YWR: Qatar changes Everything

Everyone’s focused on the rise in oil prices.

Meanwhile, another bull market is unfolding.

A bull market no one is talking about.

US LNG.

And potentially thermal coal.

Director,roll clip of Patrick Pouyanne at the Total Strategy Day, September 2025.

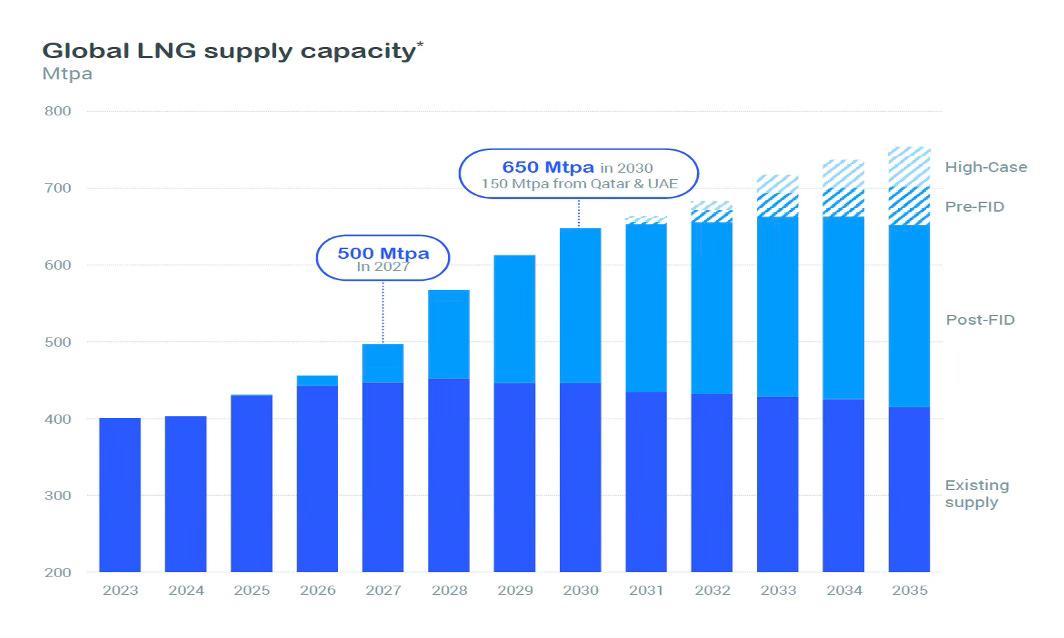

Patrick was positive on Total’s LNG business, but kept reiterating the challenge for the market would be absorbing the upcoming supply wave. Between 2025-2030 global LNG supply would increase from 420 MTPA to 650.

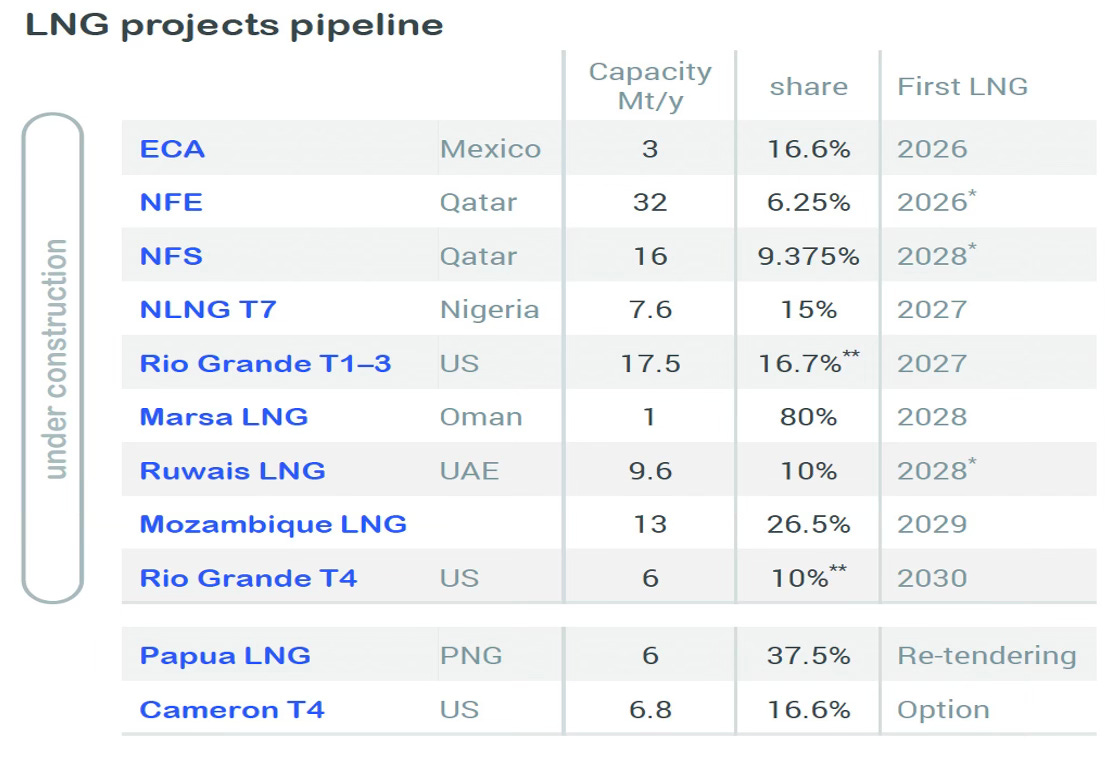

And the biggest source of the new supply was Qatar’s North Field East (NFE) and North Field South (NFS) projects. NFE would bring a massive 32 MTPA in 2026 and NFS another 16 MTPA in 2028.

Side note: Of the 650 MTPA in expected future supply 150 MTPA would from the UAE and Qatar. Supposedly.

Summary: LNG demand from Asia would grow, but the new supply coming on line had it more than covered.

Director. Stop clip.

Fast forward to March 2026.

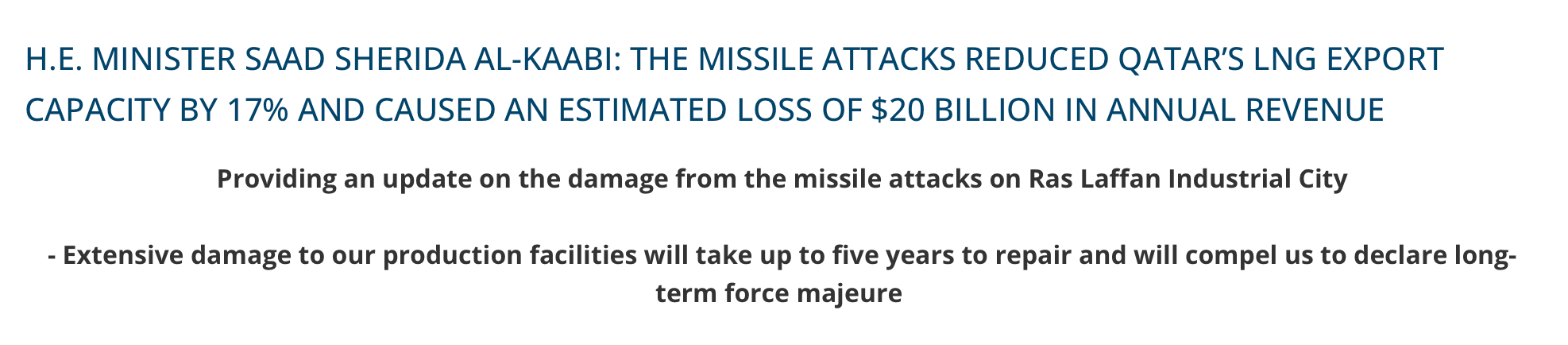

Qatar isn’t adding 32 MTPA, it’s losing 12.

Potentially for 5 years.

And Technip, a major contractor on NFE and NFS, has employees sheltering in place and relocating out of the Gulf.

12 MTPA is 3% of world supply, so manageable.

But a bigger ripple effect will play out over the next 5 years if there are project delays to NFE and NFS.

Because these questions come into play if you are an LNG buyer:

#1. Is this a 1-2 year delay? Instead of 2026-2028, NFE and NFS are completed in 2028-2030? Or will it be longer?

#2. Does the Iran situation get sorted out, or is Persian Gulf LNG structurally high risk?

#3. Do you keep switching from coal to LNG? Or, is it risky to depend so heavily on a complex energy supply chain dominated by the US and the Middle East? Is it better to stick with coal?

Let’s work backwards starting with coal (#3).

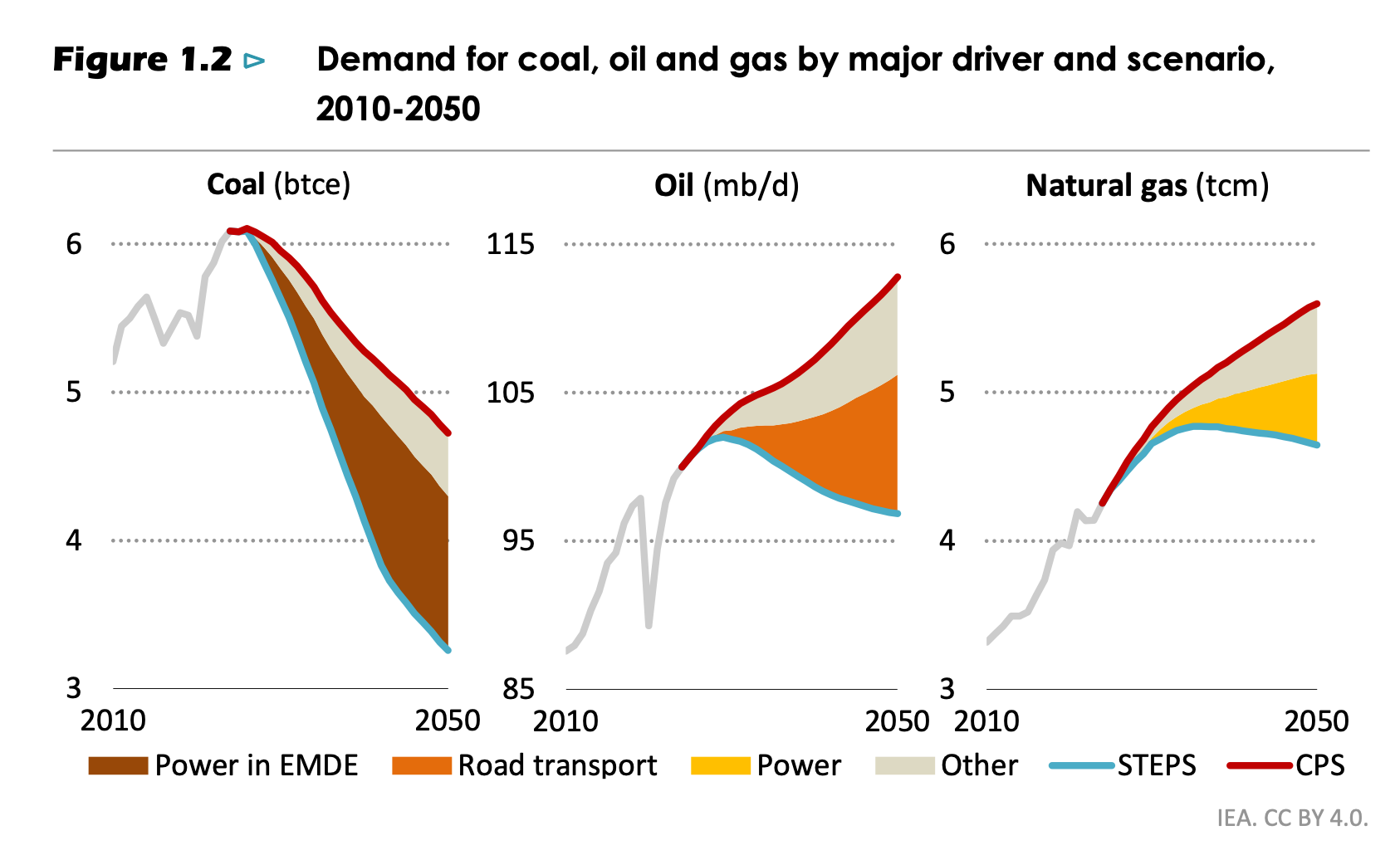

Coal demand was supposed to collapse 25% in the years ahead.

Now it looks increasingly sensible to for a country to keep its energy sources diversified, especially if they have local access to coal. There is still the pressure to shift to gas, but the previous shame and guilt around coal is giving way to practical considerations around energy security.

Coal is also a lot cheaper.

The JKM price of $20/Mmbtu for LNG is equivalent to $300/ton for thermal coal ($135 currently).

We can’t model every investment decision in the world, but existing coal plants likely just got a few more years of life, and the shift to gas moderated slightly, especially for poorer countries.

Is the Persian Gulf structurally higher risk (#2). Yes, and it always has been. What happened this March is the earthquake we’ve all known could happen one day. But the risk was always there. The risk perception will settle down eventually, but for the next 2 years LNG buyers will be wary, and consider US projects instead, even if they could be creating a new concentration risk.

What is the delay to NFS, NFE? (#1)

It depends a lot if the damage to Ras Laffan Industrial City was to standalone LNG trains or includes shared infrastructure which was also supposed to be used for NFS and NFE.

Can new contractors come in and work on everything in parallel and it’s a only 6-12 month delay? Or do NFS, NFE exports make use of infrastructure which will be offline for 2 years?

With the surge in US LNG projects is there spare contracting capacity available to immediately start work in Qatar?

I’m pencilling in that these projects are delayed by 2 years and the first trains start coming on line in 2028.

Now connect the dots.

How do we make money?

Quick public service announcement: I’m not moving to Kenya. The Nairobi Solution is a short story I wrote. I’m sharing a chapter a week. Chapter 1 was last week, Chapter 2 drops Sunday.

US LNG Terminals (LNG,VG,NEXT)

If you are a US LNG terminal trying to sell capacity over the next 3 years the Qatari force majeure is a game changer.

Your worry had been there was too much supply coming at once and it would be a dogfight to get contracts.

Now all of a sudden you are the prettiest girl in town.

First, you have the 12 MTPA of Qatar force majeure demand scrambling to buy on the spot market. If you run a diversified LNG trading business like Shell, Total and BP you can make a lot of money moving cargoes around and selling on spot. But it’s also good for terminal operators like Cheniere who save some capacity sell to the market on spot.

But the more gradual trend, which the market doesn’t seem to give much value is how global LNG buyers will have to shift to the Gulf of America for supply. US LNG really benefits. It has low cost gas, enormous projects, and supply security.

I see three ways US LNG terminal operators might benefit:

Benefit #1: the disruption in Qatar derisks future LNG trains from Cheniere, Venture Global and NextDecade. The biggest supplier in the world is offline with no visibility if/when they can ever deliver.

Benefit #2: does the price of future tolling agreements increase from $3/MMbtu to $5? Do we want exposure to the projects with the most optionality; supposedly ‘risky’ projects like NextDecade?

Benefit #3: Are we underestimating how much the terminal operators are going to make from selling uncommitted volumes into the spot market? These could seem like 1-off gains, but the gains could compound over time if it enables the terminals to pay down debt faster than otherwise, and shift to share buybacks.

Normally, I would want to look at the natural gas producers and play for a rise in 2027 Henry Hub from $3 to $6, like how we would play a gold miner, but strangely, I’m drawn to the terminals instead.

My biggest concern about the terminal trade is that it’s going be long and boring.

The quarterly earning announcements will be dry updates about FID’s, and financing. For long periods of time the stocks will probably do nothing, and the dividend yields are low or non-existent. Meanwhile, everyday there will be lots of excitement around AI and chips competing for our attention.

But if you patient and willing to lock in to owning strategic LNG infrastructure plays for the next 4 years, they could all do really well as the their new capacity comes on line, the cash flows compound and the stocks rerate.

I see three ways to play this and they all look good.