YWR: Killer Charts

Disclosure. Just market commentary. These are not investment recommendations, for that seek professional help.

Let’s get going.

The Big Tech Rally Everyone is Missing.

This Tweet by Kuppy sums up the ytd for most all hedge funds.

Revenue growth for big tech has been slowing and fund managers were not expecting a reacceleration of the rally to new highs fuelled by AI.

Earnings have been growing, but the multiples have been expanding too. Note the increasing allocation to capex.

Buffet pioneered the company which doesn’t pay out dividends. Amazon pioneered the company which doesn’t make a profit.

The Record Profit Bank Crisis

In March while the regional bank ‘crisis’ was raging I wrote why this was not going to be 2008 again, and that I was bullish on banks.

Investors were underestimating/not understanding the large gains that were going to flow into net interest income from the higher Fed Funds rate. Yes, the expense for loan losses is higher, but the magnitudes are different. We needed the Q2 2023 results to see the actual numbers behind this.

Look at the far right column on the JPM Q2 earnings slide. Net interest revenue is +$5.8bn compared with Q2 2022. Down in th memo you see excluding the investment banking business it’s +$7.8bn. Massive. Credit costs are up. Yes. +$600mn. Overall effect; net income is +$3.4bn.

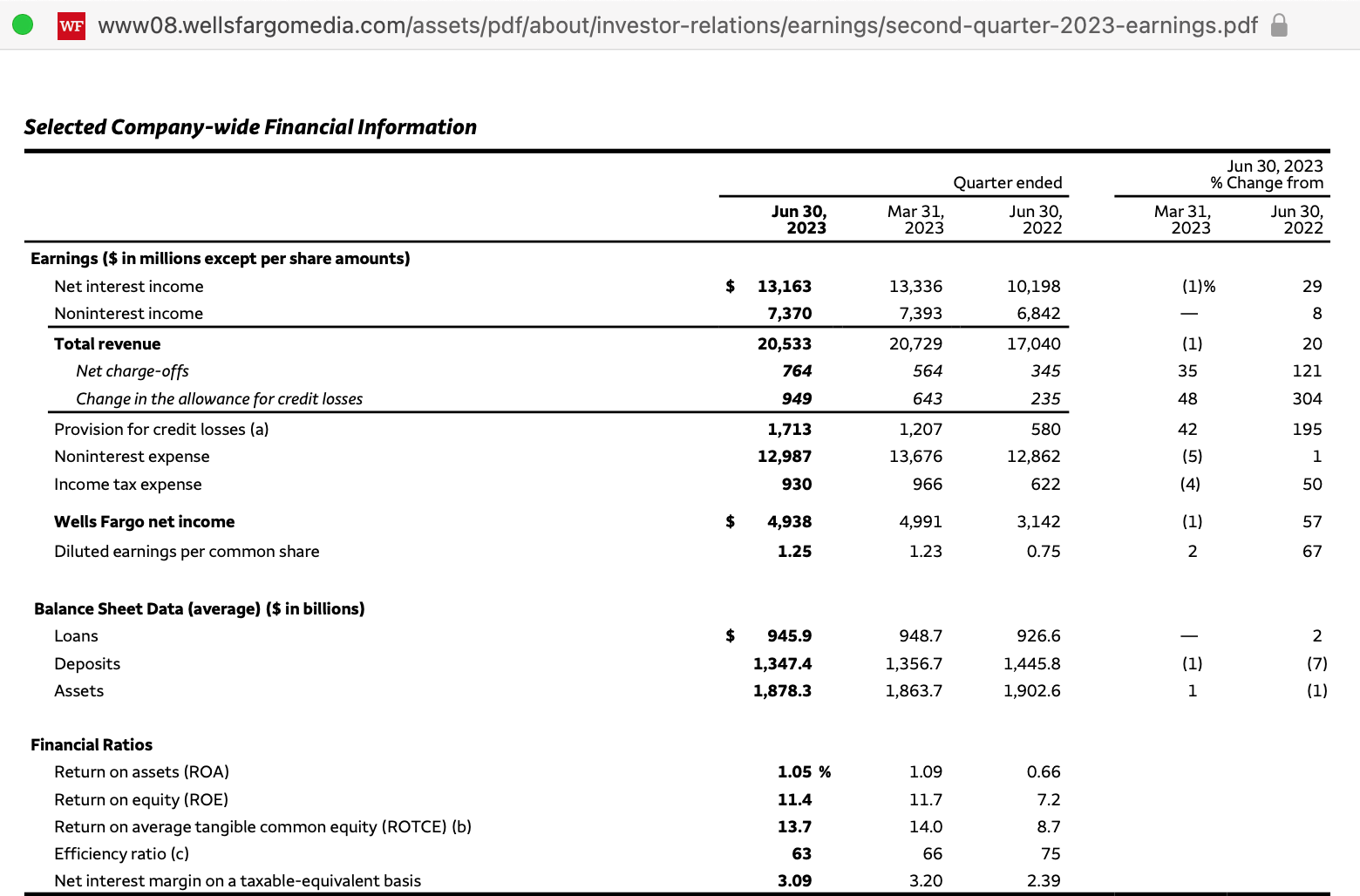

Look at Wells Fargo. It’s similar. Net interest is +$3bn vs. June 2022 while credit costs are up +$714 mn = Net income +$1.8bn yoy. 67% EPS growth.

Bank Stocks Bull Case

Bank stocks aren’t expensive (almost record low valuations in Europe)

Investors still severely underweight the sector

Net interest margins still expanding as balance sheet reinvests into higher yielding assets.

Shorting US banks is considered one of the most crowded trades (see BofA chart below).

I prefer playing this same theme, with even more juice, in Europe (The upside everyone is missing in European banks).

Charts from BofA June Fund Manager Survey

The BofA survey confirms the other work we’ve done on sentiment, fund flows and positioning.

Investors are skeptical on the market and the pain trade is still up.

Investors’ view of the economy is bearish.

Sentiment and cash levels show investors are afraid to invest in the equity market.

They’re either afraid they missed it or just happy to earn 5%-6% on money market funds and 2yr bonds.

It’s interesting to see investors are waiting for lower interest rates, or higher growth.