YWR Share Buyback List

I’m joining the view that when it comes to value stocks nobody cares if you’re cheap. You need to be cheap and buying back your own shares!

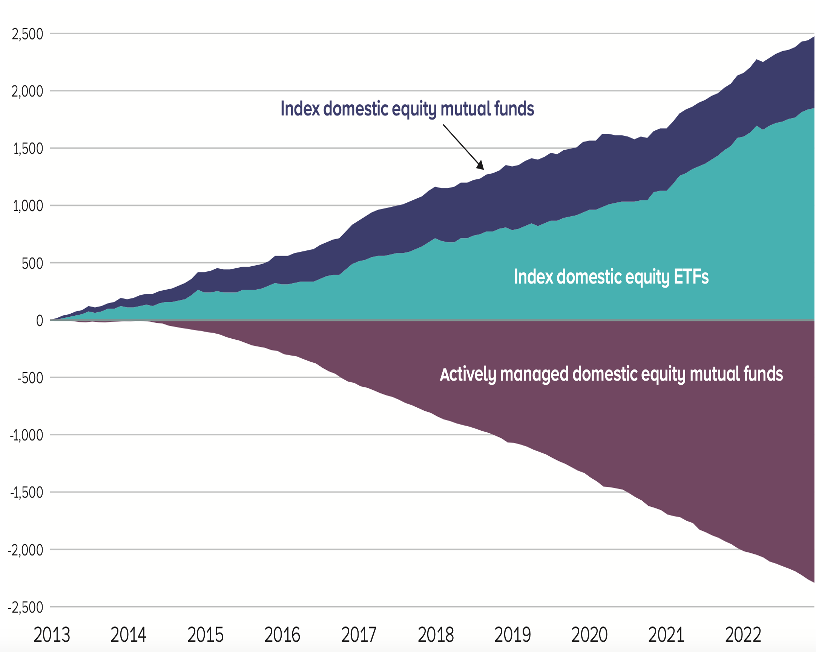

Net fund flows into US equities over the last 3 years are basically $0.

, 08

50 00

Cumulative US Equity Flows (ETF'S and Mutual Funds) 2021 , n 2024")

Within that it is -$2.5 trillion out of active and +$2.5 trillion into passive.

There are reinforcing passive inflows into the largest stocks in the market, and net outflows from everything active managers find attractive (value and small cap stocks).

And now enough is enough.

The investment community has given up that this will ever change. The message to companies is nobody will touch you unless you buyback the shares yourself, and create some kind of a bid.

wrote about this last year in Just Smash the Buybacks. And as usual hits the nail on the head.I’m going to make a special point when it comes to my “basket of deplorables,” or those companies that trade at mind-numbingly cheap valuations as they don’t quite check the ESG box. Look, I think if you trade at less than five times full-cycle cash flow, you should first make sure that you’re de-levered. After that, you should probably plow every last cent into buybacks.

The accretion is just insane, and shareholders are starting to wake up to this fact when they decide which “deplorable” to invest in.

You’re a clunky business that even your shareholders probably wish they weren’t invested in. They only own you because you’re too cheap to ignore. Their biggest worry is that the shares stay cheap indefinitely and their clients yank their money to buy MAG7, since that actually goes up.

Look at some of the coal companies that have bought back huge percentages of the shares outstanding over the past few years. Despite that, they still trade at between two and four times cash flow!! Imagine how much worse the share-price performance would have been without the buybacks?? Guys aren’t selling these coal companies because they’re no longer cheap—they’re the same cash flow multiples that they were a few years ago. Rather, guys are selling because they have redemptions. Just keep taking advantage of this fact, until the situation changes. Smash the buyback button…

Then this week

echoed the view in The Forcing Function for All Assets and The Insensitive Buyer.…. it is simply not enough for active managers to buy woefully cheap public equities in the cyclical value / smallcap / commodity / EM space and wait for Mr Market to magically come to his senses about valuation. Nobody is coming to save you. Everyone is just trying to survive and stay in business.

There is really only one solution to the Value/Small problem — one which Mag7 Tech Bros inadvertently stumbled upon in the aftermath of 2008: you need a price insensitive bid.

The point is this: 4x Ebitda will become 3x, 2x, 1x… The only solution to non-Mag7 and especially Value/Smallcap equity underperformance is for managements to introduce a price-insensitive buyer — the corporate buyback — to offset relentless price-insensitive Active redemption sales that weigh on their share price

The message from the investment community is clear. The only value stocks which which will get any support, will be those with buybacks. As corporates respond and the buybacks become more pervasive it might be the catalyst for value stocks to actually start to work. GM’s monster $10bn buyback is a sign of this.

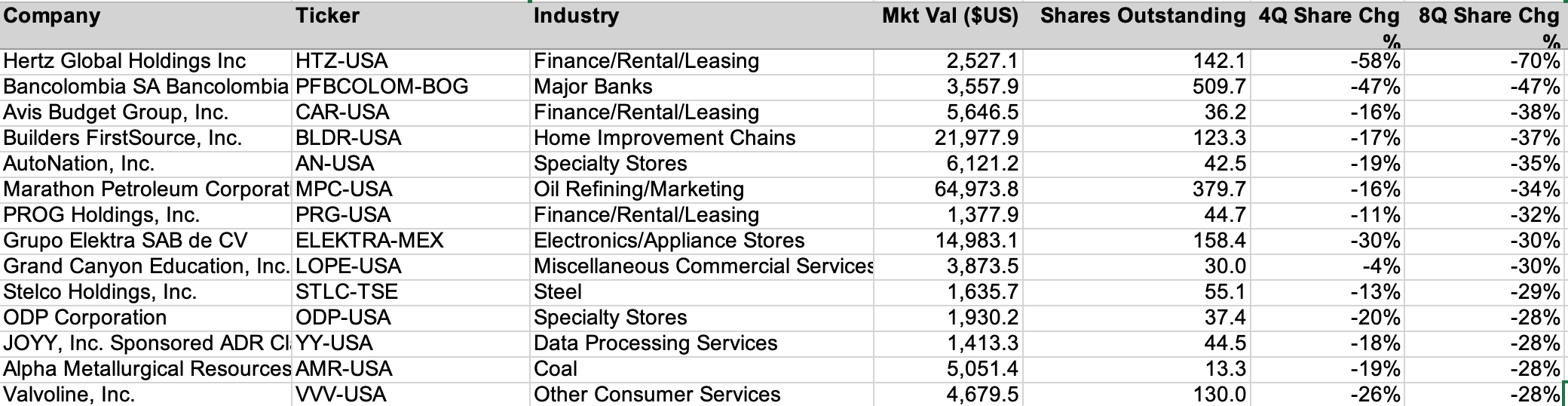

So I’ve screened for stocks globally who have been buying back shares over the last 2 years and sorted them by % change in their share count.

TOP 20 COMPANIES FOR BUYBACKS(Past 8 Quarters)

The European banks don’t make the Top 20 (yet), but they are on the list, and their buybacks will increase after they report 2024 results. Unicredit is #24.

Full Global Buyback List Below: