YWR: The AngloGold Turnaround

Disclosure: These are personal views, not investment recommendations to buy or sell a security. For investment advice seek professional help.

Director, roll clip of Hugh Hendry in St. Barts.

https://twitter.com/hendry_hugh/status/1783253669686763736

Oooof. That’s not going to age well.

But what do you see?

Hugh, a legend in his time, sitting around on the beach giving 100% backward looking advice on the gold miners at exactly the wrong time.

Factually, he’s correct. They’ve been terrible. Terrible for 13 years. And it’s hard for almost anyone to see past that.

But this whole interview has value.

The tone. Having drinks on the beach while imparting wisdom to gold mining investors without any actual work. It all tells us something.

It tells us gold miners are about to rip a hole in the roof.

And what do you see at the end of the clip? Hugh wants to show everyone his ‘office’, which is a beachside table at the restaurant.

Hugh’s beachside ‘office’ tells you how much work is being done on the sector and how much he is paying attention to AngloGold CEO Alberto Calderon’s improvements in monthly ore processing at Obuasi.

The old Hugh, the London Hugh would have known the numbers.

Oh well.

I don’t want to pick on Hugh though. Usually he’s great.

Here’s another dose of financial wisdom from the peanut gallery.

Newmont was +12% after these ‘terrible’ results.

Alberto and Hugh are saying you can buy gold, but definitely don’t buy a gold miner. The argument that miners are ‘beta’ to the gold price never works. It’s just something you tell Doomer Gold Bugs to do capital raises and sell tickets to mining conferences.

Buy the Epic Gold Miner pullback.

I want to reiterate the call we made back in March to Buy the Epic Opportunity in Gold and Gold Miners.

The negativity from Alberto and Hugh, and the way gold miners sold off 3X the gold price on Monday when WW3 didn’t start is a sign nobody trusts these stocks to work. This is how it feels at the beginning of a trend. Lots of volatility.

But enough contrarianess. Let’s get into the weeds a little with one miner in particular that I think is going to work.

AngloGold Ashanti.

Alberto Calderon and the AngloGold Turnaround

I’ve followed AngloGold for a long time, and it’s been a mess. Mark Bristow at RandGold did due diligence on AngloGold in 2015, but decided everything was in such bad shape they weren’t interested.

Mark probably made a good call. From 2015 onwards operations struggled and production fell from 3.9 million ounces to just 3.3 million in 2019.

Then in 2020 AngloGold sold its South African mines to Harmony in what seemed like a terrible transaction. This sale took group production down to 2.6 million.

The future looked bleak Everything AngloGold touched turned to lead. They couldn’t run anything. AngloGold would just shrink with every new ‘strategic review’.

Then in 2022 AngloGold brought in a new CEO, Alberto Calderon. No reason to take any notice at the time. Probably just another dead body in a long line of failing CEO’s.

But then Alberto started to make moves.

It got my attention when he moved the HQ from Johannesburg to Denver and made the NYSE the company’s primary listing. Denver is a gold town. Newmont is in Denver. I liked that.

AngloGold was rebranding itself as more of a US business.

The goal was to close AngloGold’s discount to the majors (Newmont and Barrick).

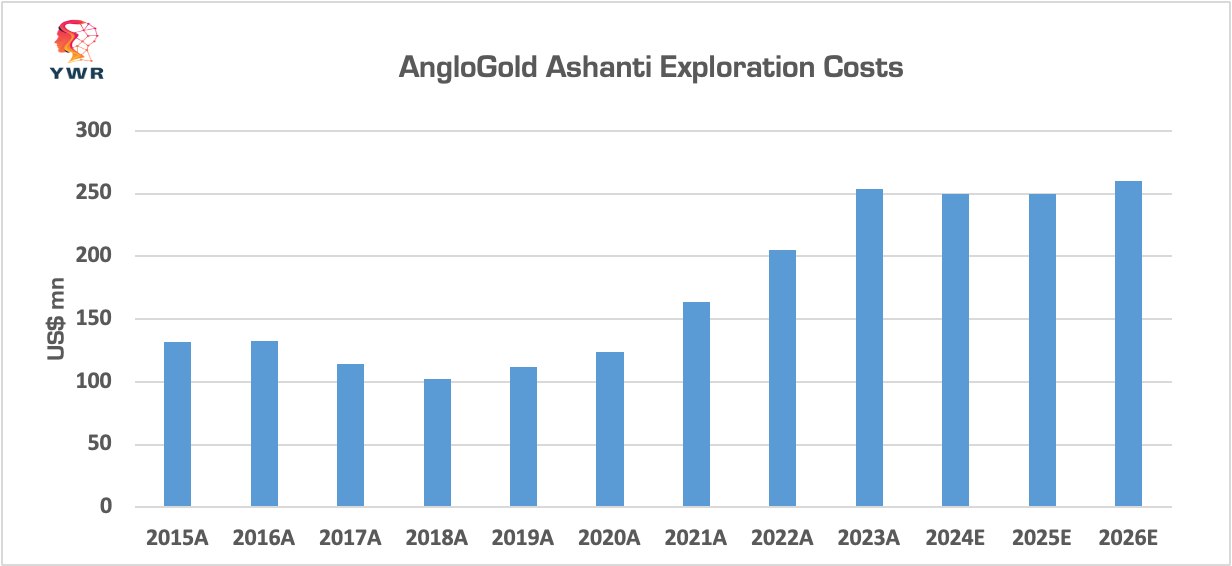

Alberto also stepped up investment in exploration. Exploration spend went up from $130mn to over $200mn. It was a risky move, but Alberto’s view was ‘No more death spiral’.

They had to grow again. And they had to find some gold.

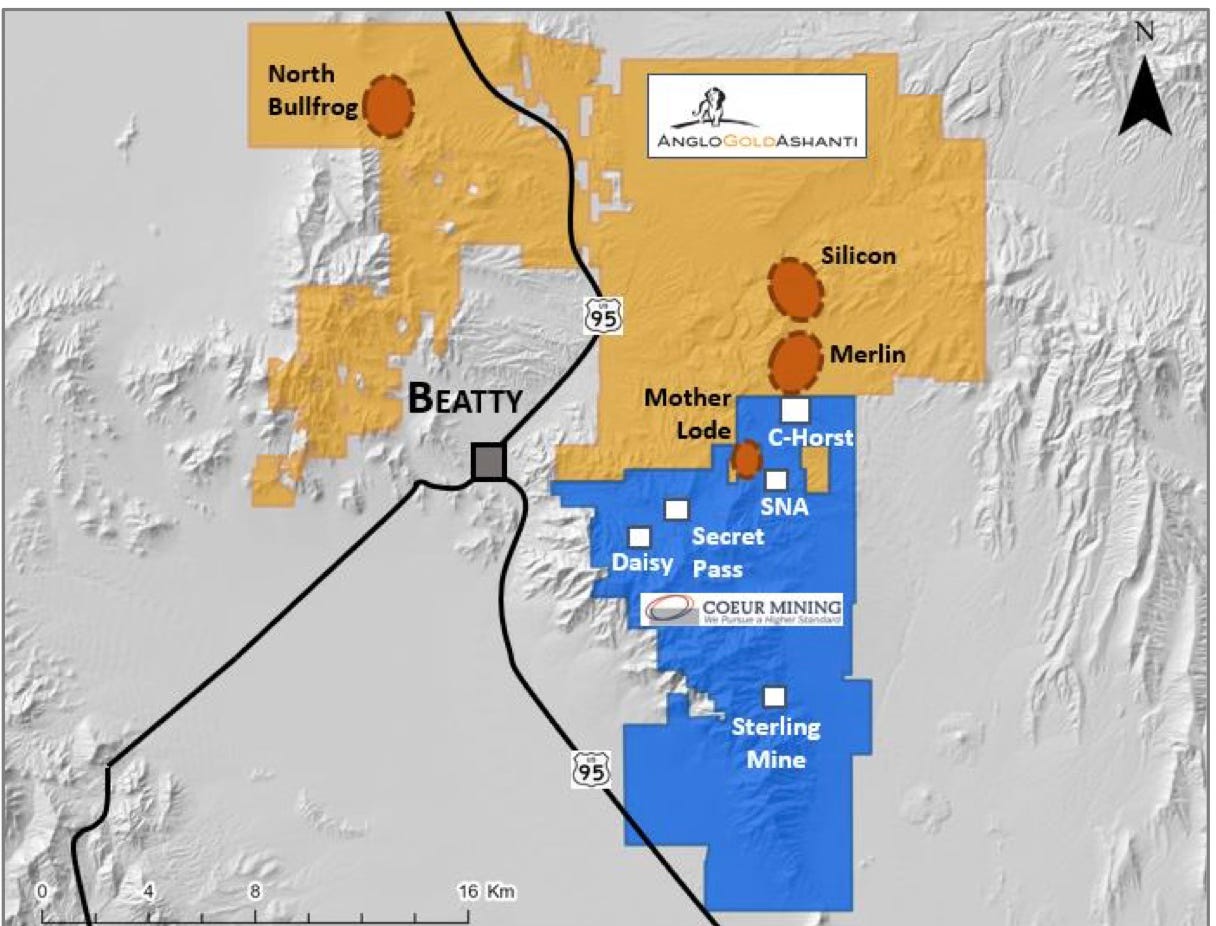

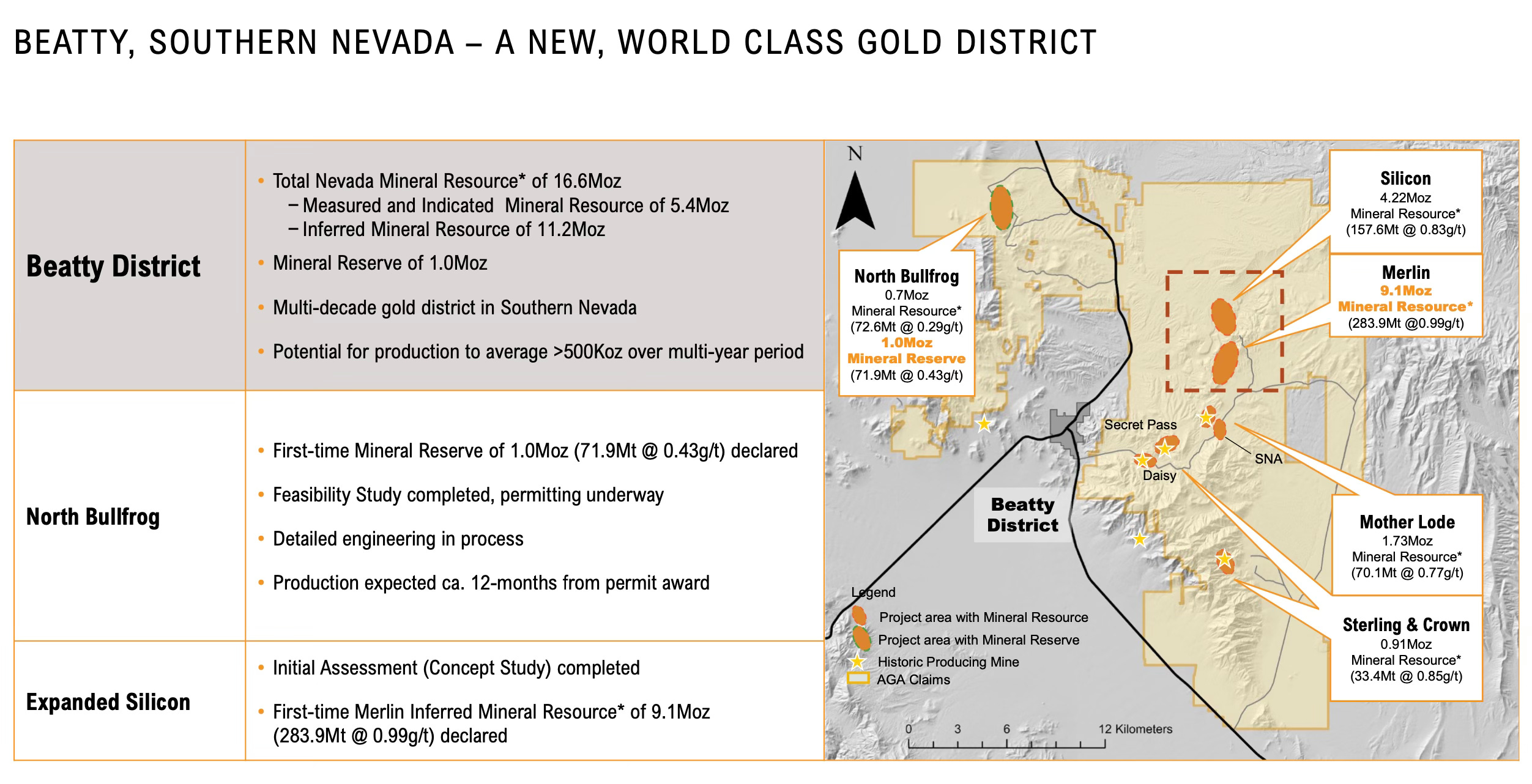

Alberto would focus exploration on Nevada. A Nevada mine would provide AngloGold consistent operations in a stable jurisdiction. Something they didn’t have, but which Newmont and Barrick did. It would also strengthen the ‘Made in the USA’ rebranding.

To speed along the Nevada strategy Alberto would also spend $500mn acquiring 2 junior gold explorers with projects adjacent to AngloGold in the Beatty gold district. Paying out $500mn was another bold move given the shape they were in.

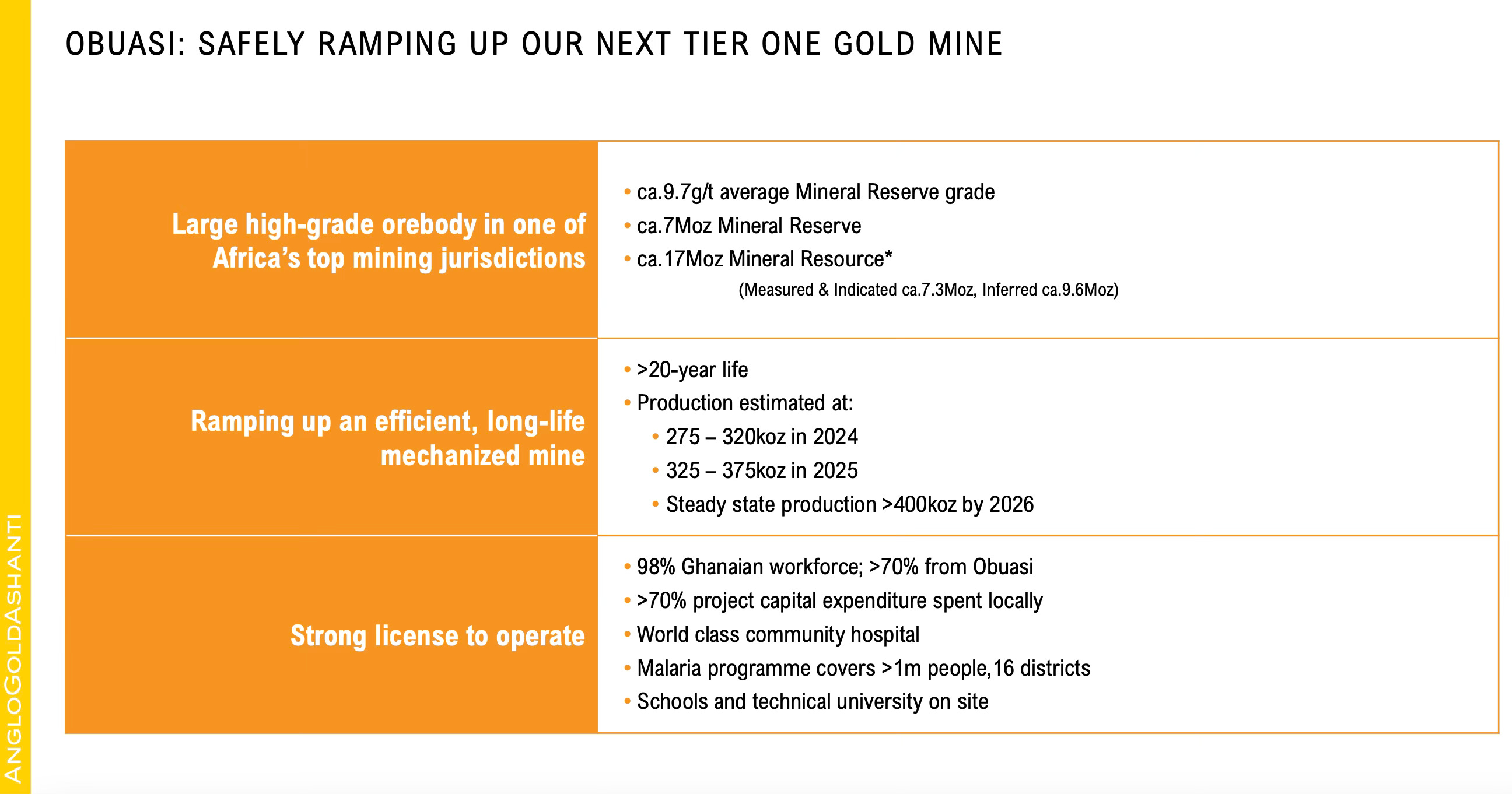

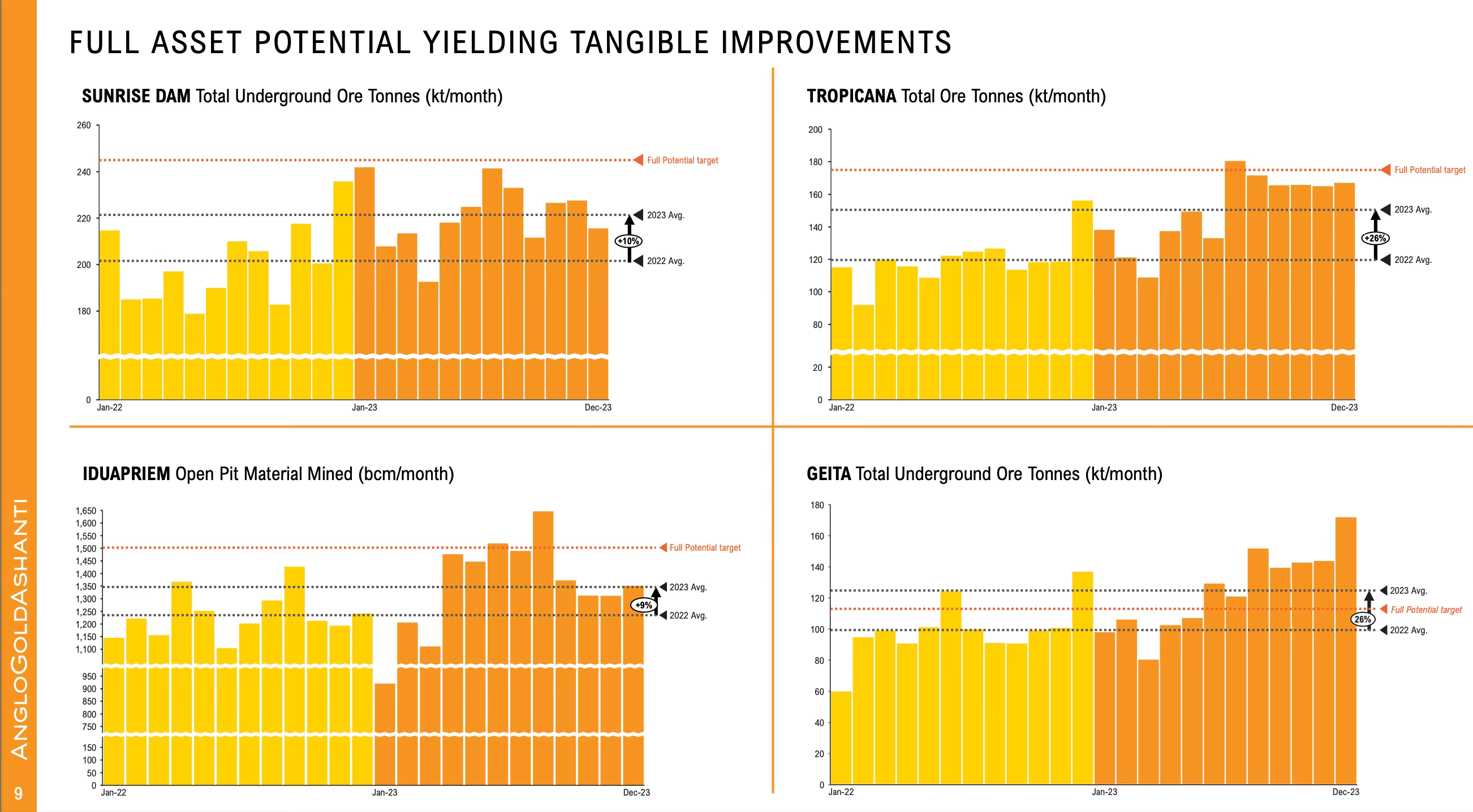

Alberto would also get down to the nuts and bolts of the mine operations and improve efficiencies, especially at Obuasi in Ghana. This was the mine which originally captured Mark Bristow’s attention. Obuasi is potentially a great mine if you can run it well. It has a 7mn oz reserve with high grades (over 9g/ton).

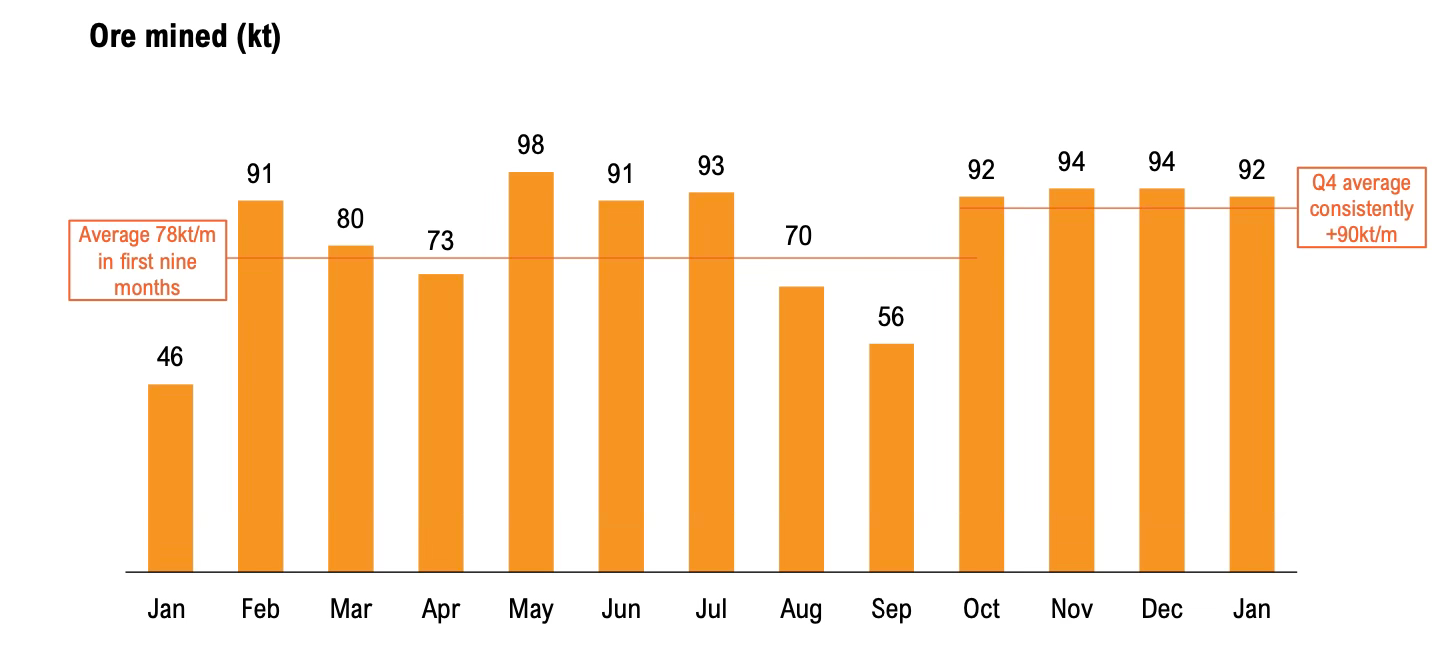

Now less than 2 years later the monthly throughput at Obuasi is improving. Monthly ore mined is averaging 90k tons/month up from of 80.

But it’s not just Obuasi. The rest of the mines are improving too.

And the exploration bet in Nevada?

That worked out too. Massively!!!!

AngloGold found 9mn ounces at Merlin which could be the largest US gold discovery in the last decade. Altogether the North Bullfrog, Silicon and Merlin discoveries have enough gold to build out a substantial US business for AngloGold over the future years (500oz/year eventually). North Bullfrog will produce first gold in 2026 and will add 100,000 oz’s in 2027.

It’s all coming together.

The turnaround at Obuasi. First gold from Bullfrog in 2026.

Finally, AngloGold’s production profile starts to turn up again.

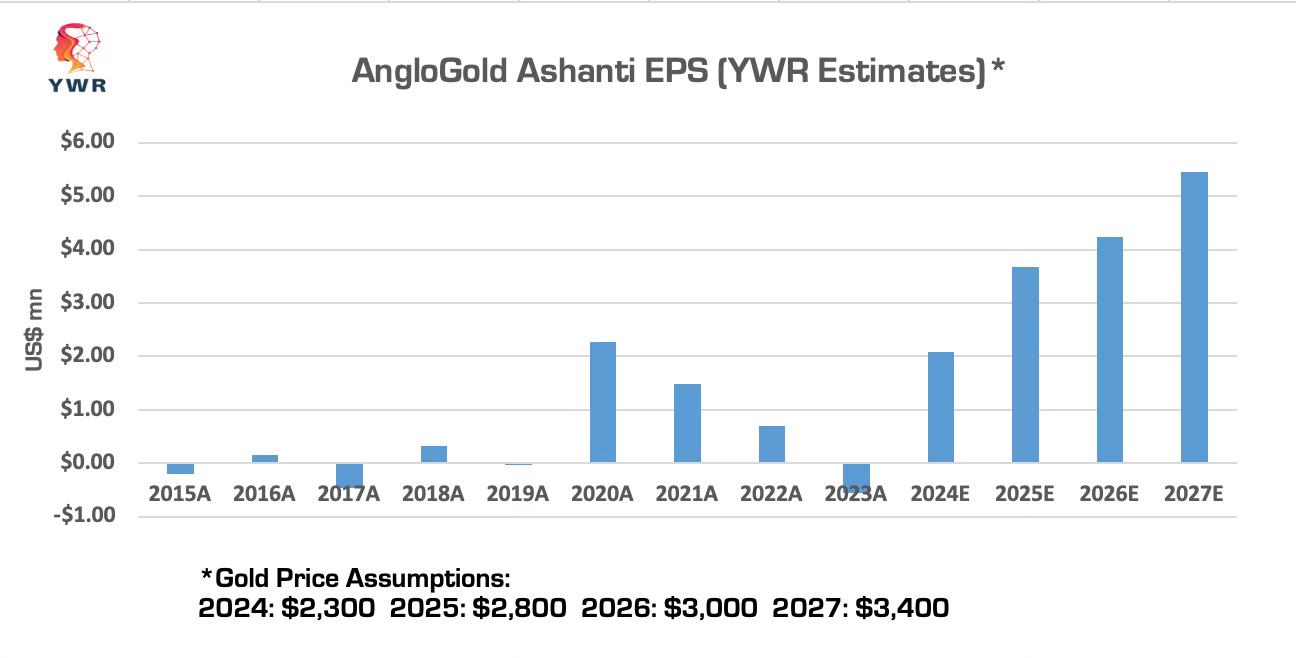

And if gold starts to work..EPS climbs rapidly from $2/share to over $4.

We could have a $22/stock (currently) earning $4share in 2026 with a mega project (500oz/year) in the US just over the horizon showing a pathway to $5 or $6/share.

So can AU 0.00%↑ maybe get to $40/share or $45? (+100%) in the next 2 years?

And then can we later get to $60 if Nevada starts to come on line and production grows to 3.1 mn ounces?

You can make +50% on gold, but also potentially +100% on AngloGold (near term) plus 15% in dividends (get paid unlike with gold) with more optionality to come in 2027. They both sound good.

Below is the full AngloGold Ashanti earnings model.

Note, these are estimates which are bullish on gold (highlighted in yellow). But the model shows how things can work. Feel free to be conservative.