YWR: The 7%'ers

Disclosure: These are personal views and market commentary. Definitely not investment recommendations or advice. For that seek professional help.

From: Katie Chen <kchen@utico.org >

Date: 29 August 2023 at 21:42:44 BST

To: Erik @ YWR <erik@ywr.world>

Subject: Asset Allocation Question

Hi Erik,

Loved your email to Tim last week in ‘Investing in Horses’.

Can I ask a question too?

I’m also on the IC for a large endowment.

Why question is this.

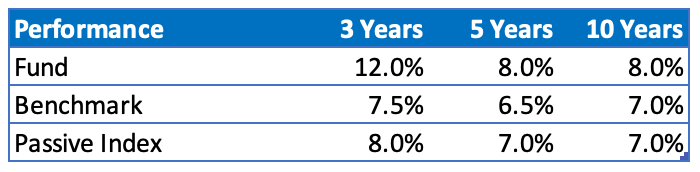

Our fund has been doing pretty well, and we are beating our benchmark, but I’m worried.

We’ve allocated 24% to PE/VC/Private Credit & 30% to public equity, taken lots of risk, and beaten the benchmark, which is great. But given the long period of strong returns, I worry we should have performed better. It won’t take much of a downturn for us to give the outperformance back.

I also worry we have no visibility on our PE and VC investments.

I identified with the CIO in Pine Stone Capital.

We keep investing in PE because the returns have been great with no volatilty. PE + VC have been the biggest contributors to our outperformance the last 5 years. It’s been 20%/year like clockwork, but we have no idea of the current opportunity set.

We just keep doing what we’ve been doing because, well… it’s working, and it’ ‘Blackstone and Carlyle and KKR’. You know..

But what if we and everyone else are now over allocated to Private Equity and returns for the next 10 years are going to be awful?

I didn’t like that chart you showed of all the uninvested cash. $3.7 trillion. It made it seem like all the pension funds are backward looking and piling in at the top of the market. Or maybe this asset class is in a structural growth trend.

Oooof. I hate saying that.

It’s just hard to know.

The problem is our fund has a 7% required return, every year, no matter what. Even if there is a recession. The trustees don’t care. The 7% keeps compounding regardless.

It’s like a Zombie which chases you and never stops. It gives me anxiety attacks.

If PE and VC start to not work we haven’t built up enough of a performance cushion and would quickly fall behind the 7% required return.

So what should we do?

Should we take a break from PE/VC, let it blow up, and come back later when everyone hates it again? Maybe look at distressed secondaries?

Or, should we just stick to the current allocation (what the consultants say) and not monkey with something that’s working?

Or should we be shifting more into value stocks? Or more into bonds?

Sorry for the long question, but would love to hear what you think.

P.S. I’ve attached our current asset allocation and returns.

Thanks,

Katie

From: Erik @ YWR <erik@ywr.world >

Date: 29 August 2023 at 22:25:10 BST

To: Katie Chen <kchen@utico.org>

Subject: Asset Allocation Question

Katie!!!

Hook ‘em horns!

Love the questions. Thank you.

I have the same concerns. Everyone does.

PE and VC feel like investing into a black box. It’s worked so well for so long you just have to wonder. Also, when you see all the big funds increasing their allocations to this space and the record uninvested capital it seems like a yellow flag.

I put together a presentation (Mega Fund Positioning Review) of what the other Mega Funds are doing. You might find it useful. I tried to show how the allocation to PE+VC has been growing. Below is an example from Princeton.

On the positive side the Blackstone’s of the world know you need your 7%, and you’re their bread and butter, so they should be trying hard to get you that 7%. On the other hand they’re always going to say the opportunities are great to collect more fees.

And those fees are really going to be a drag if the market gets tough.

But there is an opportunity for you.

You need 7% returns?

Europe, HK and Emerging Markets are full of big cap stocks with 7% dividend yields. These are big liquid stocks with 7% dividends which will probably grow, so the return could be much more than 7%.

Here is a table to give you an idea of what’s on offer. It’s Big Energy, Autos, Banks, Tobacco, Telcos, China; basically all the YWR Untouchables we’ve been writing about.

Did you know a 7% dividend yield stock which grows the dividend 4%/year mathematically generates a 50% total return over 5 years or 8.6% compounded?

Here’s another idea.

With the sell-off in bonds it gives you the entry point to increase your fixed income allocation.

Sit back and earn 7% on bonds. Imagine that.

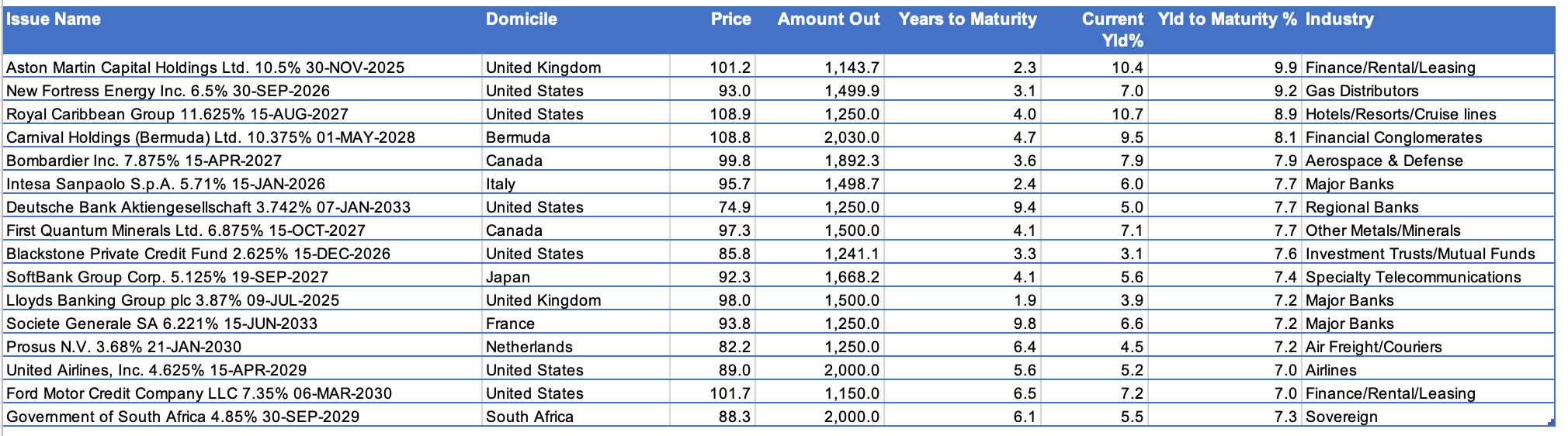

Here’s a sample of benchmark issue short to medium duration bonds with 7% yields in $’s. Again, lots of European Banks.

I’ve attached a spreadsheet below with 197 equities and over 200 bonds with yields over 7%. I hope this helps.

Have a good weekend!

Erik

P.S. Here is the 7% bond and equity database: