YWR: Making Money in Exchanges

We have a new money making exchange idea.

But first we need to review the results from our holdings in SGX and HKEX. Gotta eat your vegetables.

Plus it’s good market awareness to track these capital markets and know which products are growing. It might give you other ideas.

We bought these positions last year (SGX an Exchange Masterclass, HKEX our China FOMO Play), even though they looked expensive, because we expected earnings expectations would radically change. The E would be much higher than expected.

We predicted a bull market in Asian stocks was about to unfold. And the sell side, as is typical, lacked imagination on where earnings were going to go.

Where are we with that view?

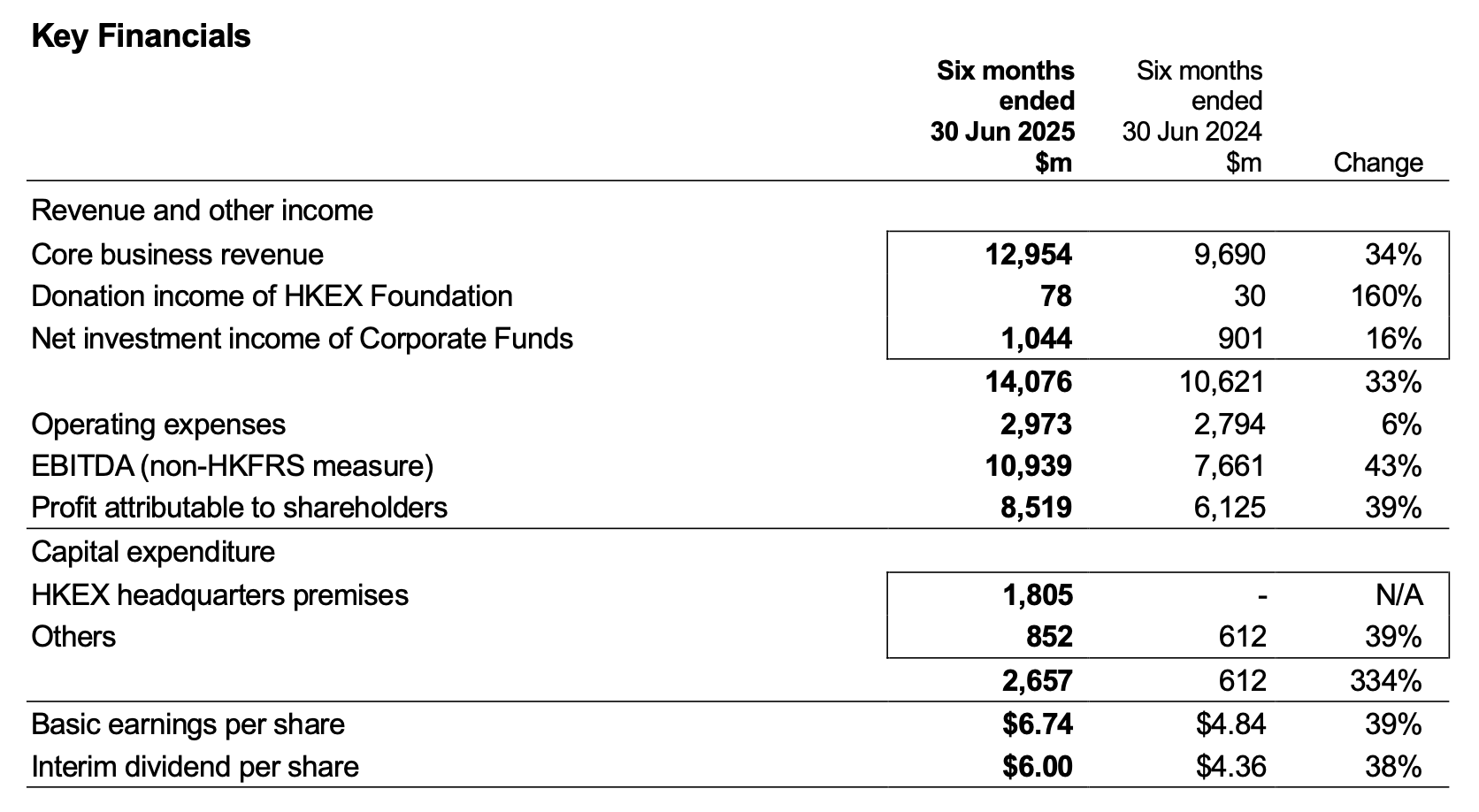

Our current 2026 EPS estimate for HKEX of HK$ 17.9 is +69% vs the consensus estimate in October last year. For SGX it is +41%.

The story is playing out. Asian markets are lifting, trading volumes are building, and we are getting massive operating leverage out of the exchanges.

Take HKEX. It’s a monster.

Revenues are +34%.

EPS is +39% yoy with 89% of it getting paid out to you as a dividend because they don’t need the money. HKEX is a software platform with a few people. The business has little marginal cost.

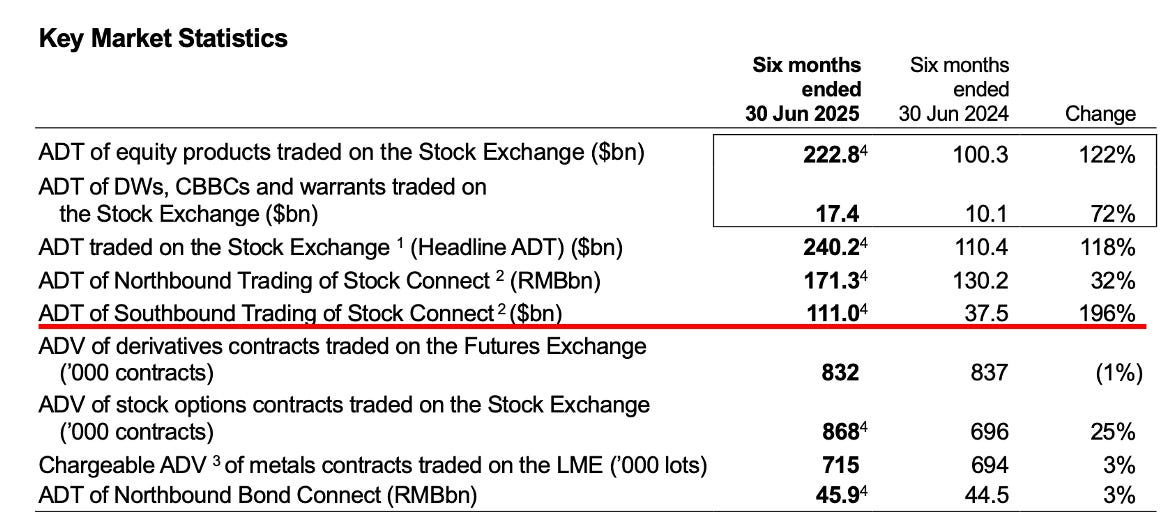

Getting into the details equity volumes are booming (+122% yoy), but strangely futures volumes are -1%, which has been a drag. LME metals futures were also sluggish at +3%. HKEX bought the LME in 2012.

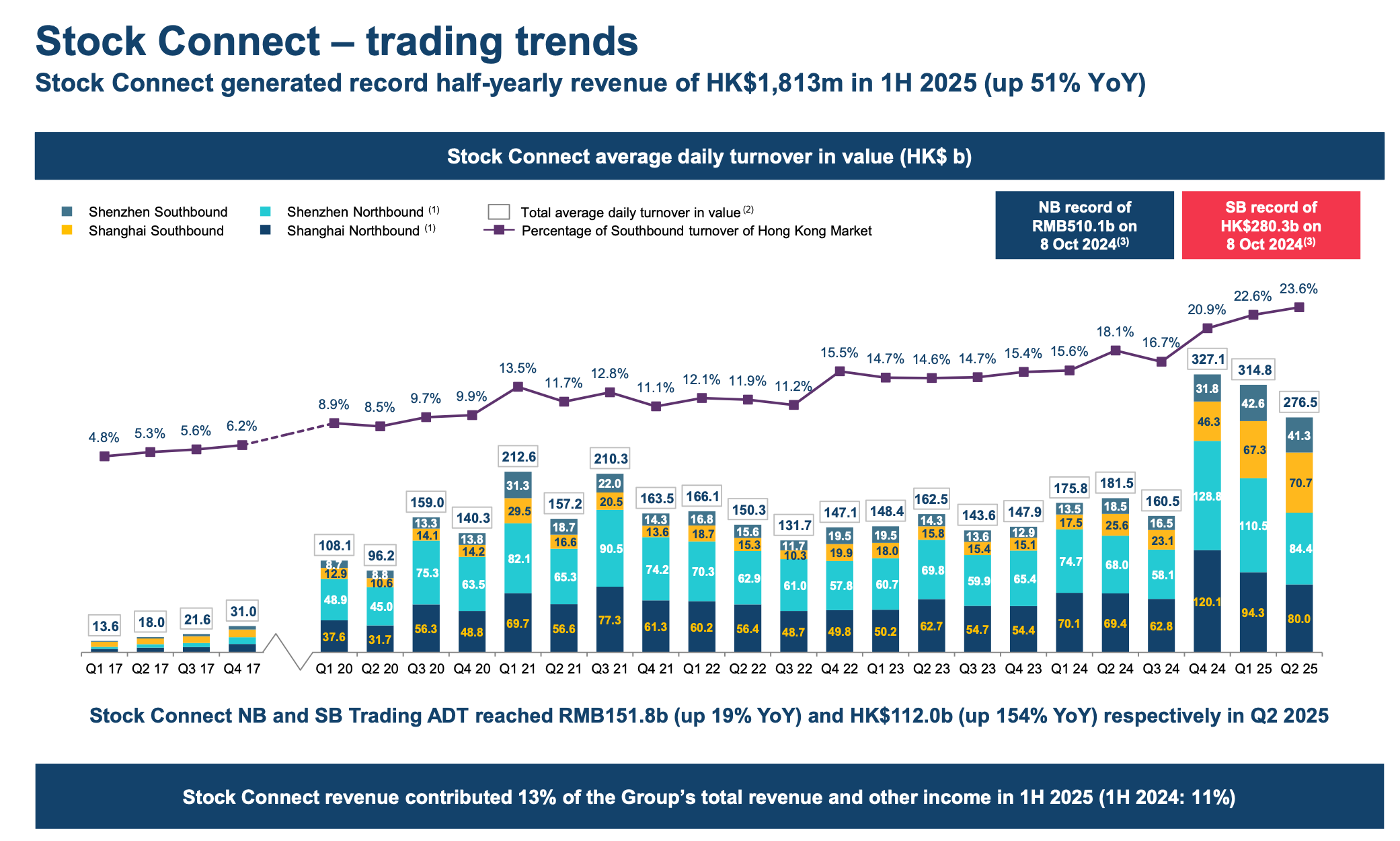

But I want to point out these StockConnect volumes.

Northboud StockConnect is a settlement system to enable traders in HK to buy shares listed in Shanghai and Shenzhen. Southbound Connect is the opposite; a way for Shanghai and Shenzhen traders to buy shares on the HKEX.

Southbound Connect is what we have our eye on. Yes, we care if US and European investors get bullish on HK listed stocks, kind of, but really the elephant in the room is the Chinese savings pile. That’s what we really want.

Southbound Connect Average Daily Traded value is +196% to HK$ 110bn in 1H 2025. And its’ becoming a big effect on the exchange with 23% of daily volume on the HKEX being trades which are routed down from mainland China. That used to be 12-13%. It’s happening. The China money pile is coming to us.

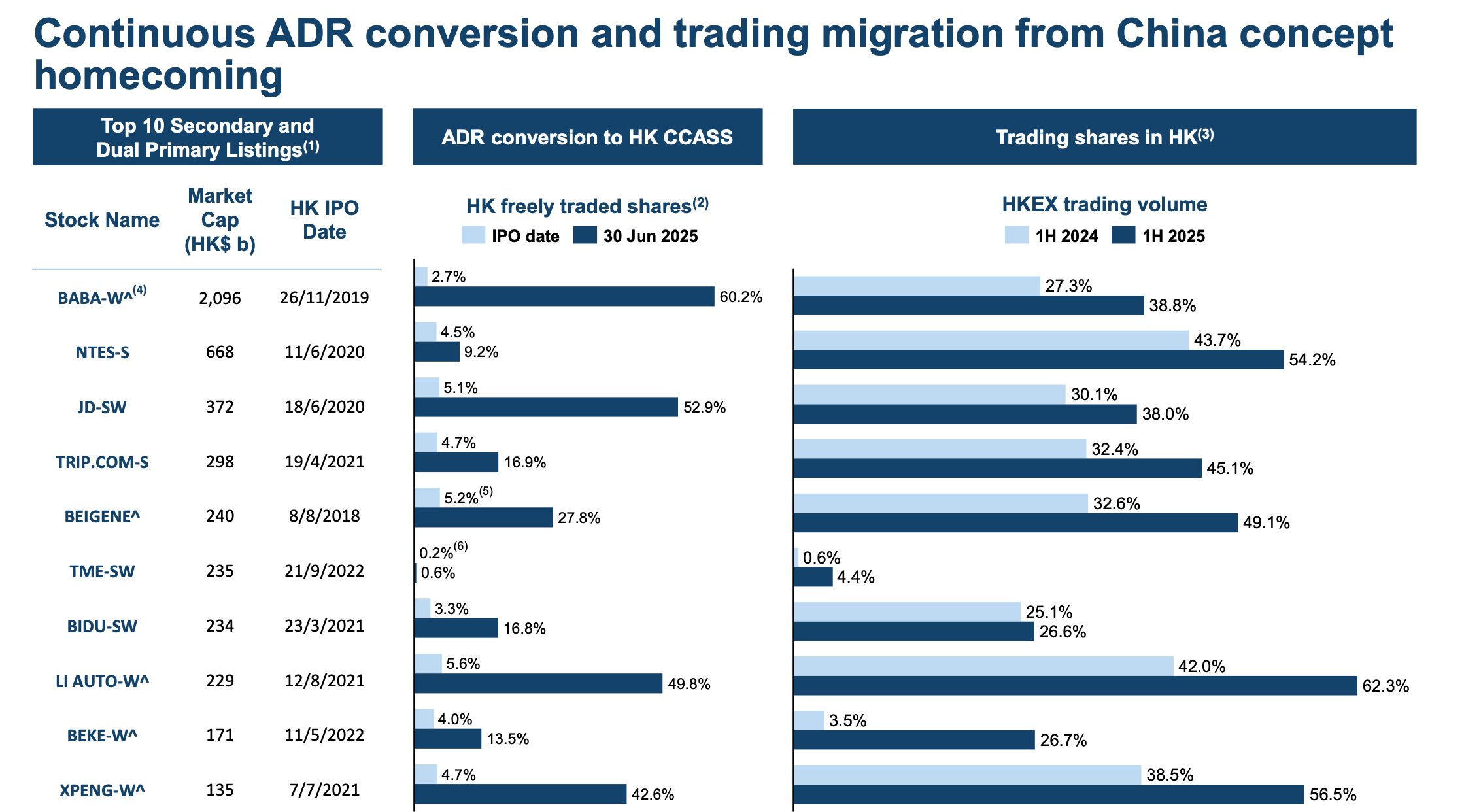

One other market structure detail. Chinese ADR volumes are shifting to HKEX too. For example, last year 27% of Alibaba volume traded in HK. This year it’s 39%. It’s the same for all the dual listed ADR’s.

So HKEX is working. On to SGX.

SGX is a different model. They don’t have the massive cash equities home market like HKEX, so they’ve built up over time a diverse business of cash equities, equity futures, and OTC FX. It’s less torque compared to HKEX, but more stable.

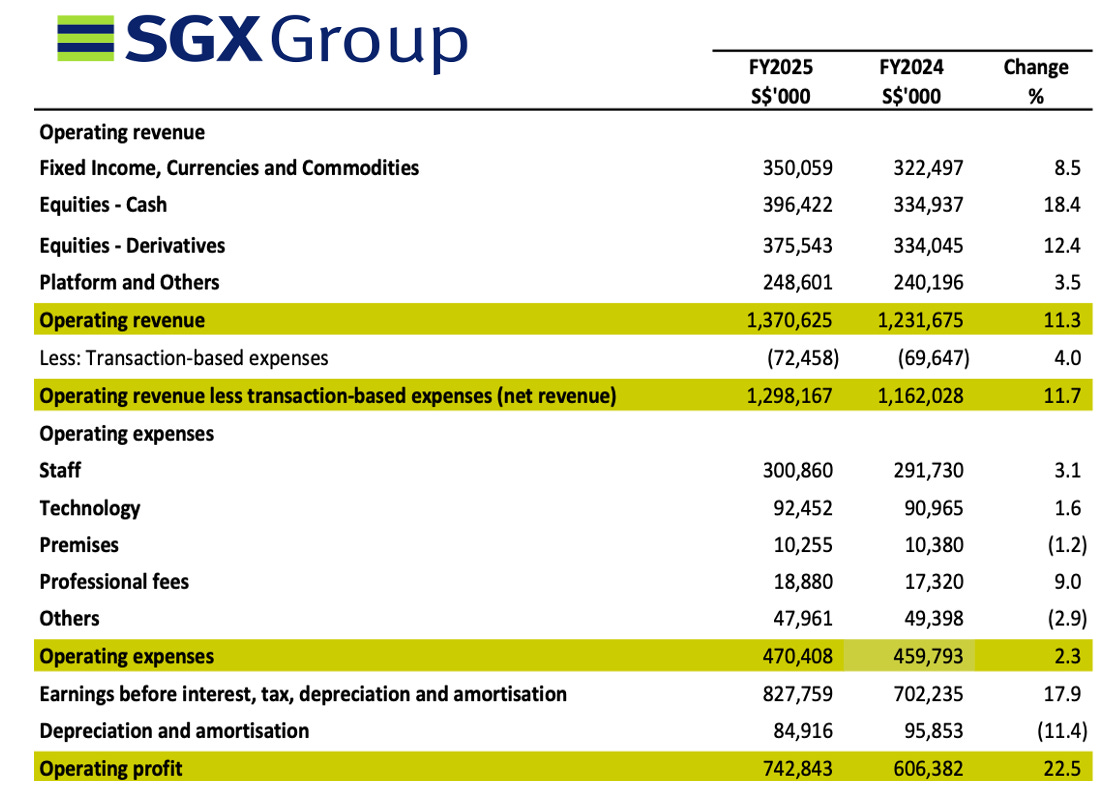

Full year 2025 (June 2025 year end) revenues were +11%, which isn’t as exciting as HKEX, but with 2.3% cost growth we get 22.5% operating profit growth. Not bad.

And that revenue growth is across all the business lines.

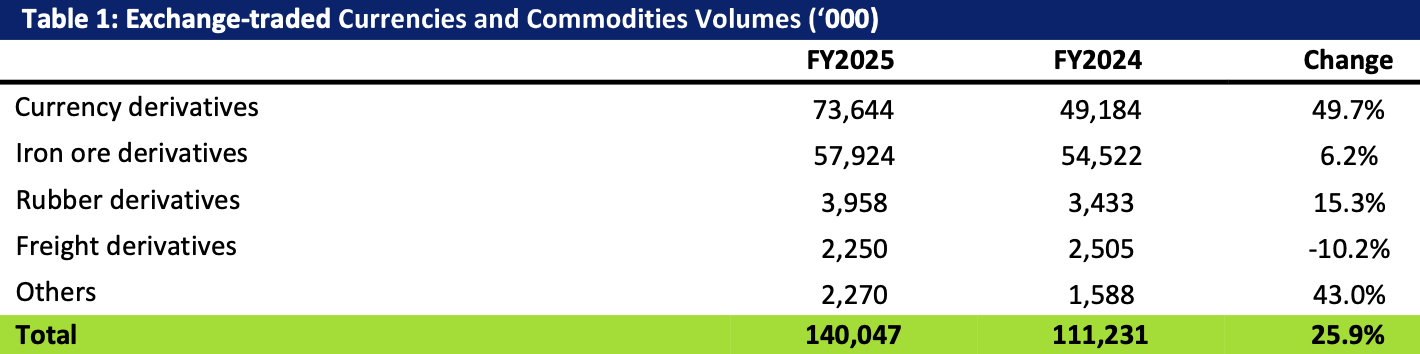

SGX is creating a hub for sophisticated risk management. Like a CME of Asia. Their FX business grew almost 50% in 2025 driven by the CNH/$ and INR/$ contracts. The two most important currencies in Asia. The iron ore business is also big and growing steadily. They’ve put a lot of work into the iron ore ecosystem.

Interestingly, SGX is working to expand is FX business outside of Asia. They announced a partnership with B3 to build volumes in BRL/$ futures.

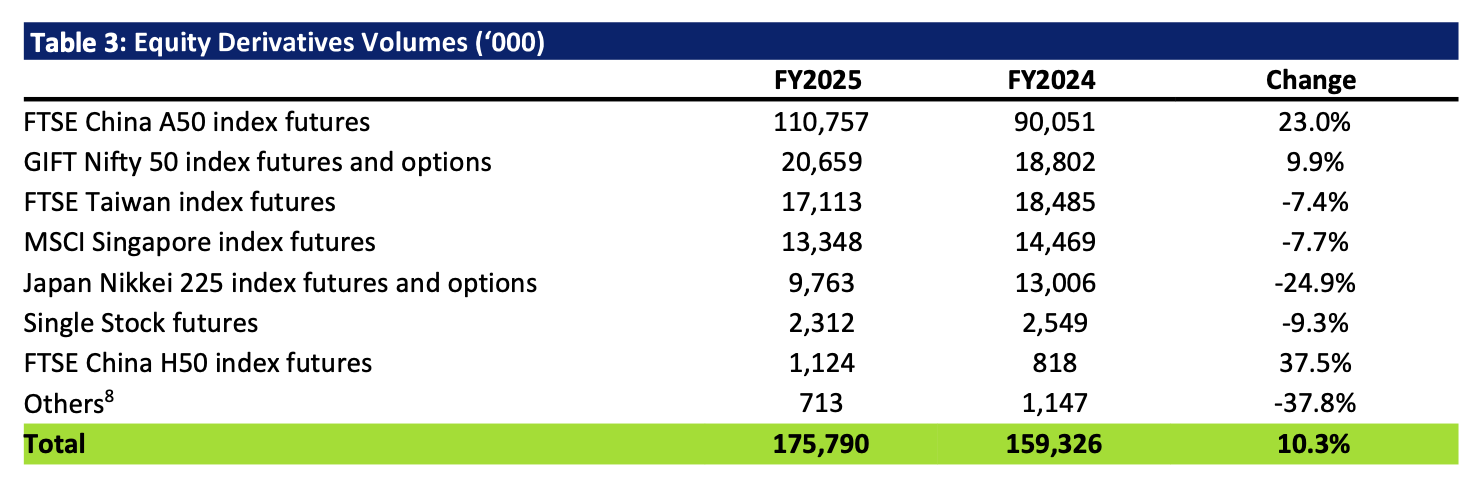

Then in the equity derivatives business the China A50 and India Nifty 50 equity futures contracts are growing strongly. On the negative side SGX continues to lose volume in their Nikkei 225 contract. I’m not sure why that it is, but it’s been a multi-year trend.

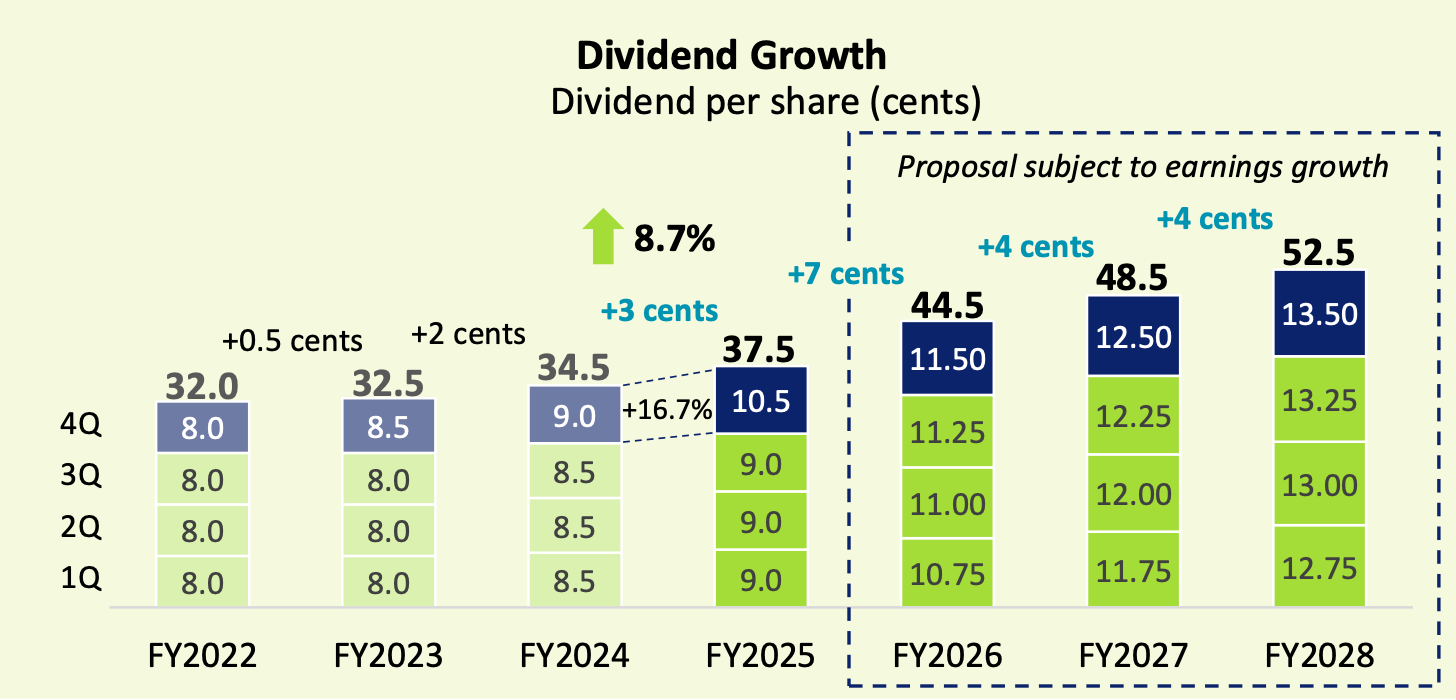

Given the strong earnings growth and positive outlook SGX announced they would grow the DPS $0.25/quarter every quarter through 2028. Yes, that’s only a 2.7% yield, but it’s growing, and we’ll take it.

At the bottom of the post are links to my updated models for HKEX and SGX.

Now on to the new idea.

Why have we done well in SGX and HKEX?

Because we bought them on the lows, when their markets were dead, when people said China was uninvestable, Singapore was asleep, and nobody anticipated the trading boom about to unfold.

We bought them when nobody could imagine what was about to happen.

So What’s another great exchange fully integrated with both cash equities and futures products with its own clearing house?

What’s an exchange sitting at one of its lowest valuations ever, at a P/E of 13x in an out of favour market, buying back 6% of its shares as we speak?

What’s a market which has tripped and fallen so many times we now laugh and make memes about it? A market which can never rally?