YWR: June QARV

Interesting asset allocation tidbit.

If you run a global quality screen with value factors the results end up overrun with Chinese stocks.

There are so many highly rated Chinese stocks you have to filter them out. Which we do.

Don’t worry. The full unfiltered rankings are at the bottom of the post along with a link to the QARV data app.

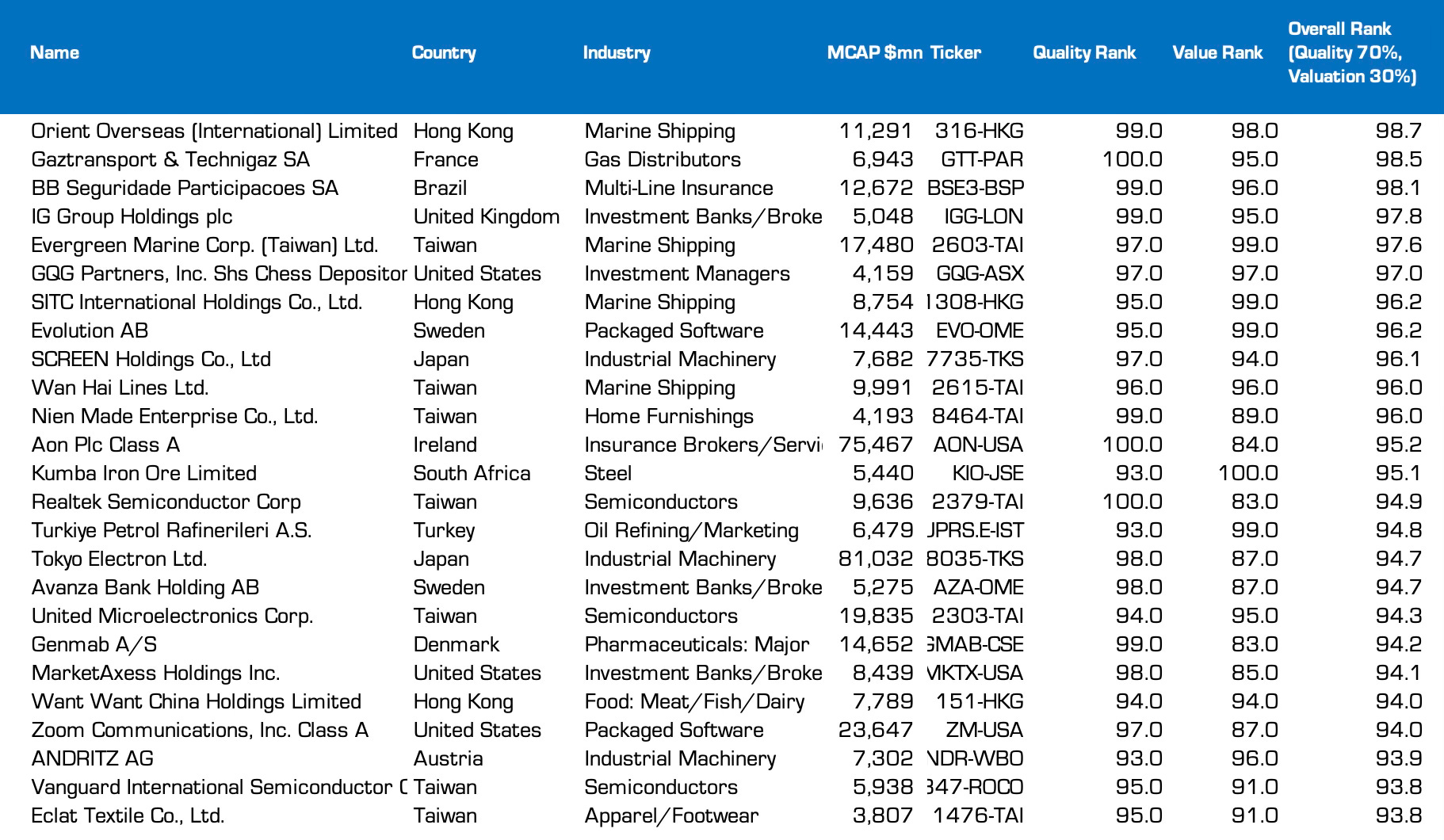

Below are the top 25 ranked QARV stocks as of June 12th (ex-China).

Top 25 Global QARV Stocks* (June 2025)

The quality part of ‘QARV’ is based on average annual financial data so the quality rankings don’t change much month to month. This means many of the same sectors keep showing up each month, which gives a chance to take a deeper look at why these high ROE sectors are trading at low valuations.

For example, in May we looked at the rising long-term ROE of container shipping companies. Despite 30-40% ROE’s and no debt, the stocks are trading below book value. Investors keep assuming the recurring spikes in container shipping costs are one-offs and not sustainable. However, when we looked deeper we realised yes, there were one-offs, but the sector was benefitting from the growing logistical complexity of the China + 1 trend. Investors were missing the trend behind the trend and over discounting the sector’s cyclicality.

And so this month we investigate another highly cyclical sector which scores well on the QARV rankings. And here again, like with container shipping, investors are over discounting the cyclical risks. Investors are missing the subtleties of the sector and why the high ROE’s are more sustainable than investors realise.

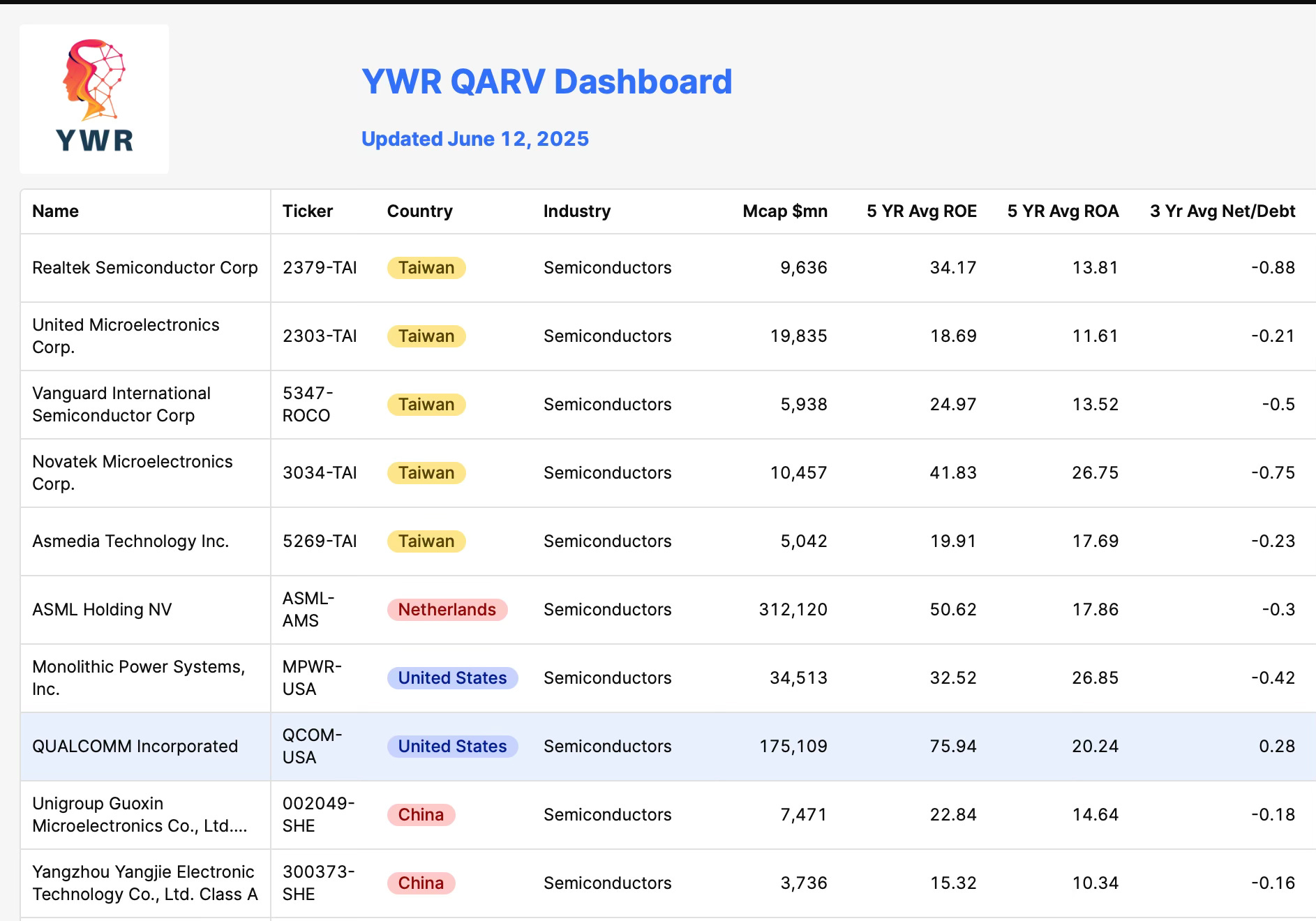

It’s semiconductors. Especially, Taiwanese semiconductors.

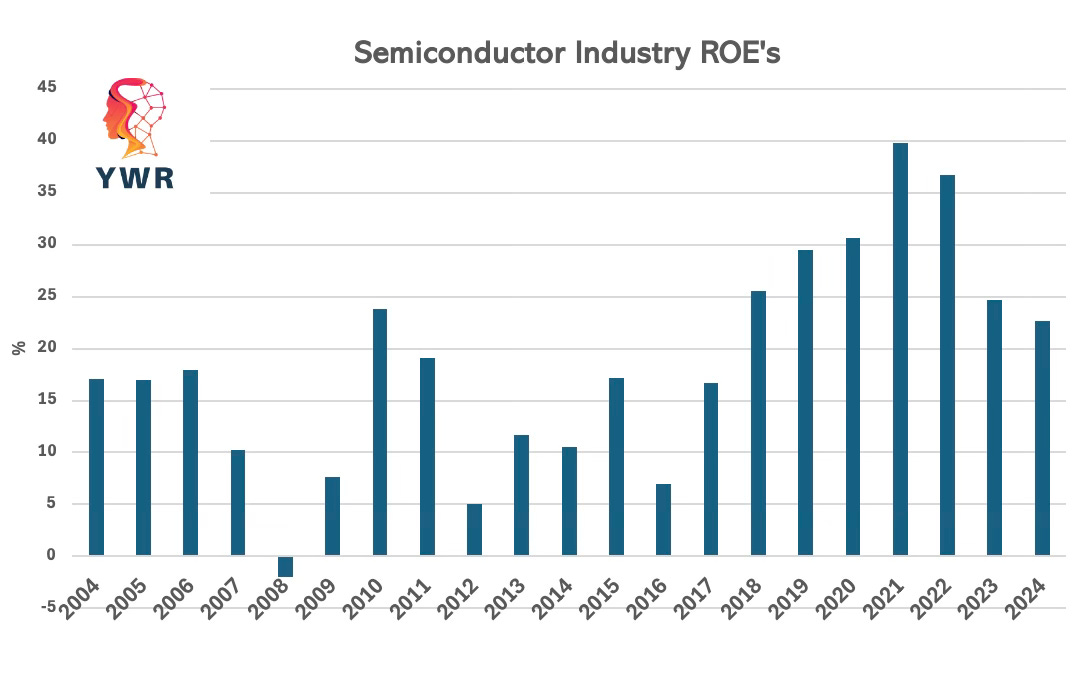

A decade of Semi-conductor outperformance

Starting in 2015 the average ROE for the semiconductor industry started to rise. There was still cyclicality, but instead of 5-10% ROE’s, the range started to rise to >20% on average.

Despite this 10 year structural improvement in semiconductor profitability semiconductors are one of the biggest sector underweights for institutional investors. Investors appear to have missed this long-term trend, and keep missing it. Why?

Why do investors not like Semis?

In the 1990’s semis were hot and investors made a lot of money. But then from 2000-2015 the sector lost its secular growth. It became less profitable and more cyclical.

Investors shifted their focus to internet stocks and software.

Semis are hard to understand. Very technical. It’s much easier to understand SaaS.

The industry is highly fragmented with many layers to the supply chain. Hard to know the importance of each layer.

Investors are terrified of the cyclicality of anything with inventory and supply chains.

What are investors missing?

Several things.

Its not 1999 again. Investors are trying to draw parallels between today’s AI surge and the 2000 tech crash. Instead, this wave resembles the cloud computing buildout post-2010: methodical, capital-heavy, and driven by hyperscalers with real cash flows and enterprise demand. Capex is growing year after year, not peaking.

Moore’s Law is slowing—and that’s bullish: With transistor scaling hitting physical limits, capacity growth is now expensive and time-consuming. That moderates the historical boom-bust supply cycles. You have to buy more units.

Fabs cost $50 billion and are highly technical projects. These are such big investments that foundries are extremely careful with how they bring on supply.

This is year 3 of a multi-decade cycle. Major cloud and enterprise buyers are not speculating—they’re responding to demand from Fortune 1000 companies (not Pets.com).

The Taiwanese semi-supply chain is a bunch of mini-Nvidias.

Maybe it’s the early 1990’s again and ‘hard tech’ not software is the new hot thing.

Thank you The Curious Mind for flagging this great podcast with Val Zlatev where they really dig deeper into the semi-conductor theme and what investors are missing.

Resources

Below are links to the update QARV Data app and Google Sheet as of June 12, 2025.

Grab a coffee and go through the rankings and data on over 3,000 global stocks. Let me know if there are new trends we need to dig into.