YWR: QARV Nvidia

It’s Friday.

Should we review a top ranked stock from the latest QARV rankings?

Or, should we go over Jensen’s blowout Nvidia GTC keynote?

Amazingly, we get to do both.

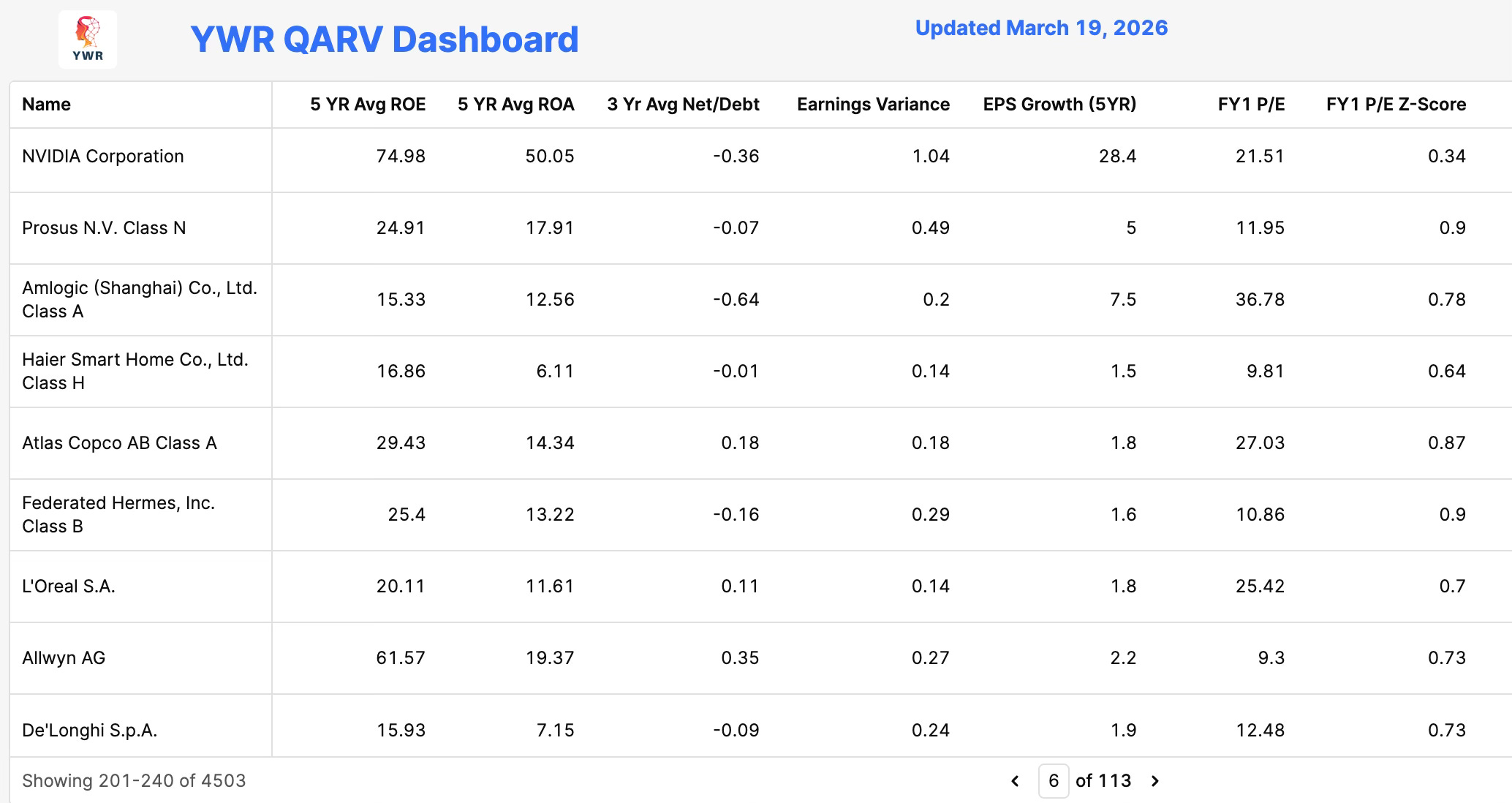

The monthly YWWR QARV rankings screen highlights stocks with a combination of high ROE’s, low debt, earnings consistency, and relatively attractive valuations.

A link to the March QARV rankings dashboard is at the bottom of the post.

The combination of a 7 month consolidation in Nvidia’s share price, while earnings tore a hole in the sky, creates an attractive set up where it ranks #229 out of over 4,000 stocks in QARV.

Nvidia was always high quality with a 5 year average ROE of 75%.

Now it’s good value too.

The 2026 estimated P/E is 21x.

But on to the Nvidia GTC Keynote.

Because these have become must watch events.

There is technological revolution underway and Jensen is happy to tell you exactly how it unfolds.

He is so forthcoming because he locked up Nvidia’s position years ago. There is little his competitors can do at this point. His strategy, as it was with CUDA, is to bring as many large firms as he can into his ecosystem.

Here are my takeaways.

This is not a summary of everything he said, just what occurred to me while I was watching (besides that I’ll probably buy a little more NVDA).

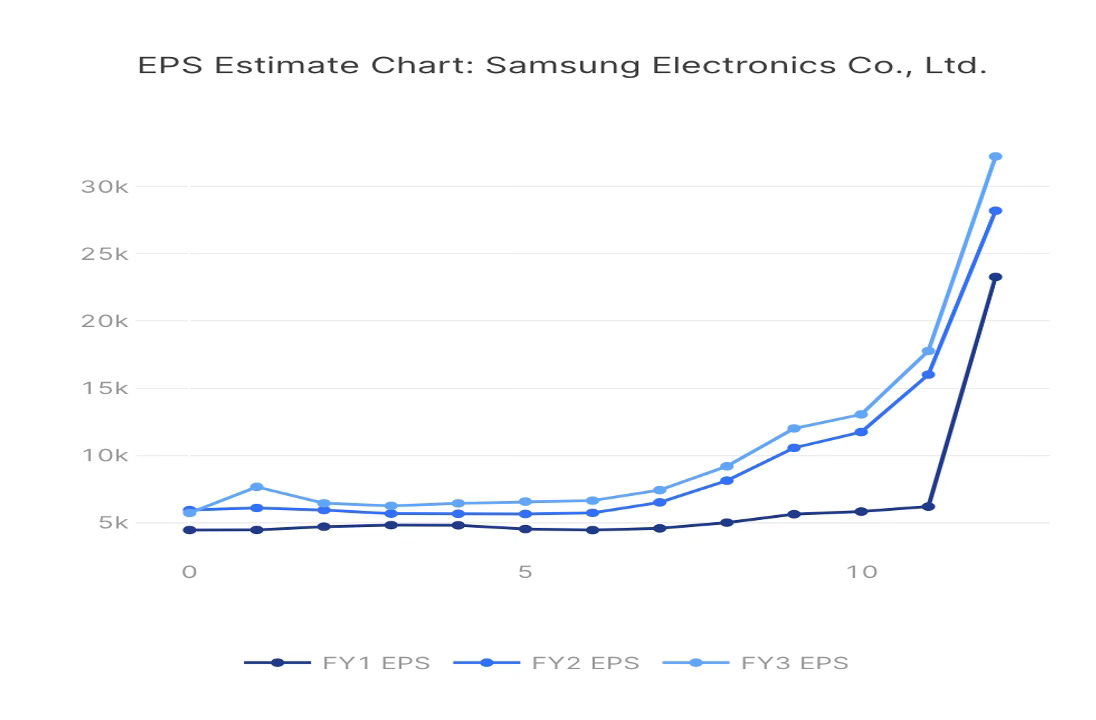

#1 Samsung’s Foundry business could have massive upside: Jensen announced the new GROK chip which uses SRAM for memory (or something like that). Irrational wrote a good, but highly technical summary of how the GROK chip is architected differently and why Nvidia bought GROK. After revealing GROK Jensen thanked Samsung for their good work (1:33:07) ramping up production of GROK chips because Nvidia needs a lot of them.

This is interesting because at the end of 2024 Samsung Foundry was a laughing stock. Samsung Foundry was set up as a separate business line, but had always struggled to get mobile customers because of the conflict with Samsung mobile. Their efficiency yields were also notoriously problematic. Samsung’s problems further reinforced the bull case for TSMC. “Even Samsung can’t figure it out..”

But if Samsung could create a #2 rival to TSMC it would be tremendously valuable. Lot of opportunity, but in early 2025 the foundry business was still money losing, problematic, and had no value in the Samsung share price.

Then in March 2025 Tesla signed a $16.5 billion deal to manufacture chips at the new Samsung fab in Taylor, TX. Musk said he would be personally involved in the processes to make sure it worked. A sign of the skepticism of using Samsung Foundry. The tide is to turning though. Now Nvidia is also using Samsung to manufacture their GROK chips. It tells you there is so much chip business to go around that TSMC can’t handle it all and there is an opening for Samsung Foundry to win high profile deals.

Samsung is trading on 6.5x 2028 estimated earnings because nobody trusts the money they are making on memory chips, but what if by 2028 Samsung also has a world leading foundry business? Could the 2028 EPS be too low and the shares also rerate to 15x because it’s a new mini TSMC? That’s potentially another +100% upside on Samsung. It made me want to buy more EWY.

#2 Are we too negative on Oracle? Jensen explained how AI workflows will be intense users of vectorised databases and how Nvidia is working with Oracle on this. On a micro level I see this myself with the Stevie AI analyst. But it also reminded me of a Founders podcast about Larry Ellison. There was a story about how Larry Ellison saw better than anyone else that the internet was going to massively increase use of databases. At the time Ellison went all-in on positioning Oracle for this. Apparently, that was not an obvious strategy at the time. Now it looks brilliant.

Isn’t Ellison doing the same thing again with AI?

We are hammering Ellison because he seems like he is reacting late to AI, spending a fortune, and killing his current free cashflow. But if we think 5 years out isn’t Ellison doing exactly the right thing to make Oracle one of a handful of leading AI inference firms? Couldn’t Oracle do really well given it is already a firm enterprises already trust. They are already past the gatekeepers.

Ellison is one of the richest people in the world because he keeps seeing things others don't. We should probably bet with him, not against him.

#3 “The storage system is going to get pounded!” (1:35:05) This was one of the most emphatic comments Jensen made over the 2 hours. It stood out. Nvidia is working with enterprise storage companies to make sure storage can keep up with the ever faster GPU’s. Storage is a new bottleneck.

I’ve heard Jensen talk about the need to rearchitect enterprise storage before and every time he mentions he is working with Network Appliance. Coincidentally, NTAP is another highly ranked QARV stock which no one is paying attention to.

Is enterprise storage going to be the new memory? NTAP is trading on 13x forward earnings for 2026.

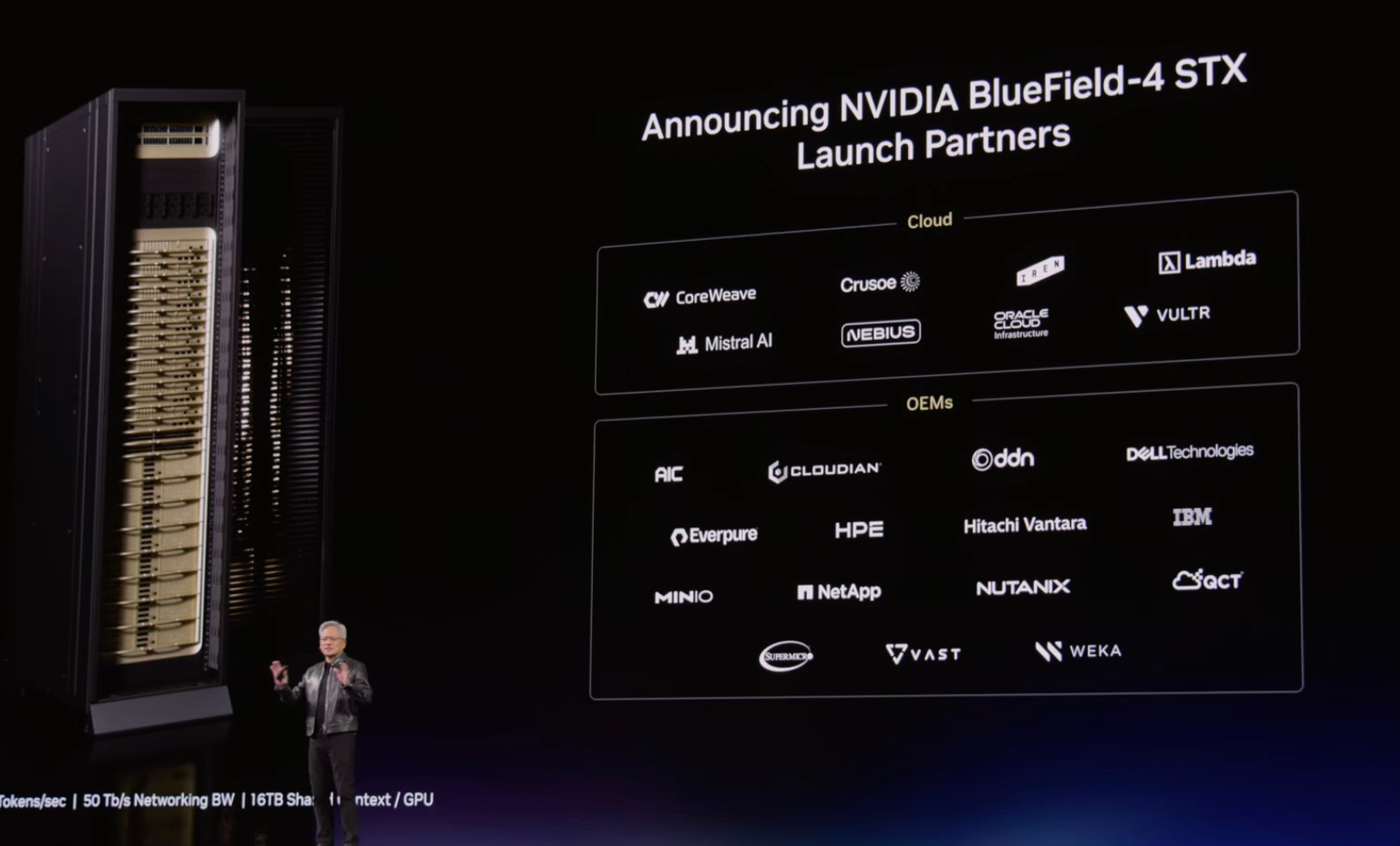

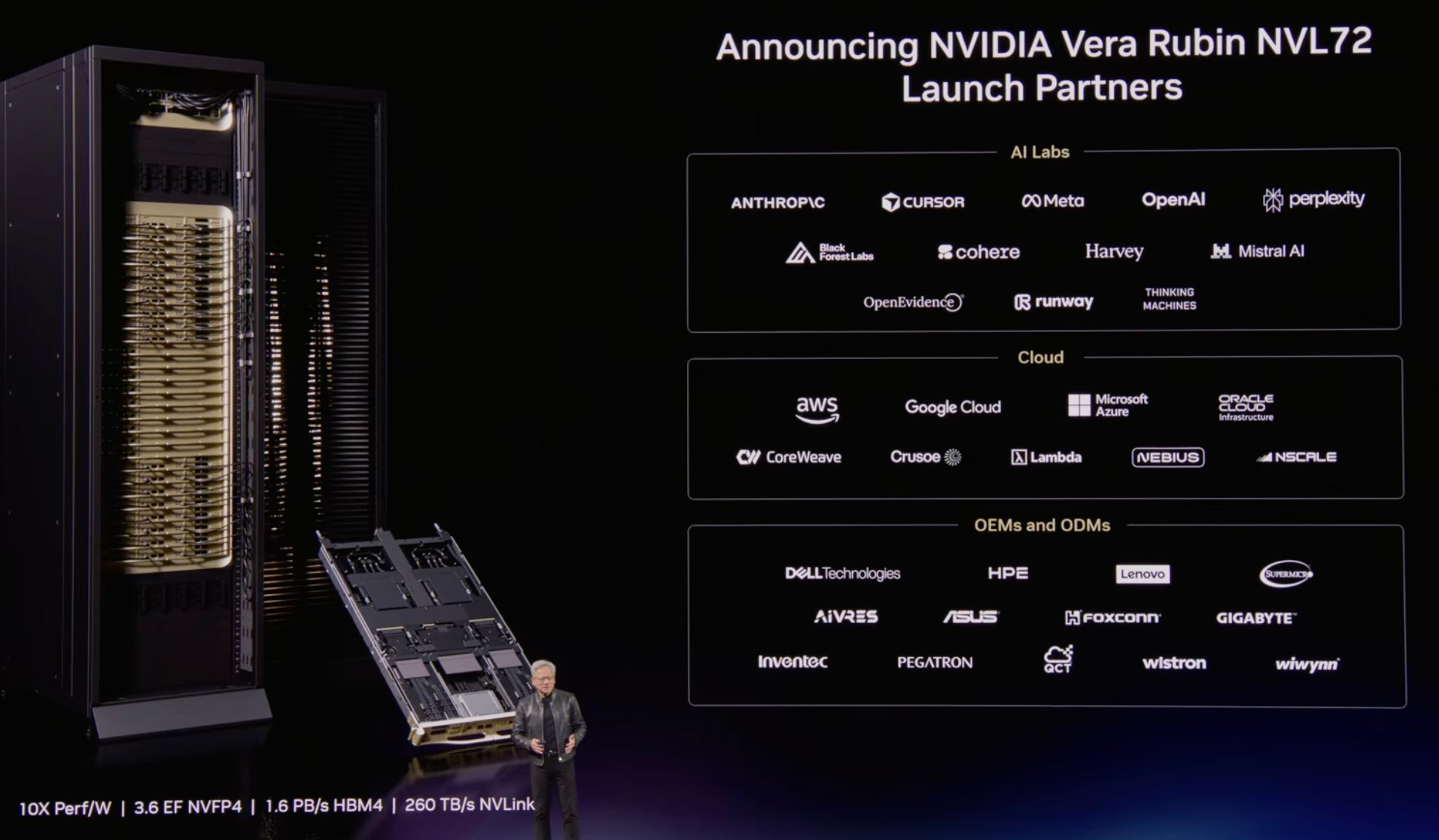

#4 NASDAQ is a geopolitical force: I was looking at Nvidia’s Vera Rubin launch partners and noticing the names. It’s a who’s who of US tech. AWS, Google, Microsoft, Oracle,Hewlett Packard, Dell. It’s a reminder that this world changing AI revolution is dominated by large US tech companies and Taiwanese suppliers. It’s under-appreciated how dominant this ecosystem will become in the years ahead. Like with cloud computing, the whole world will depend on a handful of US firms to ‘think’.

#5 AI is a drug and the invoice is coming: Jensen forecasts Nvidia sales could reach $1 trillion by 2027. That’s an insane amount of money getting spent on chips from one company. Then we saw Amazon, Alphabet and Meta increase their capex estimates 80-100% to invest more in datacenters and chips. Amazon is going to spend $200 billion this year.

Who is going to pay for all of this?

You.

The market is critical of this spending and the current ROI. But I think they miss the strategy. This is the cloud all over again, just bigger. It’s like selling drugs. Keep AI affordable in the early years so firms build AI into their work processes and become dependent on it. Once AI is in their veins gradually ramp up the prices and make back all the investment. I see it myself with how much my AI bill has grown from the free tier to one $20/month subscription with ChatGPT, then to $40/month 2 (Claude + ChatGPT) then upgrading to Claude Pro and keeping ChatGPT ($120/month). From $0 to $120 in 1 year. And probably going higher. Imagine how much companies must be spending?

MAG7 have all derated back to average market multiples. But once MAG7 have hooked corporates on the AI drug won’t they raise prices and grow earnings for years? It’s another reason I think the whole market could be a buying opportunity here.

12m fwd PE rel MSCI US Market

200%

---

Average (+/- 1sd)

180%

160%

140%

120%

100%

80%

2011

2013

2015

2017

2019

2021

2023

2025

UBS")

Those are my takeaways, but I highly recommend taking the time to listen to the full keynote.

I didn’t even go into the part about NemoClaw.

A link to the March QARV Rankings Dashboard on Retool is below.

There is also a link to the rankings on a Google sheet so you can download the data.