YWR: QARV

Time to review our monthly QARV rankings.

The top of the rankings has too many Chinese stocks, so I filtered China out for you.

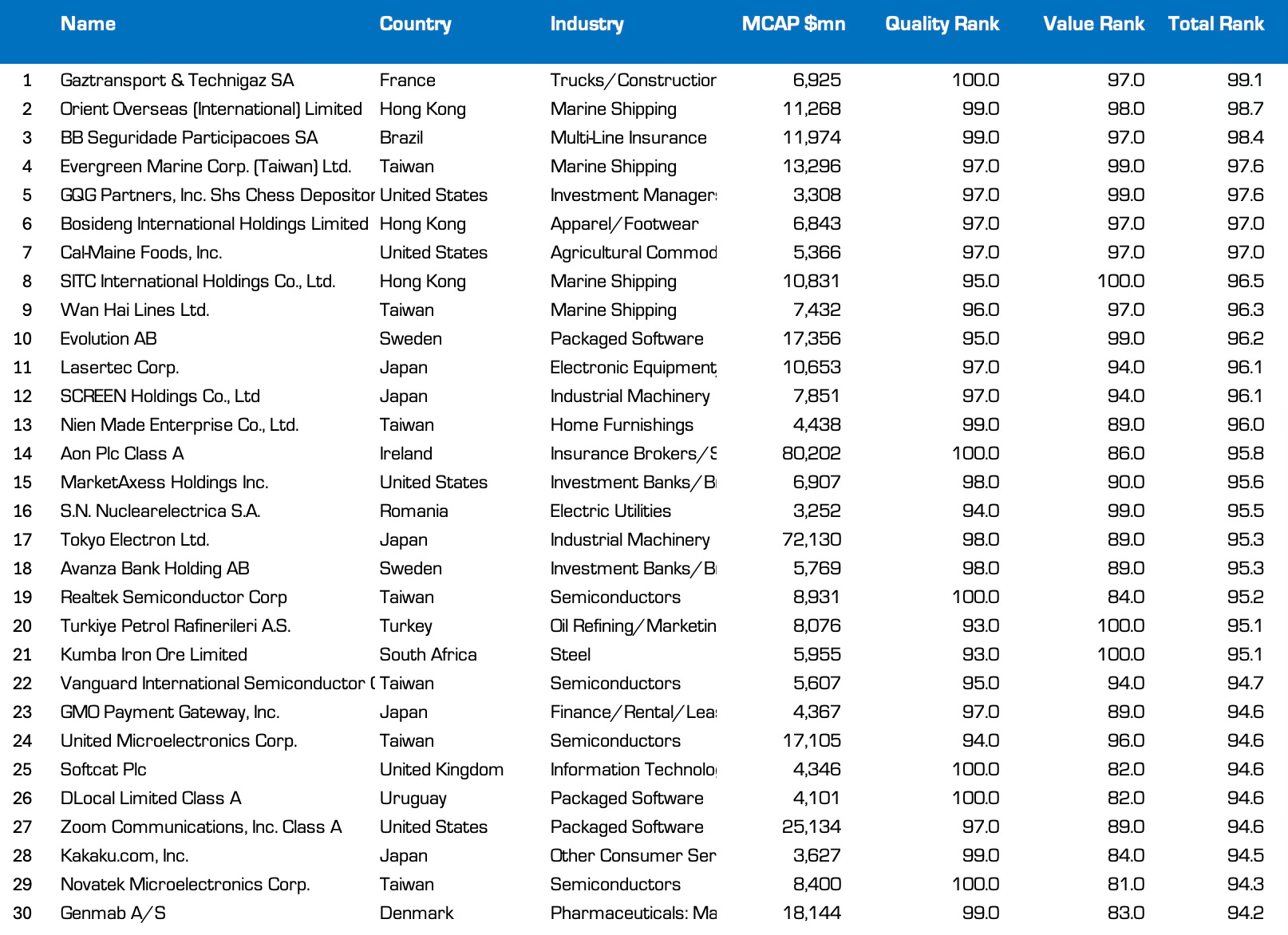

Top 30 Global QARV (without China)

Unlike the Global Factor Model, the QARV rankings don’t change much month to month. The Quality score is based on 5 year average ROE’s, net debt and earnings variability. The value score is more variable, but only 30% of the ranking.

As a result we see persistent themes month to month where companies are generating high ROE’s with low debt, but the market is skeptical and doesn’t want to pay up. The key themes are:

China. Nobody cares about profitable businesses if they are Chinese. Our view is we are in year 1 of a massive China bull market.

Chinese Alcohol: This is still the worst performing sector in China, but screens really well.

Container Shipping: This sector continues to have surprising profitability, but which everyone is convinced is a series of unrepeatable 1-off’s (COVID + Houthis + Inventory build ahead of tariffs). A contrarian view (still under development) is that the diversification of supply chains will increase shipping complexity and keep shipping rates tighter than investors expect. It’s the underlying reason why these events keep creating spikes in the shipping rates.

Taiwanese hardware: The Taiwanese semiconductor supply chain stands out as highly profitable and undervalued. Everyone focuses on Nvidia and the datacenter buildout but misses the whole Taiwanese supply chain behind this. Tokyo Electron and ASML also screen well.

Active Asset Managers: Active management in public equities is dead, but for some reason TROW Price, GQG, Artisan, Alliance Bernstein and Schroders keep generating 20-90% ROE’s and trade on P/E’s of 13x. Everyone wants to own Blackstone and KKR, because that is supposedly where the growth is, but the public equity managers are diversifying their offering and getting into alternatives too.

Iron Ore: Chinese property has crashed and nobody needs iron ore anymore, but for some reason Fortescue, Rio Tinto, Kumba Iron Ore are earning 20% ROE’s with P/E’s of 12x or less.

Brazil: Brazil might be the new China. Nobody cares how much money you make if it’s in Brazil. BB Seguridade, Ambev, B3, Itau and Vale all screen well. Most stocks trade at <10x.

Global Growth: I’d say there is an underlying meta theme. Why do China, Shipping, Iron Ore, Hardware, Brazil…. all stand out if you screen high ROE’s with low valuation? What’s the disconnect? It’s skepticism about global growth. We’re taking a contrarian view on this too.

Links to both the Retool Data app and Google Sheets with the full QARV rankings on over 3,000 global stocks are available at the bottom of the post.

Those are the themes, and we’ve flagged most of them before, but there is one stock which sticks out every time I look at the rankings.