YWR MegaFund Positioning Review 2024

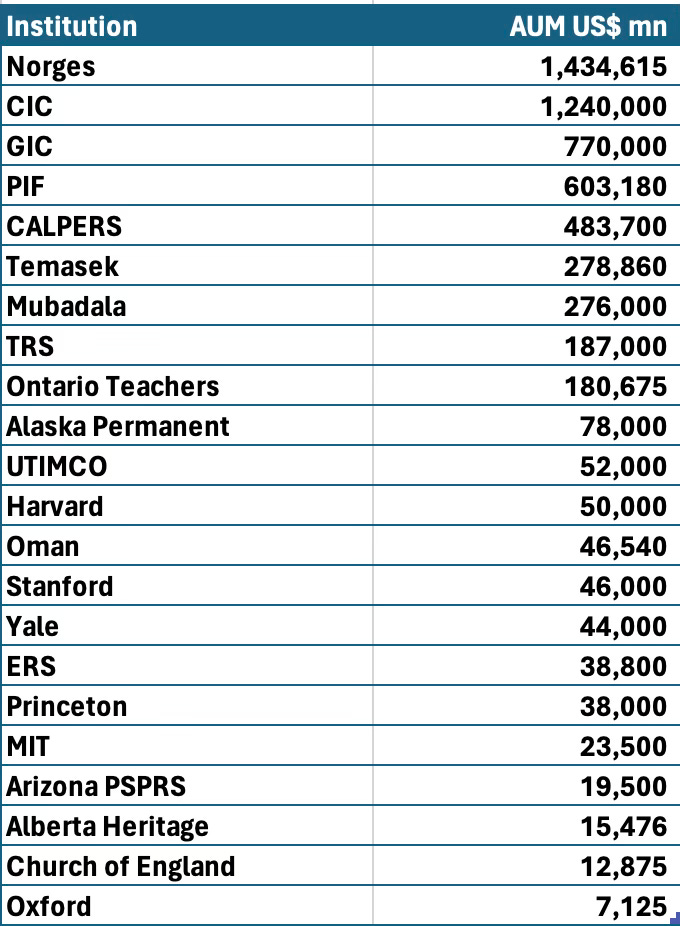

It was a lot of work, but we’ve updated The Global MegaFund Positioning Review for 2024 with the latest data. We reviewed 23 MegaFunds controlling $6 trillion in assets.

At the bottom of the post there is a link to the a YWR MegaFund 2024 Slide Deck.

It’s 200 slides on data, charts and commentary I found interesting. Get your coffees and take a flip through what the biggest funds in the world are doing.

Later we will work on how to make money on this, but today let’s just absorb some of the insights and go through the deck.

MegaFund Summary Insights 2024

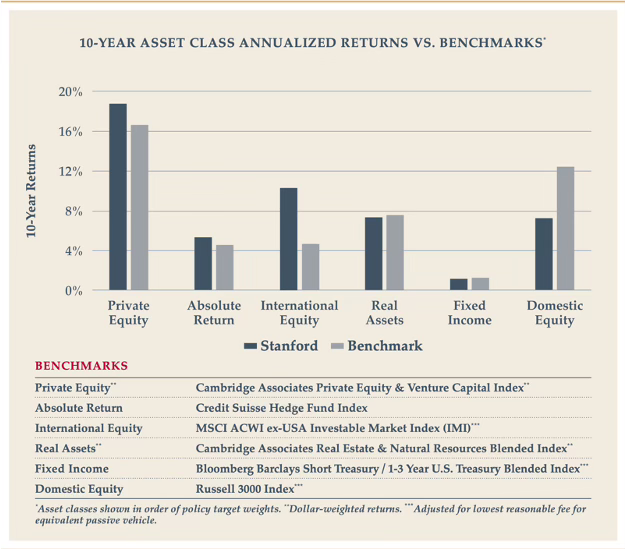

Private Equity returns are addictive. 16%/yr for 10 years with low volatility.

Allocations to Private Equity have grown over time (15% to 30%).

Endowments have 35% PE+VC exposure. Pension funds closer to 15-20% range. PE sales people should focus on pension funds.

Is 50% the new 30% when it comes to private investments? Private Equity + VC + Private Credit + Infrastructure.

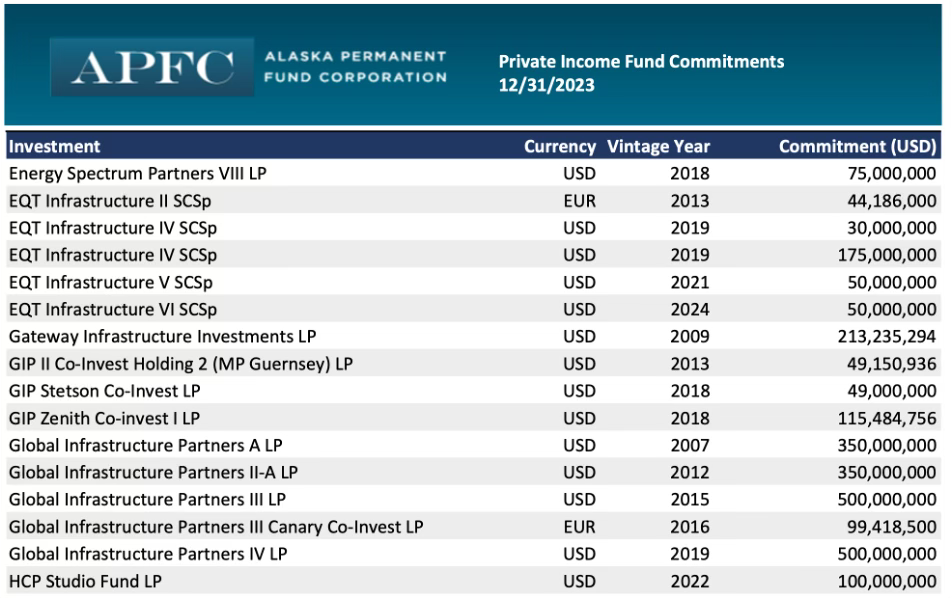

Infrastructure is getting a lot of focus.

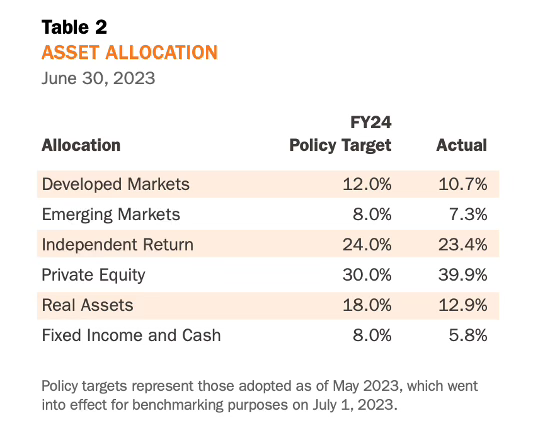

Funds are currently over their target allocation in Private Equity and trying to manage the exposure down gradually through lower annual new fund commitments. This is offset by sizeable prior commitments.

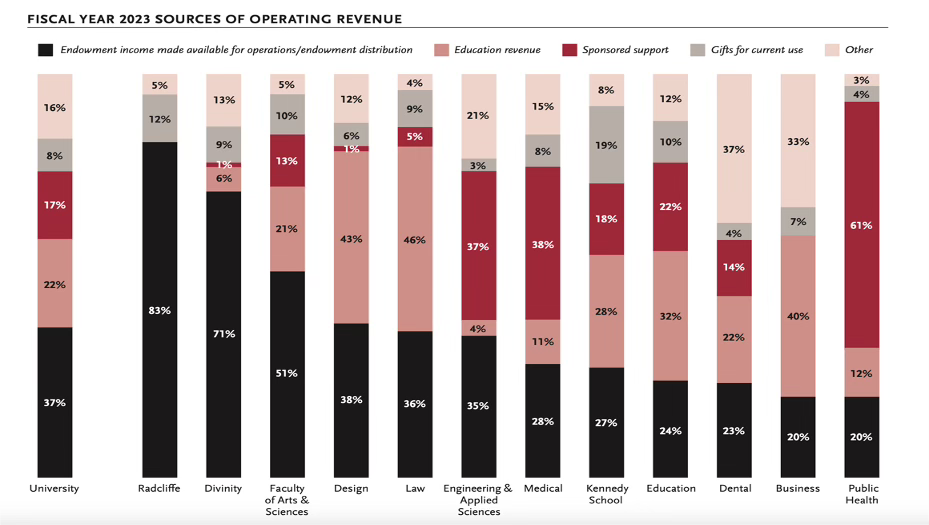

Endowments are supporting 20-37% of University operating budgets.

Endowments still paying out 4-5% of the fund each year to universities despite excellent investment returns. Given great performance this number should be falling, but university expenses are growing in line with endowment AUM. Potential train smash to be discussed later.

Level of reporting at endowments is declining slightly. Trend towards University endowments reporting on investments within in university financial report rather than standalone reporting. Less detail. Public pension funds have best disclosure.

Private Equity Funds provide 3 important advantages 1. Smoothes investment returns, 2. Hard for public to know exactly what the fund owns 3. Provides political correctness blast shield if any underlying investment does something politically incorrect (‘In our DDQ’s we were clear about our views on XYZ… we would never support such activity… PE firm did a bad job…. we will redeem immediately…’.

No interest or discussion of high yield credit despite 8% yields. Nobody is interested in fixed income except GIC.

Every fund’s strategic priorities: Sustain the energy transition, Diversity Equity and Inclusion, Performance and Liquidity, in that order.

Every Annual Report needs a Wind Farm. I hope they are good investments because every fund has them.

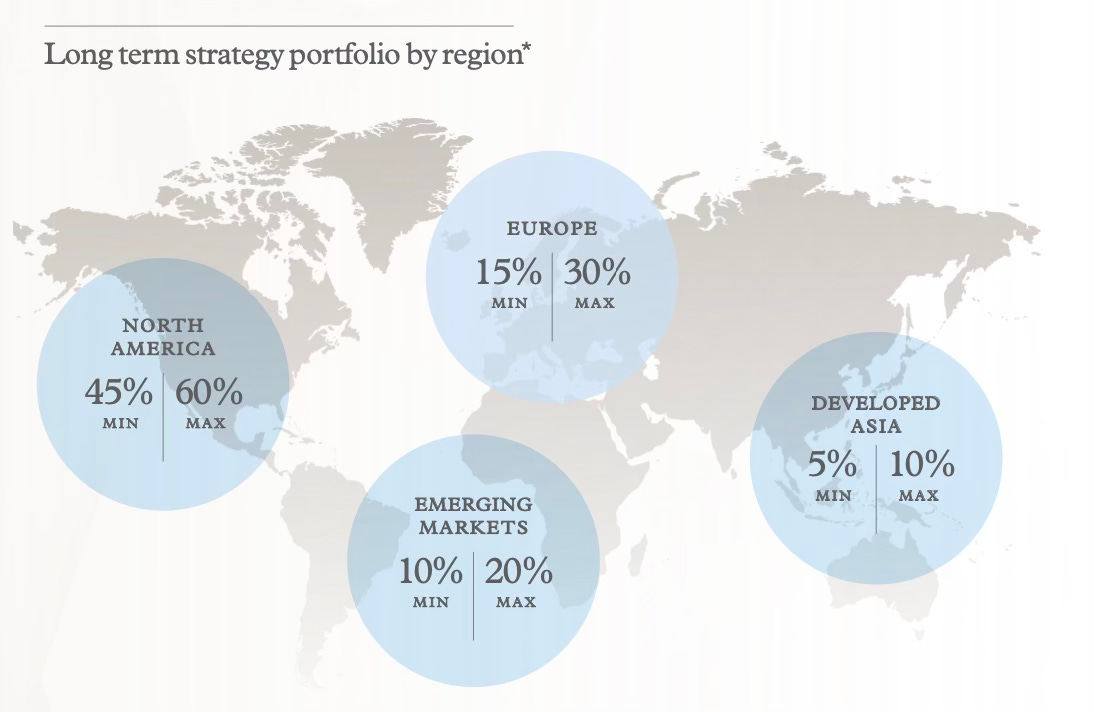

Every fund seems to agree 50% of AUM should be invested in US. 5-10% in Asia.

China is less than 5% for every fund, except Temasek (22%).

SWF’s are now national development firms to diversify the economy. Everyone following the Dubai model, which was the Singapore model. Create transport hubs (big airport, national airline, container port), grow tourism (real estate), become a financial hub, invest in tech starts ups, eventually try to get into aerospace.

$LCID will not run out of money.

Everyone has identified the same MegaTrends: Energy Transition (Wind Farms, Solar, Batteries, Electric Vehicles, Digitisation (DataCenters, Tech), Urbanisation (Tollroads, Ports, Airports, Real Estate), Aging Society (Biotech startups).

‘MegaTrends’ should be sufficiently vague to incorporate any investment.

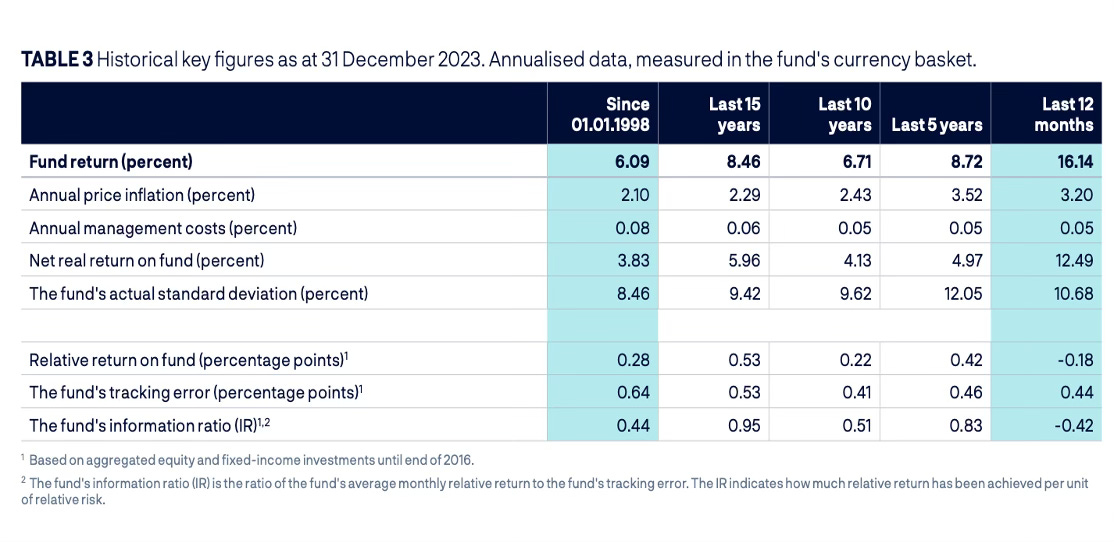

Private Equity firms and consultants pray nobody is paying attention to Norges model. 8.5% return annually in public equities with management fees of 5bps.

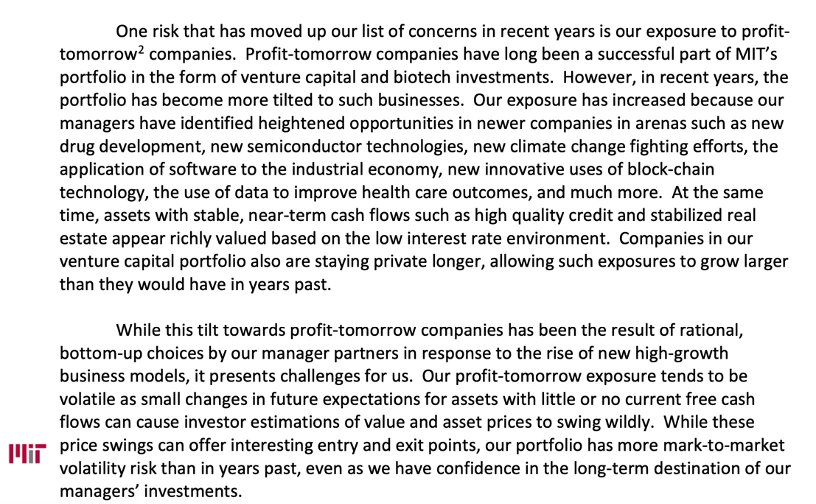

Most insightful thing I saw: ‘Our Portfolio is overweight Profit-Tomorrow companies’. MIT 2022 Investment Letter.

Portfolios have low levels of dividend income. Everyone focused on private equity funds, tech and energy transition.