YWR: Killer Charts

Disclosure: This is personal market commentary, not market recommendations or guidance. For that seek professional help.

We’ll review charts on the stresses building in US multi-family real estate, some massive wage deals, and then on to whether it’s time to buy bonds.

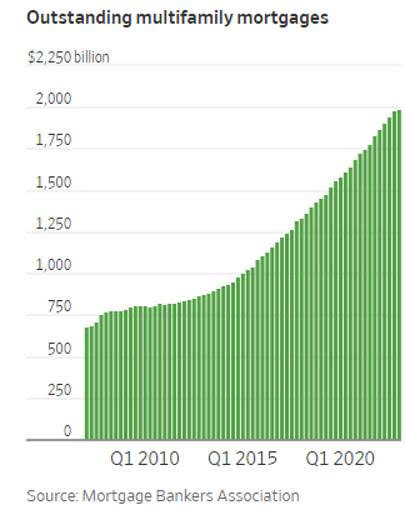

I’ve always loved multi-family RE. I guess everyone else does too. Big move in loans outstanding from $750bn to $2.2 trillion.

NEXT REAL ESTATE PROBLEM - Apartment buildings, long considered a real-estate haven, are emerging as the next major trouble spot in the beleaguered commercial-property world. Investors bid up the prices of multifamily buildings for years, attracted by steadily rising rents and the prospect of outsize returns. Many took on too much debt, expecting they could raise rents fast enough to pay it down. Unlike office buildings and malls, which have been hit hard by remote work and e-commerce, rental apartments have low vacancy rates. The apartment sector’s main problem isn’t a lack of demand—rents have soared since 2020—it is interest rates. The sudden surge in debt costs last year now threatens to wipe out many multifamily owners across the country. Apartment-building values fell 14% for the year ended in June after rising 25% the previous year, according to data company CoStar. That drop is roughly the same as the fall in office values. (WSJ)

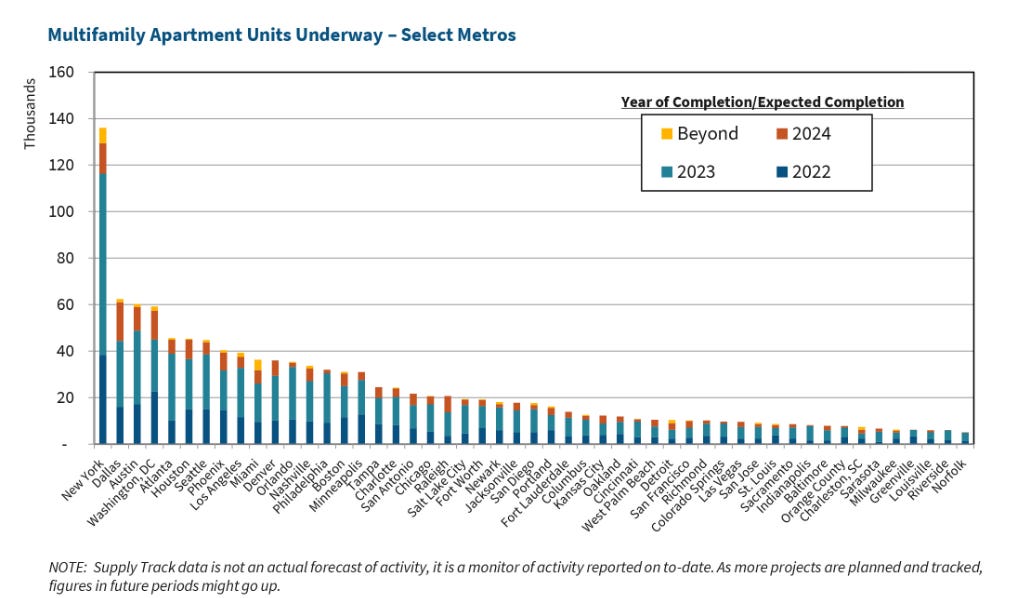

Compounding the interest rate problem is a surge in new supply on the way. This always happens at the end of good asset class cycle (same thing in semis).

It looks like investors may have over played the theme of workers moving to Texas and Phoenix. Huge supply in NY too. Detroit still looks good (Why Detroit is the New Austin).

Multi—family cap rates probably have to move to 6% (which isn’t too bad). It really depends on where LT rates go from here.

We’ve been discussing why some wages need to move in clips of 30%, not 5% (30,000 reasons wages aren’t falling), but I’m a little surprise how strongly this is playing out.

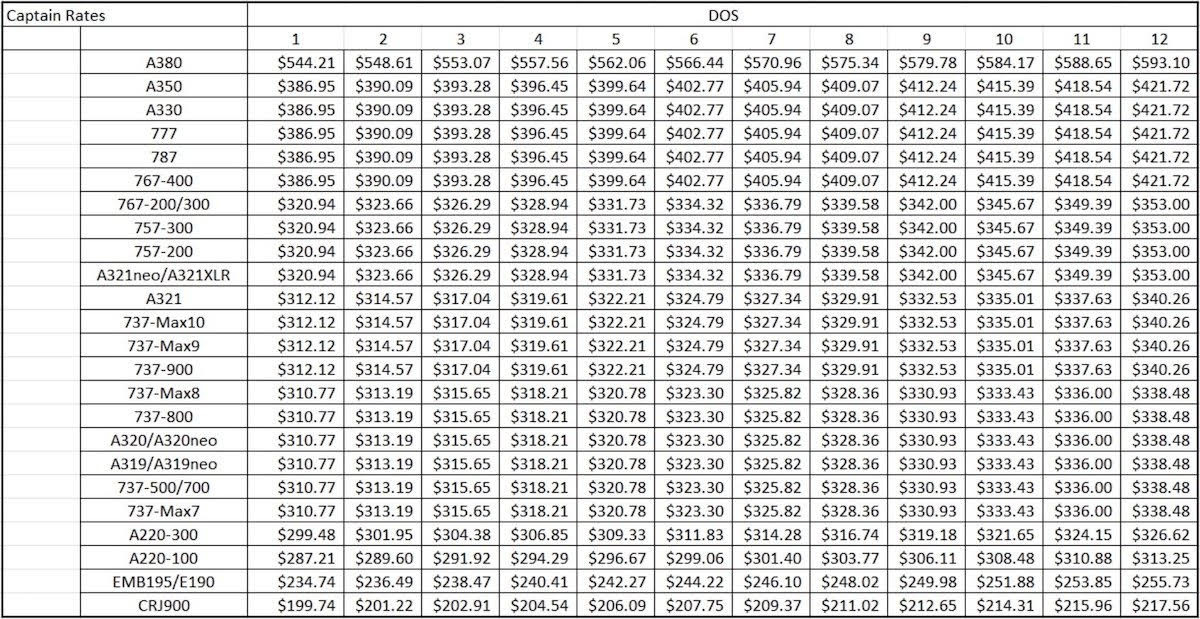

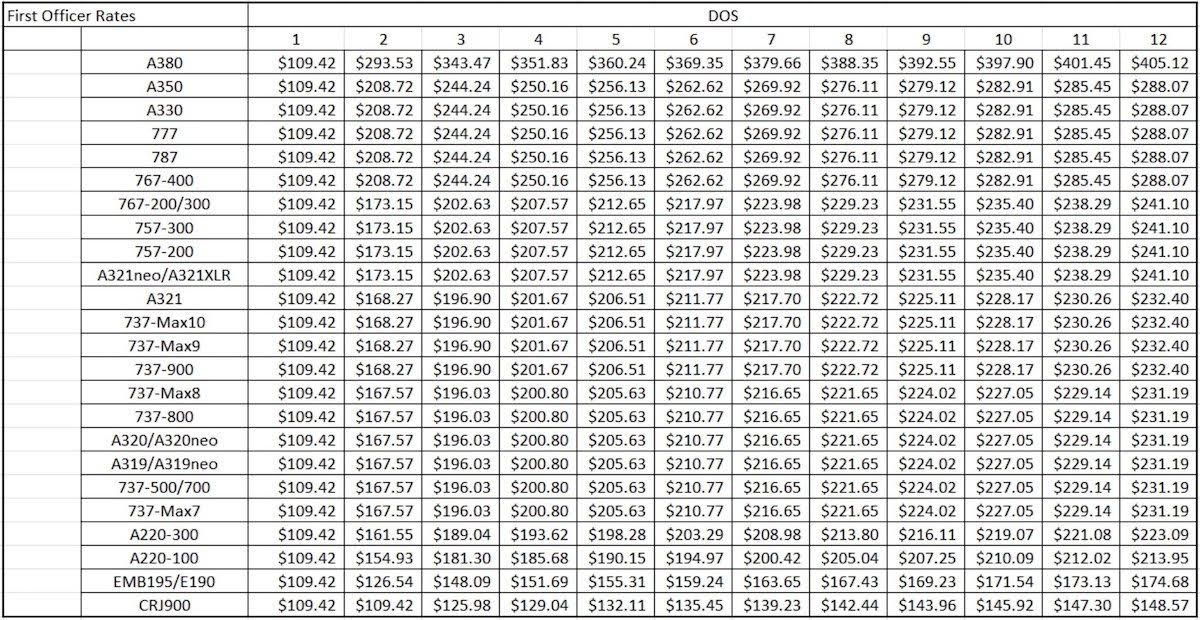

Below is the new pay scale for pilots at United. These are hourly numbers, so basically add three 000’s to get an annual number.

I respect the extreme responsibility of being a pilot, tough conditions…..etc, etc, etc, but I’m a little surprised a pilot for a 737 flight from Denver to Phoenix is making $325k/year, and the co-pilot is making $210k.

And UPS drivers making $170k?

In London we’ll see where tube driver wages end up, but I’d say it’s looking good.

There are two ways to look at this:

This is Project Zimbabwe, and the wage driven inflationary cycle is in full effect. This is why core inflation will remain high into 2024 and beyond.

Or… this is setting up for a massive whipsaw if we get a downturn.

What is going to happen at United and UPS if we get a sudden downturn, activity drops off, and these companies are staring at drivers with half full trucks, done by 3pm earning $170k, or pilots with half full planes earning $300-400k?

Does it turn into an abrupt slash and burn and the unemployment the Fed has been hoping for arrives with surprising force?

Did we all over play the inflation story? Did the multi-family apartment owners raise rentals too much and are going to find demand is more elastic than they thought (other places to live)?

EQUITY BEAR - JPMORGAN’S KOLANOVIC SAYS SOFT LANDING FAR-FETCHED, AVOID STOCKS - As equity valuations price in economic optimism, JPMorgan Chase & Co.’s chief equity strategist Marko Kolanovic is maintaining a defensive stance and reiterating the bank’s call to stay underweight equities. “We disagree with the market’s expectation that soft landing is the most likely outcome,” Kolanovic says Monday in note to clients. Kolanovic warns multiples look “too high,” with central banks unlikely to ease near-term, ongoing quantitative tightening and his team’s base case for macroeconomic slowdown. (BBG)

So how might one make money on the whipsaw scenario?

Here are a few potential set ups.