YWR: The Curzon Global Opportunities Fund

Office of Pembroke Advisors

Mayfair, London, 1899

Lord Curzon, welcome! Please come in. Let me take your hat and coat. There we go. Can we get you anything? A cup of tea perhaps? Come this way. There are two chairs for us by the fire.

Thank you Timothy. Yes, Lloyd a cup of tea would be wonderful. No sugar though.

Now I have to say Lord Curzon we only received your letter yesterday, but of course we are glad to see you anytime to discuss your investments. And we understand you will be soon be returning to India for your new appointment and it will be harder to correspond. How can we help? What is it you would like to discuss? As agreed, your portfolio is well diversified globally, performing well and in line with the risk profile we created during your onboarding.

Yes, the portfolio is doing well, but I have two key changes I would like to make before I leave for India. The first one regards my US allocation. I want to double it to 30%.

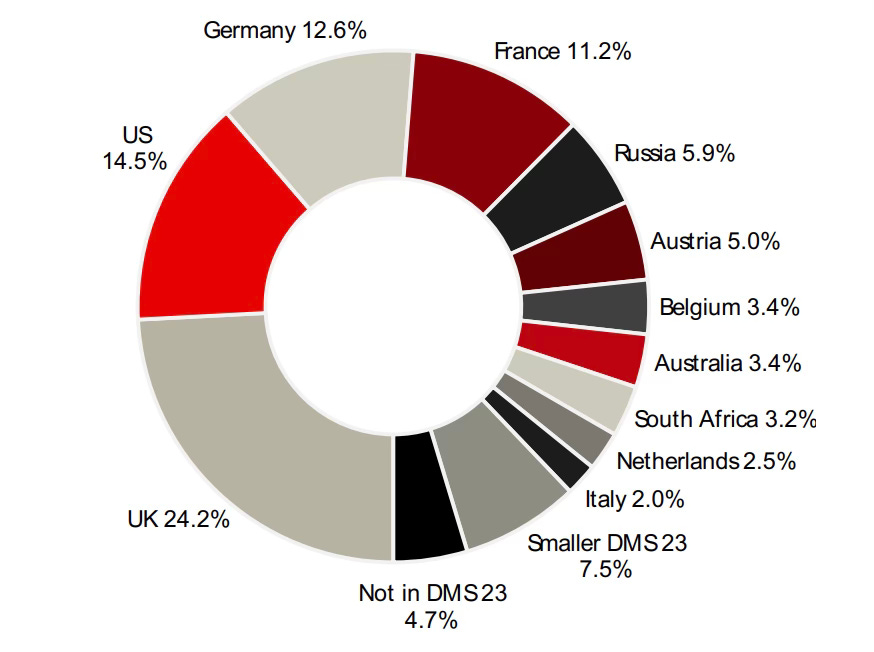

Lord Curzon’s country allocation (1899).

Double it to 30%? Did I hear correctly sir? But, you are already double the benchmark weighting of 7%. Increasing the US means reducing your allocation to Europe and the UK. Forgive me for asking, but why would you want to do that? You are allocated to the finest, most stable countries in Europe. Plus, you have the safety of the pound, the franc and the deutche mark.

The US on the other hand is highly risky. The economy has been in recession since 1896. At any moment hostilities with Spain could recommence. Furthermore, their economy is not industrialised to European levels and probably never will be. They have no leading universities and will struggle to innovate. And where do we begin with their President McKinley and his tariffs. His VP, this Teddy Roosevelt character, is even worse. Yes, we get along with the Americans for now, but there is always the possibility of future disagreements between them and our King.

So I’m sorry dear Lord, as a Chartered Member of the Royal Society of Investment Advisors (RSIA) I cannot in good faith support a 30% allocation to a bunch of raccoon skin cap wearing frontiersman. It would not be prudent.

Thank you dear Timothy. We’ve been friends a long time and your advice is well noted. But, and I say this in the politest way possible, what you possess in prudence, you lack in imagination.

I see the outlook differently. Yes, these Americans have had many wars, even a terrible civil war. But, I see these as the growing pains of a young country finding its way. And yes, they are less developed than Europe. But rather than a risk, I see this an opportunity. I see instead the early days of a great nation. Americans themselves don’t even realise the brightness of their future.

You say their industry is behind the UK, but for how long? They are catching up quickly. I know it is unimaginable that a bunch of tobacco spitting frontiersman can best the great minds of Cambridge and Oxford, but somehow they keep coming up with new innovations. There is actually an explosion in patents filed out of the US. Take that Comptometer they invented for example. One of my VC funds is invested in it. What if in the future every bank has a Comptometer? I know it is hard to imagine, but the patent data tells me America will soon take the lead from the UK in new innovations. And as we know good Timothy, growth follows innovation.

Geopolitically, I also see their influence spreading across Latin America and now Asia. It’s possible their influence could one day rival that of the British Empire.

Now Timothy, I understand London’s investment community is of like mind on this and negative on the United States. And it makes perfect sense. So I take full personal responsibility for the decision to raise the allocation to 30%.

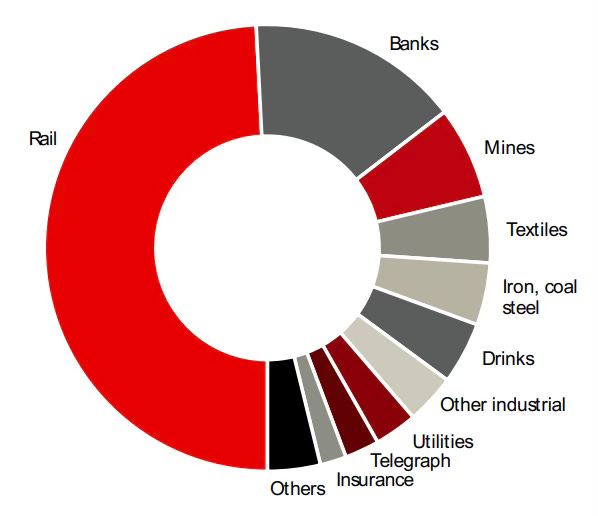

This also brings us to our second allocation change. I want to reduce my railroad exposure.

But Lord!!! Reduce the rail exposure? Again, I have to ask why? It’s been the best performing sector for the last 25 years. It’s part of our urban mobility theme. The whole economy will run on railroads. Why sell now?

Dear Timothy, do you never leave the comfort of this office? Do you never venture out on to the streets of London? Every carriage boy in London is investing in railroads. It’s become common. On the game shoots it’s the same. There is so much talk of railroads I’m no longer sure if we are hunting pheasant or stock certificates. It’s time to move on.

It’s time we think instead of the economy the railroads enable. Yes, the economy will run on railroads, but what businesses benefit from railroads? What new businesses will emerge? What everyone else is missing is how railroads enable the rest of the economy to boom. So I want to increase our exposure to other sectors like industrials, real estate, banks, and insurers. Please reduce the railroad exposure and add to the beaten down value sectors.

Tomorrow I set sail for India and from then on will be pre-occupied with my work. It will be difficult to correspond. Please make those allocation changes. Then leave the portfolio like this for the next 125 years. In 2025 on of my heirs will come by to review the allocation and make some new changes.

Definitely my Lord. We will carry out your instructions as you wish. Safe travels. India is lucky to have your leadership. Farewell.

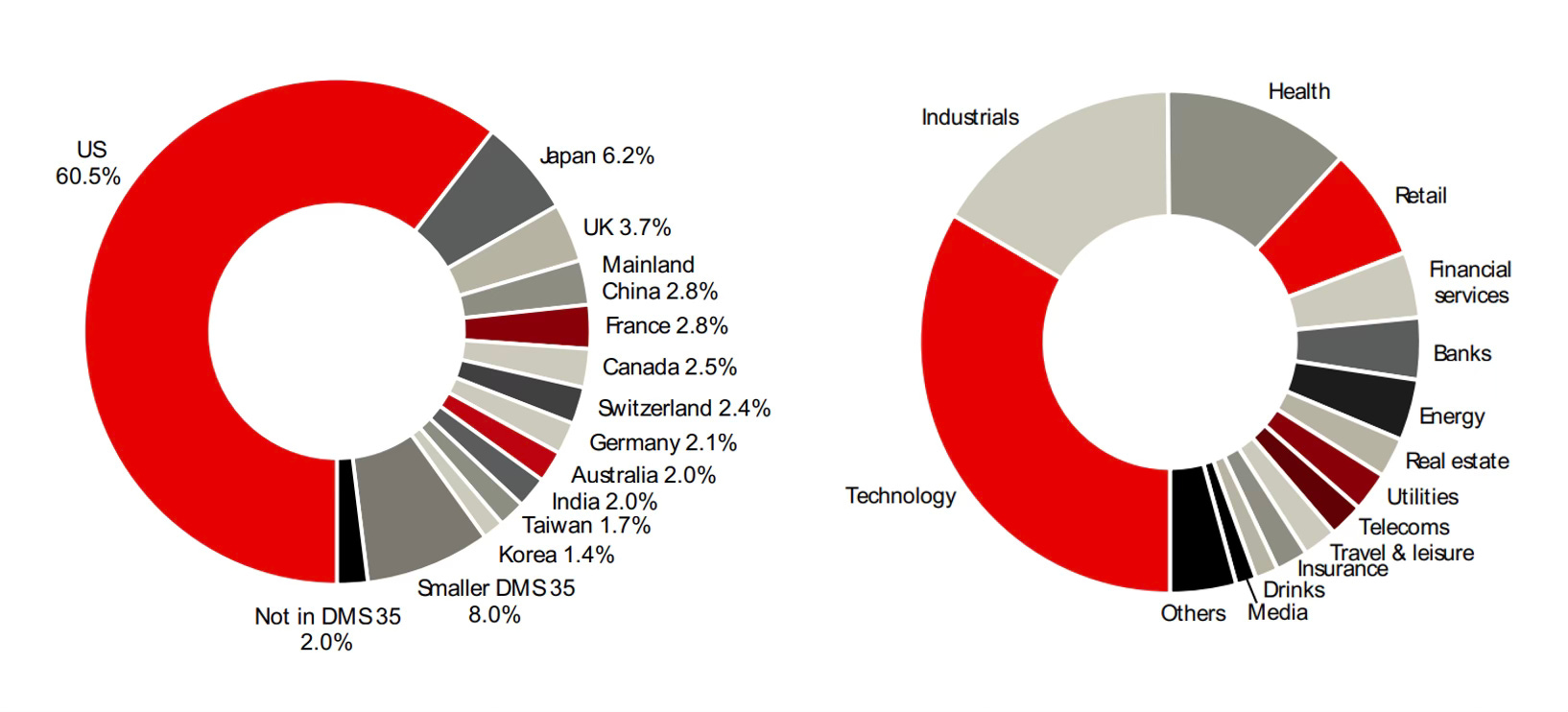

The Curzon Global Opportunity Portfolio in 2025

Below is Lord Curzon’s allocation 125 years later.

In hindsight Lord Curzon was a genius. He saw the inflection point. Saw a massive trend emerging and changed to an allocation far outside the conventions of the time.

But if Lord Curzon walked into Pembroke Advisors today and looked at his allocation what would he say?

What would be his allocation for the next 25 years?

This is how I think he would tell Timothy to allocate.