YWR: Killer Charts

Disclosure: Personal market views only. Definitely not investment advice or guidance. For that seek professional help.

Let’s whip through positioning and sentiment, then hit UK mortgages, Semis and China.

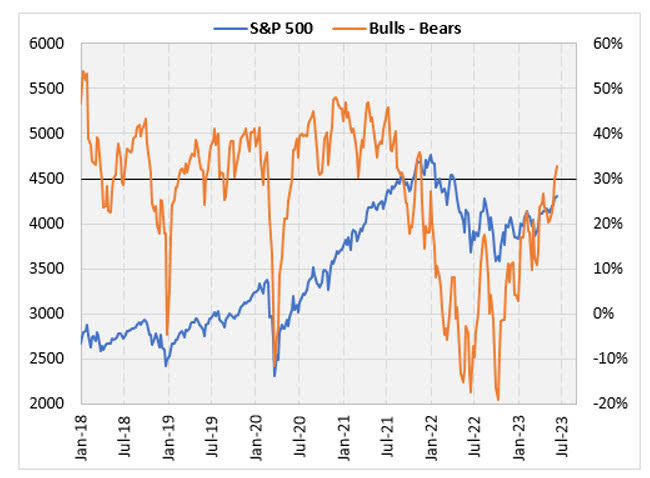

Sentiment has definitely reset for the S&P. Not extreme, but not the tailwind it was. Earnings growth will have to carry the market from here.

Fundamental Equity Long/Short hedge funds (dark blue line) have switched their positioning and are no longer so bearish.

In October 2022 the net was 45%. Now it’s back to 55%. Just above average over the last 5 years (63rd percentile).

S&P 500 share buybacks are running at record levels. Making up for fund flows that show investors are not really buying the market (they like money market funds and bonds much more).

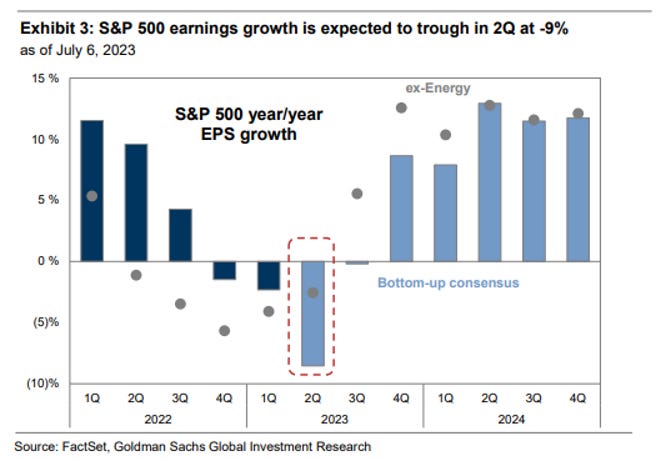

It’s worth noting that S&P 500 YoY EPS growth is about to turn positive. Ex-energy the EPS growth runs at 12%.

In the latest S&P Institutional survey institutional investors’ aren’t that positive, but their favorite sectors are Healthcare and Staples.

Real Estate, Financials, Mining, and Consumer Discretionary are still hated.

The favourite markets are Japan and rest of Asia.

China,Europe and the UK are most hated (and hence the most interesting!). The UK looks really extreme.

Globally investors love government bonds and hate commodities….

I had drinks with some fellow investors visiting London from the US and the conversation turned to the high level of negativity on UK housing. Everyone is bracing for what happens when mortgages reset to higher rates. It’s a concern, but we have 2 years to prepare and in the meantime maybe ask for a raise (30,000 Reasons Wages Aren’t Falling).

Ever since I saw the extreme semiconductor capex plans announced after Covid (in response to the temporary chip shortage), I thought there would be multi-year problems ahead. It reminds me of the mining industry’s capex boom in 2012.

Most semi companies have revised down their capex plans slightly since 2021, but Samsung and TSMC are still charging ahead.