YWR: Put down the AUM Incineration Shovel

The PE/VC train smash continues to play out as expected.

YWR Megafund Positioning Review 2024

The University Endowment Train Smash

Anatomy of a Private Equity Train Smash

What was initially controversial is slowly gaining acceptance (PE/VC returns will be terrible for the next 10 years).

Institutional investors are experiencing the first signs of this problem. They can’t get their money back. For example, they are putting 4.5x more money into VC funds than they are receiving in distributions.

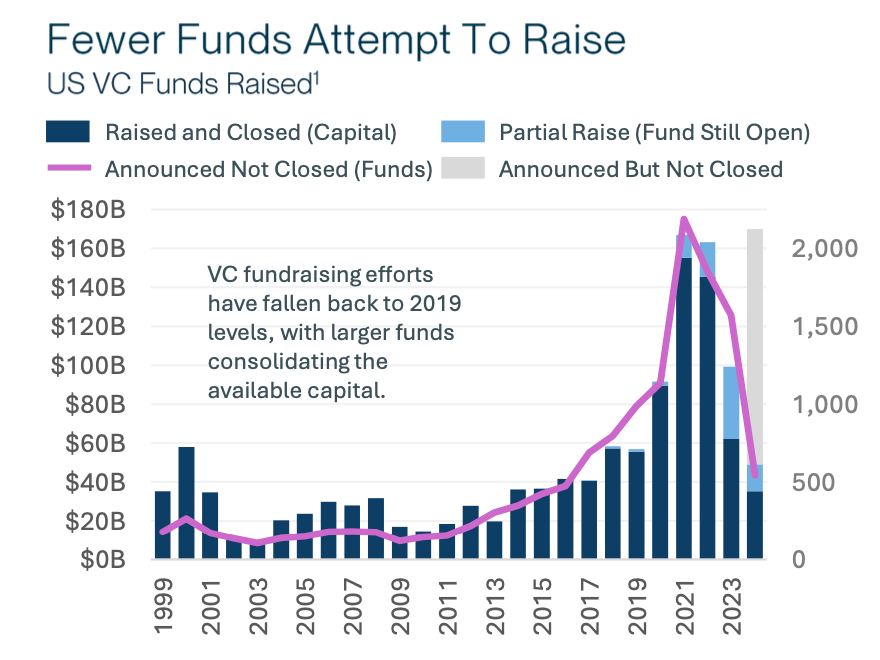

But I’m surprised any new money is going into VC funds. New VC funds raised $35bn in 1H 2024. Why isn’t this # 0?

The 3 Realisations

PE/VC teams at large endowments and pension funds will go through 3 realisations over the next several years.

Realisation #1. Investors haven’t accepted yet how much money they’ve already lost and are going to still lose. Ten years from now the total losses could be 40%, and they will be permanent.

Investors can’t get their money back because there is a mark to market problem. The NAV’s funds are sending out are most likely wrong. Assume the real NAV, where there is liquidity, is -20-30%.

But what’s done is done. The extra damage is what happens next.

When you get a distribution back from a PE/VC fund do not reinvest it back into a new fund (unless legally required and even then try to get out of it), because you are going to lose 25% again on the next fund. The compounding of losing 25% on Great Opportunity Fund 1 and then losing 25% again on Greater Opportunity Fund 2 is why at the end of this these PE/VC allocations will be down 40% and the losses will be permanent.

Over the next 12-24 months greater losses will be realised. 55% of VC portfolio companies have less than 12 months of cash runway. Without new liquidity many of these could be zeros.

An under appreciated imbalance is how many VC funds invested in Seed rounds. There is a scarcity of funds to invest in the Series A. SIVB calls this the Seedpocalypse. Some of this will sort itself out, but it’s part of what’s making it harder for the Seed companies to get more funding.

Realisation #2. Public markets are not going to get ‘better’.

There is so much speculation as to when the IPO market is going to ‘open’ and VC’s can finally unload all their investments on the public. Maybe 2025 will be the year.

While there’s always a small chance the insanity of 2021 will return and pigs will temporarily fly, the base case should be that the market freeze continues. The public market has several structural problems for VC IPO’s.

Problem #1. The death of the active manager. This is a problem of unintended consequences and I encourage investors to always look for this type of problem whenever there is a hot theme or trend everyone is doing. It’s usually why the good ideas don’t work out.

When all the pension funds and endowments were thinking what a good idea it was to index their public equity investments and increase their allocation to privates they never considered the unintended problem down the road of who would be left to buy these private investments when they wanted to exit.

Over the last 10 years almost $3 trillion has shifted from active managers to index funds. In 2024 for the first time ever the share of total AUM managed by index funds exceeded that managed by equity managers.

Life for the active managers is terrible. They have constant outflows and margins are falling. Yes, they can participate in IPO’s, but they need to make room in their portfolio by selling something else, which makes it hard and makes them very sensitive to valuation. And the track record of PE/VC backed IPO’s has not been good. Active fund managers don’t want to be stupid bag holders either.

This brings us to the second reason public markets don’t want VC IPO’s. Valuation. Private investors don’t realise the low valuations in public markets.

My guess is the PE/VC teams at large funds don’t speak to their public equity counterparts. These private investment teams probably live in a silo where they only speak to other PE investors or sales people from PE/VC funds, and only go to conferences with other private markets investors.

Because if I had a PE/VC team I would show them all the ways I could replicate any of their ideas either for free, or with no performance fee using public markets. We highlighted this in Venture Cap Giveaway Weekend.

You like Space-Ex? Yes, I own that for free in Scottish Mortgage Investment Trust. You’ve never heard of SMIT? Let me tell you about it. It’s really cool. It’s a fund where you get all the top tech stocks in the world (with low fees) and then because they are Scottish they are really nice and give you a bunch of private companies too, for free.

You like robotics? Let me check. Yup. I get that for free too. I own Hyundai on a P/E of 5x and it owns Boston Dynamics.

You think Thrive is a good VC fund? And we should invest in it? Let me see…. Oh yes, I got that one for free too. You see RIT Capital gave me a bunch of free VC funds. It’s nice. I don’t even pay attention to them.

I’ve never thought of actually subscribing to a VC fund separately. Do they make you pay performance fees?

You think we should invest in a cool new fund which will build wind farms? Hmmm… I’m not sure. When will it go into production? What will the yields be?

How about we just go the LSE and pick up a basket of renewable funds with 8% dividend yields already? And does the fund you are thinking about charge performance fees? Because these ones don’t.

And consider what the above table means for any renewable company which eventually wants to IPO. That’s the public comp table. I doubt any PE/VC fund is valuing a wind farm or solar park at an 8% dividend yield.

The problem is outside of the MAG7, valuations for most public equity sectors and international markets are at historic lows. It will take an epic rally in public markets to make these VC exits feasible. If the only way to exit a private investment is if public markets go up 100%, then why not invest in public markets? They look way more attractive.

This is why the growth of private secondary funds is so important. The private investing industry has figured out the only way to offload private investments at private investment valuations is to sell them to other private investors. It’s a way for the private investing world to develop their own ecosystem uncontaminated by public market valuations.

Realisation #3: These are bad investments and these funds are bad investors.

Yes, Yale and Stanford made lots of money over the decades in private markets, and that’s what everyone clings to, but something has changed.

I’m generalising but I don’t see PE/VC funds doing cool deals anymore. Instead I see them moronically chasing one cash incinerating bubble after another. And you start to wonder if this is the new model.

Just think of all the hot trends these funds chased which went nowhere.

E-commerce was supposed to be great, but then we see from Prosus that aside from a few established leaders like Amazon, Alibaba and JD.com, the margins are terrible and nobody makes money in it.

Food delivery. That never made sense and has been an investment disaster.

What about all those electric scooters and bikes lying around on the sidewalk? Did those companies work out?

And the crypto startups in 2021 at the top of the crypto bull market?

Edutech?

How are the SAAS things going?

Remember logistics? Remember when the hot thing was to build warehouses? It was a play on e-commerce. How is that working out?

Oh… wait did too much money herd into a hot idea, overbuild, and now vacancies are rising and rents are falling? Seems to be a pattern. Add logistics to office buildings on the list of real estate fund problems.

CBRE Q2 2024 Industrial Review

What about ‘infrastructure’? Another hot theme. Is it bad for all the renewables projects everyone is building if power prices are increasingly negative? I wasn’t sure.

What we learned from Patrick at Total (the Future of Power with Patrick Pouyanne) is that it turns out the key to make money in electric power is to own the whole ecosystem (renewables + gas + trading) and that probably where you are going to make all your money is in power trading. Just owning the wind farm or solar park on its own doesn’t work. But buying shares in Total with a 5% dividend yield would be too easy.

And now datacenters and AI are the new thing. 2 year old AI companies which are already worth over $1bn.

Back to the silos. Do any of the PE/VC teams listen to Baidu conference calls? Has anyone been following what Robin Li calls the ‘Hundred Model War’? Baidu has China’s best AI LLM with over 200 million users and is struggling to figure out how to monetise it. China is always on the front end of these overcapacity train smashes (batteries, solar, EV’s, AI) so it’s good to pay attention to that market.

What Baidu is learning is customers love AI, but you have to mix it with another existing business to make money. For Baidu, AI itself doesn’t make any money, but it boosts the profits in their corporate cloud business. AI also enables their robotaxis business which people seem to like (although the robotaxis don’t make money yet either).

In 3 years we will find out the 2 yr old AI unicorns were slightly overhyped and not good investments. And likely we find that what happened with logistics happens to datacenters too.

‘Pacing’

The questionable practice of continually investing every year into PE/VC no matter what is going on (‘pacing’) is based on the idea that who knows which year will be great, so if the market is soft you keep investing. It resembles the practice of averaging down in public markets, but it’s not. It’s different because in PE/VC you are not averaging down on the same investment.

What I see instead is a perpetual bubble chasing machine. If one theme is soft the fund managers just shift to something else. So you aren’t averaging down on oversold ideas, you are just chasing one bubble after another, which is why there is no end to how much money you can lose.

Really you should put down the shovel and sit this sector out for 10 years. After decades outperformance there is too much money, too many funds, too much hype and it is going to take years to wash out.

If you have to invest in the space one idea might be to find a VC fund which specialises in investing in bubbles that have crashed. For example, that VC fund should now be investing in NFT’s for example. Or, any other sector VC funds use to love, but now hate and can’t exit.

I miss the good ole days

Do you remember when Apollo bought Lyondell on the lows during the financial crisis? Epic. Or do you remember when JC Flowers and Ripplewood bought Long Term Credit Bank in Japan in 2000? Those are the classic PE deals I love. But where are they now?

Why aren’t the PE firms with their hundreds of billions of $’s of dry powder scooping up Chinese real estate, Chinese credit, or taking a UK bank private at 5x earnings, or buying tobacco companies, or offshore drilling companies, or approaching Nestle and Unilever to take over their African consumer businesses? Where are the cool deals?

Why is everyone trying to be a tech investor?

IMHO the way PE firms should play AI is to buy boring businesses at P/E’s of 5x (NatWest), incorporate AI into the business, and then sell it back to the public as an exciting tech company for 12x. It’s not a 10x homerun, but it’s still a good uplift, with divies along the way. Importantly, the exit valuation is low enough so you can IPO it. Just keep doing a bunch of deals like that in massive size while everyone else is chasing 2 year old AI unicorns.

My apologies to the amazing PE/VC funds who have made more money than god over the years. Great job. I’m sorry for this negative view. I’m sure some funds will still do well (the Sequoias and General Atlantic’s of the world). But there are cycles to everything and overall I see a prolonged washout underway. In the end the industry will come out better for it.

Dear YWR, What should I do?

It’s painful, but tell your PE/VC team they have one job. Get your money back. They really need to focus on that.

Then have an open discussion on the investment case for PE/VC. Maybe read this paper from HBS on whether the case for PE/VC even makes sense anymore, or if PE/VC firms have turned into asset gatherers who just care about AUM and don’t really care about performance.

Maybe no new money goes into privates unless it is super non-consensus.

Consider taking the money recovered from the PE/VC funds and reinvesting into value stocks with dividends and ongoing share buybacks.

You can probably make most of your fund’s hurdle rate from high visibility dividends which are also growing because the company is reducing the share count. If growth surprises to the upside and the shares rerate from a PE of 7x to 11x, then that’s a bonus.

This might require shifting resource to build out the direct public equity team or finding disciplined value managers who run segregated accounts targeting the yields you need.

If you need any more ideas please let me know.

Have a good rest of the week.

BTW, I put a link below to the VC presentation by Silicon Valley Bank. It’s also in the YWR Library.