YWR: PEVC Q1 Deal Tracker

We’ll get into the Q1 2025 PE/VC deals, but first a quick update on ‘Anatomy of a Private Equity Train Smash’ our made for Netflix tragedy. The writers came up a with a new plot twist I wanted to share.

Do you remember in the original script how the university endowments (like Yale, Harvard and Princeton) all over allocate to Private Equity at the top of the market, and then can’t get their money back? In the original script we had it where they slowly suffer for years; bleeding out their liquid positions in hedge funds and public markets to fund operating costs while hanging on to an increasingly illiquid portfolio.

Well we decided to make the story more exciting.

In a new plot twist we have the Universities get into a fight with the Federal Government about their Diversity Policies and lose both Federal research funding and the tax exempt status for their endowments. In this new twist instead of being able to wait patiently for PE and VC values to recover the universities have liquidity problems and fire sale billion dollar portfolios into the secondary market. It’s a complete surprise for the audience because these are the same ‘patient, long-term investors’ who were supposedly so perfectly suited for private equity because they could ‘handle the volatility’.

In the movie fire sales by the university endowments drag down valuations for entire asset class, which means the pension funds have to take mark downs too. For a while they resist, but eventually the investment committees get anxious and decide unanimously to reduce their ‘model’ private equity and venture capital allocation. This leads to more calls for liquidity. More forced selling.

We’ve kept the rest of the script the same where eventually interest rates step another leg higher and the final capitulation ensues.

Then in the final chapters, ‘a new era’, we have a whole batch of new CIO’s takeover who promise a ‘greater focus on portfolio liquidity and risk management’ (which means selling the remaining positions on the lows). This change in CIO leadership sets up the next 10 year bull market for private equity, which all the endowments then miss.

That’s the script so far.

We’re brainstorming another plot twist where there is a computing improvement which makes vast datacenters obsolete, kind of like old IBM mainframes. Future datacenters are the size of a suitcase and the datacenter office parks become dinosaurs.

But we’re still workshopping it.

As I said, the movie’s going to be great. But it’s also sad. It’s a reminder to the audience to try to be a little bit non-consensus and resist the power of the crowd, especially at extremes.

Anyways…

Moving on to the Q1 2025 top deals. Remember the data is from Factset and spotty on the participants and deal amounts. Deal amount data typically given for the venture deals, not PE.

At the bottom of the post is the full dataset with every investment round and investor for Q1.

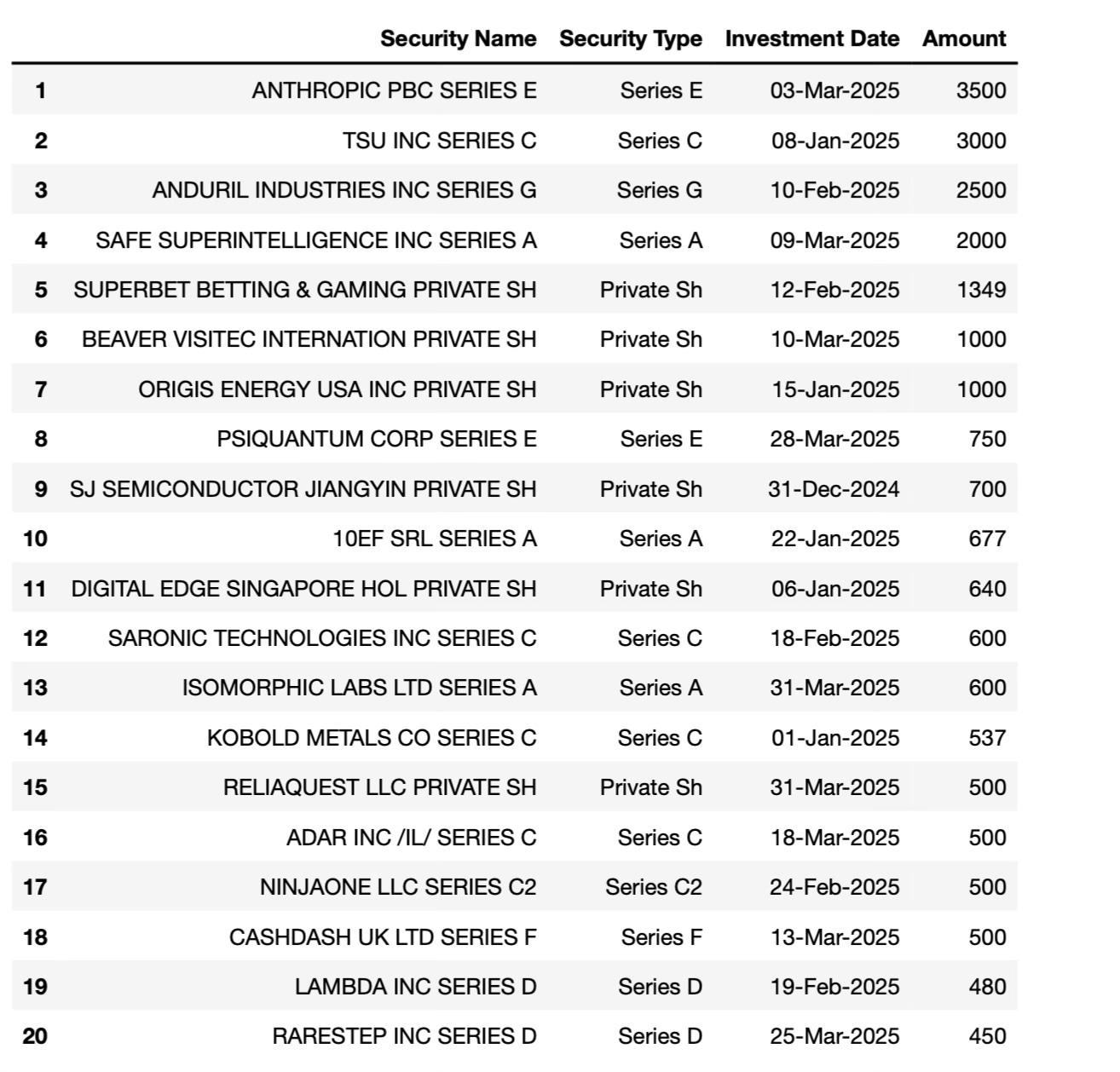

Top 20 Deals (>$100mn)

Anthropic: $3.5 billion raise. Anthropic seem to have found their niche as the best AI at coding, which keeps them in the game. And coding really is an AI super power.

Claude 3.7 Sonnet has set a new high-water mark in coding abilities—an area where Anthropic plans to make further progress in the coming months.

Between xAI, OpenAI and Anthropic, these businesses really are tremendous consumers of capital.

Anduril: Who would have ever predicted the greatest danger to the People’s Liberation Army would be this guy?

But Lucky Palmer is amazing. The Anduril press releases show tremendous cadence. Silicon Valley does defence really well. They probably wonder why they didn’t get into this industry earlier.

Anduril Unveils Copperhead: A New Era of Autonomous Undersea Dominance

Anduril Test Fires Hypersonic Solid Rocket Motor for the U.S. Navy

Anduril Introduces Seabed Sentry Undersea Sensor Network

Anduril to Provide AI-Powered Counter Unmanned Aerial System (CUAS) Technology to Safeguard U.S. Marine Corps Installations Globally

Barracuda-500 Selected to Move Forward on the Enterprise Test Vehicle Prototype Project

Anduril and Microsoft Partner to Advance Integrated Visual Augmentation System (IVAS) Program for the U.S. Army

Safe Super Intelligence: A $2bn raise at a $23 billion valuation, after $1bn in September 2024, for the Ilya Sutskever start up which has no product, no website, but researches safe AI.

Superbet: Blackstone quietly rolling up European betting companies. These are great business for incorporating AI.

Origis Energy: Solar farms are still able to get money, but it’s way down from 2023.

PsiQuantum: $750 million into a quantum computing company at a $6 billion valuation. PsiQuantum focuses on photonics instead of circuits.

The Palo Alto-based company is taking a distinct route from rivals like Google and IBM. Instead of superconducting circuits or trapped atoms, PsiQuantum builds its quantum bits — called qubits — using individual photons, or particles of light. These photons move through waveguides on silicon chips, where they’re manipulated using mirrors and sensors. PsiQuantum says this allows it to leverage traditional chipmaking infrastructure to scale production.

And they are going to set up a quantum computing park… in Chicago.

SJ Semiconductor:

$700mn raise for a Chinese semiconductor company. Surprisingly, no US venture funds involved. The round was led by Wuxi Chanfa Science and Technology Innovation Fund, Jiangyin Binjiang Chengyuan Investment Group, Lingang Xinxin Fund of Shanghai Lingang Special Area Administration and China Life Private Equity Investment Limited. Not your household names.

Question. Is Wuxi Chanfa the new Sequoia? Instead of laughing, should we be ditching western VC’s all chasing the same ideas in a crowded market, and go into Chinese venture capital funds? I know it’s not possible. Just stirring the pot.

Digital Edge Singapore: A US private equity fund (Stonepeak), run by ex-Macquarie Australians, comes up with a radical new idea to invest $1 billion in data centres… in Singapore.

Maybe they can star in our movie if we do the data center scene.

Isomorphic Labs: When you analyze the start of any great innovation city, there is usually an early company, or two, which started it all (Microsoft and Seattle for Seattle). In the future, when they write the book on the London AI boom, they will say it all started with Deep Mind, and Deep Mind spin-offs like Alpha Fold and Isomorphic Labs.

LONDON, 31 March, 2025 - Isomorphic Labs, an AI-first drug design and development company,today announced it has raised $600 Million in its first external funding round. The financing round is led by Thrive Capital, with participation from GV, and follow-on capital from existing investor, Alphabet.

Saronic Technology: $600 million raise for another defenceTech business. Let’s take a bunch of cool themes and smash them together. Saronic, it’s like Anduril, but it builds ships, because the US needs to build ships again. But these will be AI ships, and it will be based in Austin, which is 160 miles from the ocean, but Austin is cooler and more techy than Houston.

Kobold Metals… do we laugh, cry or do we learn?

We laugh because Kobold are packaging a $537 million investment, (at $2.9 billion valuation) into a Zambian copper exploration company, with no production, as a high tech AI investment.

$3bn for Kobold, the ‘AI’ Zambian copper explorer with no production, or $10 billion for First Quantum which produces 450,000 tons of Zambian copper/year? You decide which makes sense.

We cry because they actually raised $537 million on this nonsense with Bill Gates, Sam Altman and Jeff Bezos personally putting in money. FFS.

But in the end instead of making fun of Kobold, should we try and learn from them?

Maybe this is the new way you raise money for mining in this day and age. What did Jesse James say? Go where the money is.

You want to raise money for a Zambian copper mine? Don’t go to Vancouver and squeeze water from a stone. Go to Silicon Valley. Go where the money is and pitch it as an AI investment.

Let’s learn the great art of story telling from this NY Times article and use it for our next raise.

Part 1: Connie Chan and the ‘realisation’

KoBold originated half a decade ago in the belated realization among Silicon Valley’s barons of what lay ahead.Their products had become the backbone of the United States economy. But their businesses couldn’t grow much further without a gargantuan increase in the mining of a handful of raw materials that make batteries, without which everything from cellphones to electric trucks simply can’t function. They needed far more copper, cobalt, lithium and nickel.

“The more you realize how dependent we are on these technologies, the more you ask: How the hell were we so slow to the fact that we needed vast amounts of raw material to make it all possible?” said Connie Chan, a partner at Andreessen Horowitz, the biggest venture capital firm in the United States and an early investor in KoBold.

Part 2: A call to action! The Hero’s Journey.

Investors from American and European private equity funds that collectively manage trillions of dollars in assets, including ones started by Silicon Valley giants like Bill Gates and Sam Altman of OpenAI, were joined by more traditional industrial companies in putting hundreds of millions of dollars into KoBold.

Part 3 in the story will be the low point when the Zambian government screws them, and the mine has no power.

Part 4: will then be a heroic ending where the AI copper mine saves the planet’s datacenters and keeps the chatbots running.

I need to stop. This is too painful.

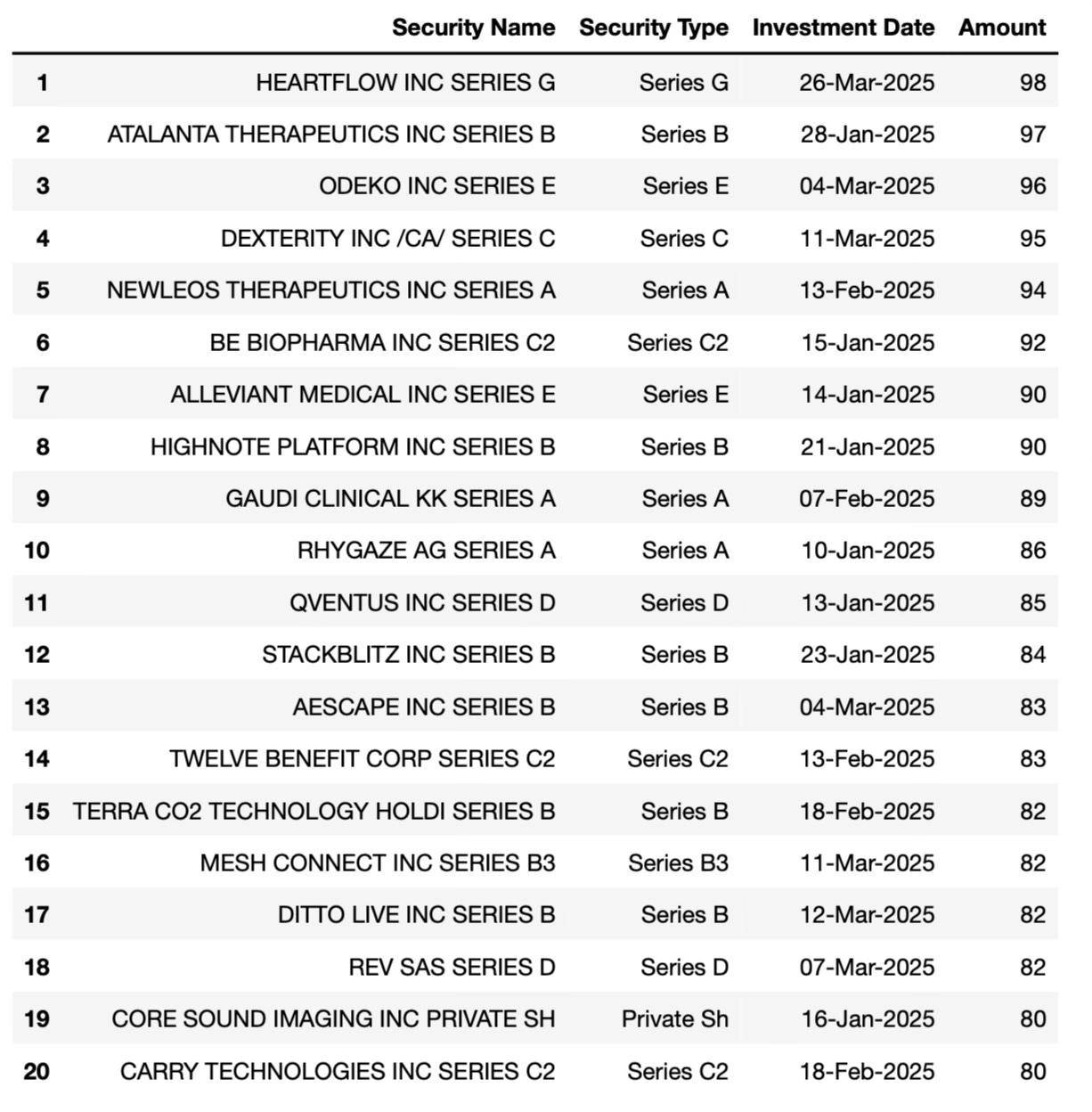

Top 20 Deals (Less than $100mn)

We focus on the big deals, but most deals are under $100 million. These deals are heavily biotech.

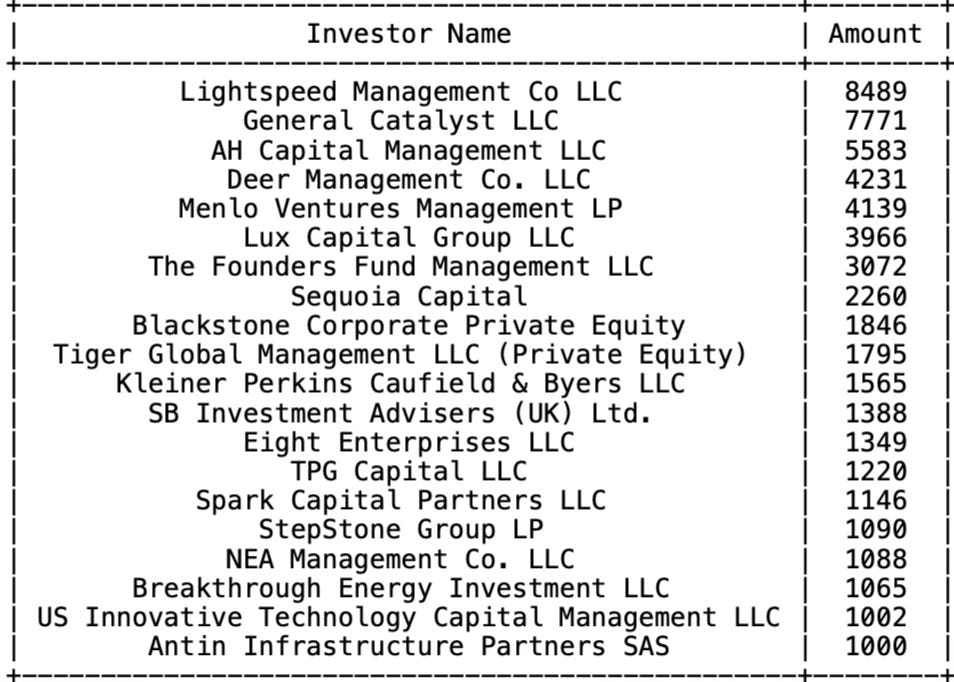

Most Active Funds

In this table we sum up every time a fund is part of a deal, and the deal amount, to get some sense which funds have been most active in the quarter. There are obvious gaps in that methodology, but it’s the best we can do with the data we have.

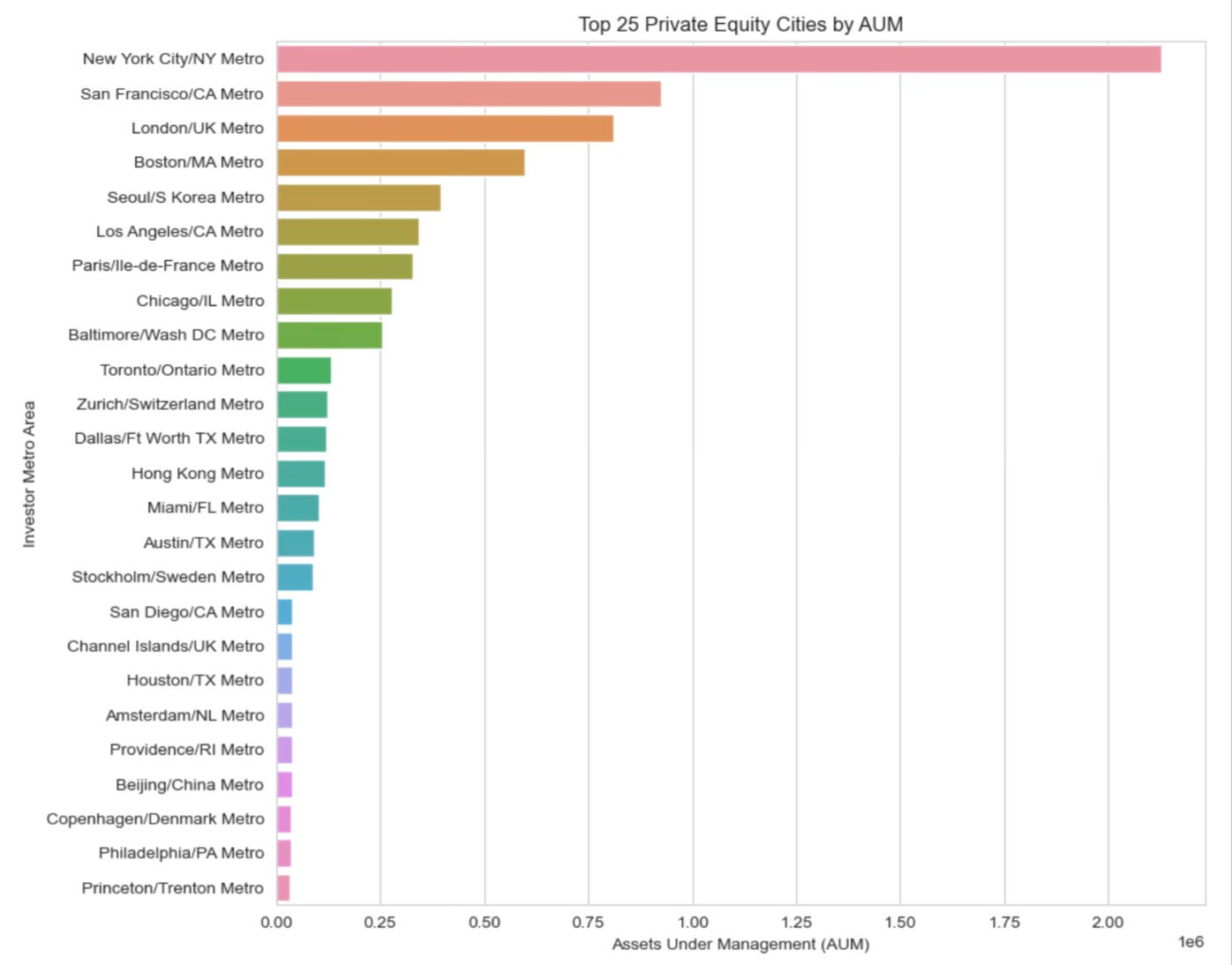

The Borg

Anyone who thinks NY is ‘done’ should look at the concentration of Private Equity AUM by city. And it’s the same for hedge funds. On these charts NYC is very alive, even if the PM’s live in Miami.

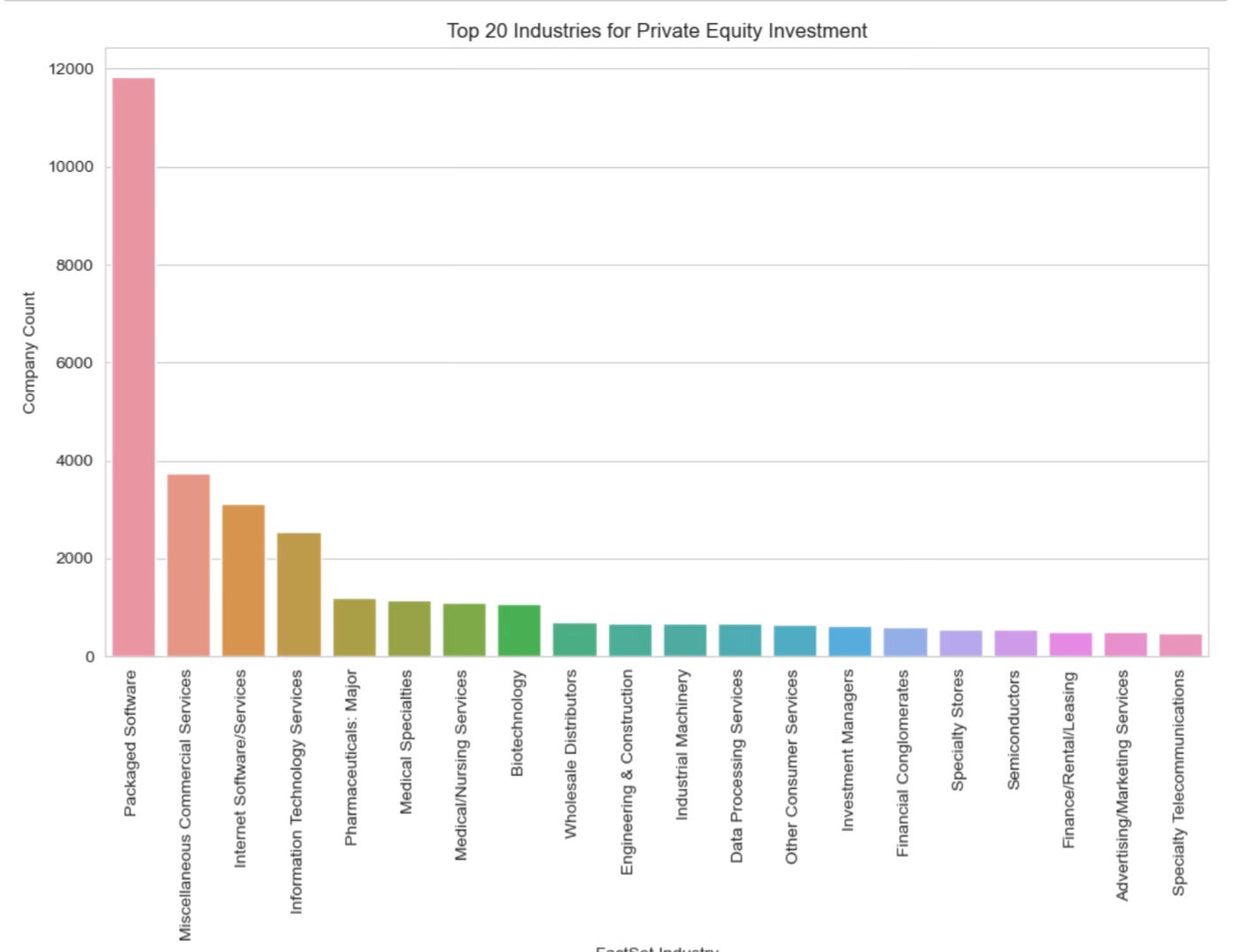

In Appreciating AWS we highlighted this analysis of 46,000 private equity holdings by industry. It shows how much Private Equity and Venture invest into software and internet services. The focus on ‘tech’ is so dominant.

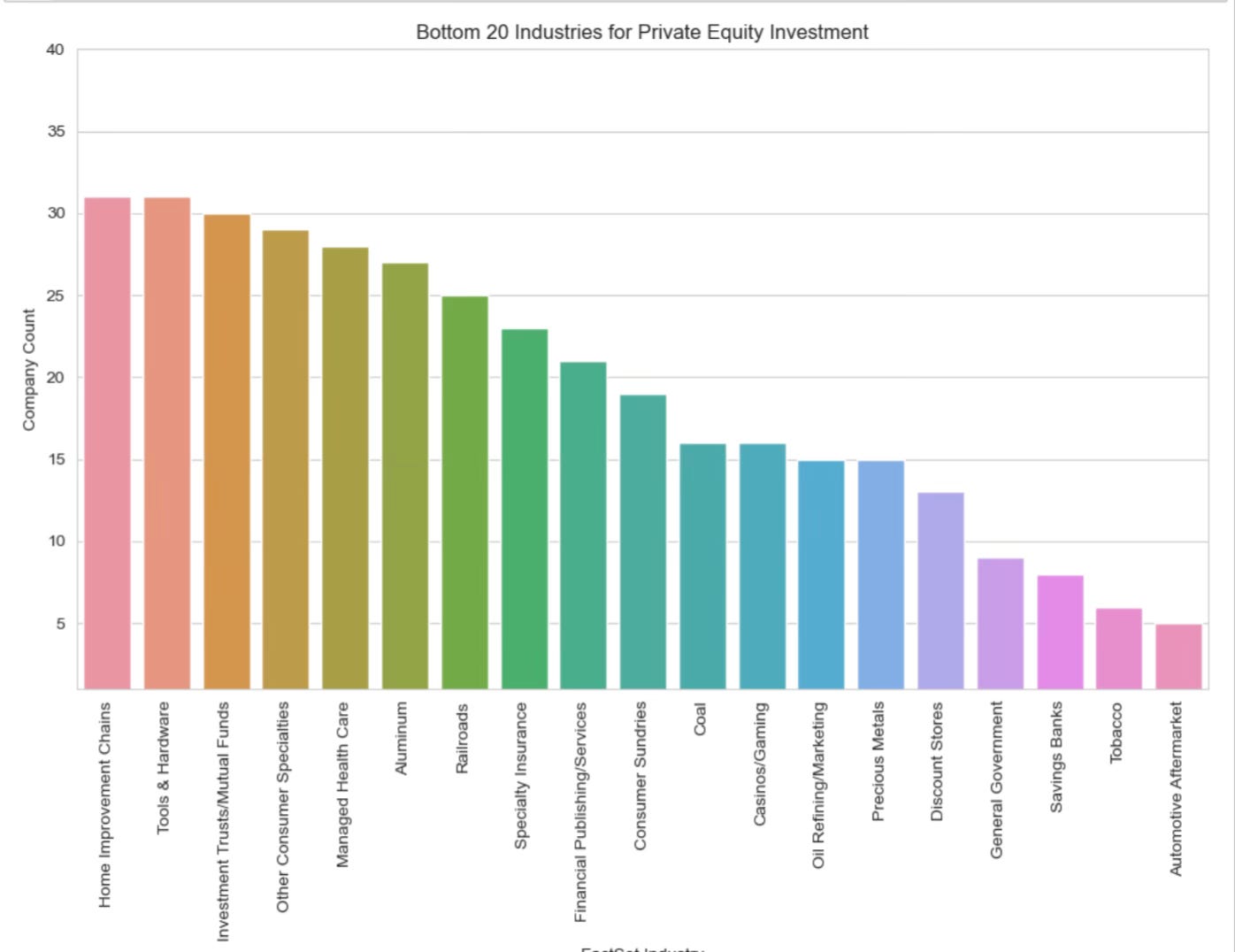

And when we look at the bottom 20 industries we see how few portfolio companies are in automotive, tobacco, savings banks, precious metals, refining, and casinos, and coal.

The full Q1 deal dataset is below.