YWR: Tesla @ $550/share

Disclosure: These are personal views, not investment recommendations to buy or sell a security. For investment advice seek professional help!

Investing in Growth is hard to do.

Growth investing is hard. Hard to do well. It’s easy to get sucked into expensive growth ‘stories’ that don’t work out and you sell on the lows.

But how do you identify a true growth company and have the perspective to hold it for 20 years?

That’s the hardest thing.

How do you know Monster Energy is going to be the best performing company over 20 years by a factor or 2? Or Tractor Supply? How could you know in 2012 that Amazon had a whole new growth leg about to unfold?

What are the common factors?

Here’s my checklist so far. This isn’t all encompassing, and there are exceptions, but they are helpful guidelines.

Founder CEO: A company run by a dynamic founder has a super human advantage over mainstream corporate rivals. Founders are driven in a way other companies aren’t and over time this adds up. Founders are ALWAYS thinking about the business. When Jensen Huang is walking his dog he is thinking about chip design. I didn’t appreciated this enough when I worked at small hedge funds. It wasn’t until I worked inside a mega bank like HSBC that I realised how brain dead large companies can be. Now I appreciate the difference. A controlling family stake with a dynamic Chairman, can have a similar positive effect (Botins with Santander). But a founder/CEO is best.

Innovation is 80% of profitability: If you are going to outperform for 20 years and the stock is going to go up 50,000%, somewhere in there you have to be innovating. It’s why the best performing stocks are usually tech stocks. They started out doing something different. Amazon with online retailing and cloud. Apple with the iPhone. But it doesn’t always have to be a tech innovation. BlackRock innovated with ETF’s. Monster with energy drinks. Just something different and the ability to keep trying new things.

Market share gains: This goes hand in hand with innovation. Usually long-term growth companies take tremendous market share in their industry. Market share gains mean they get the double whammy of increasing scale and profitability. Revenues are growing and profits are growing faster.

Have a Crazy Target: For a growth investor it helps/essential to have a long-term perspective of where things can go over 10 or more years. How big can this be? This is how you stay in the trade. For Amazon it might have been the vision that 20% of all retail sales could one day be online, or with Monster that energy drinks could spread across the entire US (not just California). Or, in the early days of McDonalds that there could be a McDonalds in every town with a Chevy dealership, ie thousands of McDonalds!!! A long-term target makes it clear why you are in the trade and what you are playing for.

An entry point: For me it’s impossible to buy growth stocks when they are doing well and making new highs every day. I need a sell-off, an entry point. And if you are patient some set-back inevitably happens along the way and the stock temporarily falls out of favour. That’s your chance to get into the story. And then stay there.

Tesla checks all the boxes.

Driven founder/CEO. Elon Musk is probably the most innovative/impactful human being ever. Yes. And I say this having initially found him totally annoying in the early days. But I’ve changed 180 degrees. Mrs. YWR has too and she thinks everyone is annoying.

Most innovative company on the planet (electric motors which go 0-60 in 2 sec, bullet proof alloy steel on Cybertruck, autonomous driving, automated manufacturing, low voltage wiring, computer vision, AI chips, battery manufacturing, humanoid robotics…..). What other company is innovating across so many fields. Nobody.

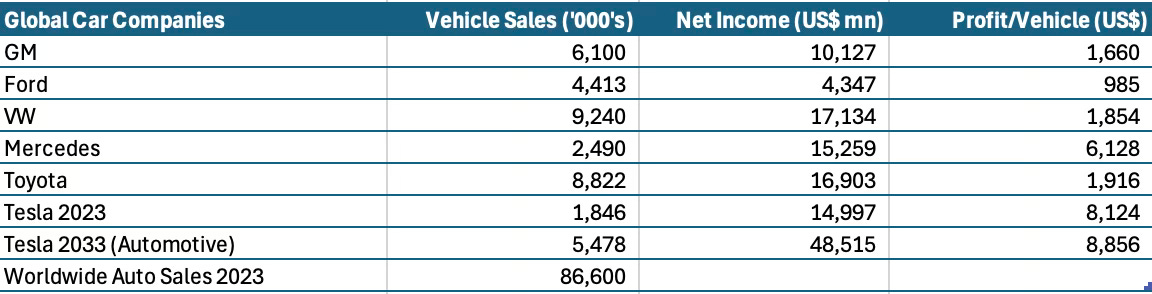

Gaining market share in global auto sales. 0% to 4% in 6 years. That’s amazing. And where can this go in the next 10 years as the Tesla vehicles get even better vs. the competition?

5.5 million vehicle target. Is it crazy to imagine Tesla could sell 5 million vehicle/year? And could it eventually earn $100bn in net income? 5.5 million vehicles (my 2033 target) is 6% global share. What if it’s higher?

We have an entry point. Tesla is currently hated by the asset management industry. Hedge funds are short and mutual funds are underweight.

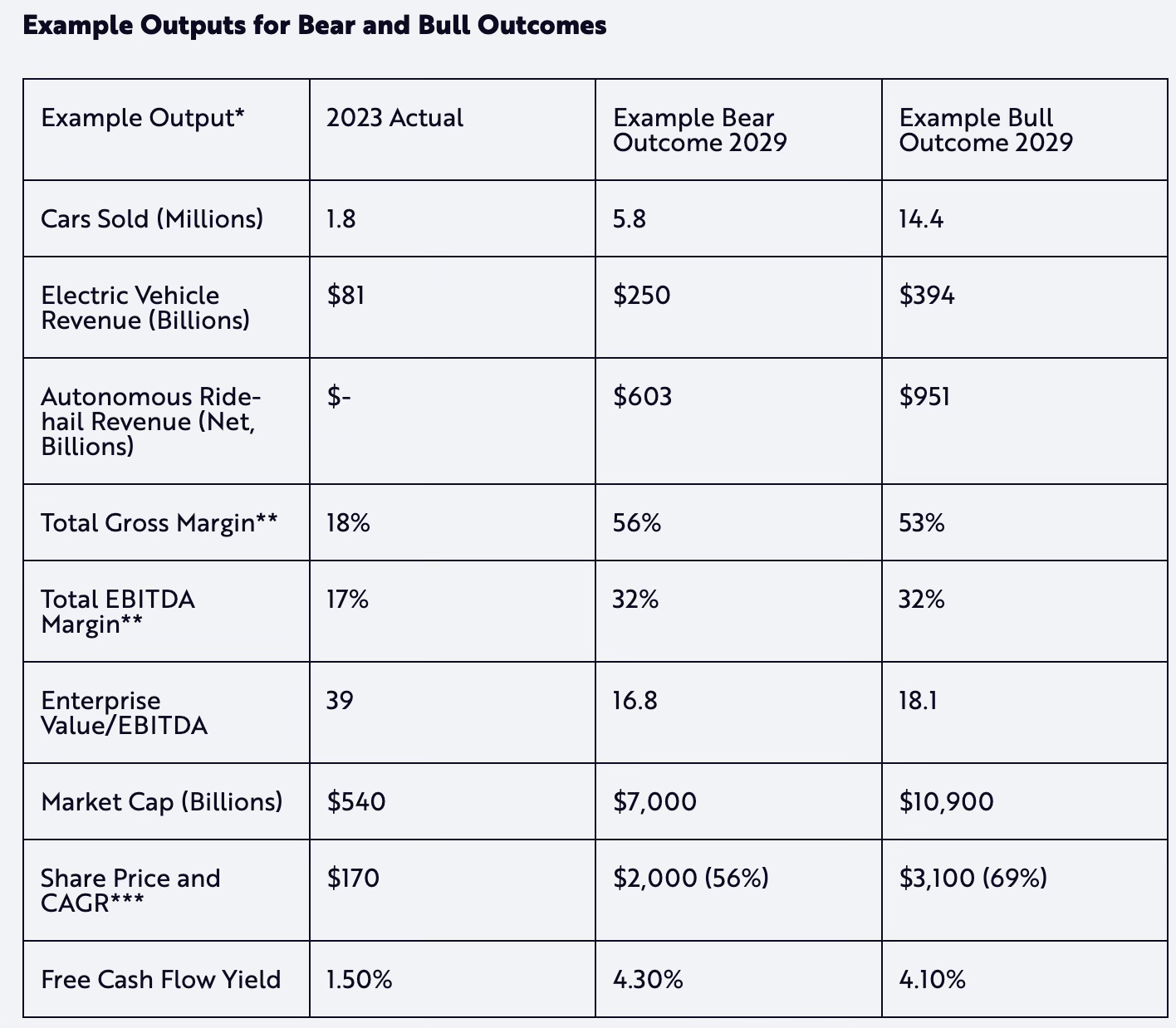

The Road to $550/share in 2033

$550/share, or 120% over 10 years might not seem like much, but the key is it’s something. It’s enough to get us involved. Growth stocks never look like they are going to do 50,000%. But they do.

I started out modelling Tesla with the question of whether it could make $100bn of net income in 2033. Was that possible? If so, then I probably wasn’t going to lose money buying it at a market cap of $780bn.

I can see a path to $83bn of net income in 2033 or an EPS of $22. Put that on 25x and you are over $550/share, plus $300bn of cash on the balance sheet when we get there.

Is this possible? I think so.

Let’s take a step back and appreciate how much Tesla has achieved so far. They went from a startup in Fremont to producing 1.8 million vehicles globally, and earning $12.5bn in 2022. 1.8 million vehicles! Think on that! There was a time when nobody thought Tesla would even survive. Even Musk was worried.

Now Tesla is fully entrenched. Tesla is the most profitable auto company (by profit margins) with $15bn of net cash. The opportunity to kill Tesla has passed. The alien is now going to take over.

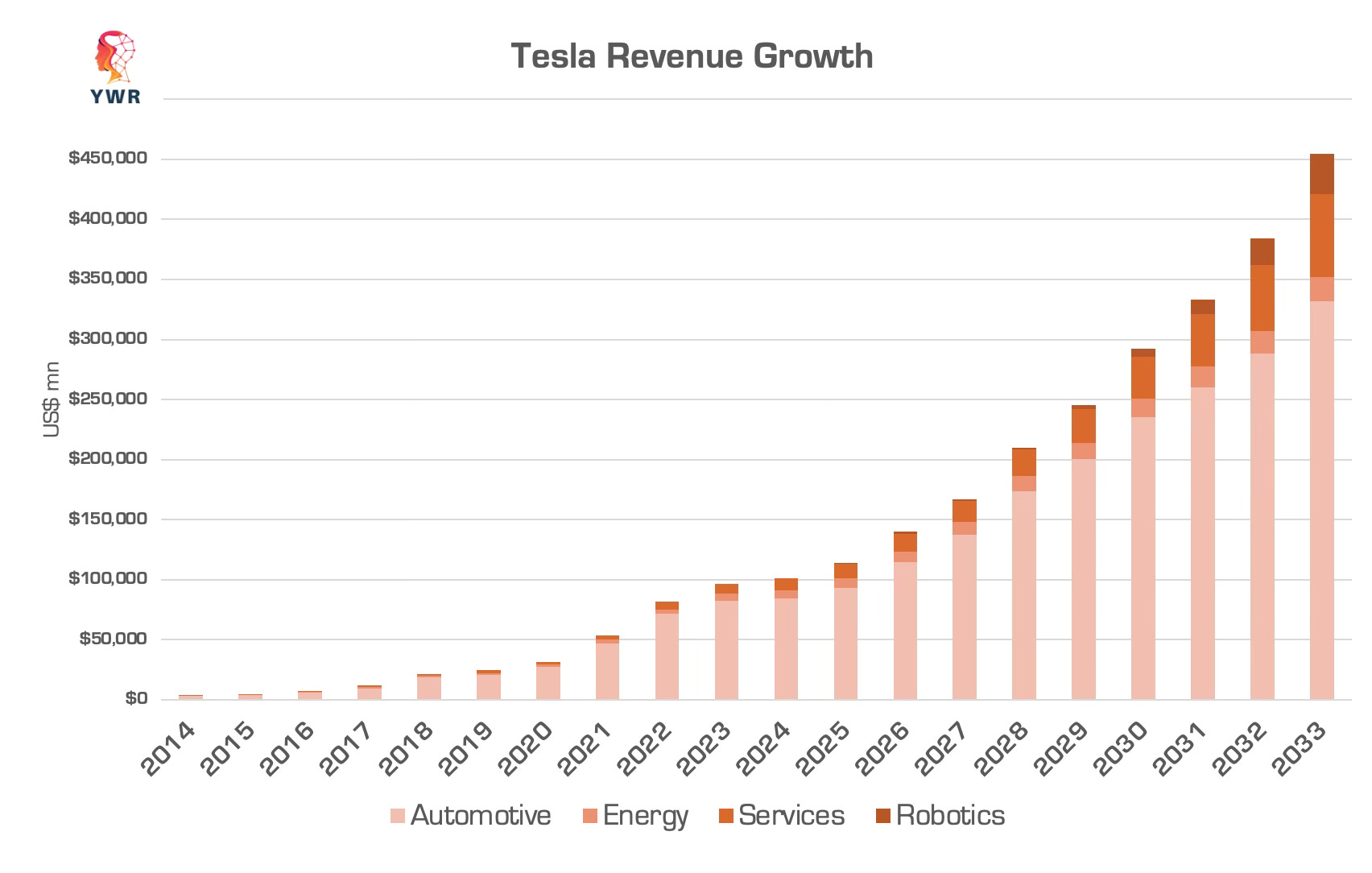

Tesla has 4 major large growth drivers which will play out in the years ahead. And these are just the ones we know about.

Cybertruck is under estimated:

Nobody really talks about the Cybertruck and yet, it could be massive. Americans love trucks. The F-150 sells 750,000/year. The Silverado sells 550,000. Ram sells over 400,000. I’ve put in the model that Tesla sells 180,000 of ‘other vehicles’ in 2033 which includes the Cybertruck.

But Cybertruck could smash the US truck market. Couldn’t the Cybertruck outsell Ram? Totally! It’s cooler and stronger.

Trucks are also the most profitable segment in the industry. It’s not disclosed but most auto analysts suspect ex-trucks Ford is not profitable. Ford makes all its profits with the F Series trucks. If Americans fall in love with the Cybertruck, which they will as they learn to modify it, we are going to have a profit monster on our hands.

RoboTaxi: Cathy Wood thinks this is a massive business line. Maybe… but I’ve only put $10bn of revenues from Robotaxi in 2033. Cathy has it earning $600bn. For me, Tesla is going to capture the profitability of a Robotaxi feature in higher auto sales, leasing and services. It will be like with Apple products. Tesla products work together and so there is a network effect. Tesla vehicles will work better with Robotaxi and so it will be another reason to buy their brand.

Tesla Semi: Commercial vehicles are much more profitable than cars. I have that Tesla Semi gets to 60,000 vehicles in 2033 and could potentially make $1bn based on $18,000/vehicle.

Optimus..where it all comes together

When I think about the next 10 years, robots are a big reason I want to own Tesla. I don’t want to miss this.

If humanoid robots cost $10,000 isn’t that the new iPhone? Won’t every household have to have one? And sure, maybe there are 20 VC startups working on robots, but who has the installed manufacturing base to make them?

When you listen to the early Tesla conference calls a lot of it was about figuring out manufacturing. Those were the tough lessons Tesla had to learn. It’s easy to make a prototype, but really hard to manufacture at scale, globally. But Tesla is already doing this and it’s something nobody else has (except maybe other car companies).

In 2 years analysts are going to have to add a new line to their spreadsheet for robots. I already have.

Robots also build on the Tesla ecosystem, like with Apple. You will have the Tesla car, the Robotaxi app, the charger system in your garage and the robot…

That’s how gross profit margins can expand from 19% to 31% in 2033.

The Texas Factor and Making EV’s cool again.

Musk is relocating Tesla from California to Texas for business reasons, but he will realise a bigger benefit.

Texas is the heart of America. When Texas accepts you it unlocks the rest of the country.

GM realised this back in the 60’s and Toyota realised this with the Tundra pick-up truck. If you want street cred, make it in Texas. And that’s why I’m starting to wonder if the 5 million vehicle target is too low.

Musk also realises something else. You see it with the Cybertruck and you see with Tesla Plaid.

People don’t buy things because they are ‘supposed’ to. They buy things because they are cool and they like it.

Plaid is an S-class EV which rockets 0-60 in 2 seconds! It’s faster than a Porsche. Musk makes you like Plaid because it’s such a cool car, not because it is good for the environment. And that’s how you win.

Same with Cybertruck. He makes it bulletproof. Why? Because why not? In a post apocalyptic world, wouldn’t it be good to have a bulletproof truck? Another reason Cybertruck could be the best selling truck in America.

Below is my earnings model. These are just estimates, and could end up being totally wrong, but a model helps us stop talking in generalities. We can put some numbers around all these products and initiatives.

It also helps us see over the horizon to where Tesla could be in 10 years so we don’t look back and say we missed it.

BTW, all data and models are also available on www.ywr.world.

Have a good weekend!

Erik