YWR Infra Opportunities Fund

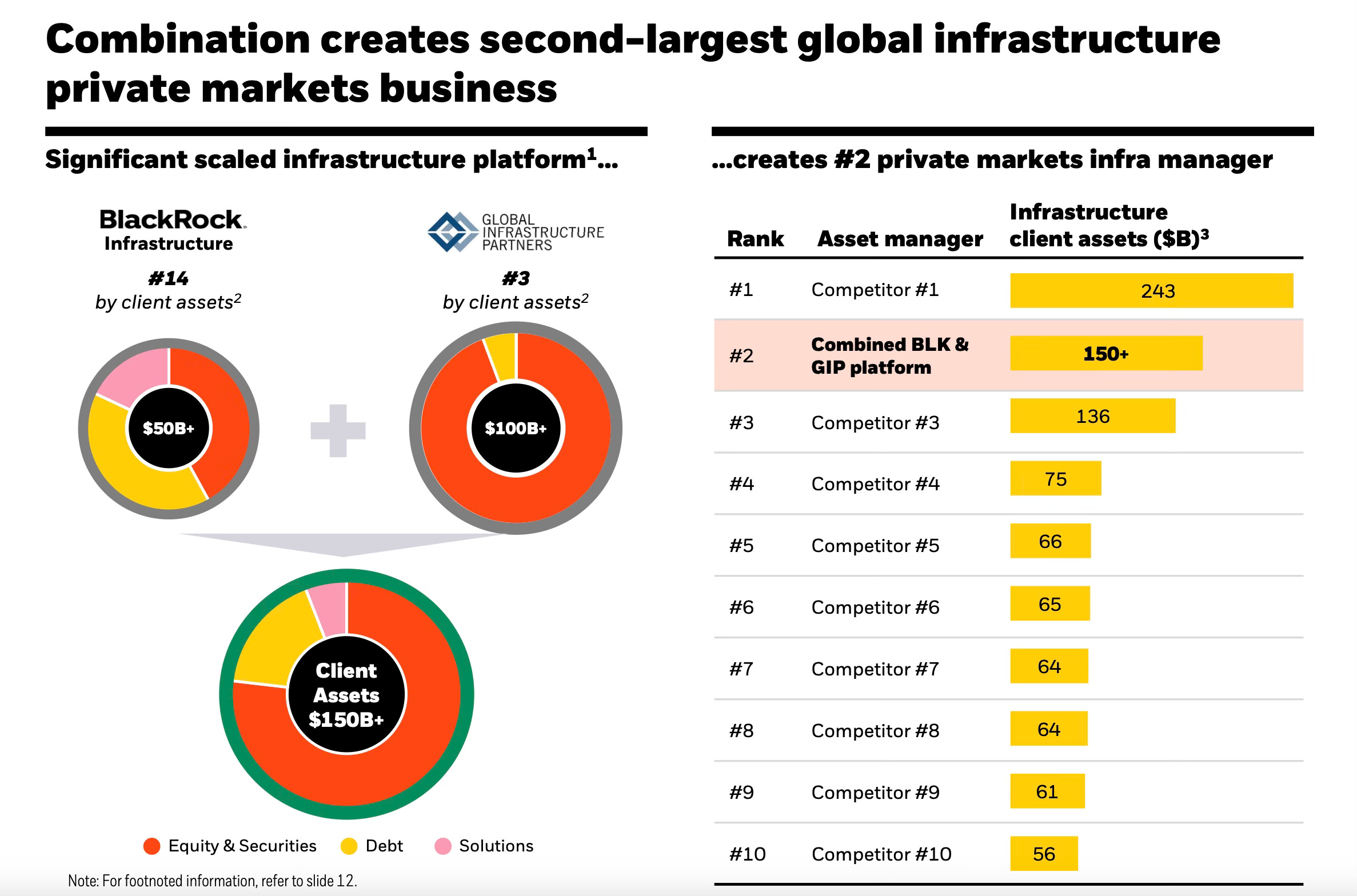

On January 12th we all wanted to be Bayo Ogunlesi. That was the day BlackRock paid $12.5 billion for his Global Infrastructure Partners (GIP). The consideration was 25x recurring fee based earnings.

And why did BlackRock decide they needed to acquire something? What strategy was so important they couldn’t grow it themselves?

BlackRock sees an opportunity to a leader in the private infrastructure space. Acquiring GIP made them the 2nd largest player behind Macquarie.

But what is so interesting about private infrastructure funds? Why pay over 25x earnings for a competitor?

I’ll give you 2 answers. The first answer is the marketing pitch. And it’s kind of true.

But I’ll give you the second reason infrastructure funds are so important to the alternatives industry.

Third, I’ll tell you how we make money on this trend. And it won’t be to invest in an infrastructure fund.

The Hero’s Journey (the Marketing Pitch)

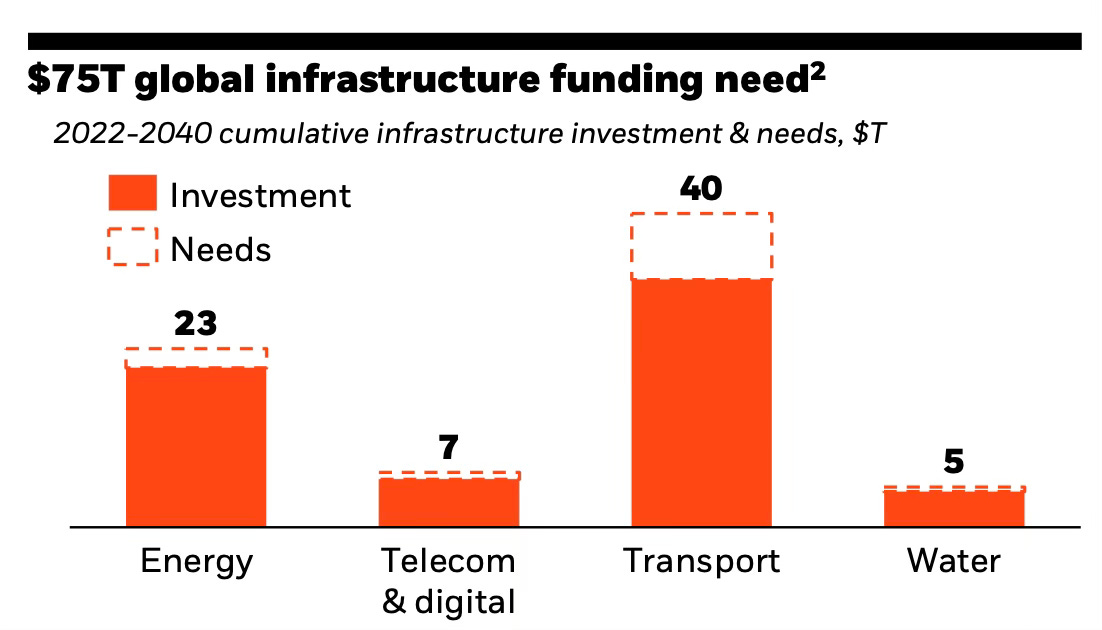

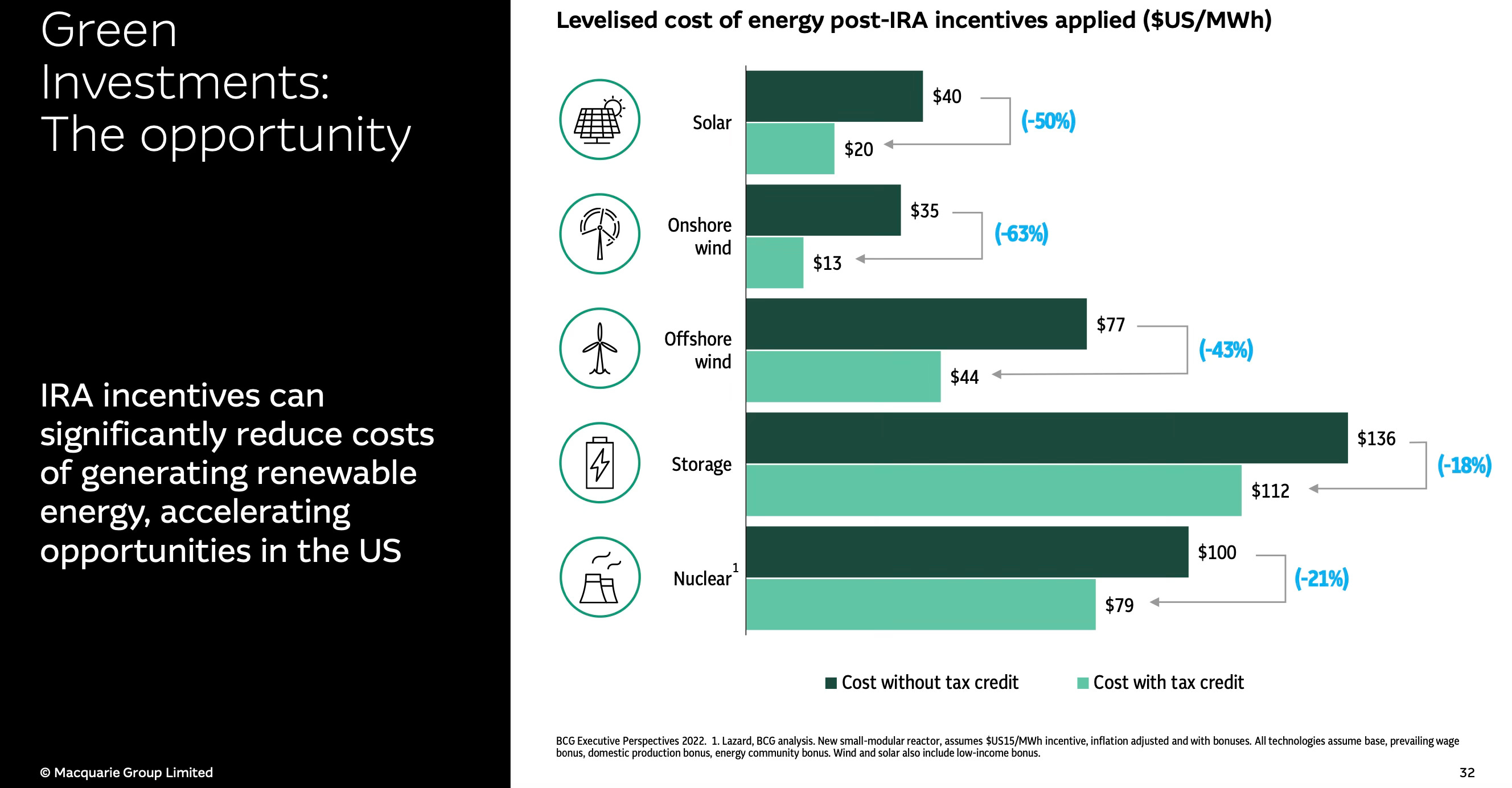

The story for the investor is that infrastructure funds are a great opportunity. They have performed well and there are vast new opportunities in renewable energy, transport and digital infrastructure (data centers).

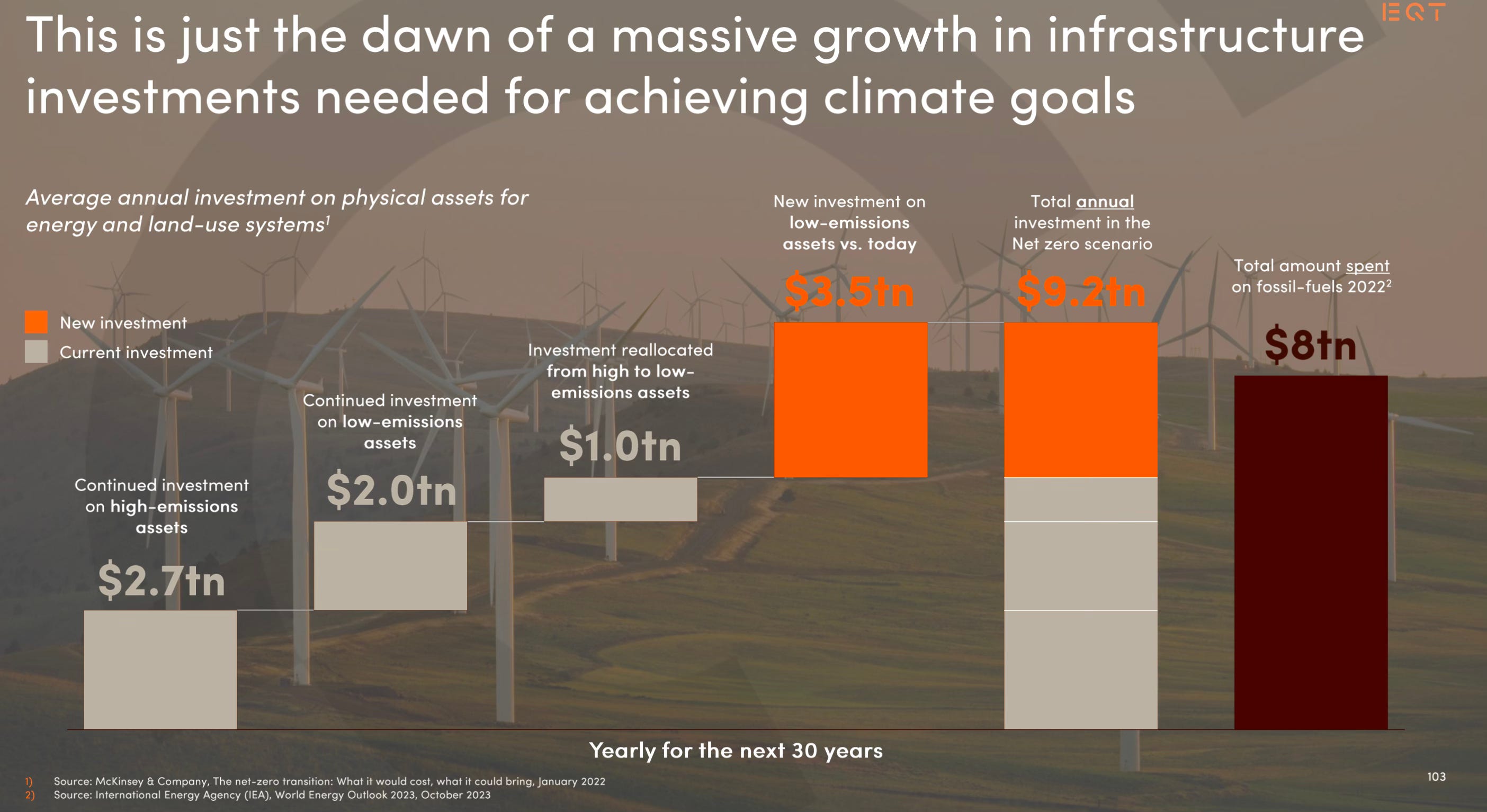

The world needs trillions of infrastructure investment to transform into a more sustainable state. And you the investor can help make the world a better place by joining BlackRock/KKR/Macquarie/Brookfield/EQT on this journey .

BTW, I am going to show slides from private equity presentations and investor days, plus our money maker idea, but doing my research I came up with more slides than a Substack post can handle. So I put all the slides from my research in a deck for you with a link at the bottom. It’s another doozy (82 slides).

BlackRock’s Infrastructure Pitch

The world needs trillions in infrastructure investment…

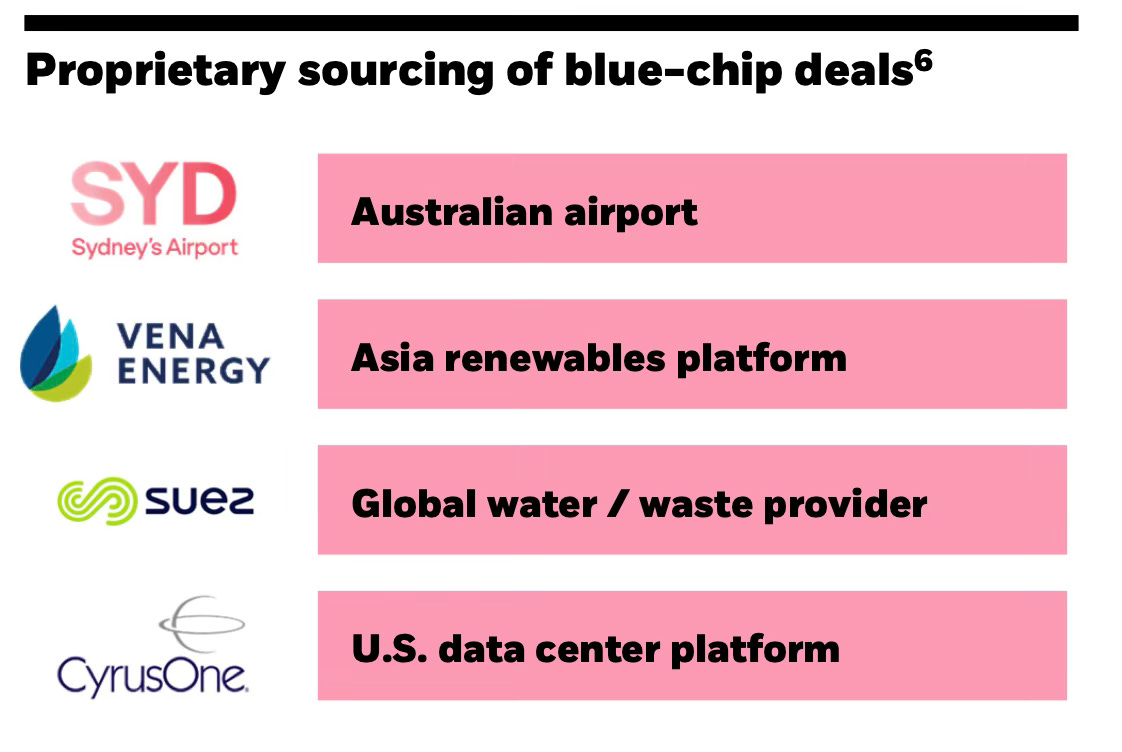

The opportunities are in renewables, datacenters, waste water and airports. We have platform companies for these opportunities.

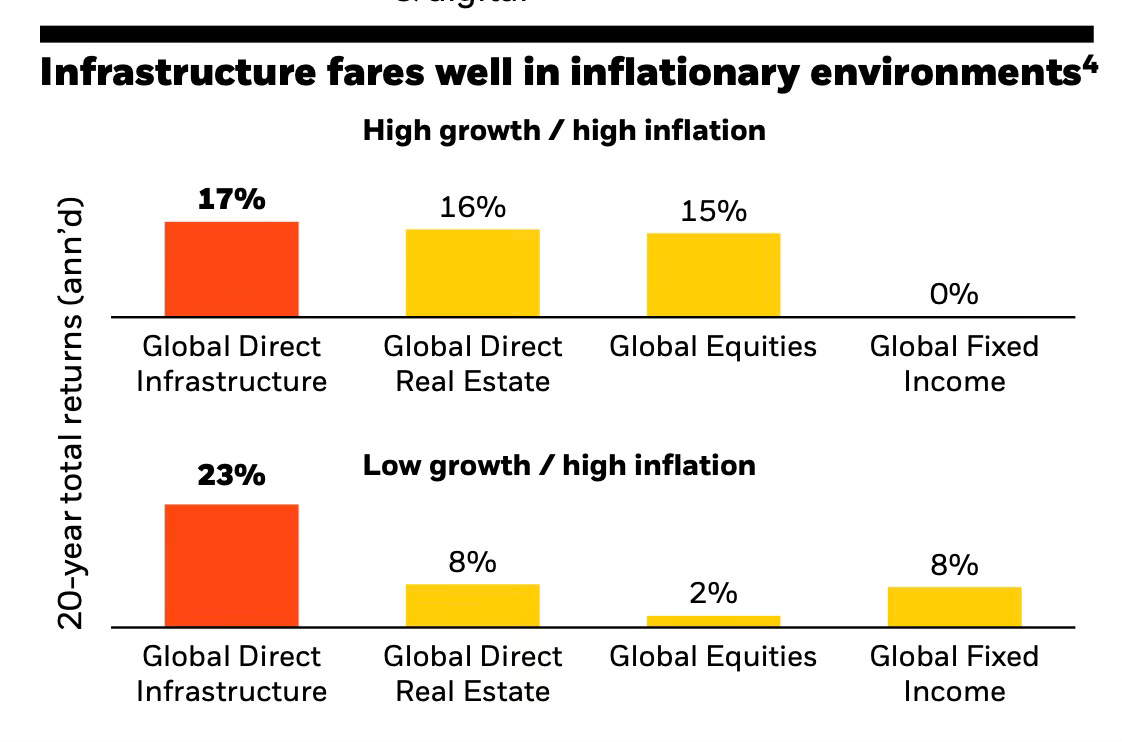

Make double digit returns whether interest rates are low or high.

Macquarie Pitch

We’re #1 in infrastructure. There are opportunities in green energy and data centers.

Did we mention we have a datacenter platform?

EQT Pitch

Trillions are needed to meet the climate change goals.

You will make double digit returns investing in infrastructure.

Did we mention we have a datacenter platform?

Reason #2 (The real reason)

The real opportunity behind ‘infrastructure funds’ is it’s something new to sell.

Pension funds are already over allocated to the private equity and real estate buckets.

So what do you do if you are a private equity firm?

Create a new bucket of course. ‘Infrastructure’.

How we make money

If BlackRock/EQT/Macquarie and Brookfield are going to raise trillions from pension funds and sovereign wealth funds around the world and invest it into infrastructure assets… then what should we do?

Naturally, we should front run the infrastructure funds and buy shares in a listed company which is already one of the largest owners of infrastructure assets and concessions globally. They own half the tollroads in France and are the biggest operator of airports globally.

This company also has an infrastructure construction business which specialises in building toll roads, solar farms, wind farm, bridges, tunnels, tank farms, etc.

So we get it both ways. Our existing infrastructure assets become even more valuable, and we use our construction business to create new assets to sell to the private equity firms.

We also earn a 4% dividend yield. It’s not a dripping roast, but it will steadily grow (6% CAGR) and I expect this company will be doing share buybacks as well in 2025. If inflation picks up the tollroads, which are literally a cash cow, are directly indexed to inflation in France.

I’ve put a link to the model and the presentation below.