YWR: 'Multi-Year Bull Market'

We could be in for a multi-year bull market where investor participation gets positively bubbly. A repeat of 1995-2000 and it is 1995.

You’ll be glad to know that was the message from the macro conference I attended today in London.

Here are my notes:

Inflation

Disinflation will be a key story.

Core PCE will be sub 2% by end of 2024.

Interest rates will revert to pre-pandemic levels

New rents which make up 30% of CPI are flat to negative.

Goods inflation is 0% and might go negative.

Wage inflation does not equal overall inflation because companies are getting > 2% efficiency gains. Companies don’t need to pass on the wage inflation if they can make it up in efficiency.

The recent quarterly inflation reading is running at 1.5% annualized. We are already below 2%.

Recession

Everyone expects a recession (52% according to BofA Fund Manager survey), but there won’t be one.

In this cycle the Fed raised rates in response to supply side inflation (COVID, Ukraine War), not demand driven inflation (which is usually what causes an interest rate cycle).

Demand is still healthy.

Demand is picking up from low levels and will accelerate as the Fed cuts interest rates.

Biggest driver of recession call by bears is the inverted yield curve.

But yield curve is not really signalling a recession. Just bond market signalling its view that current inflation and high Federal Funds rate are transitory.

We already had a ‘near recession in 2022’, with 2 quarters of negative ‘real GDP growth’. The recession is already over.

Stock Market

Stock market is not that expensive. It is fair value based on Fed model. Fed model finally works again with interest rates no longer 0% (used to give really high predicted S&P 500 values when discounting EPS by 0%).

Fed will be cutting rates in response to falling inflation while demand is accelerating.

This is going to be a great combination.

Things could get bubbly.

EM and Rest of the World could do OK, but US market likely to continue to lead the world. It has all the best tech stocks.

Not bearish on the dollar.

Leadership might remain narrow. 2000 tech boom had the Four Horseman (Microsoft, Cisco, Intel and Dell).

Eventually, participation in the rally should broaden out as happened in later in 2000 rally.

But we are still early. Maybe 1995.

China

Presentation by George Magnus from Oxford

Terrible, boring. Nothing you can’t read in the FT.

China’s population is getting older.

China is trying to stimulate the economy without repeating the excesses of 2009 and 2016.

Unlikely China invades Taiwan. Just doesn’t seem to make sense. Get ostracised from rest of the world, trade implodes, economy implodes, potential regime change and risky to blockade Taiwan with US 7th Fleet in the vicinity.

So talk about Taiwan continues but nothing happens.

Forecasts are for 4.6% GDP growth but provinces are targeting 5.2%. Might get a short-term pop out of China but longer term growth still uncertain.

Real estate is 7% of GDP and will likely decline to 3-4% in the future. (But no concept of how this could happen through both growing, with GDP faster).

China is dominating in EV and batteries.

But this focus on EV’s is typical of the problem. Too much top-down policy direction. Needs to be more free market choice.

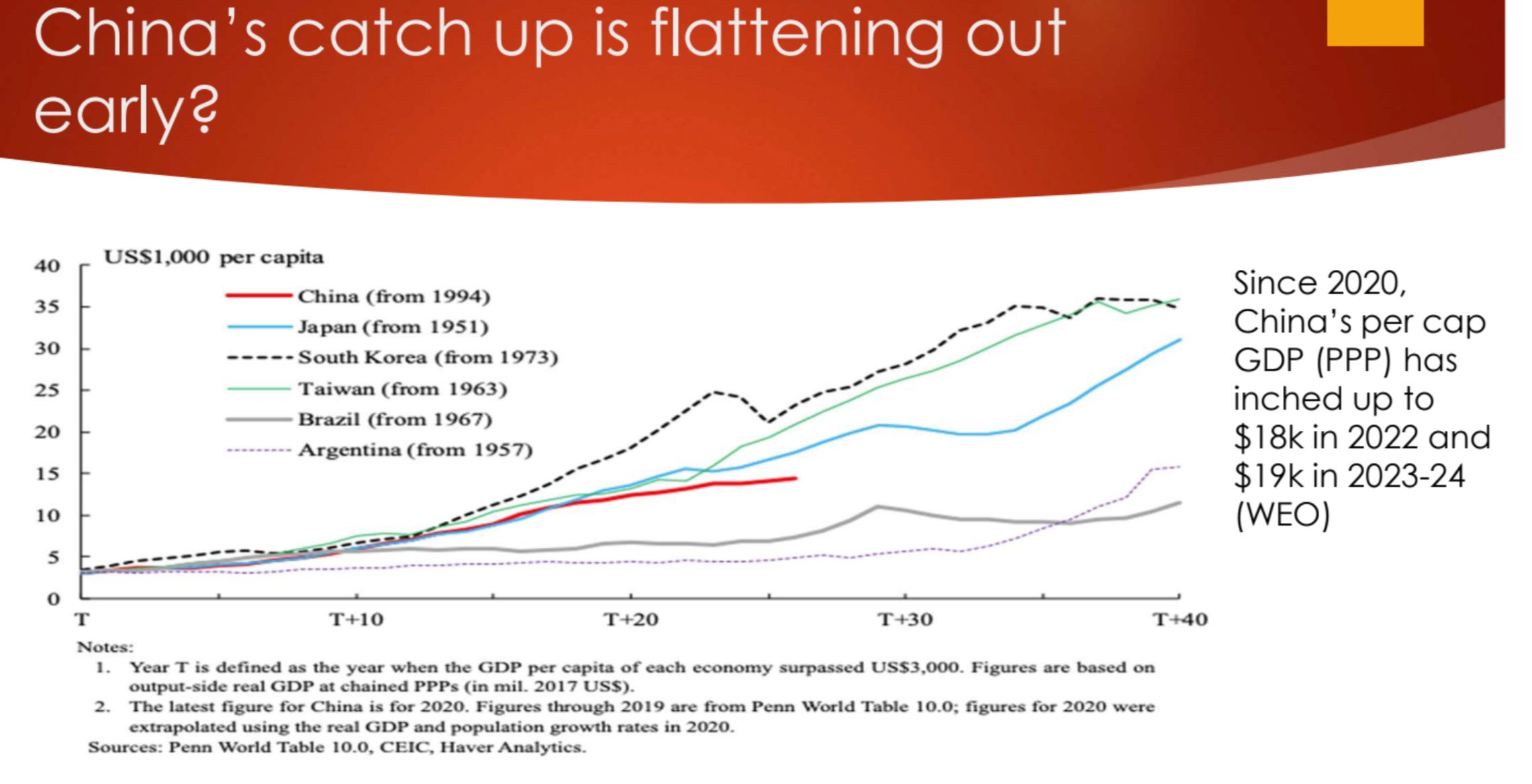

Concern that China’s has hit the middle income trap ($15k of GDP per capita), same as Latam.

Geopolitics

Wars

60% chance Isreal-Palestine conflict remains in the Gaza Strip and is market neutral.

Crude oil doesn’t react unless the conflict involves the Persian Gulf.

US economy is a lot less responsive to crude oil prices. US production means it is hedged against crude oil problems.

75% of Ukraine War outcomes are market neural (Stalemate or Peace).

Wars tend to cluster in time. One thing can lead to the other. Mimetic Effects.

Wars tend to be inflationary.

Current geopolitics are supportive of gold.

China-US

China-US will remain an economic war. Not a real war.

US PE/VC investment into China has crashed. Close to 0.

China-US trade is being rerouted. Mexico, Thailand, India and Vietnam all benefitting (exports to US surging).

China is fighting back through battery and EV dominance. Non-China Clean Energy plays are suffering from this competition.

Western semiconductor industry benefitting from government support and protection. Go long Semis/short Clean Energy.

US Election

Polling between Biden and Trump is very tight. Hard to call. Democrats might have a slight edge because of better voter turnout initiatives.

Markets usually don’t care too much about post-election unrest, but this time might be different. VIX is at all time lows.

Financials, Defence and Energy could benefit from a Trump win.

Renewables, Consumer Discretionary and Healthcare could benefit from a Biden win.

Link to the full 59 page slide deck below.