YWR: SGX, an Exchange Masterclass.

A big YWR theme this year is increasing our exposure to Asia (YWR Portfolios). We bought Chinese tech stocks in April then added HKEX + SGX in late September. The idea behind HKEX (Our China FOMO Play) is relatively straight forward, but SGX needs more explaining.

With SGX we are investing for a multi-year recovery in cash equity and equity derivative volumes, but also for the further buildout of SGX as a multi-asset pan-Asia exchange.

Note: Our YWR SGX earnings model is at the bottom of the post.

Pt. 1 The Asian Equity Recovery

SGX is an amazing exchange with great management, but you would have a hard time seeing this from the share price or EPS growth, which has been a CAGR of 8% (2019-2024).

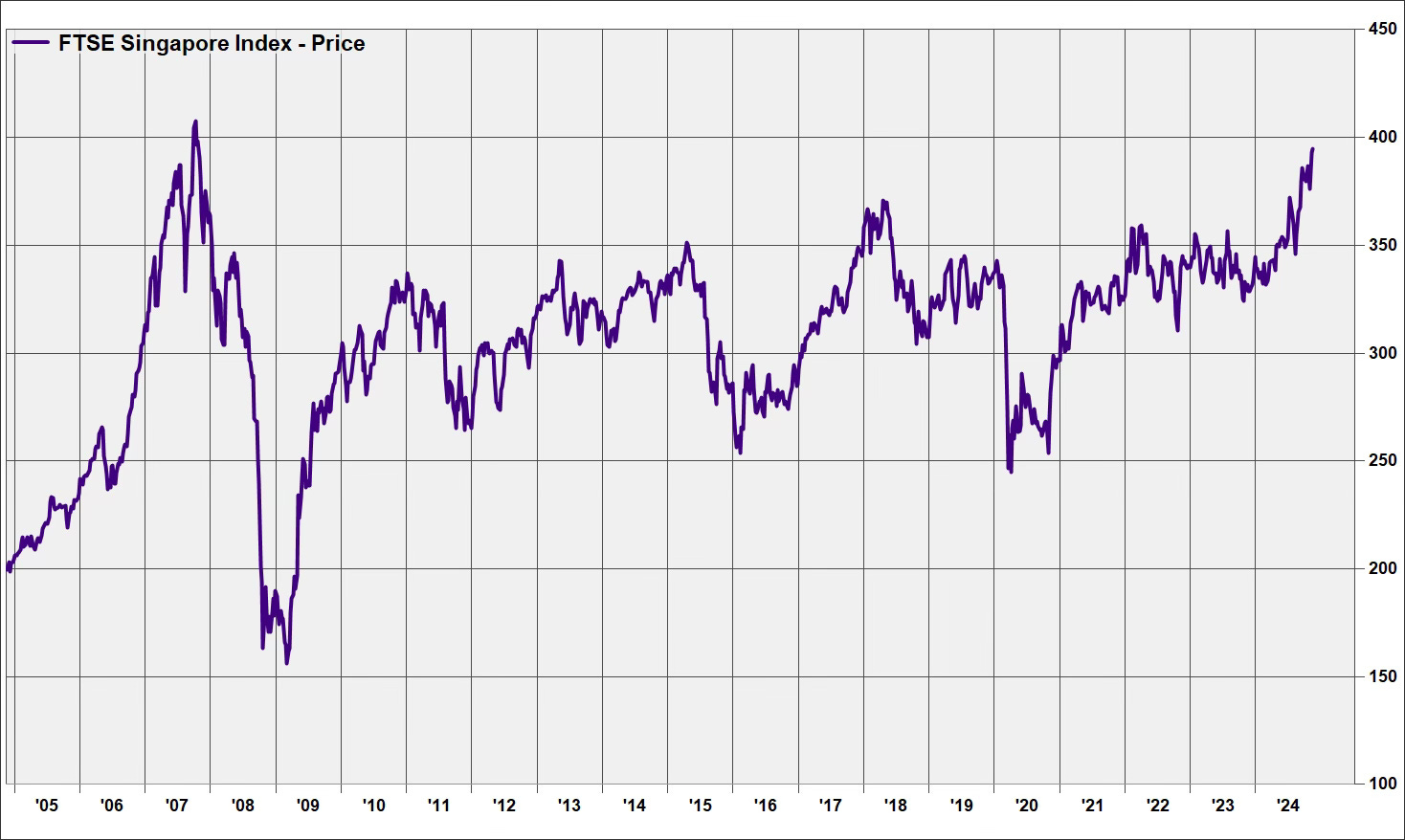

The problem is SGX has been fighting two headwinds. Headwind #1 is the Singapore stock market which has gone nowhere since 2007. Despite the dynamism of Singapore the equity index has been flat for 16 years. Cash equity value traded has been stuck between S$250bn -$300bn and new listings have been scarce too.

A key YWR differentiator is we expect the Singapore stock market is in a new bull market and SGX’s cash equity volumes will recover and make new highs. This is us being bullish on China, Singapore and the whole region. We remember the last Asia bull market and forecast cash equity traded value to potentially exceed $450bn by 2028 as the market rises in price. With improved animal spirits trading velocity increases as well.

Headwind #2 has been Chinese equity derivatives. SGX has a pan-Asia equity derivatives business with futures contracts for China, Japan, India, Taiwan and Singapore. The problem is the China A50 contract is the biggest and volumes have been in a multi-year slump. It’s rare to see equity derivative volumes for an exchange in a multi-year slump, but SGX has been getting dragged down by the China bear market.

Our second differentiated view is that SGX’s China A50 volumes will recover and grow again as the multi-year China bull market unfolds. I said this was a China play. SGX’s Equity Derivatives business returns to growth in 2025 as the A50 picks up while the Nifty 50 is also strong along with MSCI Singapore and MSCI Taiwan.

Pt. 2 The Asian Multi-Access Platform

SGX and HKEX always compete to be the financial center of Asia, but HKEX has the natural advantage of the huge China equity market and investor base in its backyard. HKEX can count on unlimited new equity listings out of China. HKEX can also grow the China fixed income market.

SGX has a harder path. They have to create growth from nothing. They know they can’t depend entirely on the Singapore stock market. Management’s long-time strategy has been to develop SGX into a pan-Asian platform for risk management. They did this with their equity derivatives platform. The idea was “Yes, go buy A-shares in Shenzhen, but come to SGX to hedge it with with A50’s.” Same thing with India. “Go buy cash equities on the NSE, but for proper futures hedging do it in Singapore.”

The next step was to also build out FX and Commodities. In 2013 SGX launched FX futures for IRN, KRW, AUD and SGD. 2013 was also the start of the Iron Ore and Coal futures contract. In 2014 SGX added the RMB/USD and Freight futures contracts. RMB, and Iron Ore have been especially big successes.

Today SGX has built a complementary FX and Commodities derivatives platform where commodity players can hedge the commodity price, the shipping costs and the FX risk all in one place.

The FX and Commodity derivatives have been a big success for SGX and a reason they’ve been able to grow their EPS 8%/year despite the slump in Singapore cash equities and equity derivatives volumes. Volumes for both the RMB/US$ and INR/US$ in particular have a lot of potential to grow in the years ahead.

This FX and Commodities business is also why I say SGX is an Exchange Master Class. Building out this FX and Commodity business has taken consistent work over more than a decade, but now it is a core contributor to the group.

The growth of FX and Commodity derivatives also diversified the SGX business and made it more resilient. Equity related revenues (cash and derivatives) are now 53% or revenues, down from over 75% in 2016. Revenues from data and connectivity for high frequency traders have also been consistently growing.

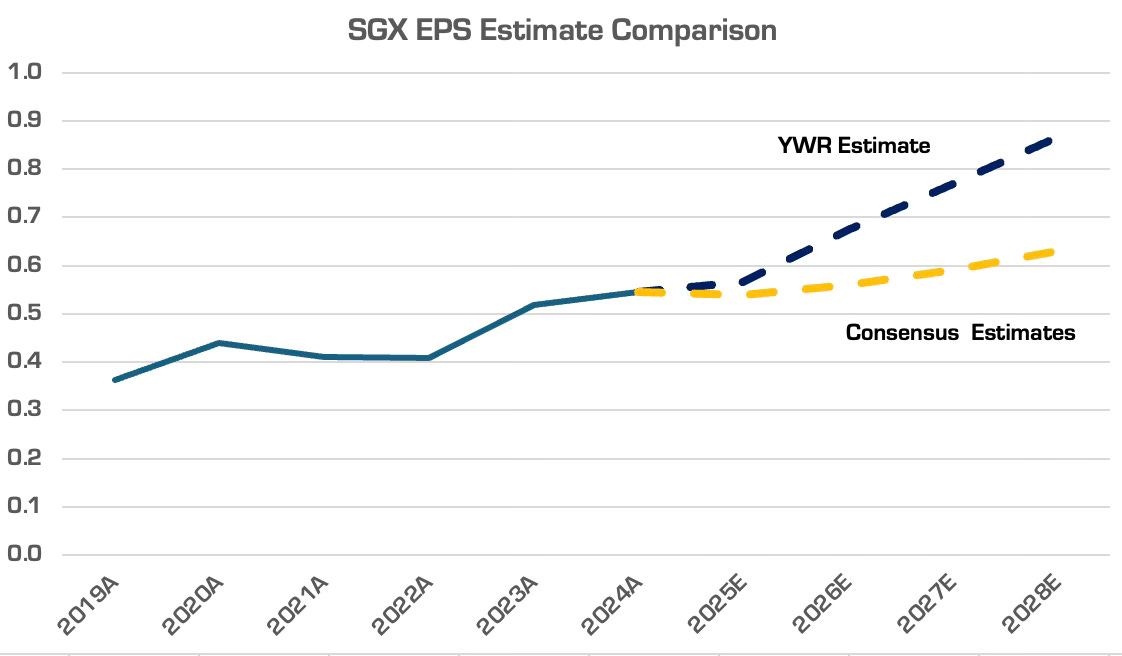

YWR vs Consensus

SGX’s revenue growth has averaged 6% since 2020 and SGX management is so beaten down from the last 16 years that they are guiding that 6% top line growth is a reasonable expectation going forward too. Combine that with 3-4% expense growth and you get pretty boring EPS growth. Which is what consensus is forecasting. In comparison we think this is an inflection point and revenue growth could average 11% (2024-2028) with EPS growth of 12% (and that is without adjusting for the 1-off gain in 2024).

We see a surprise coming as the Singapore cash equity market recovers along with China equity derivative volumes and equity derivatives in general. We remember from 2005-2007 when volumes were continually making new records and we couldn’t upgrade EPS estimates fast enough. The YWR view is that an EPS of 87cts is possible for 2028. Again, a link to the model is at the bottom of the post and also under ‘Data and Models’ on www.ywr.world.

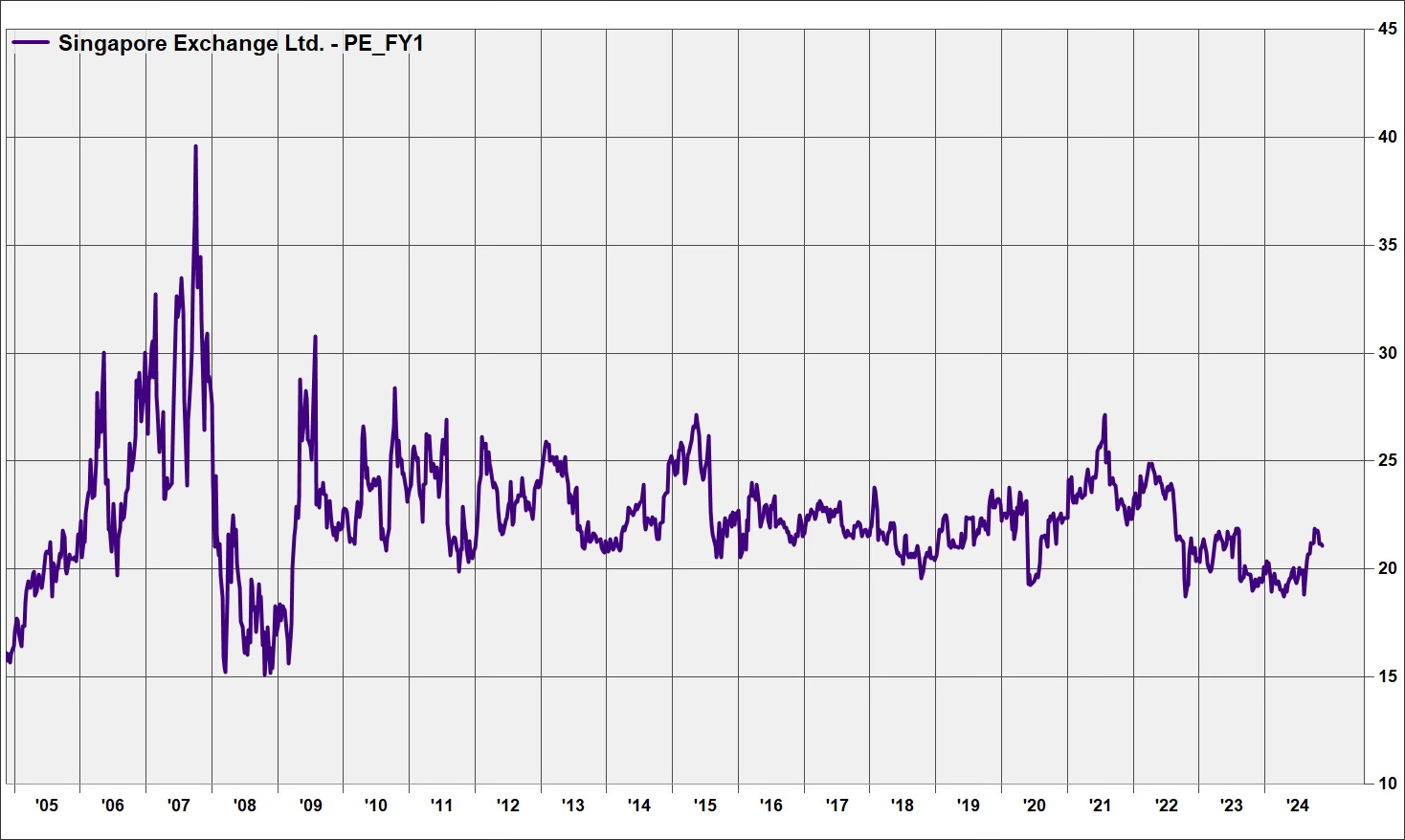

The valuation isn’t a dripping roast with a P/E of 20x, but SGX is a great business, and towards the low-end of its historical range. During a good bull market SGX can trade in the range of 30x forward earnings. IF SGX make the 80ct EPS number in 2028, and the bulls are charging (multiple expansion), the share price could exceed S$20/share. In addition SGX will pay out 50% of earnings in dividends along the way.

It just seems like a business you want to own for a long time.

Below is a link to the:

June 2024 results presentation,

YWR earnings model and

SGX Documentary..