YWR: Killer Charts

Stevie’s bearish…

US growth is likely to slow in the second half of the year as tariffs, tighter immigration laws and government cost-cutting efforts led by Elon Musk weigh on the economy, billionaire Steve Cohen said.

“I’m actually pretty negative for the first time in a while,” Cohen said. “It may only last a year or so, but it’s definitely a period where I think the best gains have been had and wouldn’t surprise me to see a significant correction.” BBG

So this month let’s do some bearish charts.

I’ve picked out 10 bearish charts from the YWR Killer Charts February slide deck with charts from:

BofA Fund Manager Survey

BofA Flow Show

Goldman Sachs

Apollo

S&P 500 Earnings Estimates

A link to the full slide deck is at the bottom of the post.

Ten Bearish Charts Stevie Would Love

#1. Cash levels at active funds are at record lows.

#2. Nobody thinks a hard landing is possible.

We’ve come a long way from 2023. Now only 6% think a recession is possible in the next 12 months. That’s always when they come. You need businesses, and investors to get confident and over order, over build, over leverage. This sets up the recession. It doesn’t happen when everyone is cautious.

#3 US real GDP estimates are sliding.

It’s still over 2% growth, but down from 3%.

#4 Fund managers see the market as the most overvalued since 2001.

It’s not a great combo for investors to have the lowest amount of cash, plus think the US market is the most over valued it has been since 2001.

#5 ‘Tail risks’ 2-5 all seem likely. Especially, falling AI capex.

These tail risks look increasingly ‘base case’, especially the possibility of an AI capex overshoot.

The market shrugged off the implications of DeepSeek, but now we are getting signs that MSFT is reducing its data center build out. BTW, weakness in data centres would be terrible for the PE industry, which is all in on ‘digital infrastructure’.

Our Channel Checks Indicate Microsoft Has Cancelled Select US Data Center Leases and Has Pulled Back on SOQ To Lease Conversion; Pulls Back on International Market Expansion.

Our recent channel checks indicate that Microsoft has terminated select leases with at least two private data center operators across multiple U.S. markets, totaling a couple of hundred MW. Our checks indicate that in some situations, Microsoft is using facility/power delays as a justification for the termination. Recall, as we highlighted in our 2022 Takeaways from PTC, this is the same tactic that Meta used to cancel multiple data center leases in the U.S. after we learned in our checks that Meta had then canceled a $48B capex program related to the metaverse (Meta subsequently cut its capex guidance by $5.4B two weeks later). Source: TD Cowen

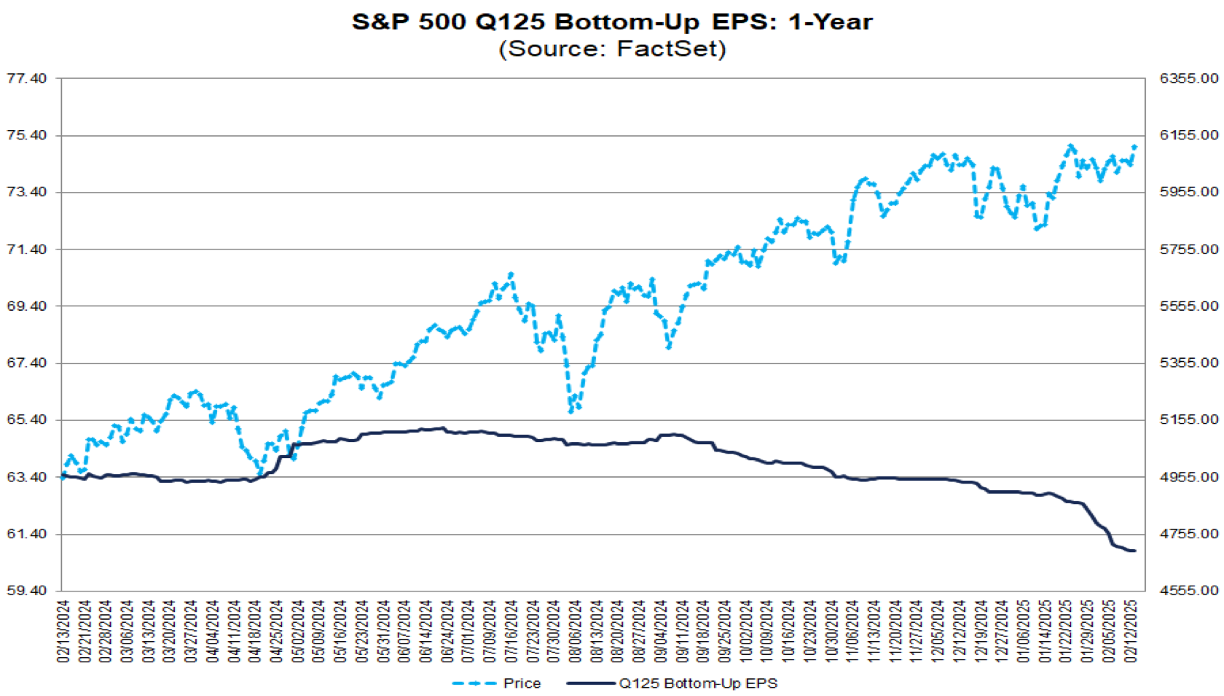

#6 Earnings estimates for 2025 are starting to slide.

Estimates for Q1 2025 are 6% lower than they were back in May 2024. This is still within the range of acceptable noise, but the divergence between the market going higher, while estimates are softening is a yellow flag.

#7. Hedge fund gross exposure is at record highs.

Hedge funds are doing well, and volatility is low, so funds have taken their gross exposure to record highs.