YWR: Project Zimbabwe Update

Alert: These are personal views, not investment recommendations!

June’s Killer Charts is a recap of our main research themes, plus a new one (Cybertron).

The full 74 slide deck is at the bottom of the post.

But here’s a quick table of contents and the main ideas.

#1 Project Zimbabwe Theme

The persistent theme driving everything.

An era of higher inflation.

Stock markets will surprise everyone to the upside.

Trading speculation will be high, but this is natural when money is losing value. It’s a sign of the times.

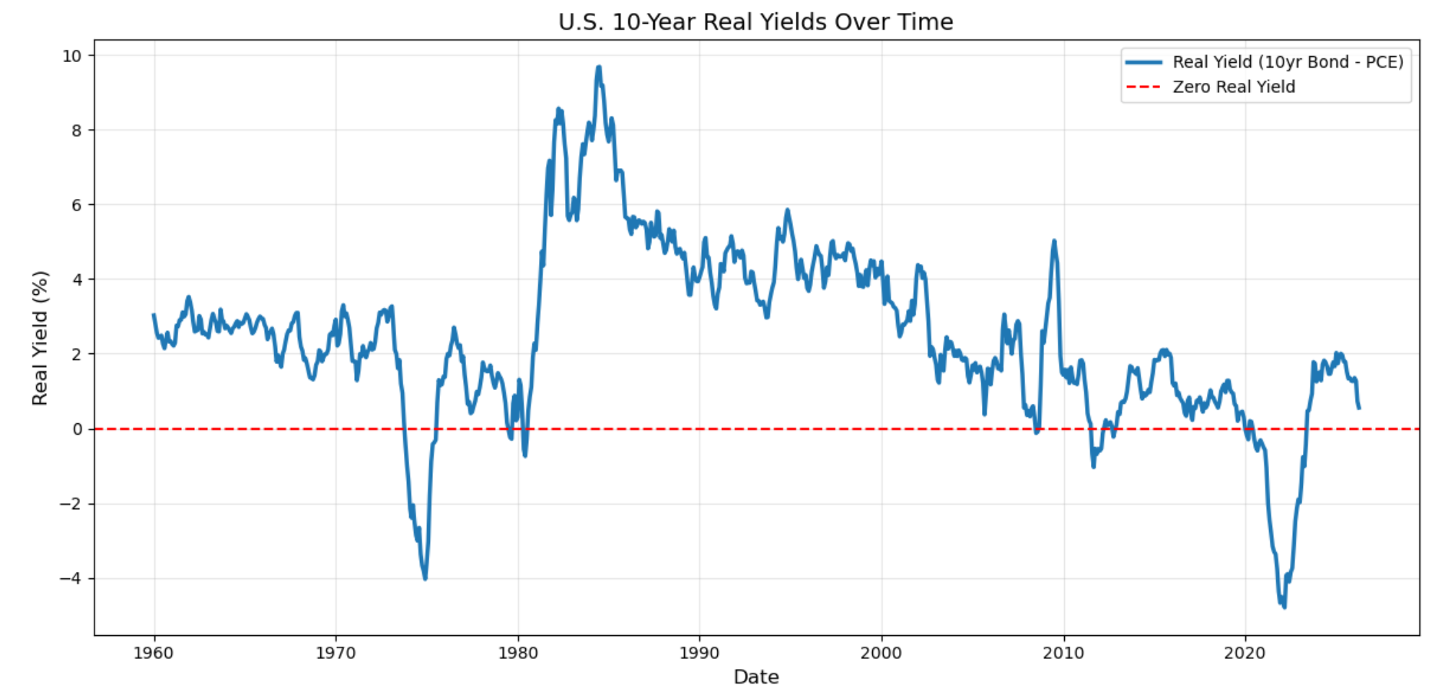

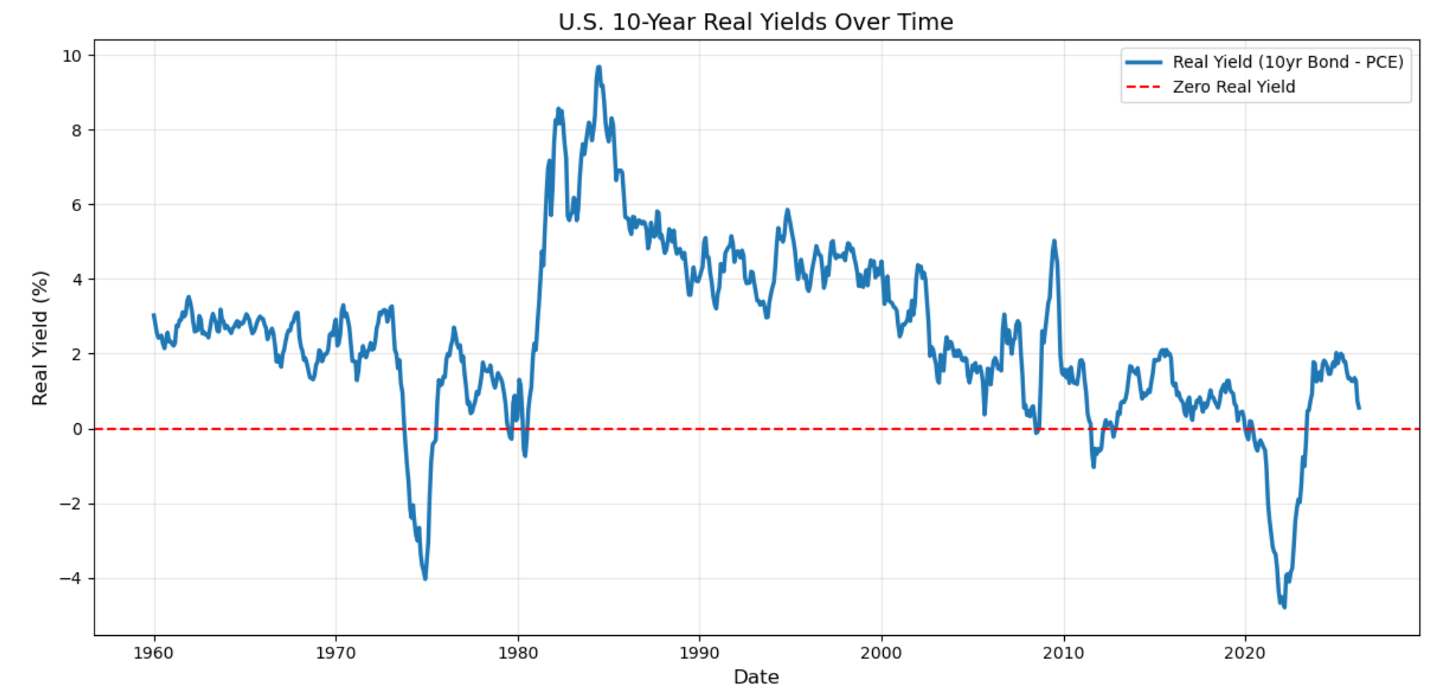

Bond yields rise over time, but remain low relative to inflation and supportive of equity returns.

‘Bad is Good’ - Society feels like it is falling apart, but markets go higher.

#2 Cybertron Theme

We are still in the early days of building the AI/Robot economy.

Winning theme of the last 25 years: Online vs offline.

Winning theme of next 25 years: Robots vs Humans

Tailwind behind robot and AI themes. Human industries derate.

Cybertron Markets (Korea + Japan + Taiwan + China + US) outperform Rest of World?

#3 Elysium Theme

Divergence not convergence

Divergence of wealth - Extreme wealth of the 1%

Divergence of Economies - Emerging markets economies don’t converge with the developed world.

Intense immigration pressure from 3rd world countries to find opportunity in Elysium (developed markets/US).

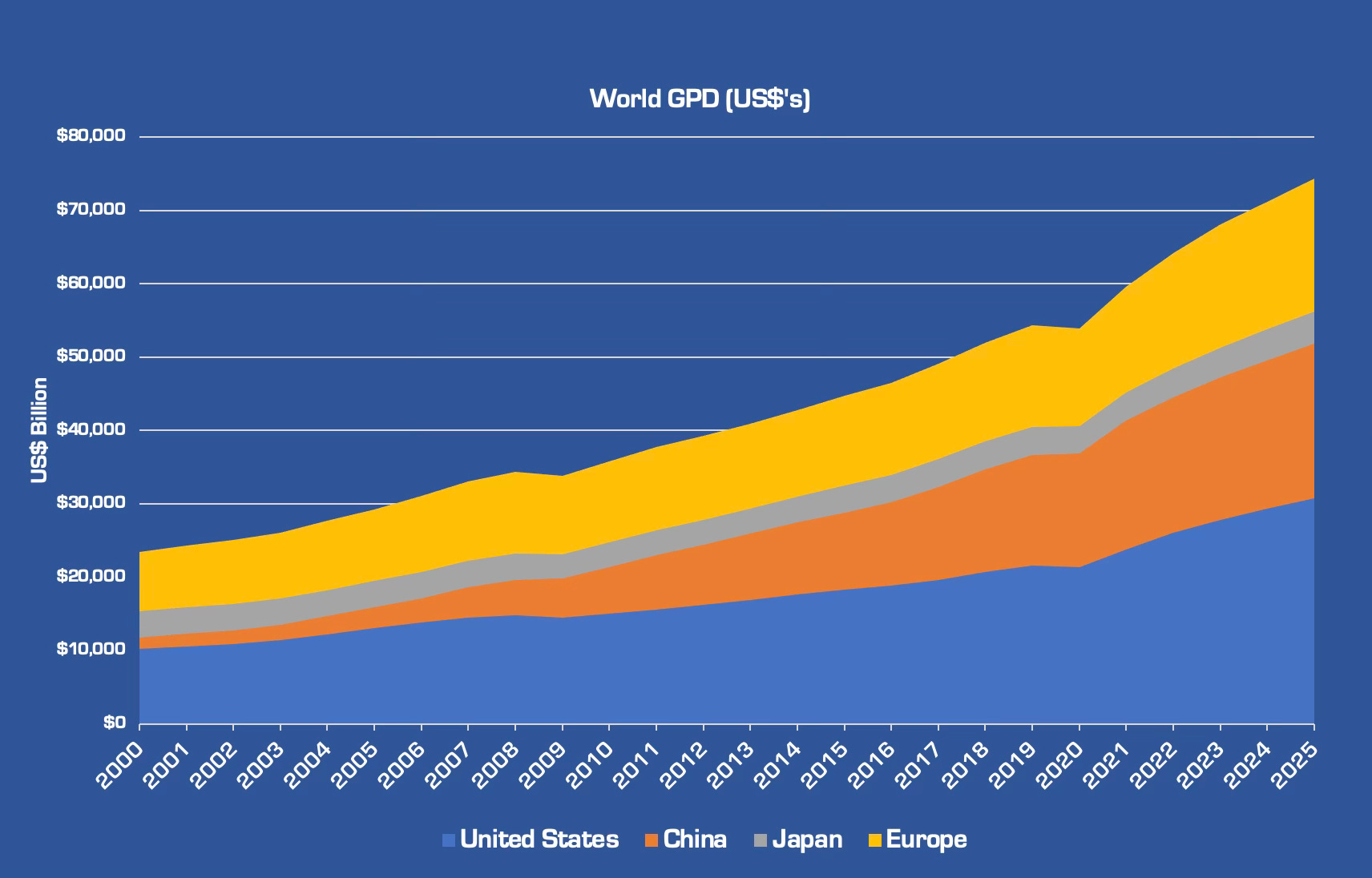

#4 World Economic Boom

Nominal GDP is growing strongly

US + Europe + Japan all booming

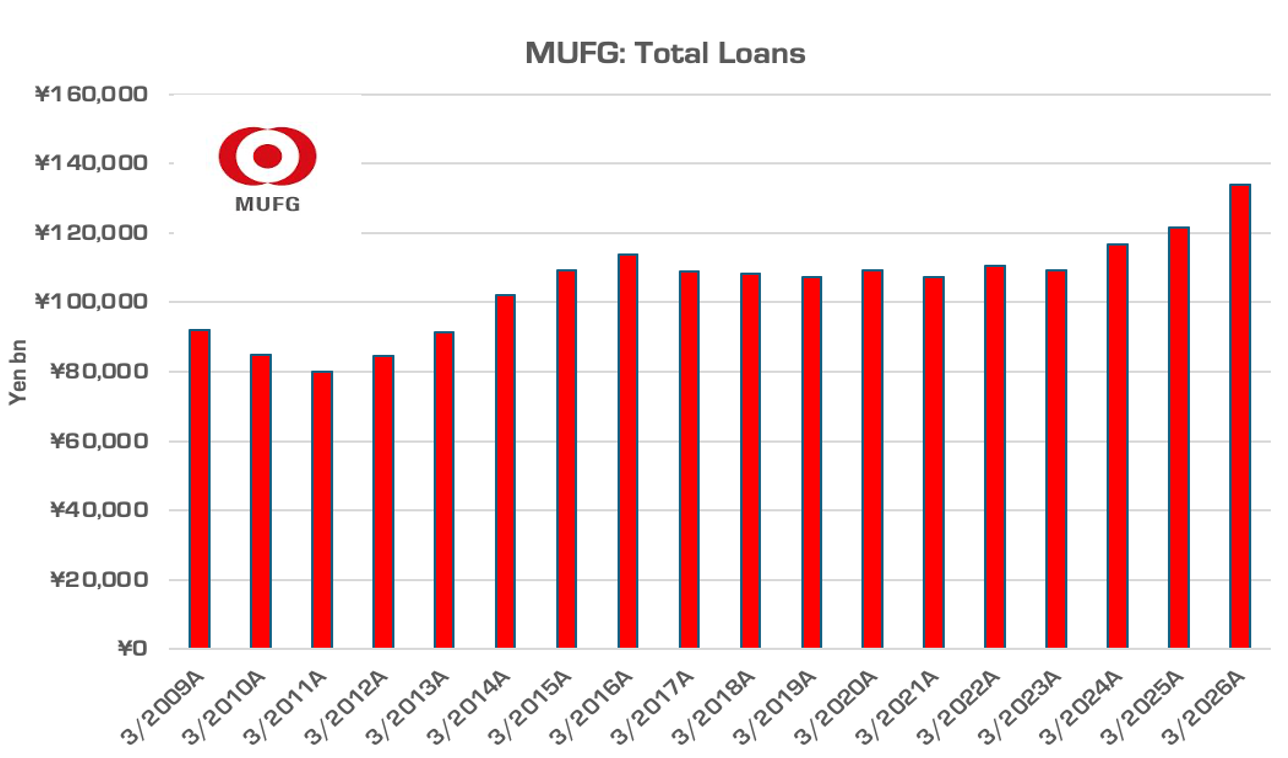

#5 Return to Loan Growth

Banks in Europe + US + Japan have never been healthier.

Record high Tier 1 capital, record profits, and strong asset quality.

Change in top down direction from government and regulators.

Pendulum swings from Post-GFC ‘Never Again’ to ‘Risk On’

Banks start to lend again.

A new driver of economic growth.

Hard to have a widespread ‘credit bubble’ when banks haven’t been lending.

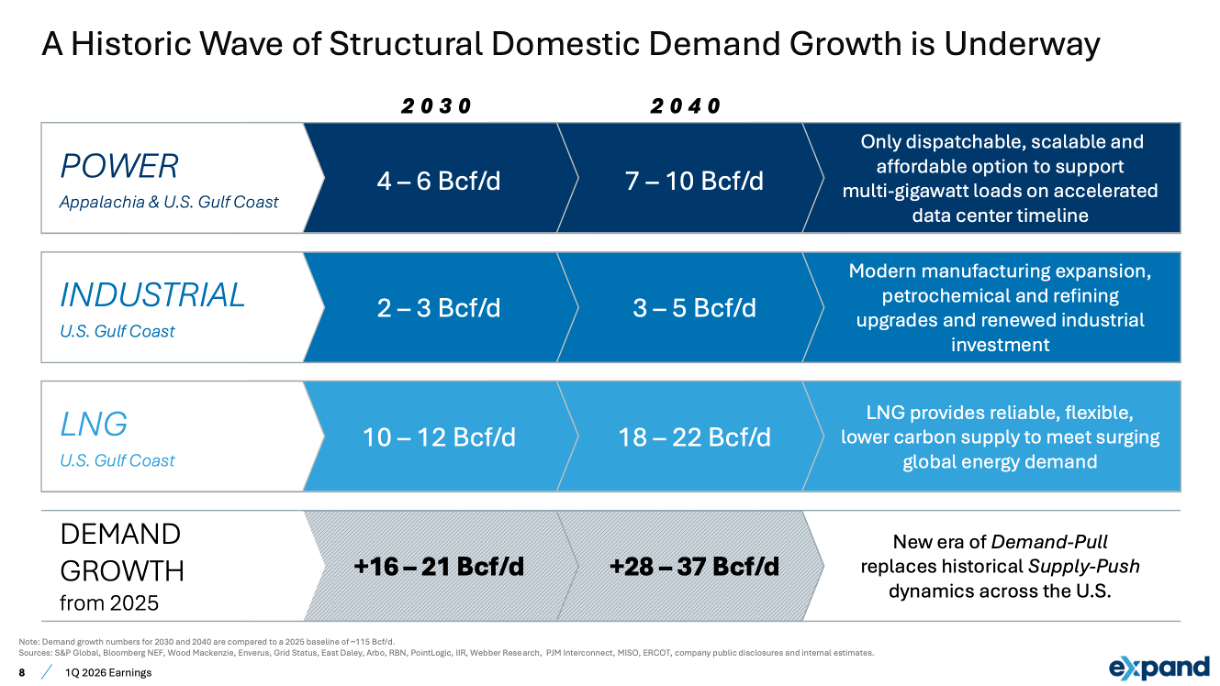

#6 The Final Bottleneck

Contrarian call on US Natural Gas

The AI datacenter play no one wants to own

Unprecedented confluence of demand drivers

Datacenter demand, LNG export demand, Industrial demand.

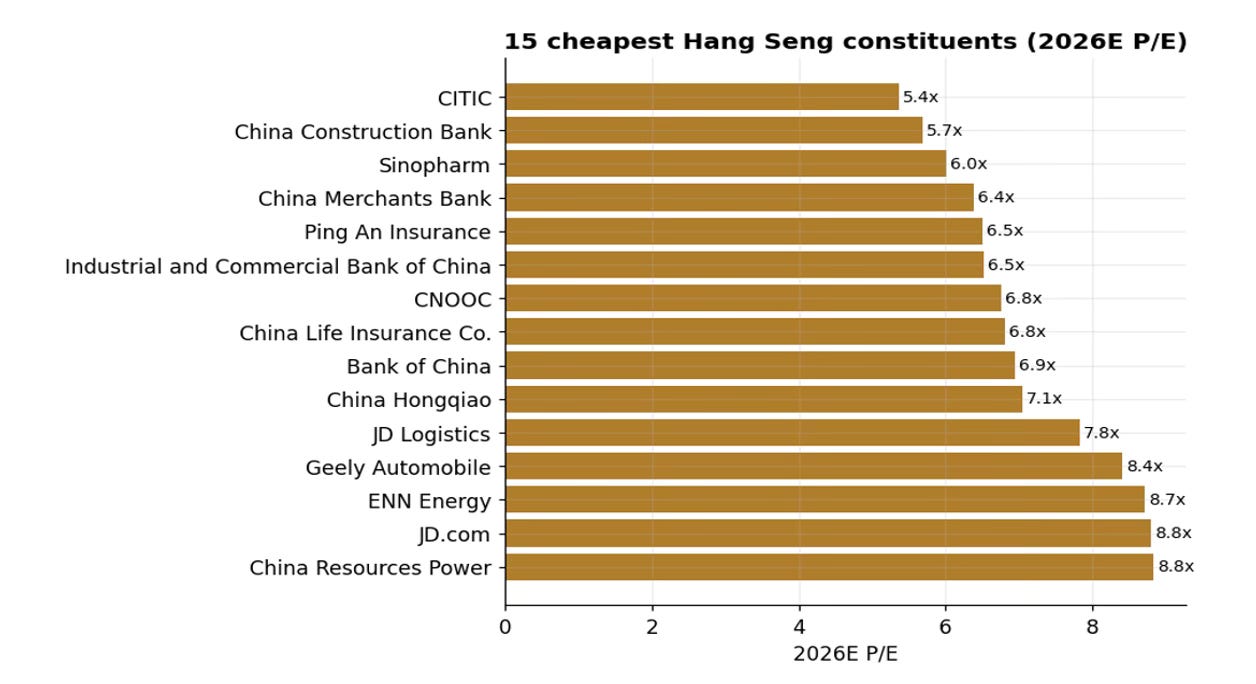

#7 Hang Seng on the Launchpad

Contrarian (but so far not working very well) call for a bull market in Hong Kong stocks.

Record low valuation

Earnings inflection.

Record low Chinese interest rates.

Negative: HK Tech is food delivery, online retail and video games, while exciting Cybertron tech is listed in Shanghai and Shenzhen.

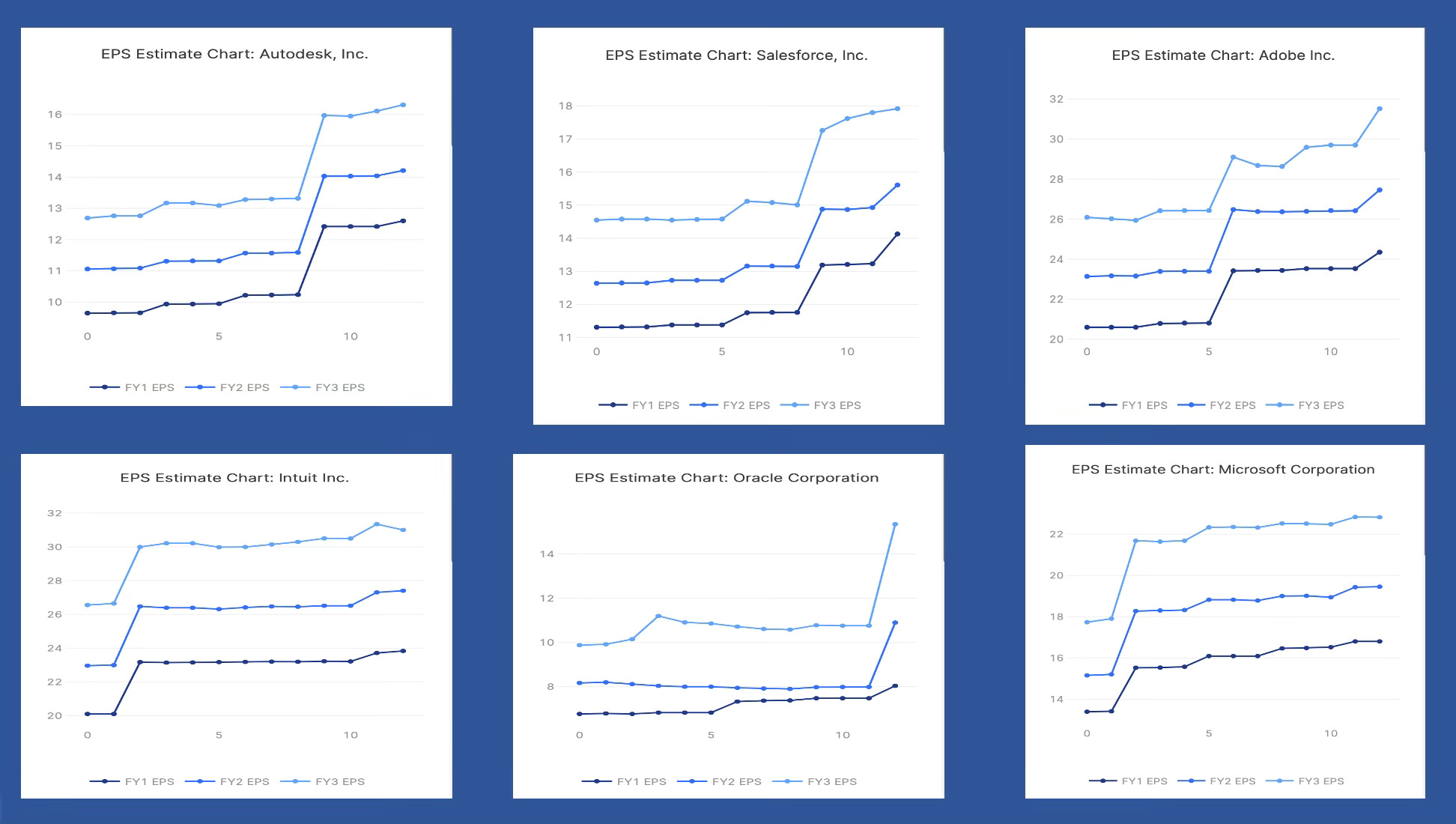

#8 Software

AI disruption fears might be overdone.

Estimate revisions are positive.

Big difference between vibe coding software and running an enterprise software business (debugging, maintenance, security)

But is it a value trap because longer-term fears around changes in the business model are warranted?

Is software a ‘human’ industry?

#9 Gold

Hard to call gold prices. No press releases or ‘catalysts’

Bull market drivers intact.

ETF Flows minimal and Futures positioning neutral.

After a 10 year winter, gold is entitled to a multi-year bull market.

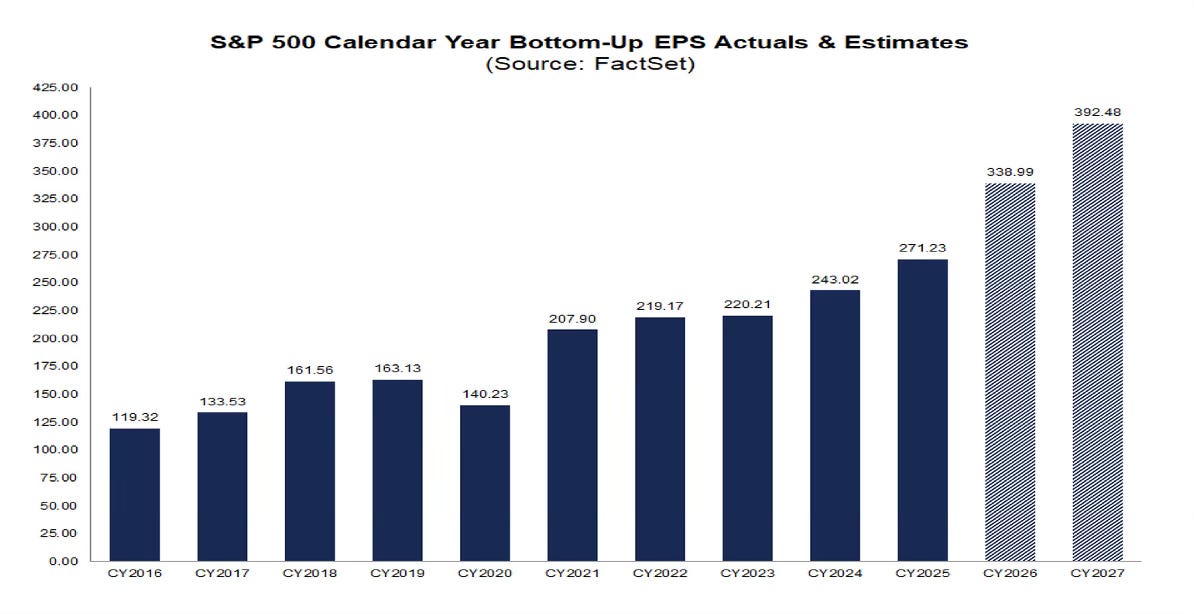

#10 S&P $10,000

Counterpoint to prevailing institutional negativity.

Earnings estimates are rising.

Earnings are curving upward (earnings growth accelerating)

Consistent double digit EPS growth with 4.5% 10 year yield justifies P/E > 25x.

Ask why bond yields are so low, not why market is expensive.

$400/share sometime by early 2028.

$400/share @ 25x = S&P $10,000

A link to the full presentation is below.