YWR: PE/VC Deal Tracker Q4 2024

Let’s review the top PE/VC deals in Q4 and look for the insights.

Spoiler Alert: $NVDA look like a bargain.

The full Q4 2024 deals database is at the bottom of the post or at www.ywr.world under ‘Data and Models’.

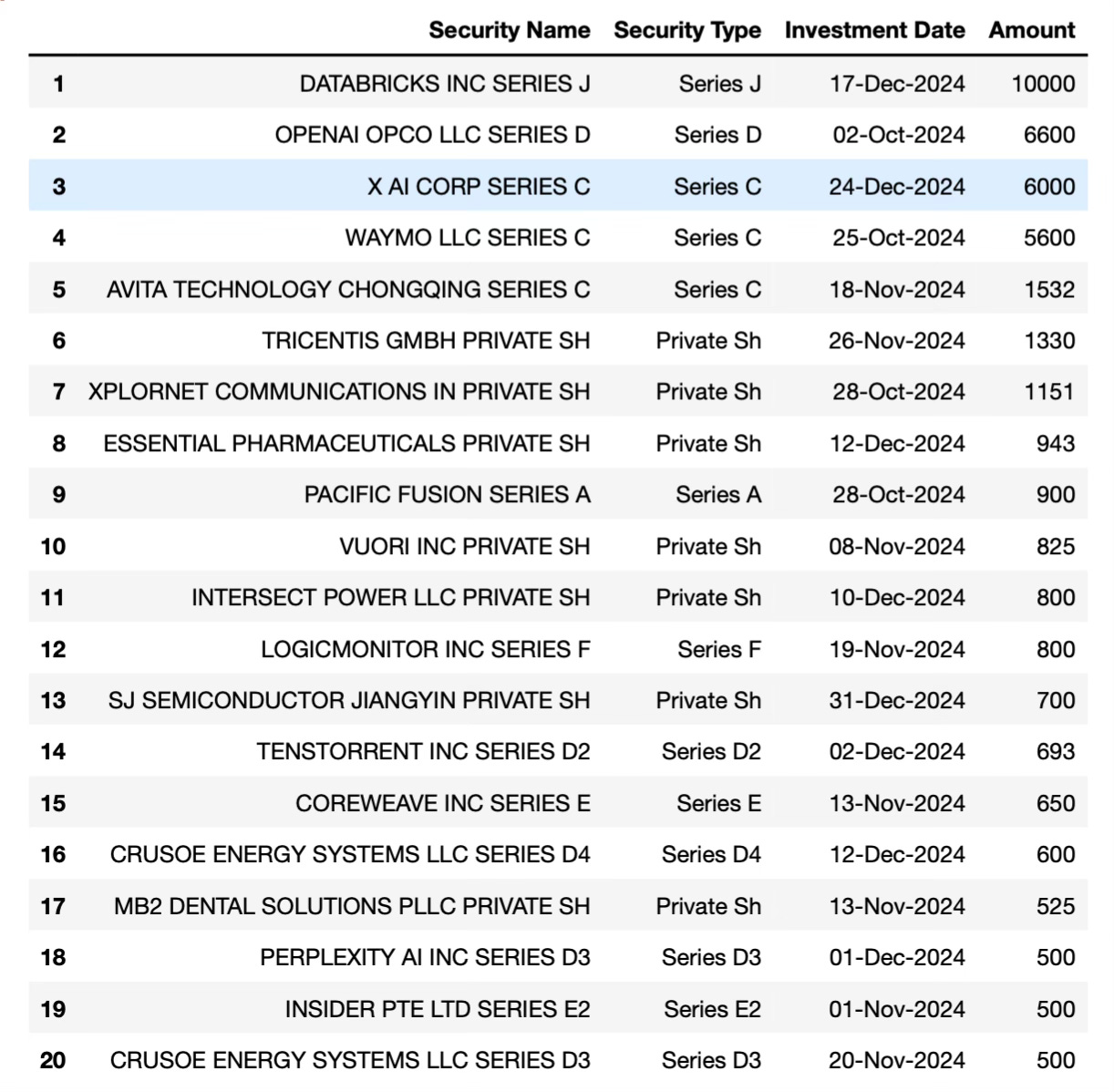

Top 20 Deals

Databricks: The deal size is stunning. A $10bn raise at a $62bn valuation. It is continued validation that private markets have reached such a scale, and diversity of players, that they no longer need public markets. In fact they’re even better than public markets for raising money. Look at the list of who participated. Notice Sands Capital and Wellington. Public fund managers are moving to private as well.

SAN FRANCISCO, CA — December 17, 2024 — Databricks, the Data and AI company, today announced its Series J funding. The company is raising $10 billion of expected non-dilutive financing and has completed $8.6 billion to date. This funding values Databricks at $62 billion and is led by Thrive Capital. Along with Thrive, the round is co-led by Andreessen Horowitz, DST Global, GIC, Insight Partners and WCM Investment Management. Other significant participants include existing investor Ontario Teachers’ Pension Plan and new investors ICONIQ Growth, MGX, Sands Capital and Wellington Management.

Also look at the valuations.

Today’s announcement comes on the heels of Databricks’ recent momentum which includes:

Growing over 60% year-over-year in the third quarter ended October 31, 2024

Expecting to cross $3 billion revenue run-rate and be free cash flow positive in the fourth quarter ending January 31, 2025

Databricks has no free cash flow, but raises $10bn in a private market deal at 20x revenues. Databricks’s biggest competitor, Snowflake ($SNOW), has a public market valuation of $55bn, trades at 15x revenues and doesn’t make any money either. SNOW would struggle to raise $10bn in the public markets and my guess is they see their biggest competitor getting ahead by staying private….

What’s the lesson? If you want to be hyper growth, and raise large amounts of money at 20x revenues, you need to stay private. It’s the exact opposite of what you would expect. It’s easier to raise money in private markets and you can get a higher valuation.

PE+VC’s ‘get it’, not like those boring public market guys with their DCF’s.

And are there even investors to meet anymore in public markets between all the index funds and algo traders?

Another $6bn for OpenAI, another $6bn for X.AI: I lose track of how much money these companies are raising.

OpenAI Series C&D $6.6bn October 2024

OpenAI Series B $6bn in May 2024

X.AI Series C $6bn in December 2024

X.AI Series B $6bn in May 2024

Waymo: Waymo raises $5.6bn at a $45bn valuation, and like with Databricks we see the public asset managers getting sucked in too.

Today, we’re excited to announce that we’ve closed an oversubscribed investment round of $5.6 billion, led by Alphabet, with continued participation from Andreessen Horowitz, Fidelity, Perry Creek, Silver Lake, Tiger Global, and T. Rowe Price.

Baidu ($BIDU) must be pulling their hair out. They have the leading autonomous driving business in China and it gets valued at $0. In fact the entire company doesn’t even get valued at $45bn. Nope. You can have all of Baidu for $28bn, including $10bn in net cash. But why would you? It’s a public stock. Public stocks are diseased. I bet Tesla is wishing it could go back in time and stay private too. None of these robot-taxi businesses make any money, but at least in PE/VC world you get big valuations.

Avita: Interesting to see a $1.5bn raise from a Chinese automotive technology company. Avita used to be called ‘Changan Ulai New Energy Automobile Technology’. Avita is developing technologies for electric drive systems, hydrogen fuel cell systems and battery technology. It’s another datapoint, along with the Mercedes Auto R&D facility in Shanghai that the center for automotive technology has moved to China.

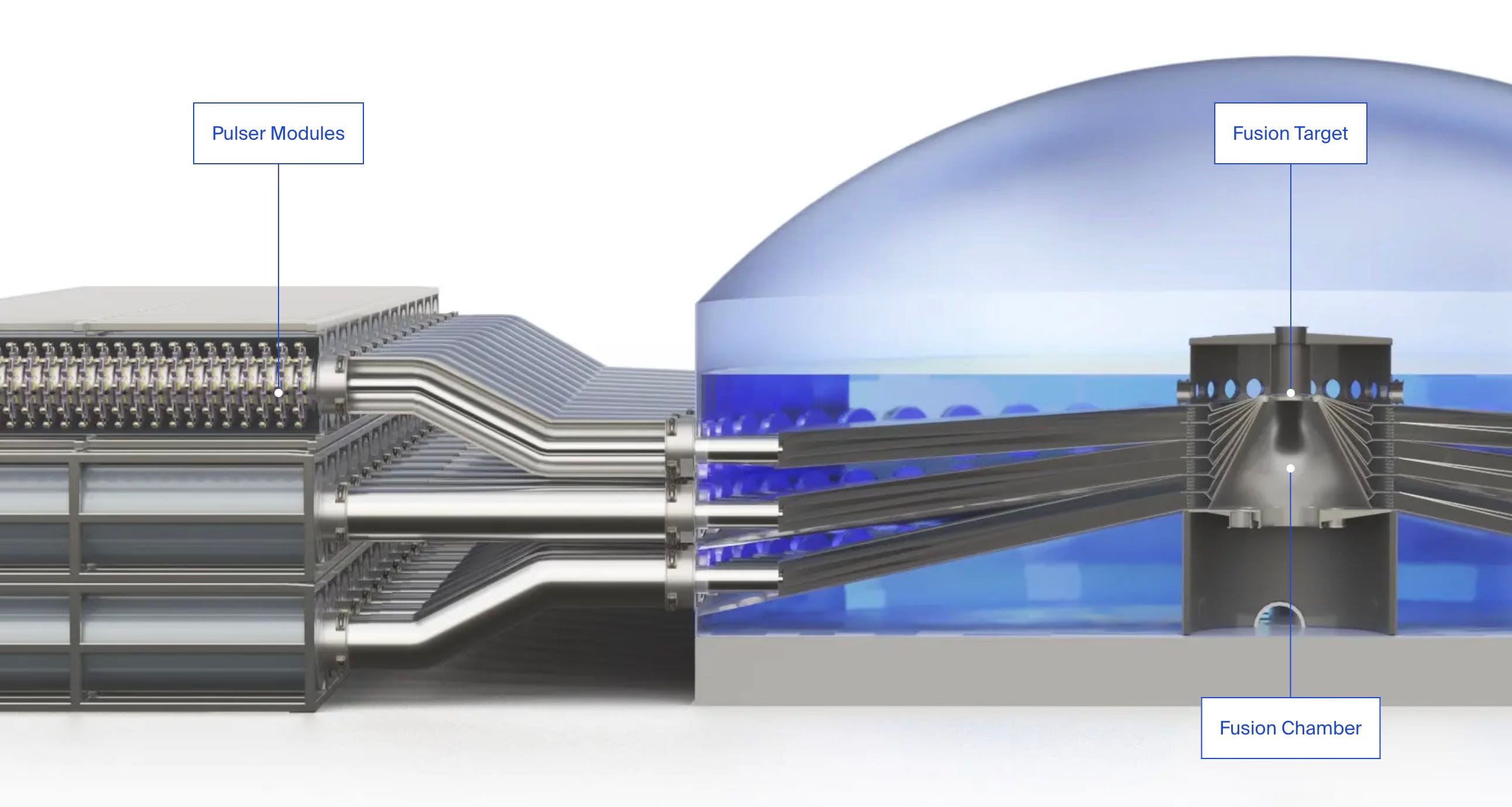

Pacific Fusion: What’s a technology which could take decades to develop and suck up billions in funding in the meantime?

Fusion Energy of course.

And who better to accept this noble, world saving, challenge? The VC industry. It’s probably a good thing though for Silicon Valley to get involved. I’ve visited the ITER project in France and there is no solution in sight (La Puissance du Soleil).

Our funding: More than $900M so far from the best syndicate we could ask for. Our plans are ambitious, and we are proud and humbled to have an amazing set of investors supporting us and our work. We have secured more than $900 million in our Series A to date. Hemant Taneja of General Catalyst led the round. Alongside General Catalyst, a great mix of institutional VCs and individual company builders have participated, including: Andrew Forrest, Breakthrough Energy Ventures, Elad Gil, Eric Schmidt, John Doerr, Ken Griffin, Lachy Groom, Leitmotif, Lightspeed, Lowercarbon Capital, Mustafa Suleyman, Patrick Collison, Reid Hoffman, Richard Merkin, and Trousdale Ventures. Hemant Taneja, Eric Schmidt, and Patrick Collison joined our Board of Directors.

You can read the full Founder’s Letter here.

Vuori: General Atlantic accidentally invested $825mn in a California clothing company. They must have thought Vuori meant fusion or AI in Latin. But it might work out anyways. There is some question whether Alo is cooler than Vuori, but my sources tell me ‘Alo is shinny and looks fake and flashy vuori is more cali’.

Top 20 Deals under $100mn

The sub-$100mn deals always include a lot of biotech, but we also see robotics deals like AMP Robotics and Carbon Autonomous. The Carbon Robotics Laser Weeder is actually kind of cool.

‘We’re focused very intently on the field. There’s a lot happening in agriculture and agtech right now and I think what folks maybe don’t realize is that some of the most advanced technology in the world in terms of AI, robotics, deep learning is being deployed right now in farms to help agriculture and agtech,”

Carbon Robotics CEO Paul Mikesell

Camusat provides outsourcing solutions for African mobile phone operators.

Speakeasy is a South Korean language app.

Most Active Funds

It’s quirk of the dataset that deal size amounts are usually only available for VC deals. It makes it looks like the traditional PE funds are not active. The other quirk of the data is we can’t see how much each firm is contributing to the deals, so I just have to group firms and deal sizes. But it still gives us an overall idea who is the most active.

Interesting to see Tiger Global back in the game.

Thrive is either going to the moon, or to 0.

For me AH is the new Sequoia, especially with their lead in crypto.

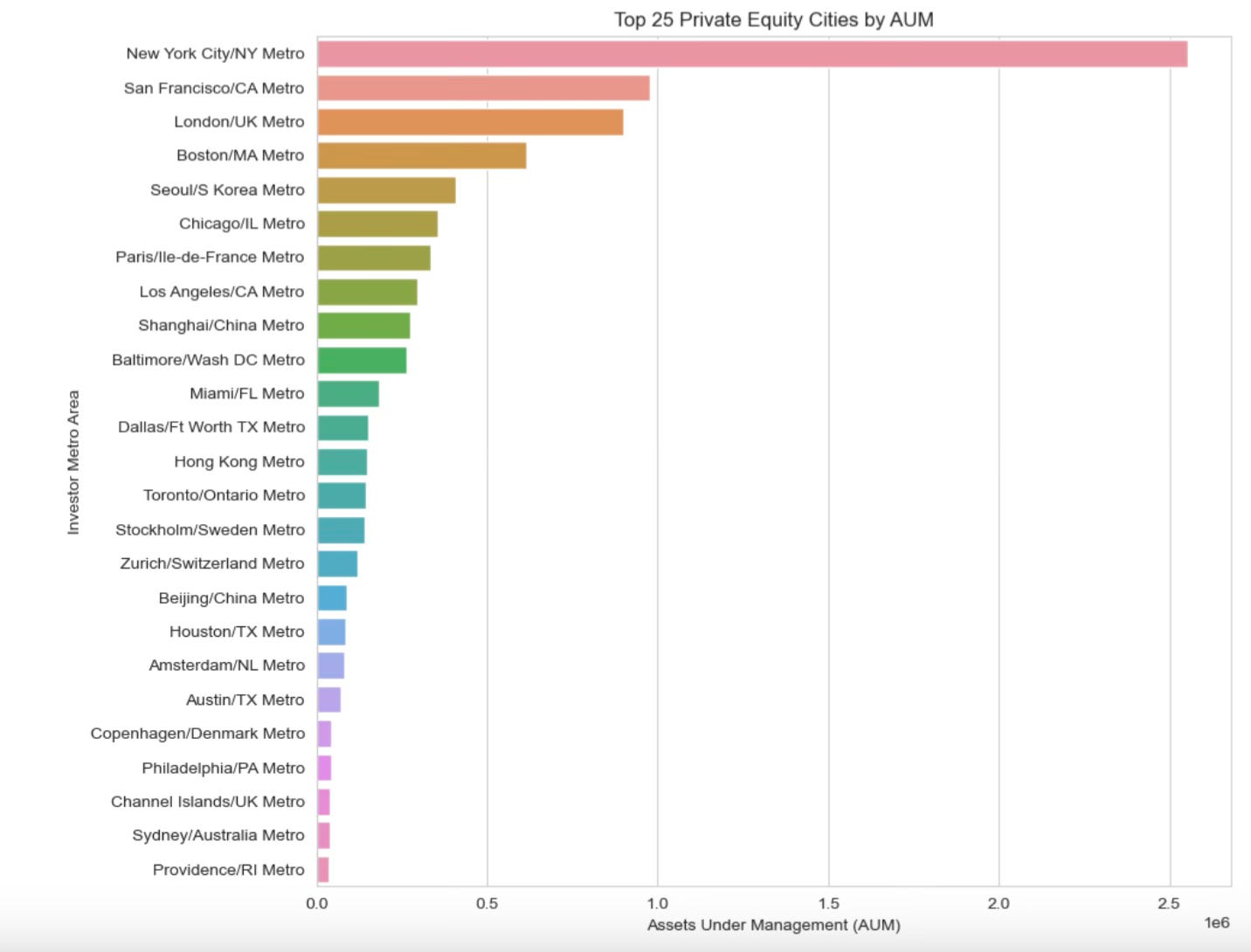

Top Cities for PE/VA AUM

If you think about it the US is in the Capital Allocation business and the Innovation business. Increasingly, the sovereign wealth funds and savers of the world send their money to a handful of US cities (NY, SF, Boston, Chicago) where money managers there decide where these savings should go. And being US based managers they naturally decide the best place for this money is to go is into US tech plays.

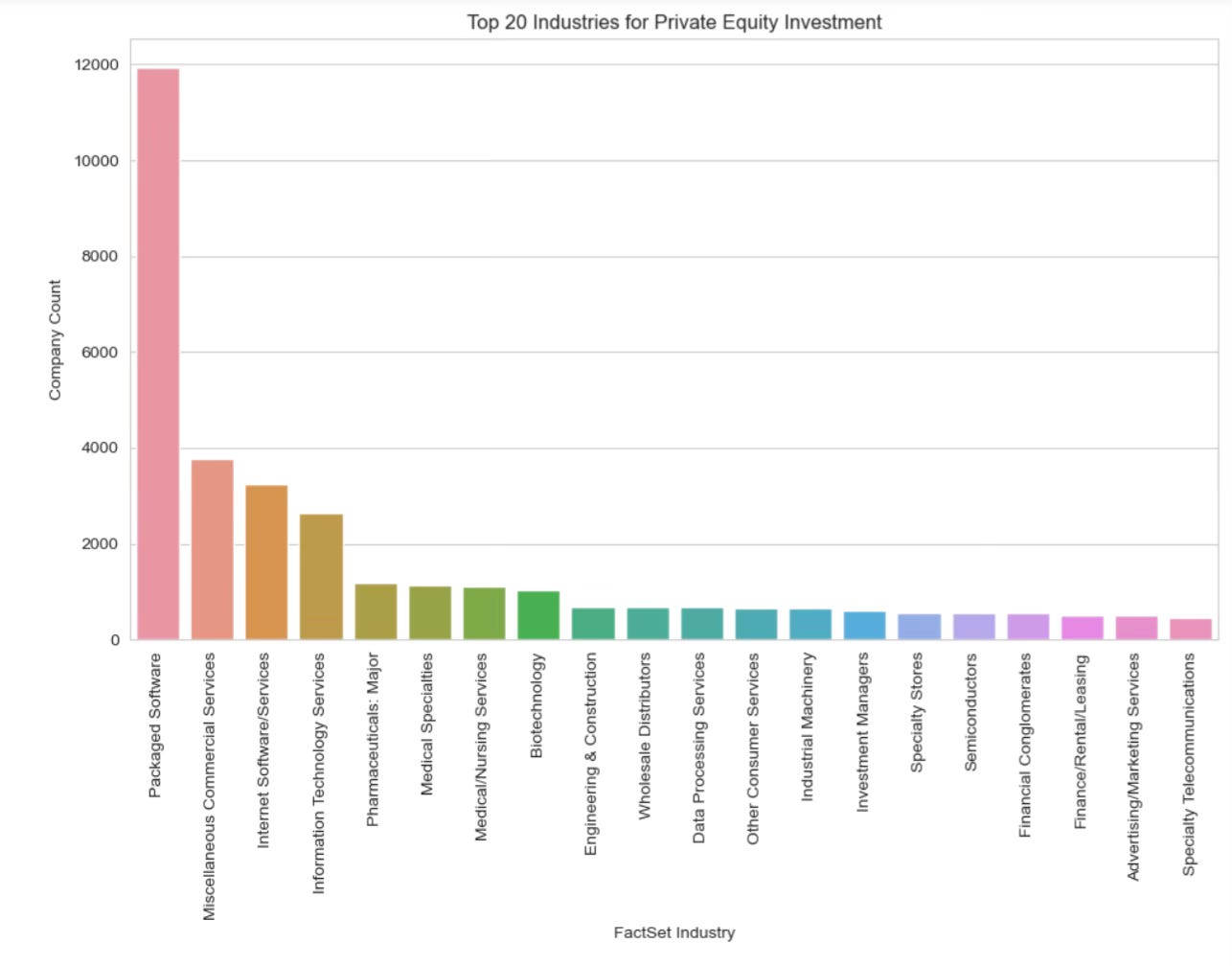

Top 20 Industries for PE/VC investments

When we analyse over 46,600 private investments we find almost 12,000 are ‘software’ companies. Another 4,800 are ‘internet’ or ‘IT’ companies. Then you have another 4,300 in medical or biotech. Overall, 38% of portfolio companies are ‘tech’ and another 9.5% are Pharma/biotech.

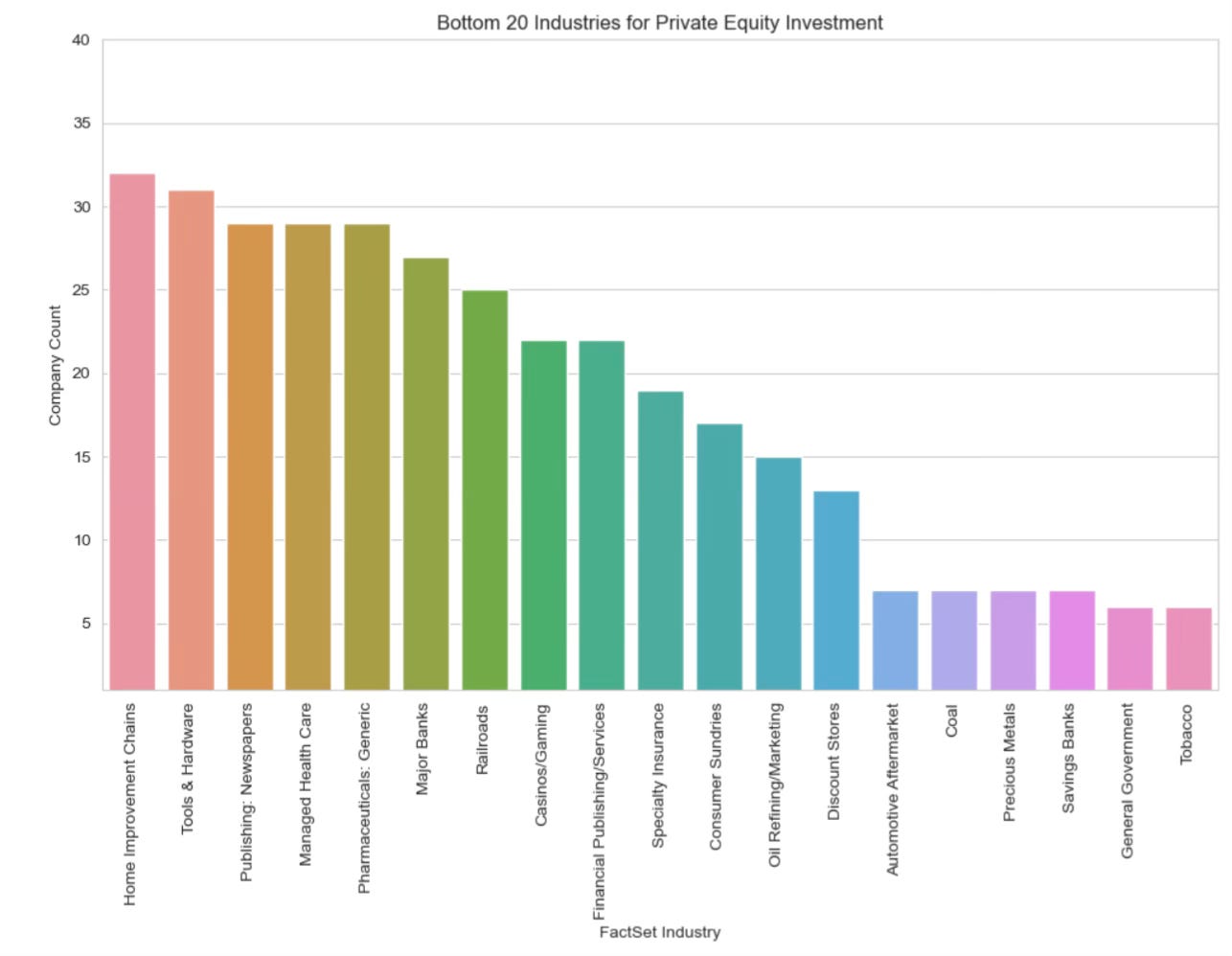

The Bottom 20 industries for PE/VC investment.

I think if you are a PE/VC investing in oil refining, insurance or banks is like investing in candle making companies or buggy whips.

Here is a link to the full dataset of Q4 deals.