YWR: Part 1. The Trump 'BOOM!'

Amazing election. So many twists and turns. It’ll make a great movie one day.

But what does it mean for markets and asset allocation?

How do we make money?

In Part 1 this week we will cover assets which benefit from Trump.

In Part 2 next week we will cover a whole industry of assets you want to stay away from for years.

PART 1. THE TRUMP ‘BOOM’

Trump’s victory reinforces many themes we already knew. We wrote about these themes back in January in our Barry Sanders tribute (Fake Left, Go Right).

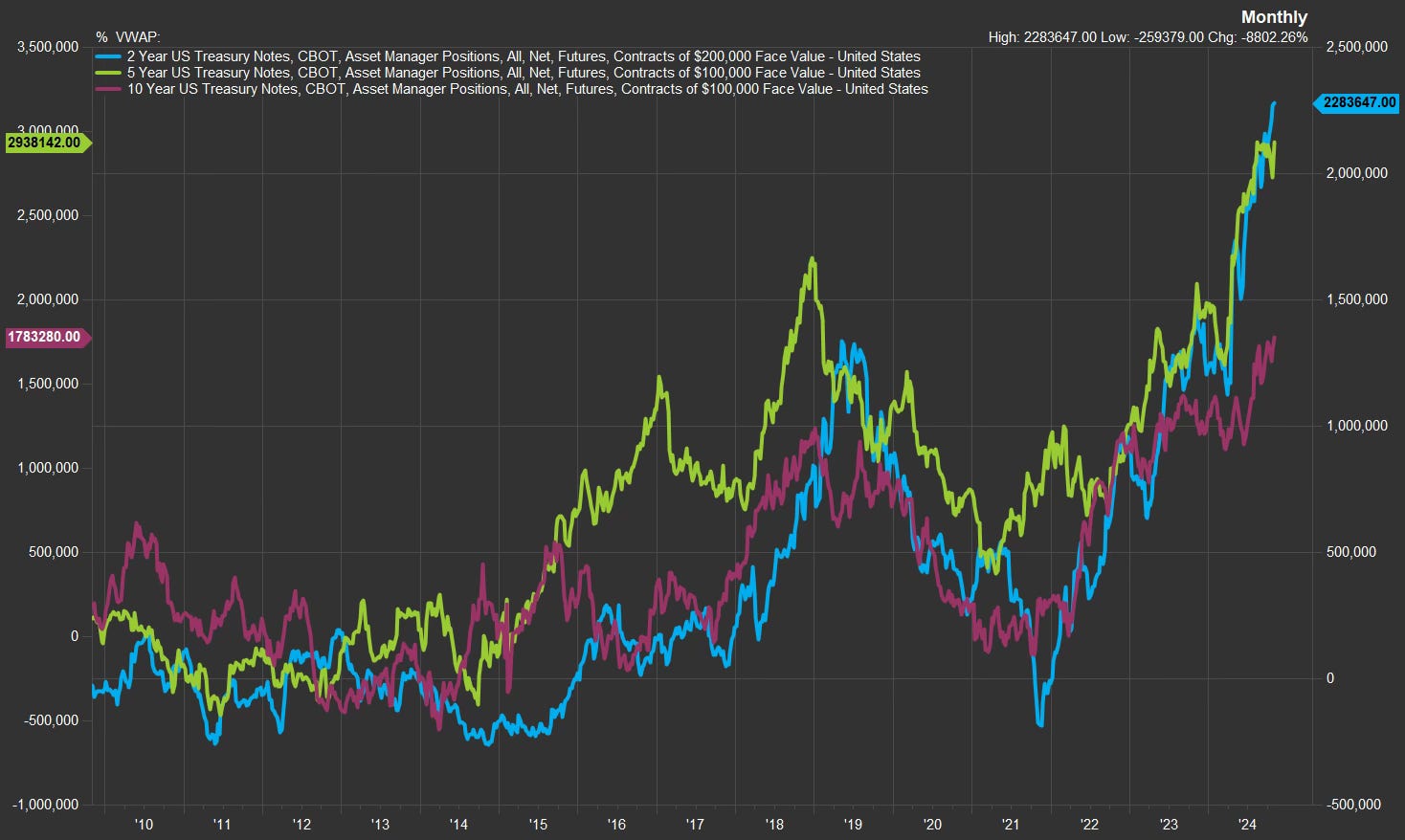

This was the key chart from that post.

This chart told us that when it comes to interest rates the opposite was going to happen.

Sometime in 2024 the inflation problem would reemerge and interest rates would do the opposite of the consensus and go higher.

That was January.

Today, when we look at net asset manager positioning in interest rate futures what do we see?

Asset Managers have never been more net long. Record Long Positions. Especially, 2’s and 5’s.

They are all getting sucked into the idea that inflation will drop to 2% and the Fed will cut rates through 2025.

But at YWR we have the view the Fed has jumped the gun. Inflation will be akin to the terminator in Terminator 2. You think it’s dead, but it forms back together.

The Fed’s cutting cycle is a mistake. And like most government institutions the Fed will try to save face and ignore the mistake. But already this week the Fed’s language is becoming more hawkish. The outlook is now “balanced”.

The whole asset management industry doesn’t get record long interest rates at the top (in yields).

How does inflation emerge again?

Back in January we imagined the two drivers were likely to be a cyclical recovery in the economy combined with higher commodity prices. Sprinkled on top and part of the commodity cycle would be Chinese economic stimulus.

How does a Trump presidency affect that view?

Trump is gas on the fire.

Tariffs “my new favorite word” will be inflationary. It’s great to move manufacturing back to the US, but it takes a 10-15 year strategic plan focused on targeted industries, supply chains and logistics. You have to be Chinese about it. Just tariffs, without working on the backend, means higher prices get tacked on to everything and you get inflation. In Africa they try this all the time (‘import substitution’). It generates 20% inflation in return for 1 new factory. Do you remember the $10bn Foxconn factory in Wisconsin announced the last time around? It’s down to $672mn.

Dollar weakness. I don’t see why everyone is buying the dollar for a Trump trade. With time we will see Trump will want the opposite, a weak dollar. The manufacturing growth strategy will be tariffs, plus a weak dollar, plus pressure on the Fed to be dovish (which will create a very steep yield curve).

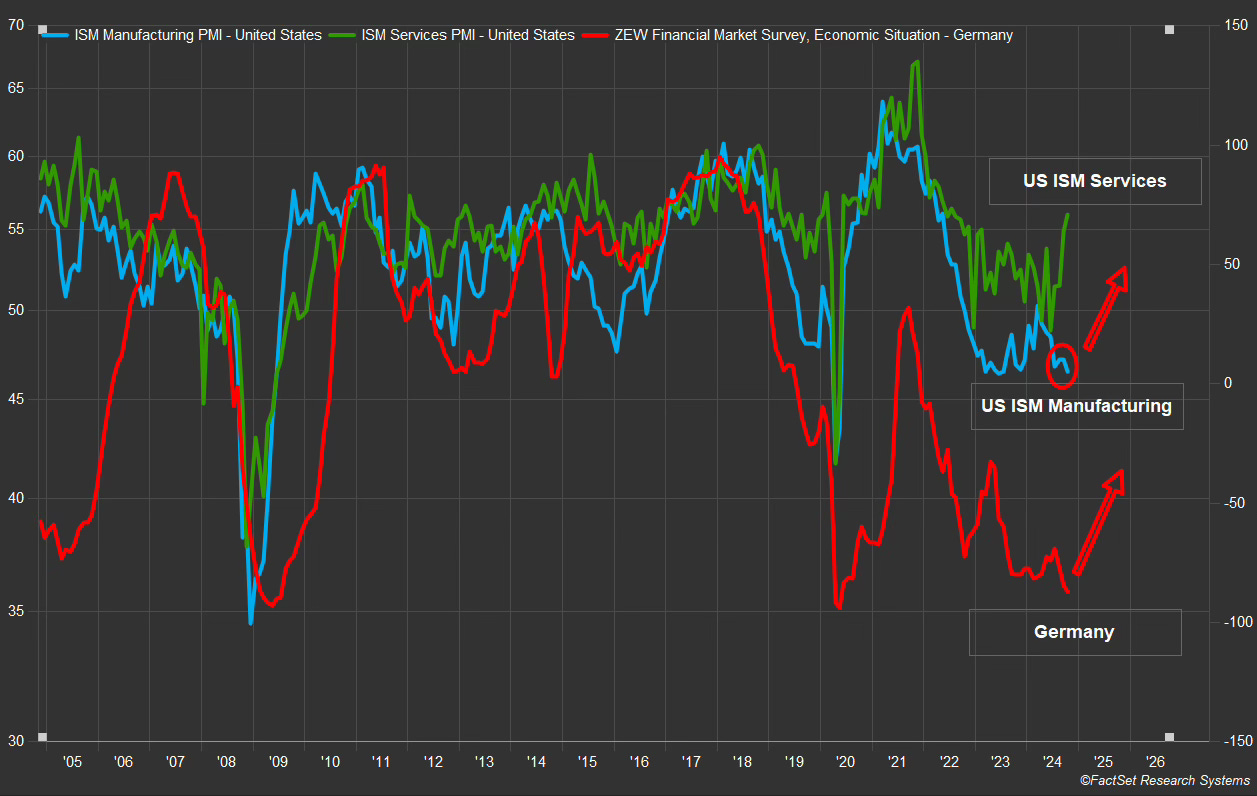

US and European manufacturing are sitting at recessionary levels, especially in Germany. At these depressed levels (45 on the ISM) it doesn’t take much to get a rebound back to more normalised levels. We already have the Fed cutting rates, but now we have election uncertainty out of the way and Trump whipping up business owner animal spirits.

China will have to stimulate more. It will be an uphill slog in January as they say for China to grow exports with the US and Europe putting up tariffs. Yes, keep moving up the value chain and making amazing products and exports will grow (maybe), but it can’t be the growth driver it was before. They might even decline. The writing is on the wall. It’s time for a new strategy. It’s what we said in #1 Trade, grow your domestic economy. Be the new US.