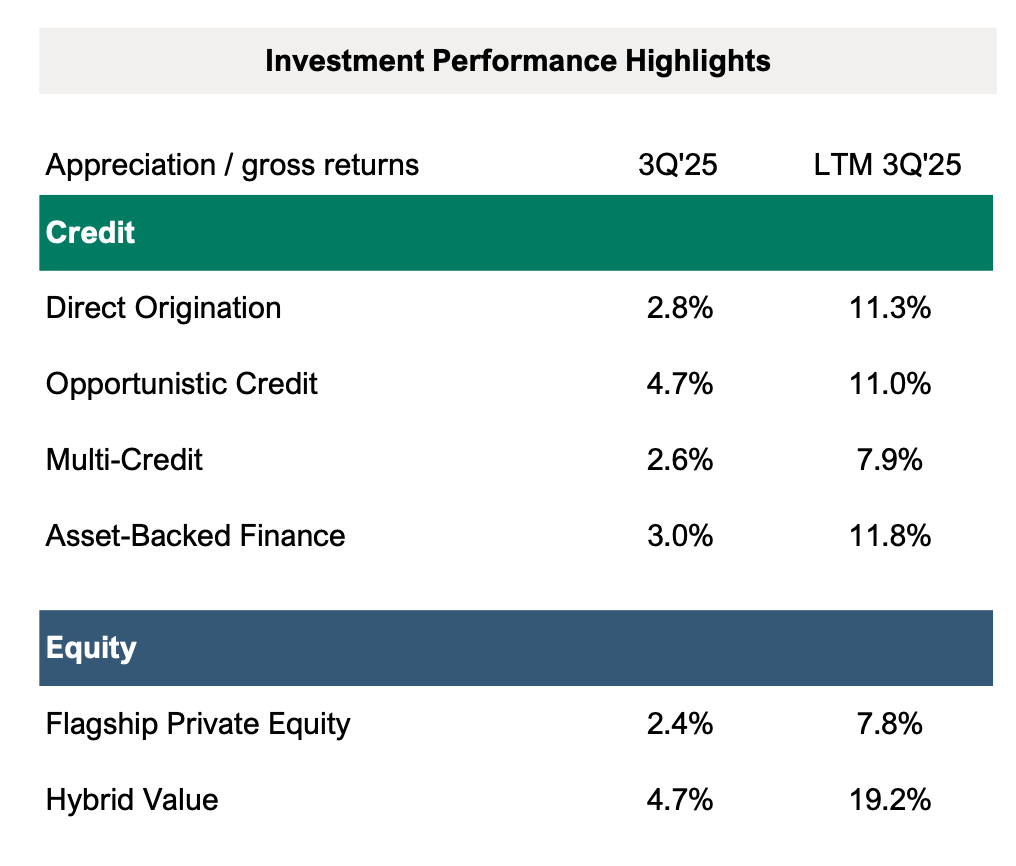

And when you go through the results for guys like Apollo, you see despite all the bearishness about private credit they are still cranking away.

Earnings are still growing.

Fund returns for private equity are ‘fine’, while private credit returns are surprisingly good.

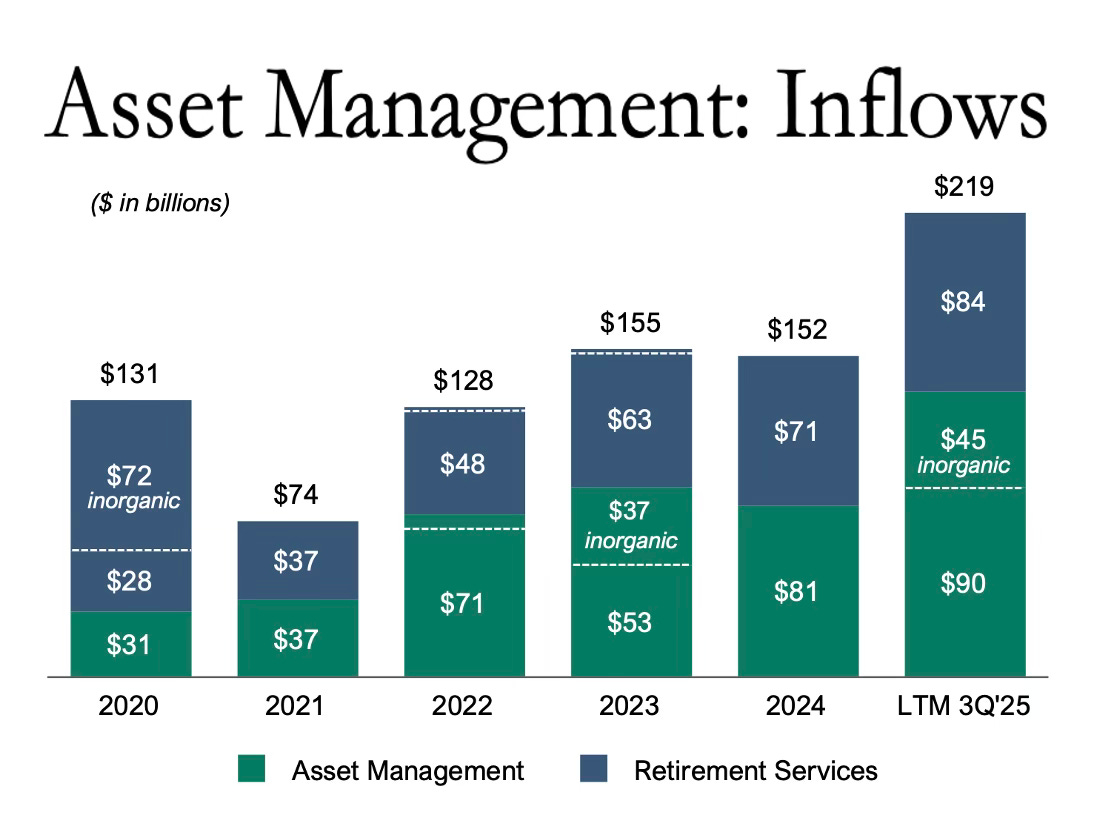

Fund raising is strong too and for Apollo making new highs.

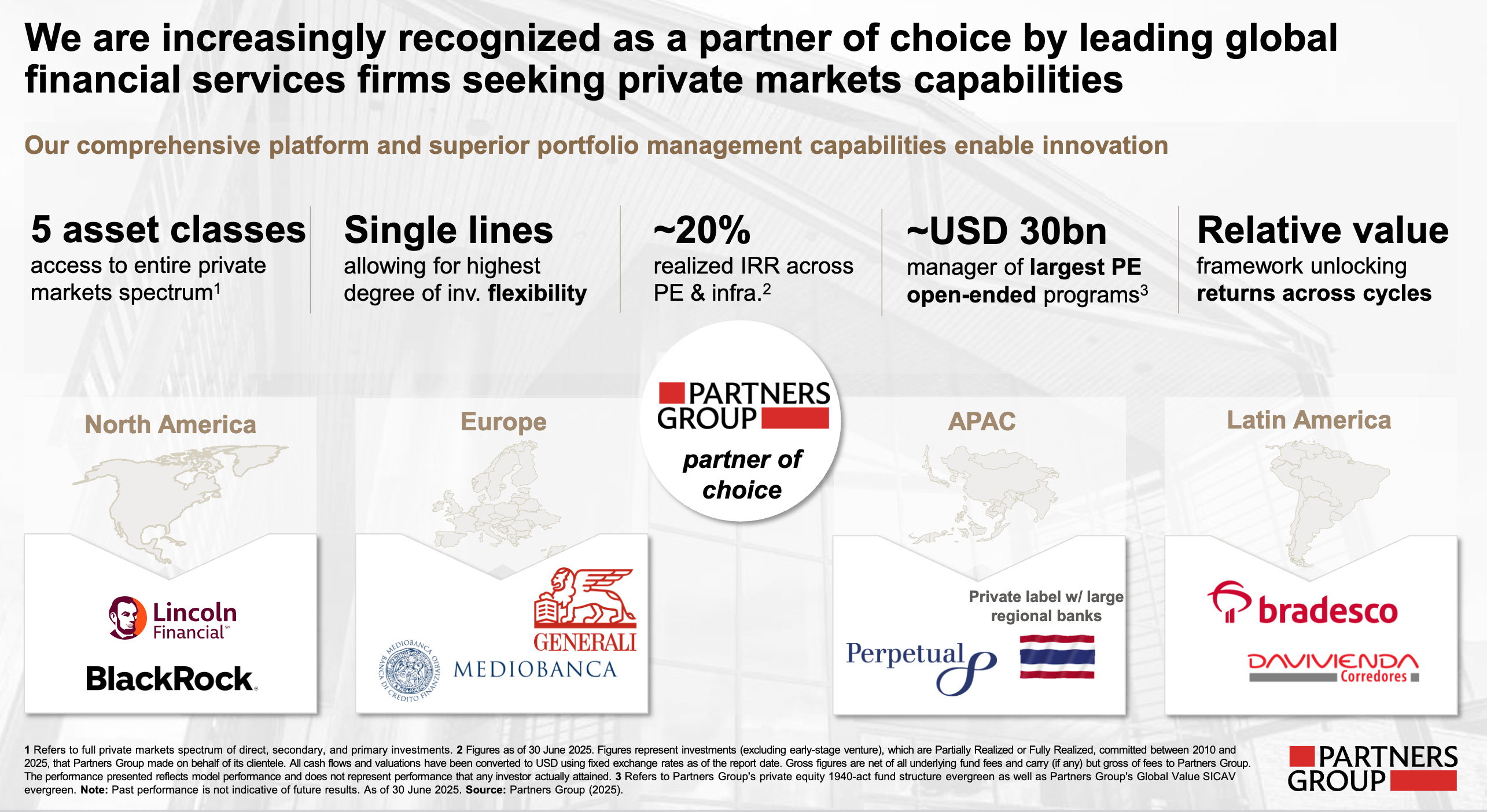

I have worried that with US pension funds and endowments already over allocated to private capital, where would the new bag holders come from. Then you see that companies like Partner Funds are already off to Thailand and Brazil busily converting the rest off the world to the private capital model too.

Global PE Lock in.

So how do we make money?

I said this realisation was depressing.

It’s depressing for the small equity fund manager hoping for a family office allocation. Hoping they will get a 45 minute meeting where they can impress the CIO with all the neat, undervalued companies they have found.

Depressing because most of that family office money is already locked up in long-term private capital vehicles, with future capital commitments as well. Yes, they can still get an allocation. It’s possible, but the challenge is that there just isn’t much money left to allocate to the scrappy, little equity manager. Most of the pie has been locked up. She’s been outsmarted, and outplayed by the big players.

But there is one thing the scrappy, equity manager can do, which no-one else is doing. One card to play.

Own the GP’s.

Own the performance fees and management fees.

Own the machine.

And that’s how you make money from PE Lock-In.

Below are links to the:

QARV Data App with AI Reports

QARV Rankings Sheet