YWR: Killer Charts

40 slides on:

$4,500 gold

Xiaomi: the Apple Killer

Blackstone: how to be a GP not an LP.

Soggy S&P 500 earnings estimates

The Rule of 10x and how to make $ in European banks.

As usual, the full Killer Chart pack is at the bottom of the post and in the YWR library.

But let’s hit the highlights.

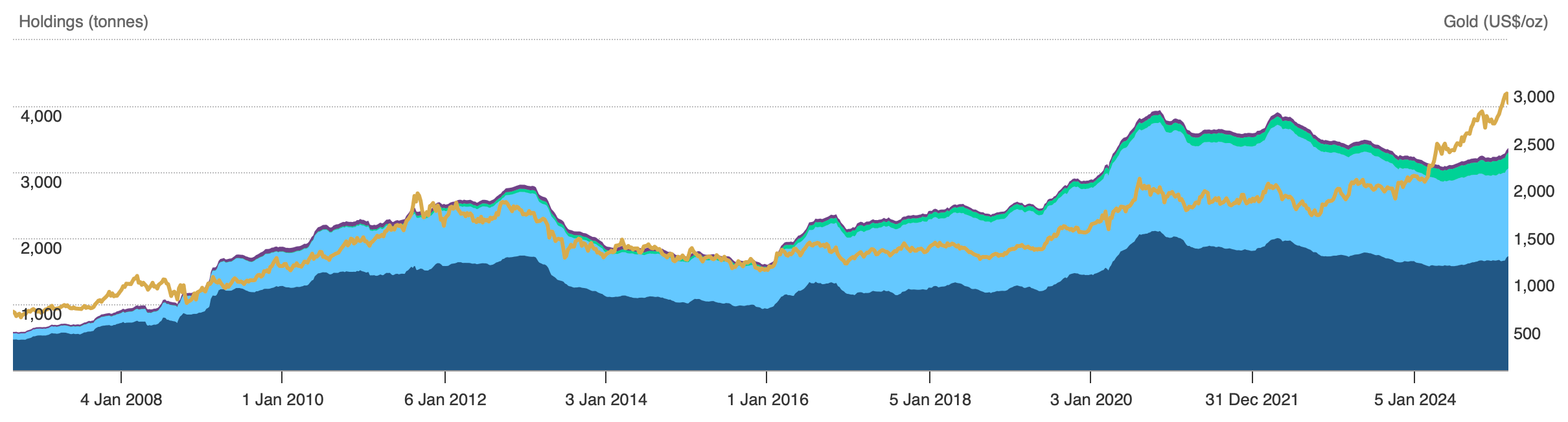

$4,500 gold:

It’s a top theme and one of the 5 surprises for 2025.

So I love that the World Gold Council ETF flow data shows despite a +50% move in gold to $3,000 oz we’ve only had 1 big month of retail inflows… February.

Gold is making new highs and yet total ETF gold holdings are still below the highs of 2021.

Retail has been selling gold the whole way up.

In the presentation there is also an interesting chart on Central Bank gold buying, which adds to the squeeze.

Do you know what this means?

It tells us we are still early in the trend. The denial phase.

A blow off top is yet to come.

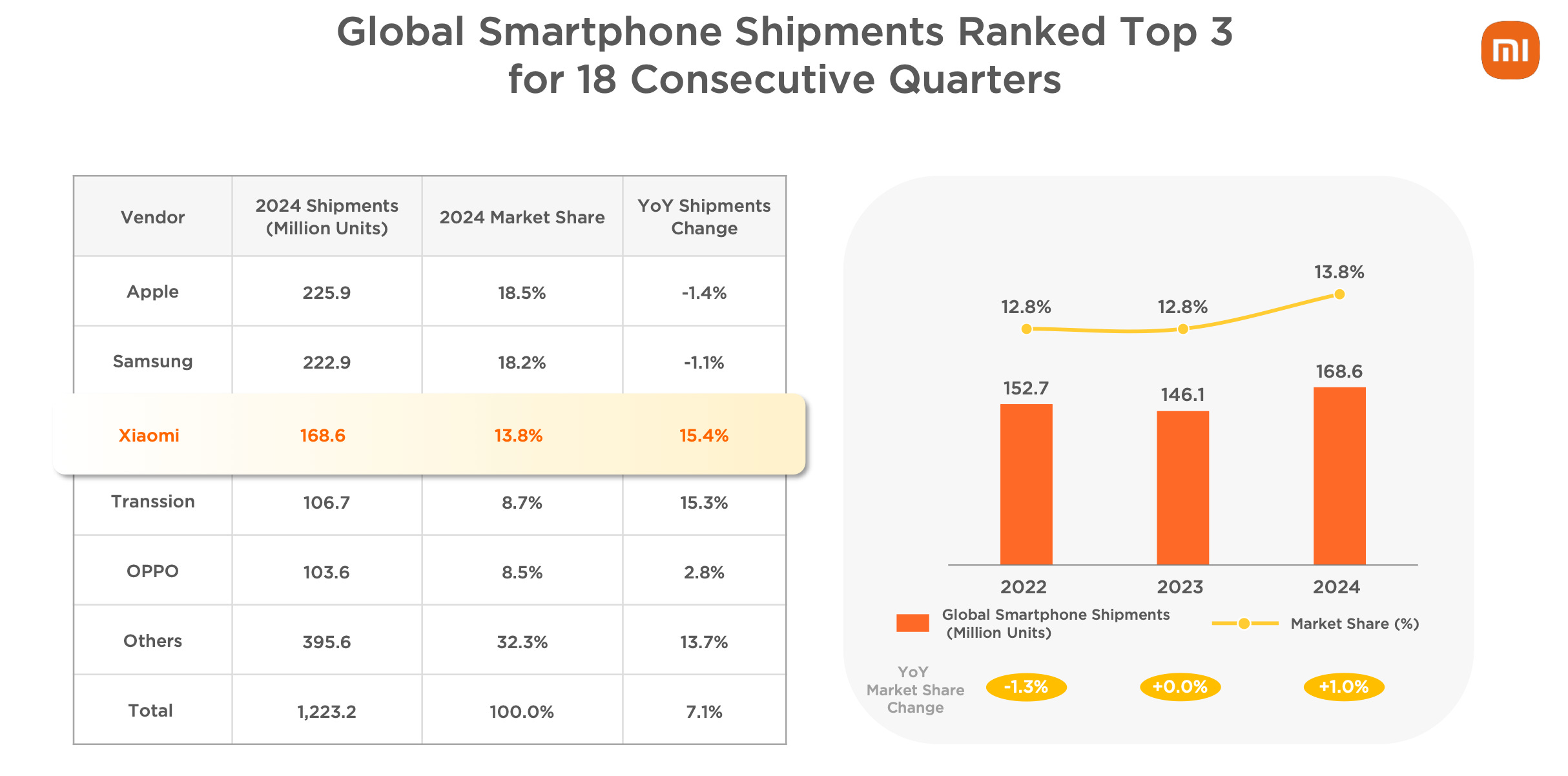

Xiaomi: The Apple Killer (1810 HK)

It’s not a name many investors know, but it should be getting more attention.

Especially, since Xiaomi is eating up global market share in smart phones, tablets, home electronics, and now cars.

Xiaomi is the 3rd largest seller of smartphones globally and growing sales +15%, while Apple and Samsung are in decline.

Xiaomi is also the 5th biggest seller of tablets globally, and growing.

I feel like many investors are living in a bubble.

They don’t spend time outside the US and Western Europe. They don’t go to Africa, the Middle East, or South Asia and see how brands like Xiaomi and Transsion are gobbling up the world markets.

Brands like Apple and Western car companies are getting boxed into a smaller and smaller market.

If the dam breaks and Xiaomi gets momentum in Europe it will do serious damage to Apple.

010

Southeast Asia

Smartphone Shipments

(Million Units)

Latin America

Smartphone Shipments

(Million Units)

0010

Middle East

Smartphone Shipments

(Million Units)

olo

6.1

2023

8.4

2024

13.0

2023

010

16.3

2024

19.0

2023

22.7

2024

9.2

2023

10.9

2024")

And Xiaomi is doing what Apple should have done. Make the car.

And sheesh… what a car. Look at the specs on the SU7.

0-100km in 2 seconds. Top speed of 359km/hr.

It’s a Porsche 911 GT3 for $70,000.

You can see the network effects Xiaomi is creating. Make the phone, the tablet, the home appliances and the car and have it all interconnected with their AI system.

We’re losing the ground game.

Blackstone: Be a GP not an LP.

I think if I were a CIO I’d find the Blackstone results annoying.

If I’m in a mix of their funds I’m probably making 7% on an IRR basis (which is an inflated way to measure it, but oh well).

Real Estate

Opportunistic

Core+

Private Equity

Corporate Private Equity

Tactical Opportunities

Secondaries

Infrastructure

Credit & Insurance

Private Credit

Liquid Credit

Multi-Asset Investing

Absolute Return Composite

4.9%

3.5%

2.8%

4.8%

3.1%

2.4%

3.7%

FY'24

0.1%

16.6%

10.1%

7.8%

21.0%

15.7%

9.5%

13.2%")

I’m up 7%, but then Blackstone, the GP, is completely creaming it and their earnings are +96%!

Management fees, incentive fees and performance fees up 64%, and then operating leverage.

Do you know what I’d be thinking?

I’d be thinking I’m getting played.

If I’m bullish on PE why be in the funds?

Why not own a basket of KKR, BX, CG and APO?

Stop being an LP and become a GP with much better economics.

But the problem is public stocks like BX can go up and down 30%, and we don’t want that. That’s volatility.

And you also have to be sure about the PE cycle, which personally, I’m not. But if we get a bigger sell-off and want to get bullish on PE maybe buy the GP not the fund. It’s what Mubadala figured out by buying Fortress.

In other PE news, it’s worth noting bankruptcies are rising, but not at alarming levels given the growing size of the industry.

Soggy S&P 500 Earnings estimates

It’s not a crisis, but more a yellow flag that S&P 500 EPS estimates for 2025 are sliding.

From $280/share in July last year we are down to $271.

8

이19!2024

이26!2024

04t03i2024

041이2024

0417!2024

0424!2024

0원01i2024

0신0털2024

0靄5i2024

0원2기2024

0원3이2024

0턴06i2024

0하13i2024

0텐21i2024

0텐2털2024

07!08仁024

07녀5i2024

07!2기2024

07!29i2024

0일05i2024

0하1기2024

0鬧9!2024

0텐26i2024

0이03仁024

0%이2024

0이17t2024

0이24i2024

1미01i2024

1엲08仁024

1먢15i2024

1미22仁024

1미2희2024

11!05t2024

11!12i2024

11!19i2024

11i26仁024

12t04i2024

12t11i2024

1기1엷2024

12t26仁024

01!03i2025

01서3i2025

01!21i2025

01!28仁025

02t04i2025

02녀1仁025

02너9i2025

02t26仁025

0친05i2025

이12!2025

03녀9i2025

0")

And the index is still trading at a high forward P/E on an E which is slipping.

0

나)

0

돈

0

미

0

다,

0

월

0

㉦

0

0

다

g

守

진

m

0

그

0

守

甬

0)

다

0

그

0

0친1떻2015

0모15i2015

07i14i2015

0희0희2015

11!04i2015

01i04i2016

이0가2016

04%!2016

0텐24i2016

0친2가2016

1엲1일2016

1거14i2016

02너3i2017

0411!2017

0하0하2017

0하04i2017

1엲0기2017

11i2엷2017

01)26i201B

이26i201B

0원2기201B

0薺相!2018

0%4i201B

11!0떻201B

01!1이2019

0친11i2019

0모07i2019

07i03i2019

0하2희2019

1미25i2019

1가23i2019

0기21i2020

042이2020

0텐16i2020

0하1기2020

1미0하2020

1기04i2020

0기03i2021

04田1i2021

0모2털2021

07!27i2021

0년2기2021

11서7i2021

01서4i2022

0지15i2022

0원11i2022

07i11i2022

0떻06i2022

11m 1) 2022

1거2인2022

0기2하2023

0426!2023

0하23i2023

0친21i2023

1엲17i2023

1기13i2023

0기1기2024

041이2024

0하0하2024

0하05i2024

1엲01i2024

11i26i2024

01i2털2025

0

0

雲

0

0

圖

0

0

0

0

0")

But don’t worry.

If the S&P 500 makes you nervous there are always the European banks.

The Rule of 10x and making $ in European Banks.

Europe is suddenly getting a lot of attention and inflows.

But is there more to go?

What happens if investors actually turn ‘Bullish’ on Europe.

If so, there could be more to go in the banks.

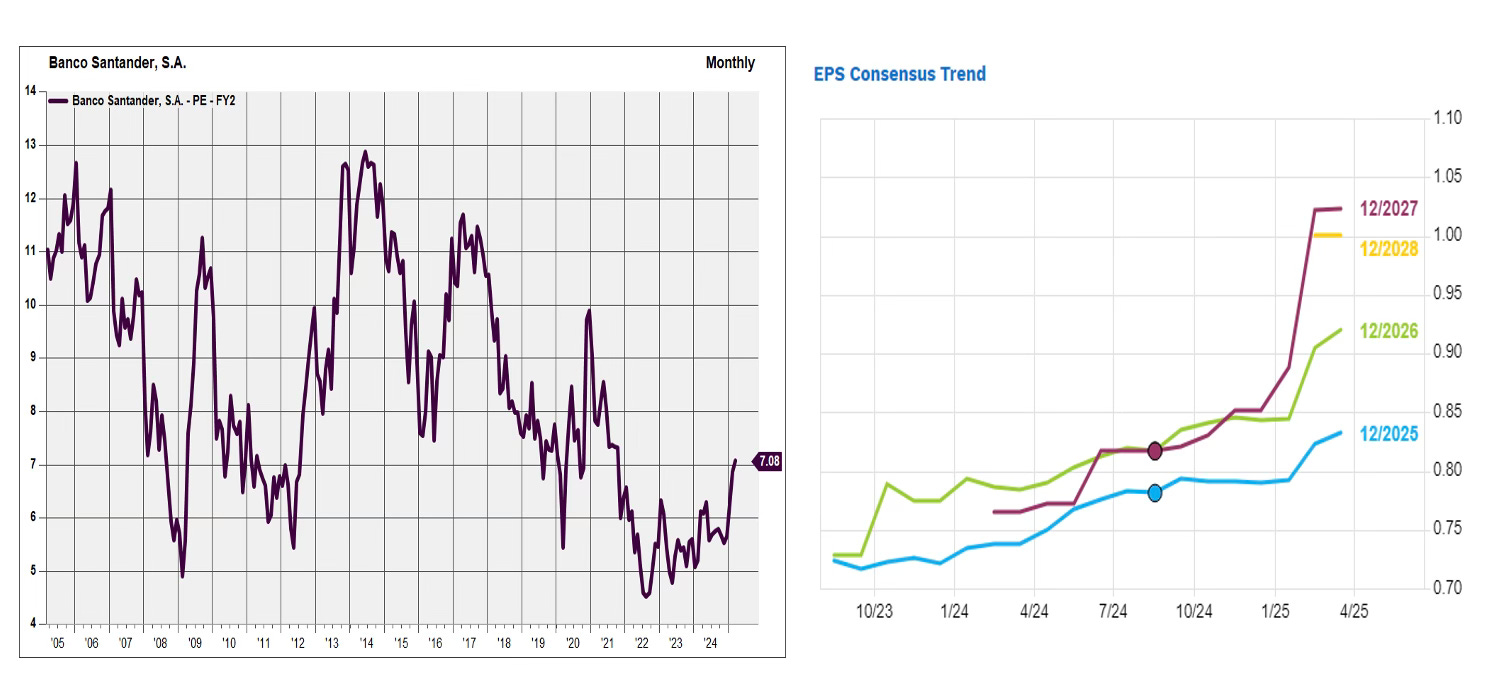

For example, what if investors are willing to pay a P/E of 10x for Banco Santander, one of the best global banking franchises in the world?

I mean what if?

I’ll let you decide how crazy things can get, but historically, the FY2 P/E (so 2026) has ranged between, 5x and 12x.

We are currently at 7x.

The 2026 EPS estimate is rising and roughly 90cts.

If it’s not unimaginable for Santander to trade on 10x the 2026 estimate you get EUR 9/share.

That’s another 38%, not including dividends. And by then the market could be looking out to the EUR 1/share EPS in 2027.

In the full chart pack I did the same chart analysis for Unicredit, Barclays, HSBC, BNP, SocGen and Piraeus.

Take a look and consider what might happen if investors get bullish on Europe.