YWR: Stupidly Bullish

It had been a long day of meetings. But now it was over.

We were checked into our hotel in Del Mar and sitting on the terrace looking out over the beautiful Pacific Ocean.

Time to relax. Just the two of us.

It was a peaceful evening and the sun was sliding down over the horizon. We had a refreshing bottle of white wine between us.

The moment was perfect.

I decided to ask the question.

“Connor?”

“Yes, Erik?”

“In those client meetings today with Capital, Nicolas Applegate and Brandeis; did you really believe the bull case on Swedish machinery stocks you were telling them? I mean aren’t you worried the Chinese property market could crash one day and the effect it would have on commodity prices and industrial machinery orders? Isn’t that a big risk? Or, have you analysed it and it doesn’t affect the Swedish companies?”

Connor paused and sipped his wine before replying.

“You know Erik.. the truth is I have no idea what is going to happen. I have no idea what is going to happen to Chinese property or Swedish machinery stocks. And can I tell you a secret?

Yes, of course!

The secret is I always tell the clients I’m bullish.

You see, I realised a long time ago it’s best to be ‘moderately bullish’. Whenever I speak to clients I tell them a moderately bullish outlook. Not too bullish. Just moderately. Be positive and sensible and that makes everyone happy. It makes the companies I cover happy. It makes the Head of Research happy and it makes the clients happy, because they own the stocks too. I say what everyone wants me to hear.”

For the next 5 minutes I had one of those out of body experiences.

On the outside I was nodding and politely agreeing with Connor on how sensible this was for our careers at the bank. Don’t rock the boat, be moderately bullish, make the Head of Research and the bankers happy.. bla blah bla. How clever and practical.

Inside I was seething. It made me hate my job. Another affirmation that I was shovelling complete nonsense. No wonder the clients never wanted to meet our analysts, answer the phone or return our emails.

So I hated Connor’s answer. Yes, I’m sure Connor’s family was happy that Connor puttered along through life like a sell-side moron, getting on the the tube every morning to Canary Wharf. He would go through life at the bank being ‘moderately bullish’ and not upsetting anyone, but to me it was terrible.

That’s how I felt then.

But years later, and after an unexpected journey to Zimbabwe, I changed my view 180 degrees. Now I realise Connor was right. Like an animal with a survival instinct he had sensed the way, he just didn’t know why. It sounded stupid, but it was right.

And maybe not that stupid.

Equities, Gold, Bitcoin, Real Estate; they’re all the same thing.

We get caught up in Gold vs Bitcoin vs Equities vs Real Estate. It’s fine. Each has their pluses and minuses, each their cycles and constituencies, but at a meta level they’re all the same thing. They are all plays on the growth of debt and currency debasement. You can own all of them.

And as you look at one market after another around the world and through history you see prices in a fiat system never go down. Not for long at least.

Yes, on a 1 year view anything can happen. Maybe there will be a crash. Or, maybe there won't. But like Connor, at any point in time if you had to pick the most statically likely outcome it would be to be moderately bullish. Another strange thing I learned in Zimbabwe is that when you think things are really bad, is when they often go up the most.

So after a long journey, and years of being a cynic and a skeptic, I’ve come too the view that being stupidly bullish risk assets is the most profitable base case scenario.

The Most Expensive Movie in the World

Why do I bring up Connor and the story of being stupidly bullish?

Because in every chat and every investor discussion right now it’s the same. Everyone with their own version of why this is a bubble and a story of how they are prudently ‘reducing risk’. Retail investors are going to get smashed, but they won’t.

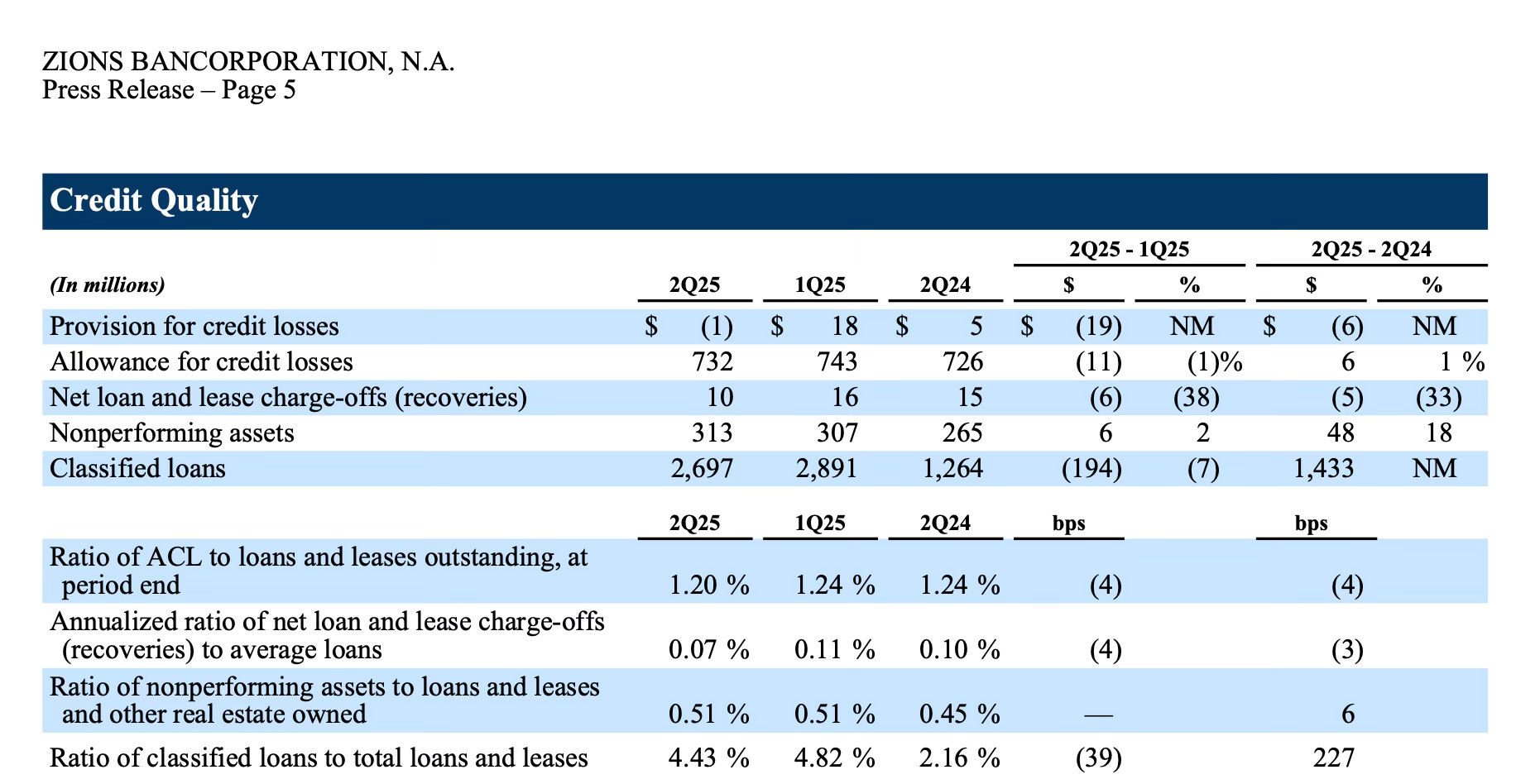

This week everyone is beared up on regional banks (again). Zions lost $50mn on a loan. A loan equal to 0.08% of their loan book. Yes, less than 0.1%. There have been a series of fraudulent loans uncovered and investors are worried these are signs of a bigger problem. The cockroach metaphor.

Yes, it’s scary for 3 fraudulent loans to come up all at once (Tricolor, First Brands and the Zions loan), but rather than it being a systemic problem is it possible that after the Tricolor loan went bad, every bank immediately began scrubbing every loan for irregularities and that is why these disclosures are coming up so quickly? On a practical basis it’s hard to have a systemically high level of loans be fraudulent. Possible, but hard. Bank loan underwriting has been around for a long time, and it’s pretty stringent, which is why private credit is doing so well. If you have an irregular profile and want a risky loan, go to a private credit fund, not a super regulated regional bank.

Which is why I think ‘The Big Short’ is the most expensive movie ever created. Not because it cost a lot to make, but because everyone wants to be Michael Burry all over again. Investors have a bank freak out about everything. The movie is ‘Expensive’ because of how much it has cost investors in lost P&L worrying about a 2008 bank crisis every 18 months.

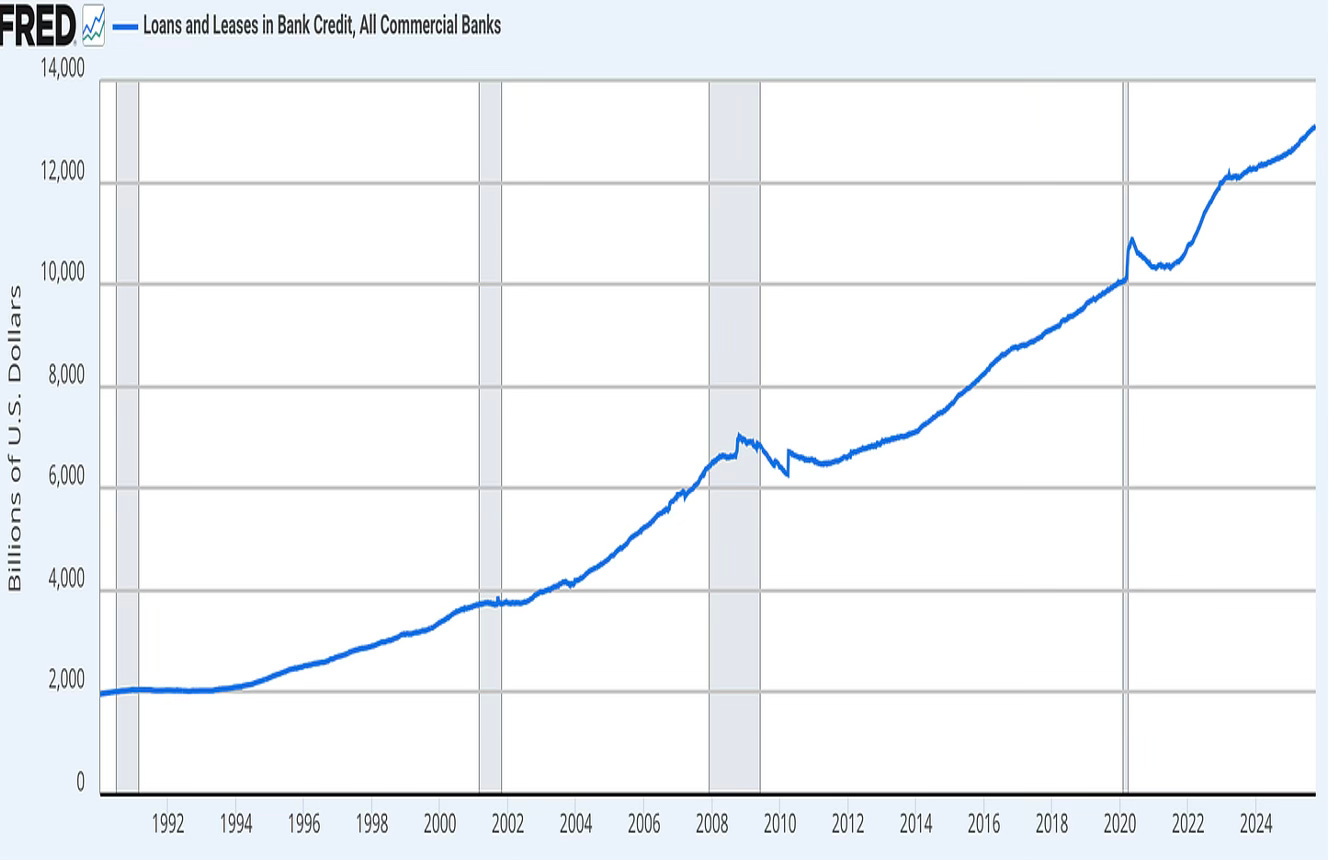

To have a banking crisis… you usually need a lot of credit creation, which we had before the GFC. Over the last 5 years banks have been growing loans and leases at a 5% CAGR. From 2002-2006 loan growth was running at a 10% CAGR.

Yes, anything can happen, but a banking crisis seems like a low probability right now. The banks haven’t been lending aggressively, the Fed is cutting rates, unemployment is super low, wage growth is good, GDP is growing >3% and the whole world is on a US capex spree. NPL’s at Zions are 0.5%. Basically, 0, which is why that $50 million loss was such an aberration and had to be disclosed.

Can I say what’s more likely?

That a real banking boom is still to come.

The Fed is cutting rates in the midst of a boom, and we have this whole initiative to re-industrialise the US.

It’s an economic war and we need data centers, rare earth mines, chip fabs, robot factories… maybe for the sake of the nation the banks are going to join the frenzy and help fund the boom. Maybe that’s Act 2. The credit boom which takes us to $10,000 on the S&P.

In 2030 when banks have been lending their brains out for 5 years then we’ll make a banking crisis call.

Not now.

Today we do something different.

We do the opposite of everyone else.

We look at new money buys.

4 New Money Buys

I’m long up to my eyeballs in European Banks, China Tech, Exchanges, Gold, AI stocks and don’t have any cash, but here’s what looks interesting for small incremental adds.