YWR: May QARV

I fixed the data bug in the QARV ratings.

I was able to filter out China. Now the results aren’t flooded with high ROE Chinese businesses trading at low valuations.

Now we can focus on the rest of the world.

Global Top 30 QARV Rankings (ex-China) for May 2025

In past QARV’s we highlighted several industries with an optimal mix of high 5 year average ROE’s, low debt, and positive earnings growth combined with low valuations (both absolute and relative to their own history).

In January we highlighted iron ore miners and the under appreciated infrastructure moats to the business.

In March we highlighted the much hated active asset management industry (Alliance Bernstein and TRowe Price).

In April we highlighted the attractiveness of Chinese baby vomit (Baiju industry).

But there’s one industry we’ve been avoiding. Because it’s a tricky one.

Container Shipping.

The QARV rankings (including China and without) are overrun each month with container shipping companies like Orient Overseas, COSCO, Wan Hai, Evergreen, Hapag Lloyd, Maersk, Kawasaki Kisen, Nippon Yuen, etc.

When you use the YWR QARV data app you (link at the bottom) can see these businesses have 5 year average ROE’s of 30-50%, yet trade below book value (implying they don’t cover the cost of capita) with dividend yields (last 12 months) of 6-13%.

Why are these stocks so cheap?

Because everyone knows shipping earnings aren’t ‘sustainable’. It’s always boom or bust.

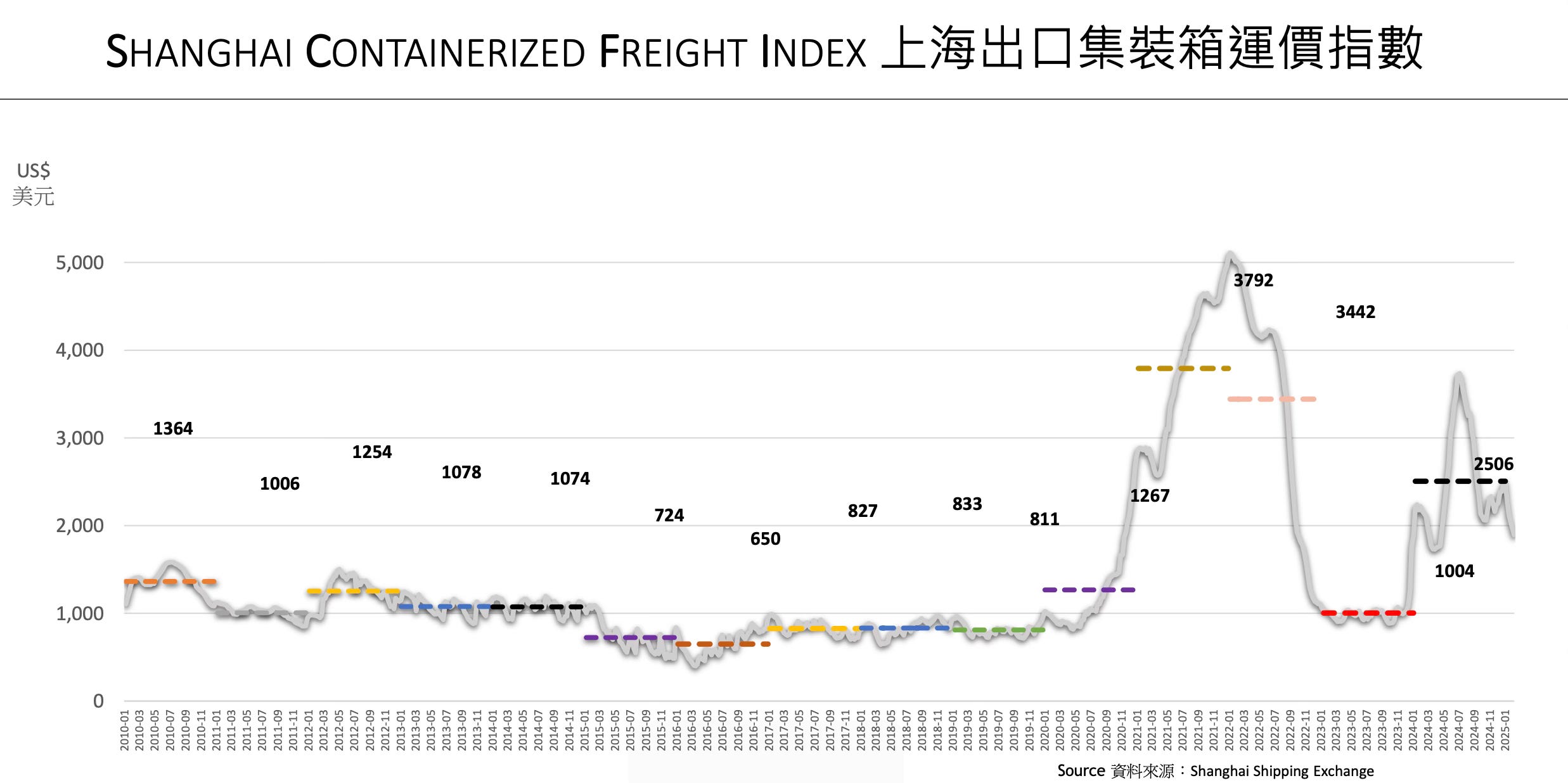

The shipping companies made a fortune from the COVID dispruption when the cost of shipping a 20 ft container from Shanghai rose from $811 to $3,792 in 2021. Then unexpectedly the shippers made money again in 2024 when the Houthis disrupted the Suez Canal. It forced ships to go around the Cape of Good hope, stretching out the supply lines and affectively taking capacity out of the system.

But eventually things will return to ‘normal’ and the industry will go back to making losses again.

Right?

Or… Has something changed? Is there a reason shipping rates keep spiking?

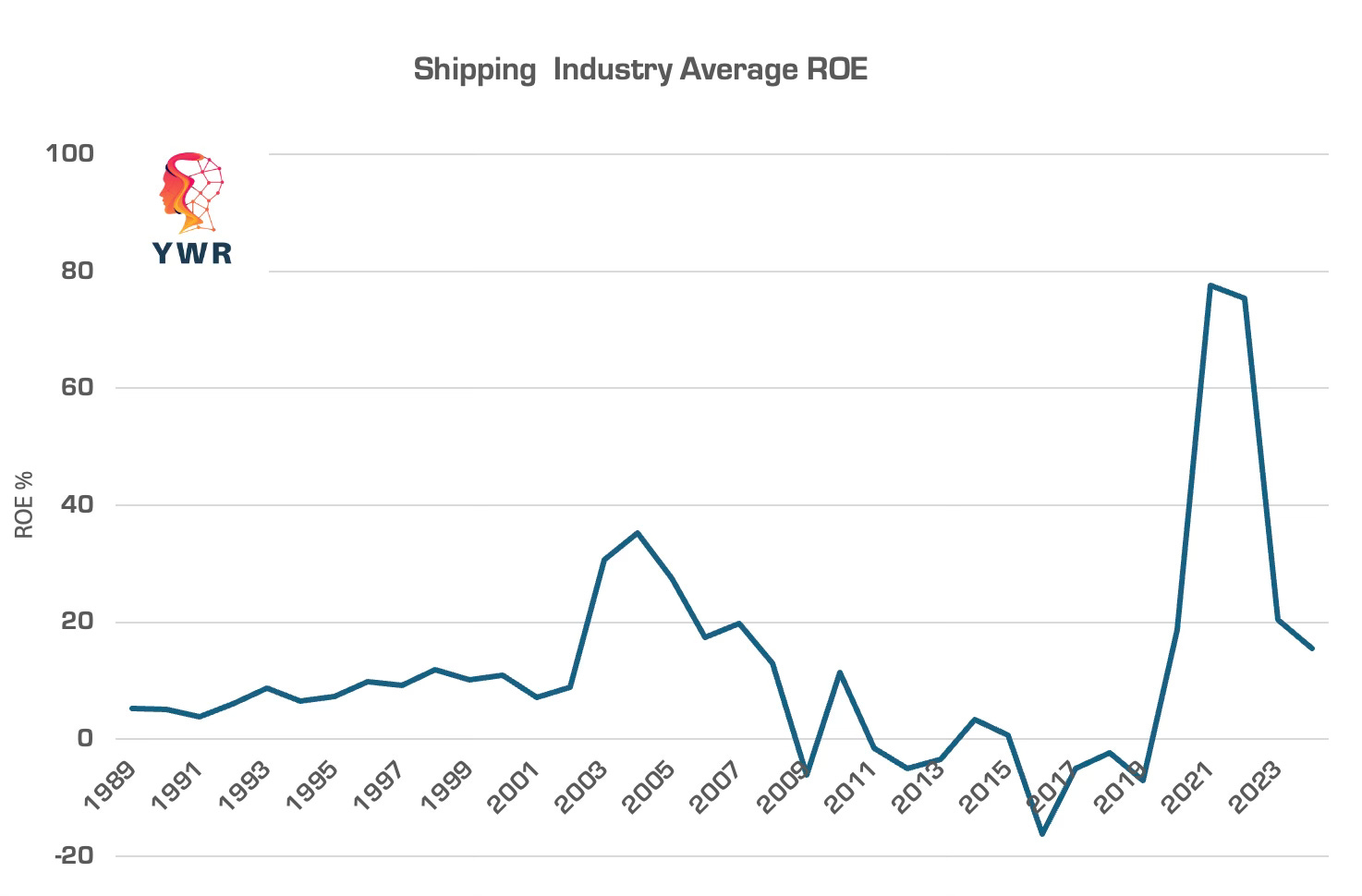

Below is a 30 year chart of the average ROE for 10 shipping companies (Japanese, Chinese + European).

Given the history you can understand why investors are skeptical. Over a 30 year period the industry spends most of its time barely making money, or losing it, with brief surges in profitability which keep everyone in the game.

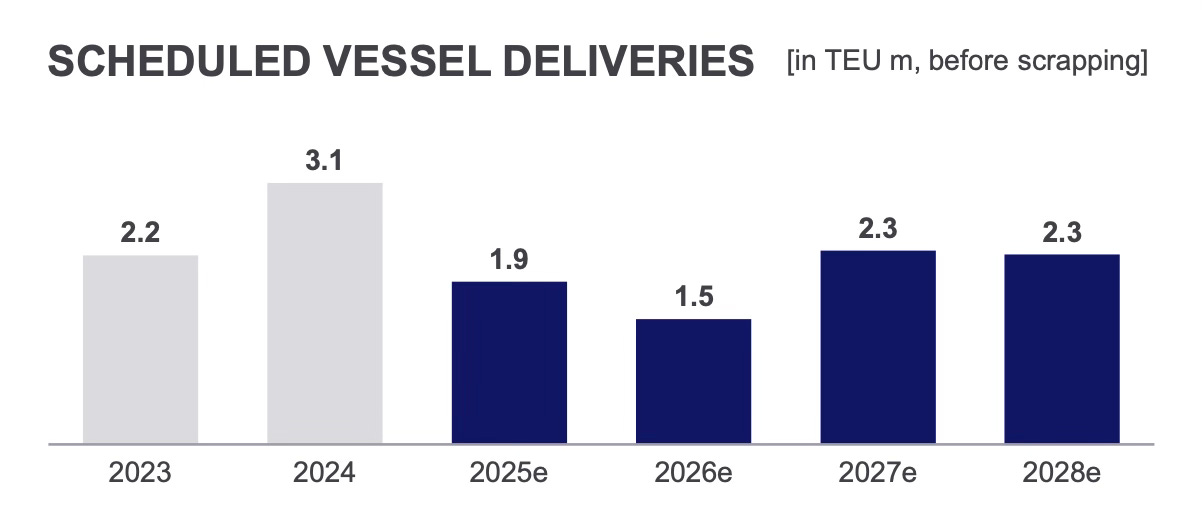

Then whenever there are supernormal profits, everyone orders new ships. Like now. The order book for new ships to be delivered is a whopping 29% of the current global fleet.

The bear case is that as these ships are delivered in 2026, 2027 and 2028 freight rates will drop, and the shippers will go back to making losses.

But, how can we think differently about this industry? I mean that’s what we do at YWR. Right?

I’ll propose three contrarian reasons why the future ROE’s for shipping can surprise and be higher than in the past. To be clear, this is an intellectual exercise. I don’t own the shipping companies.

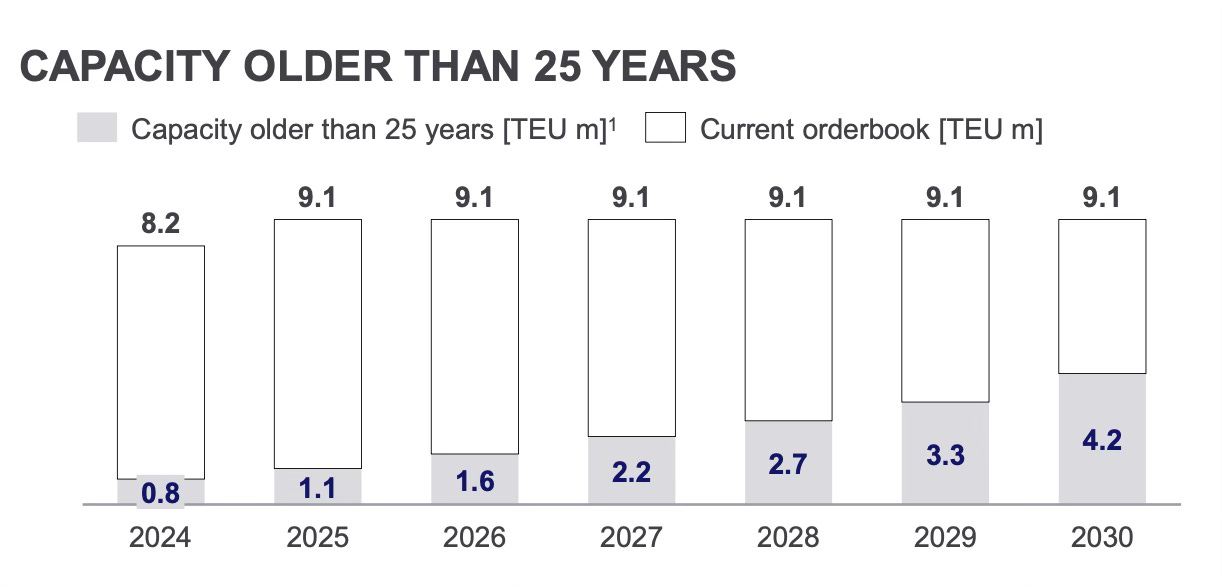

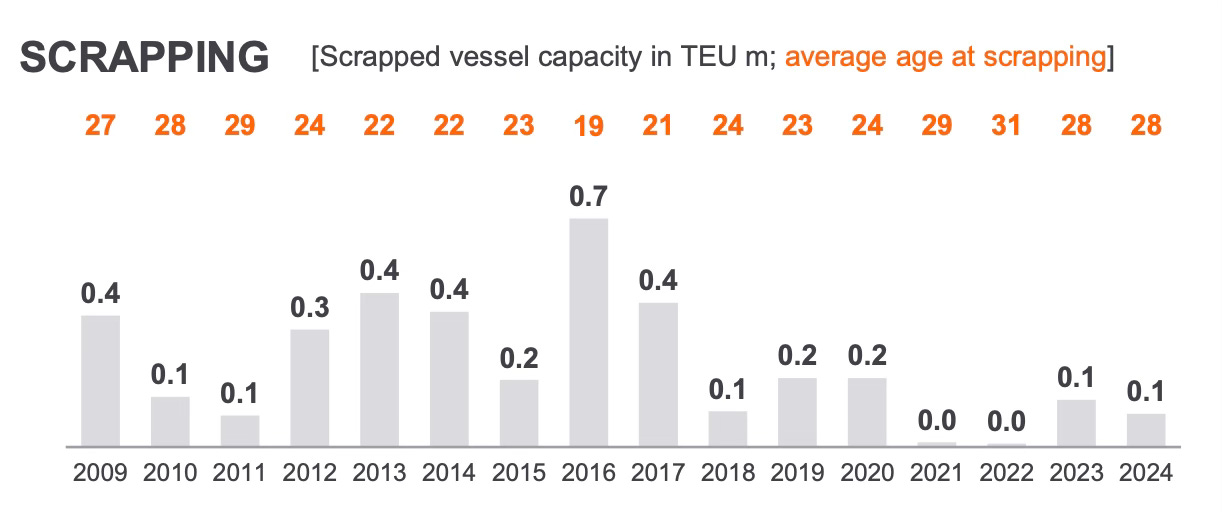

Contrarian Reason #1. Scrapping rates will surprise to the upside.

You go 10 years (2010-2020) without making money and suddenly have a bonanza of profits? Of course you are going to use some of that money to buy new ships. Especially, when a lot of your ships are old and there are ever increasing regulations around ship engine emissions.

But the surprise will be the scrapping rates. When the new ships are delivered shipping companies will not still run the old ships alongside the new ones and driving profits to zero again. Instead, there will be a surge in scrapping of old ships. 2 million tons/year will be delivered, but scraping rates could hit 1 million tons/year and continue through 2030.

Everyone can see the order book, and those ships will be delivered, but we are underestimating the scrapping. Think about it. When you get a good bonus and buy 2 new cars, you don’t also keep the old ones.

So yes, there is a lot of new capacity coming, but it will be moderated by high scrapping rates.

Contrarian Reason #2: China +1 or N(N-3)/2.

The China + 1 trend looks positive for shipping mathematically. The routes between China and the rest of the developed markets are well established and competitive. But the trend of manufacturing in multiple jurisdictions (China + 1) adds exponential complexity to the logistical system.

Like with the Houthis and the Suez Canal, China +1 stretches out the shipping capacity. It creates more interconnecting routes, which requires more ships. Yes, there are a lot of ships on order, but you might actually need them.

Contrarian Reason #3. Shipping companies don’t want to lose money.

Shipping CEO’s fear what you fear. That’s why they bought ships, but also used their windfall profits to pay down debt, buy back shares and pay dividends. They are trying to be prudent with their capital. Yes, they had to buy some new ships because of ESG, but they know it’s a competitive industry and are careful about adding new capacity.

They are also making gradual changes to the business model such as owning the terminals, not just the ships. Maersk, COSCO and Hapag Lloyd are big owners of terminals. China + 1 also gives them a chance to build new terminals in new markets. Shipping companies are also creating more integrated logistics offerings. They know shipping a box to LA is commoditised. They need to offer more value added services, and they are steadily working on it.

Bonus Contrarian Reason: Is disruption the new normal? And do shippers benefit?

Go over all these supposedly random shocks.

In 2020 global governments decide to shut down the economy because of COVID. Everyone must stay home and receive stimulus checks => Shippers boom.

Then 2024 and the Hamas-Israel War. Houthis attack ships in the Red Sea => Shippers boom.

Then in 2025 the Stop-Start of Tariff War creates windows of detente where inventory orders and shipping rates surge => Shippers boom?

Is the paradox that global conflict, Tariff war start-stops, ESG rules, China + 1 and added complexity, are all positive for the container shipping industry? It requires more ships, more terminals, and the chance to add more value added logistical services?

Chaos => Higher ROE’s for Shipping Companies?

I leave it for you to decide.

Below are the links to:

The full QARV Rankings Data

QARV Data App on Retool

Hapag Lloyd Investor Day Presentation

COSCO 2024 Results Presentation

Maersk 2024 Results Presentation