YWR: The Godzilla Trade

Grey haired elders sense its return.

Only they remember the early days.

When the great Beast ravaged our lands.

A monster from the dawn of financial history.

Spewing liquidity like fire.

Inflating the price of everything.

Stock markets, Golf courses, trophy office buildings.

East to West the Beast’s fire spread forth.

Unstoppable.

Until in the end consumed only by its own inferno.

Its final screams gurgled as it slid into the Pacific.

Leaving scorched lands to recover and heal.

An era now forgotten.

A faded folk tale whispered late at night by the few.

A yarn from the past. Never to happen again.

Yet deep beneath the Pacific the primordial monster stirs again…

Long thought dead it feels its energy returning.

Gathering itself to rise again.

It’s Killer Charts time.

Normally, we would go over the BofA Survey.

Go over S&P Earnings Trends.

Go over hedge fund positioning.

But we don’t need to.

Earnings are fine.

Managers are still bearish.

The here and now is in order.

This affords us space to cast our mind’s eye West over the horizon.

To the Pacific.

And the return of the Beast.

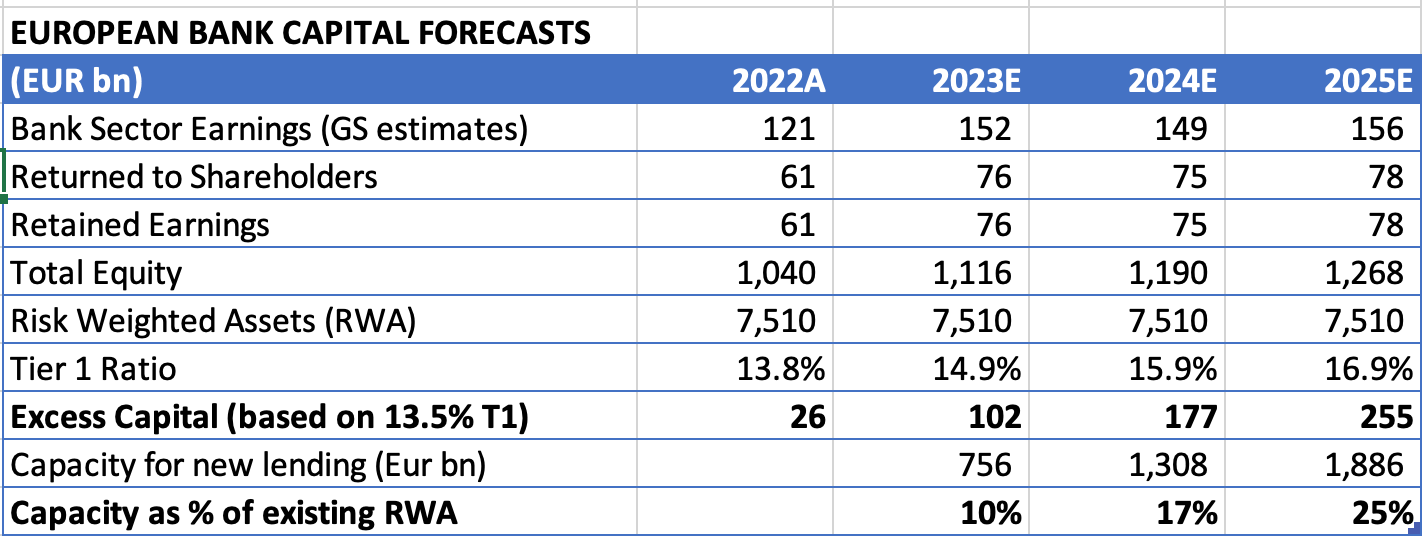

In November 2023 we wrote ‘What do you do with EUR 250 billion?’

We were modelling the rapid improvement in profitability of the European banks coming off negative rates. We were looking ahead to 2025 and the potential build up of excess capital. On our numbers European Banks would have EUR 255 billion in excess capital which could support EUR 1.9 trillion in new lending capacity.

In 2023 a bull case for Europe was unimaginable.

Europe would never grow.

Yet, we wondered what could happen in 2025 if the entire banking sector was overcapitalised and looking for ways to deploy capital.

If banks want to lend.

Pigs can fly.

And here we are with investors miraculously excited about European growth and the DAX making all time highs.

And the effects of this excess capital are still just beginning to unfold across Europe.

Which is great, but it reminds us of another liquidity pool with the same dynamic.

Godzilla.

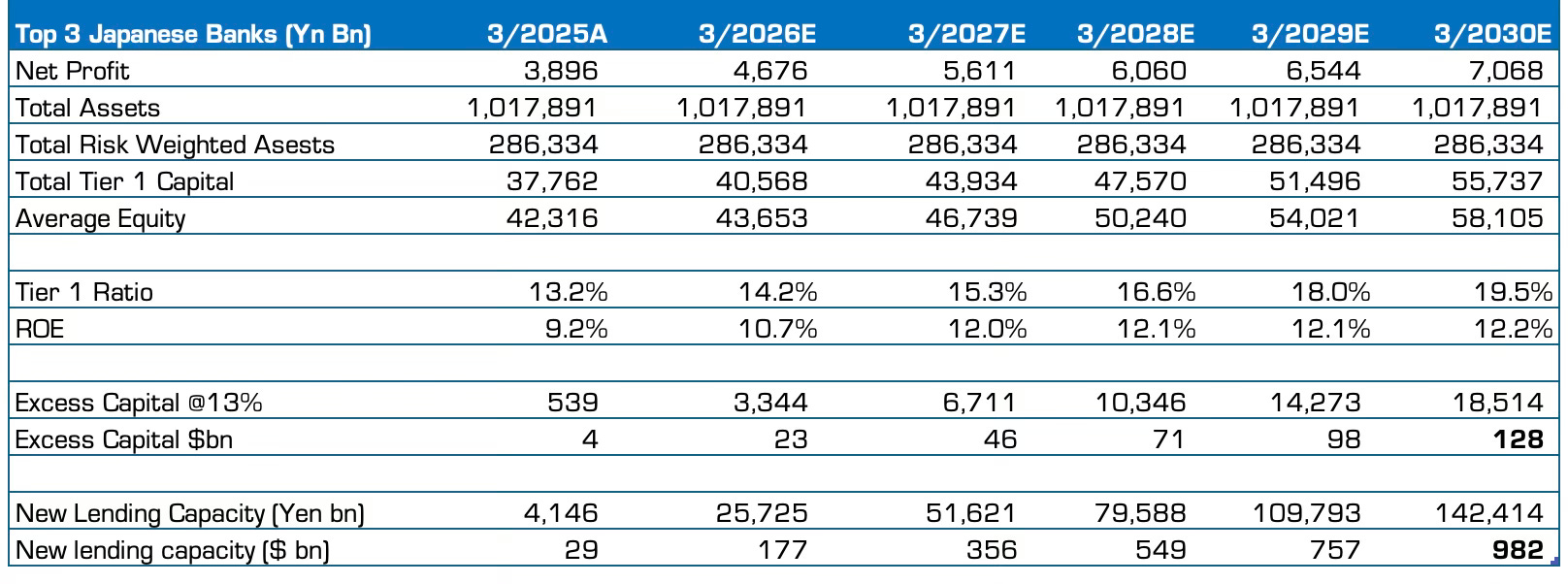

The Japanese Banks.

Like European Banks, ROE’s for the Japanese Banks are rising off low levels thanks to the end of negative interest rates.

By 2027 ROE’s for Japan’s top 3 banks should improve from 9% to 12% thanks to higher deposit spreads, higher fees and reinvesting excess liquidity into 5 year JGB’s. Net profits can improve 44% from 3.9 trillion to 5.6 trillion in 2027 without any balance sheet expansion.

But roll forward.

By 2027 net interest margins have widened and ROE’s are 12%.

Investors will want a new story.

At that point if the banks don’t increase their risk appetite, or deploy earnings into share buybacks, the capital starts to pile up. The ROE starts to drag.

By 2030 the 3 Japanese Mega banks will be sitting on $128 billion in excess capital with a lending power of $1 trillion.

That’s Godzilla money.

$1 trillion in new loans isn’t as much as Europe, but it will be more impactful because this fireball of liquidity will be directed into a tighter target.

Japan. Thailand, Vietnam, Indonesia, Phillippines, India.

And this is why we do something different from the crowd this weekend and spend 20 minutes going over their presentations to observe where 3 banks with $7 trillion in assets want to deploy their money in the years ahead.

A link to the full YWR slide deck is below with my favorite slides from all three banks.

But here are some highlights.

1. Management can see how profits will mechanically increase through 2026 as the balance sheet is reinvested with wider spreads. This visibility is good for risk taking.

Japan's Policy Interest rate: rise to 1.0% from 0.5%

O

USD/JPY FX rate: 140

-

1

Regrowth of Japan

Lead Japan's regrowth

Bottom-line profits

JPY 1,178 bn

2

Growth of Asia

Capture dynamic growth

with partners

JPY 962.9 bn

Growth of

Establish presence

---

JPY 805.8 bn

Gains of sales on

3

Capital Markets

in global capital markets

equity holdings drop

ROE

6.5%

7.0%

8.0%

9%

10%

11%

FY3/23 FY3/24 FY3/25 FY3/26

FY3/29

Around 2030

Next Medium-term Plan

Medium-term Plan after the next")

Potential for 11% range if

BOJ raises rates further

Scenarios for domestic and

Stably achieve

Consolidated Net

international economies

TSE ROE of

Favorable conditions

+

Business Profits*

of approx.

Over 10%

JPY 1.4~1.6T

Higher

Large majority of reciprocal tariffs

(assuming BOJ policy rate of 0.50%)

end of 10%

are withdrawn.

Favorable economic conditions.

BOJ raises policy rate to 0.75%

Around

TSE ROE

10% i

Gradual recovery

--

approx.

Some reciprocal tariffs continue.

9%

Mid

International economic downturn

ensues, followed by gradual recovery.

9%

BOJ keeps policy rate at 0.50%.

TSE ROE

8.5%

Stagnation

TSE ROE

All reciprocal tariffs continue.

7%

International economic downturn

ensues, followed by slow recovery.

BOJ keeps policy rate at 0.50%.

FY23

FY24

FY25

FY27

* Incl. Gains (Losses) related to ETFs

MIZUHO

10")

Domestic Japanese Real Estate is a growth area for both Sumitomo and MUFG. They want to plough money into real estate loans. It makes sense. It’s a huge local asset class and it’s recovering. Do we front run this?