YWR: The Good and Bad of Chinese Earnings.

It’s fun to hunt for new ideas and make bold predictions about future.

But, really the money is made in the waiting and tracking of those predictions in the years ahead.

Are those exciting bold views coming true?

Did you really understand the business you bought?

You learn many things about your investments in the nuances of how things play out vs. what you predicted. It’s why in our YWR models we always keep the tabs with the old predictions. Let’s not memory hole what we optimistically predicted in the past (although the sell side loves to do that).

We’ve done the European bank earnings, now let’s do our China Cash Dragons. I’m going to do HKEX and SGX in a separate post. They deserve more focus.

Our stock allocations are in YWR Portfolios.

Links to the models are at the bottom of the post and at www.ywr.world/datasets

Let’s go good to bad starting with Tencent (700 HK).

Tencent:

What stood out to me:

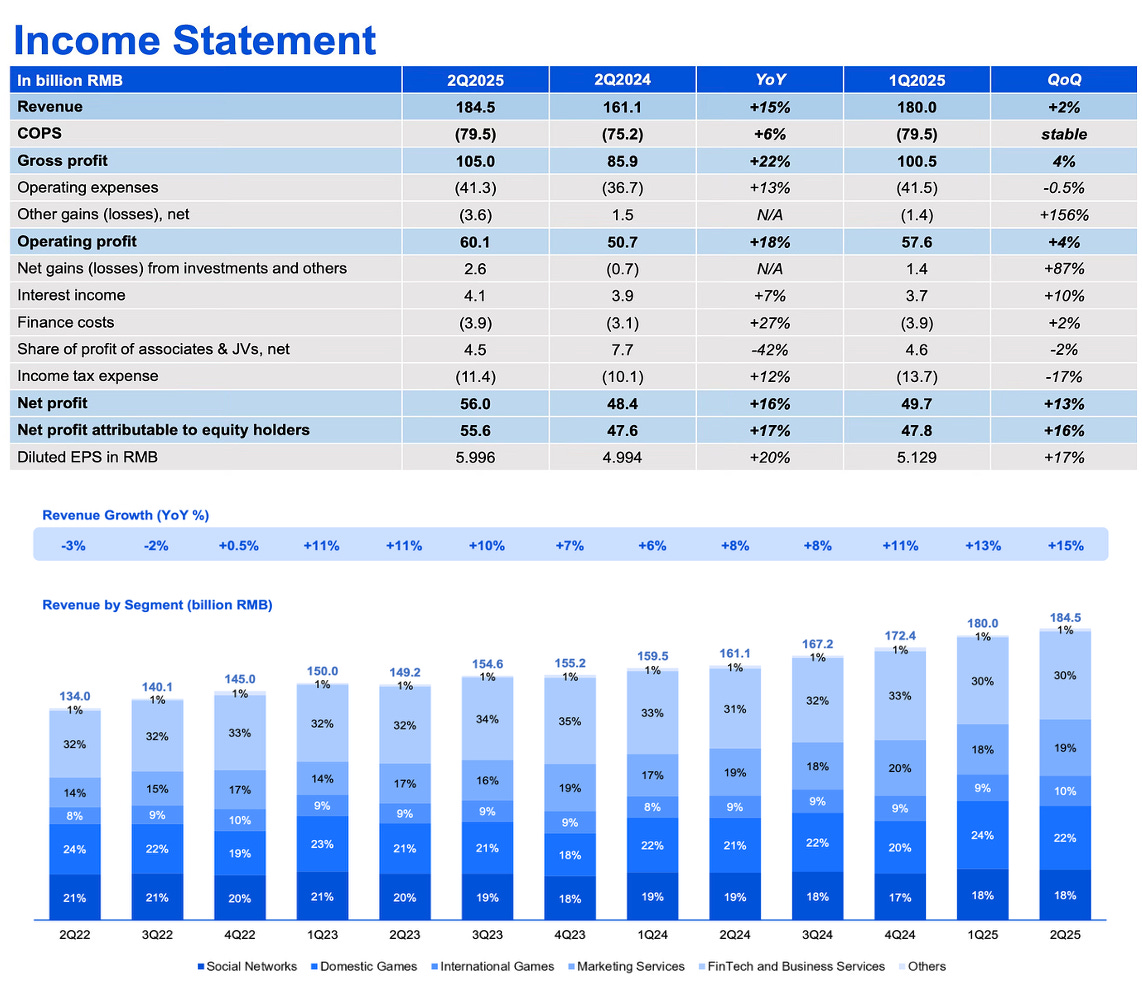

Revenue growth accelerated and areas that had been slow picked up. I thought Social Networks had gone ex-growth, then it grew +6% in Q2.

I thought Chinese domestic games had hit a soft spot and international games was the only driver, then domestic game revenues grew +17%, and international was +35%!

Big name games like Honour of Kings, League of Legends, Peacekeeper Elite, Valorant, PUGB, seem to be perpetual money machines as long as you keep the updates coming. I used to think they would die out, like old Atari games, and worried Tencent needed to come up with new big hits all the time, but instead with updates, and new features, these games seem to keep going.

Marketing Services has always been a big opportunity when you looked at how much money Facebook was getting from advertising compared to Tencent. Tencent continues to grow this business double digit every quarter. I almost don’t even think about it anymore.

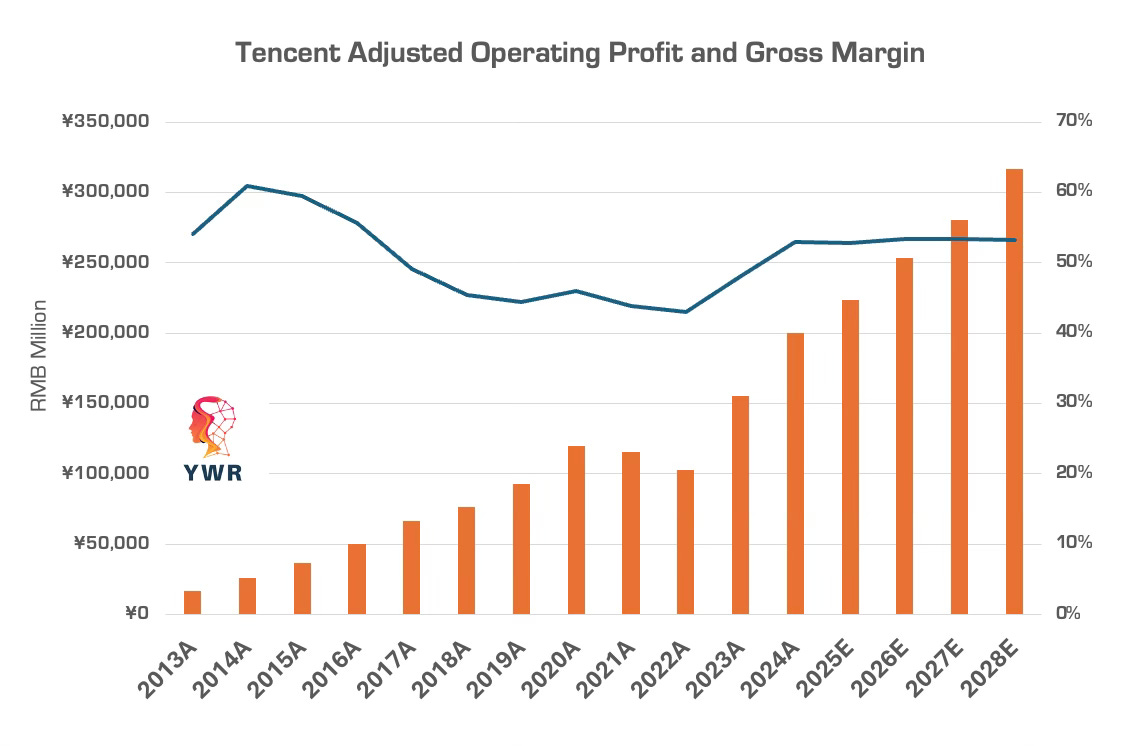

I keep expecting the revenue growth to go to Tencent’s head and the cost line to disappoint, but it’s the opposite. I have to nudge my gross profit margin expectations up from 52% to 53%.

Overall, Tencent managed the post COVID soft spot extremely well and is on to new highs. Revenues are accelerating and costs remain under control.

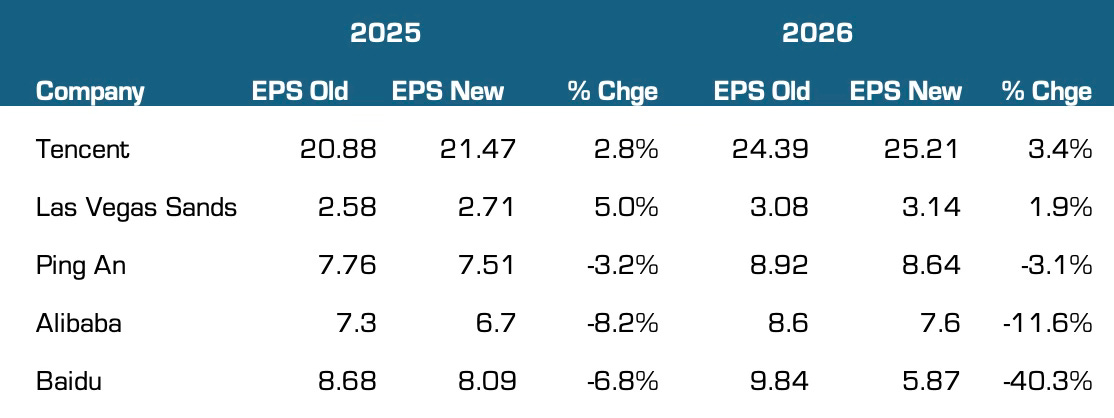

What do we do? Sit tight. We bought Tencent because of the super strong collection of businesses, long-track record of growth and execution under the original founder, Pony Ma. It was a rare opportunity to load the boat. In hindsight we should have just bought Tencent and nothing else (no Alibaba, no Baidu).The stock should make new all time highs along with the growth in operating profits.

Las Vegas Sands:

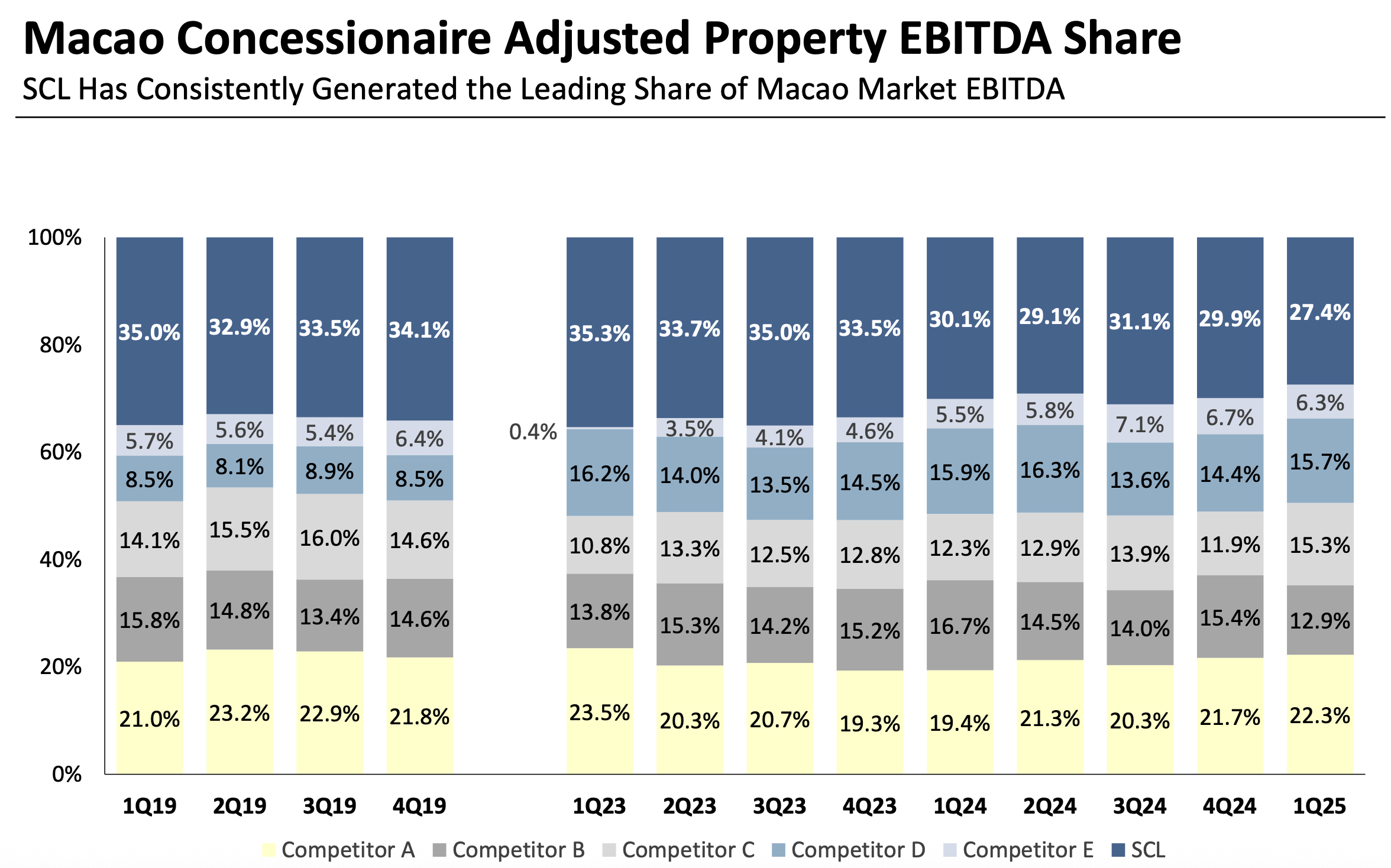

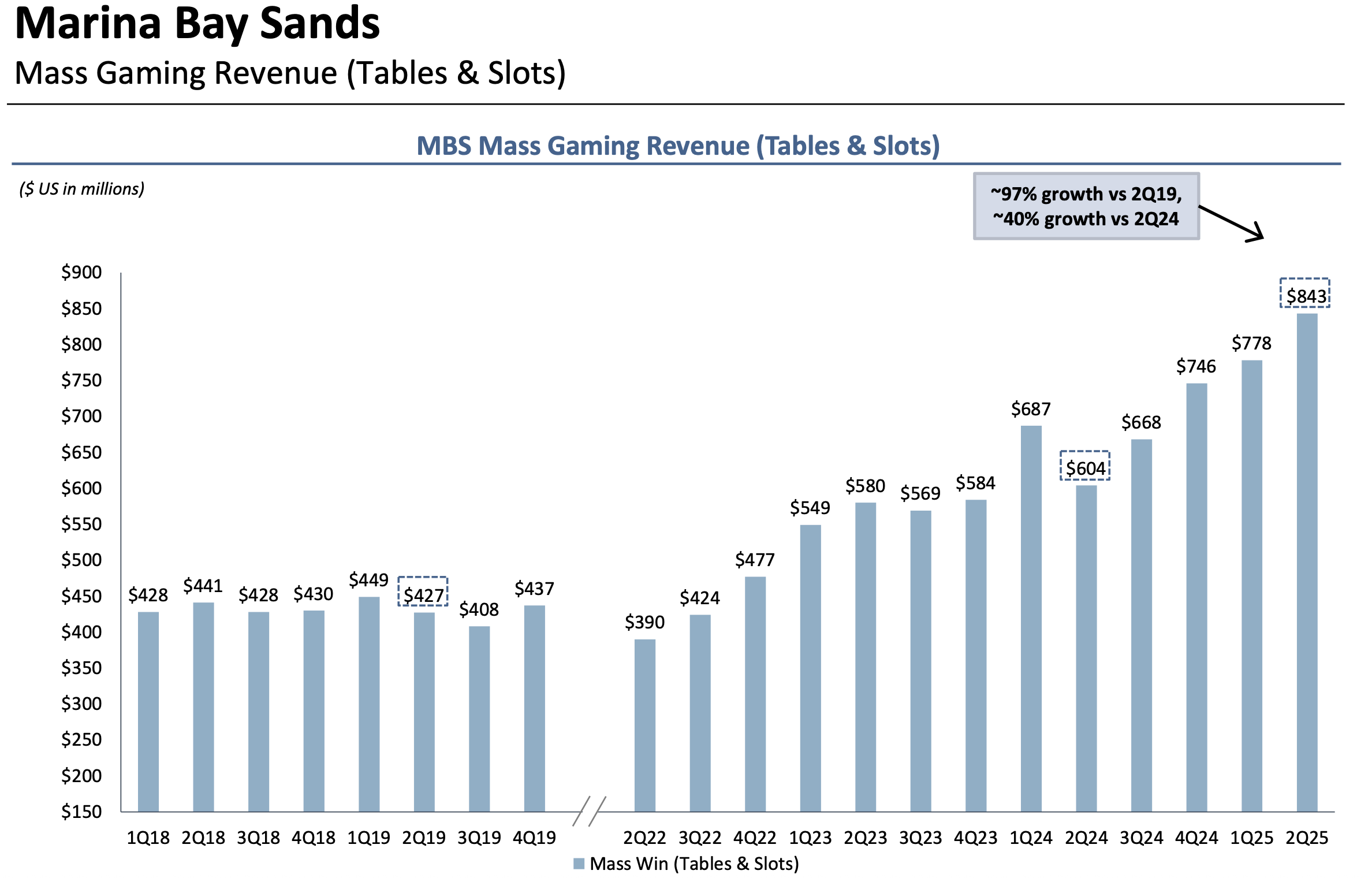

We bought LVS on the idea the Chinese economic recovery and stimulus would flow through into consumer incomes, and higher stock prices. Eventually all this stimulus liquidity would flow into our enormous cash register in Macau where LVS has 40% market share. These massive fixed cost casinos would have a huge surge in operating profits as the money flowed in. A perfect Project Zimbabwe play.

So how is it working out?

We are making money in LVS, and earnings are beating expectations, but not the way we expected.

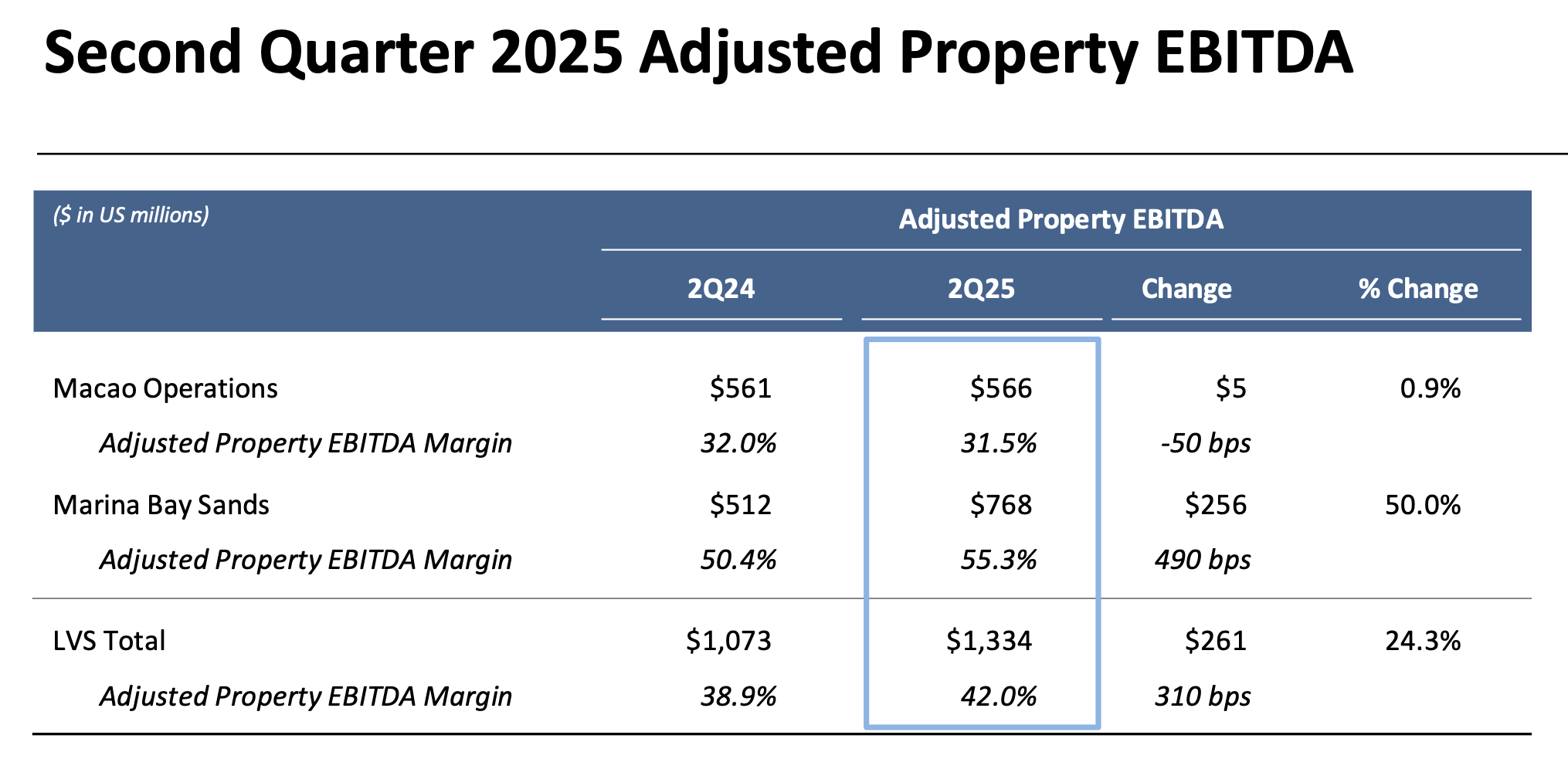

Macao has been dead as dirt. While Singapore is exploding.

If you remember Macao earnings were weak last year and the LVS explanation at the time was this was because of major renovations to the events arena and renovations to the Londoner Macau. But now those renovations are done, and the Macau earnings haven’t picked up. Instead, what you see is visitations are still weak, there is excess capacity in the market and LVS is losing market share to the other players who are cutting price. It tells you the Chinese consumer is still weak.

But then what you see in Singapore with Marina Bay Sands is the opposite. Gaming revenues keep hitting new highs. That one casino is on the cusp of hitting a US$ 3bn EBITDA run rate. It’s blowing everyone’s minds (LVS management and the sell side analysts) that 1 casino could possibly make $3bn in EBITDA. Classic Project Zimbabwe.

But Marina Bay Sands is a one of a kind property in a very unique city, in the heart of the Asian wealth accumulation, which is was another reason we bought LVS. Marina Bay Sands is the best way to play the rise of wealth in Asia. The money comes to it.

What do we do? Sit tight. Yes, the stock seems a bit expensive, but Singapore is blowing the lights out and we still haven’t had our Macau moment. With time Macau will be amazing too. We just need the China liquidity bubble to build more. Then visitation will increase, capacity will tighten, and Macau will have its own Singapore moment. In the meantime LVS keeps buying back shares and paying us dividends. Thank you.

Ping An:

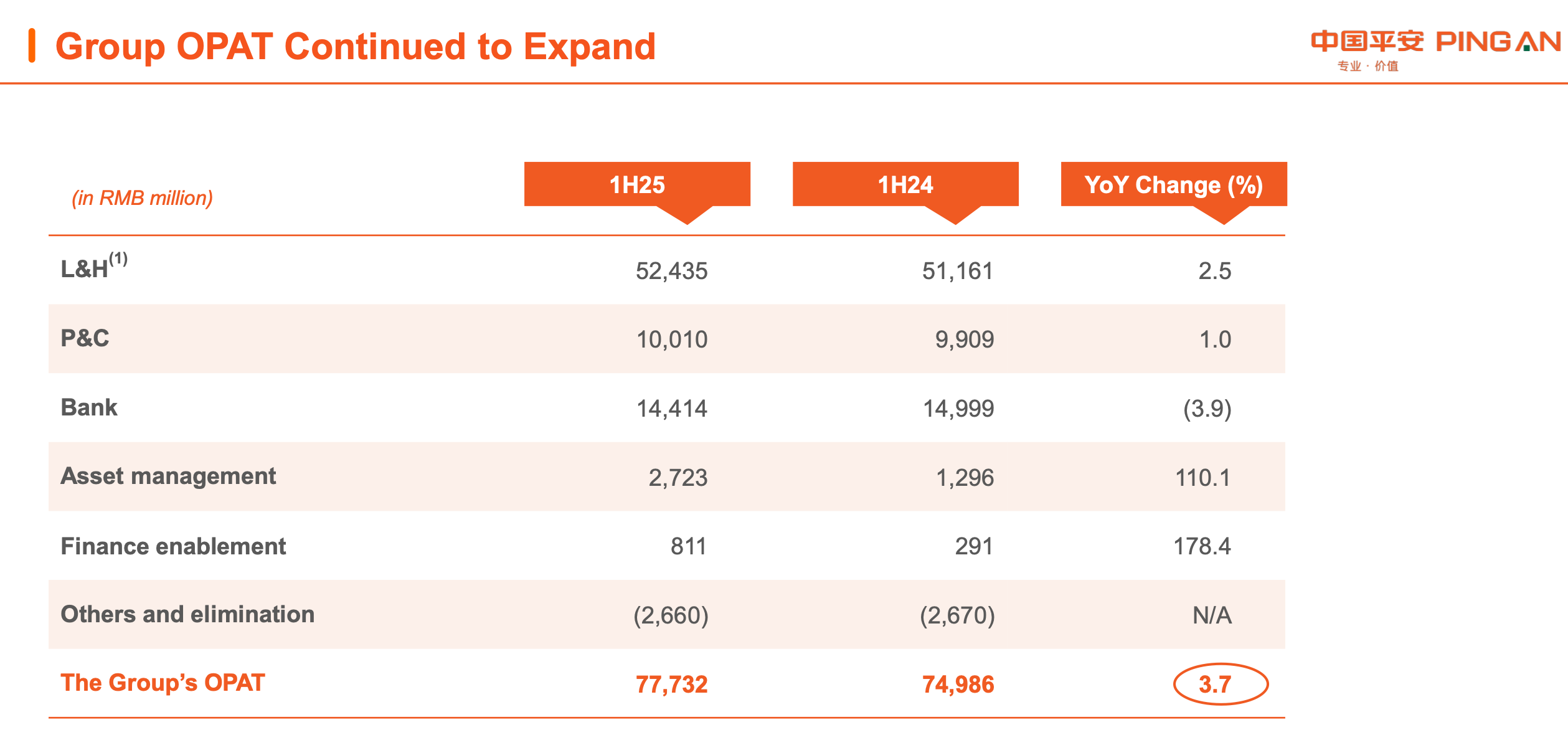

We bought Ping A because it was attractive to buy the leading private life and health insurer plus retail bank in China on a dividend yield of 6.3%. Ping An has been a consistent grower and high tech innovator. So we wanted to buy this great franchise on the lows. It was also a play on the start of Chinese private pensions, their version of a 401K. This would take time to play out, but it could lead to a huge P/E rerating 5 years out if investors start to pay attention to this growing wealth management market and Ping An shows up as the leader. In the meantime we get a nice dividend.

So how it is working out?

OK, but sluggish. Operating profits are +3.7%.

The problem for Ping An is super low interest rates are a headwind to the both the bank and the life insurance company.

In the life insurance company portfolio yields ticked lower because 79% of the portfolio is in fixed income. In the bank, asset quality is fine, but net interest margins are declining because of persistently low rates. It’s how the European banks used to be pre-COVID.

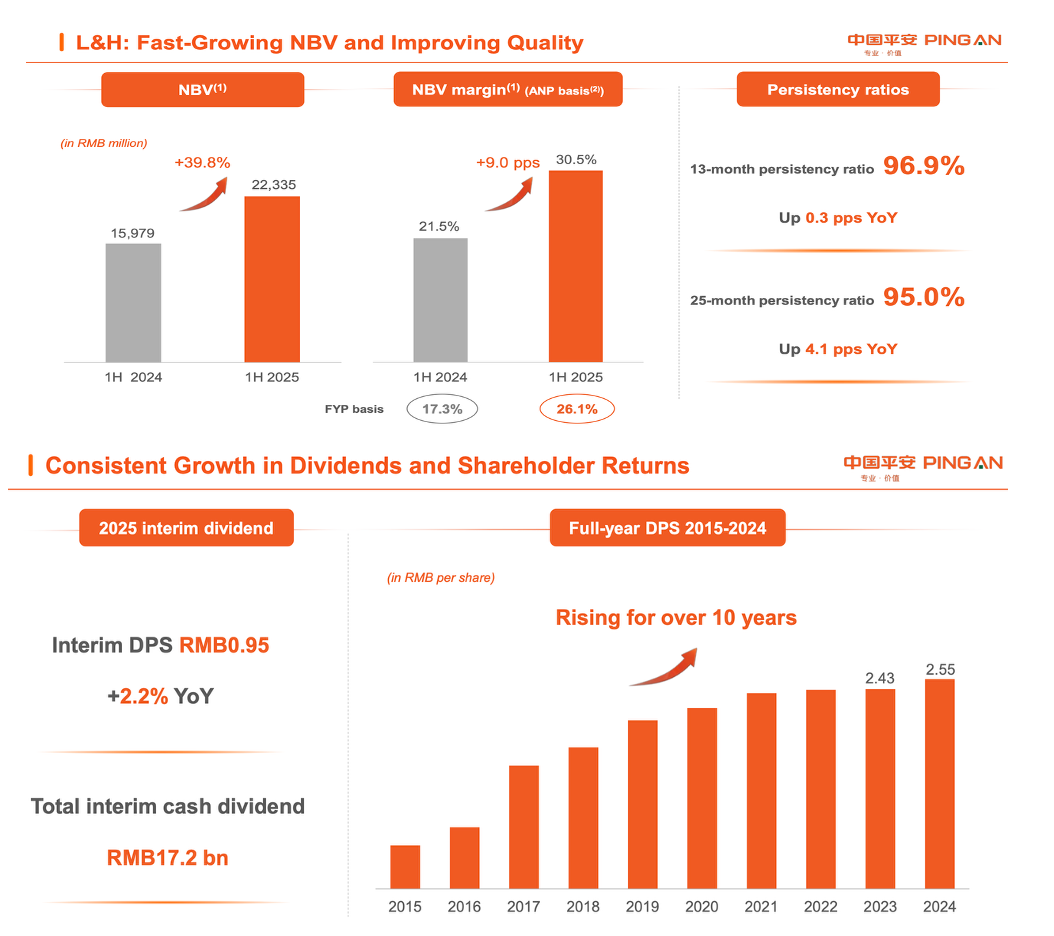

The two positives are that new business value (the value of new life and health insurance policies sold) is +40% yoy! And the dividend is growing too with a 1H DPS of 0.95/share.

New business value is one of those things that takes 10 years to play out through earnings, so to some extent it’s hard to get excited about it, but it’s the kind of thing investors will hype up in a bull market.

So what do we do? We sit tight. Ping An is still on a P/E less than 7x and we get a good yield (now 5%). The stock is working and the new business value is great. The rerate will come.

Alibaba:

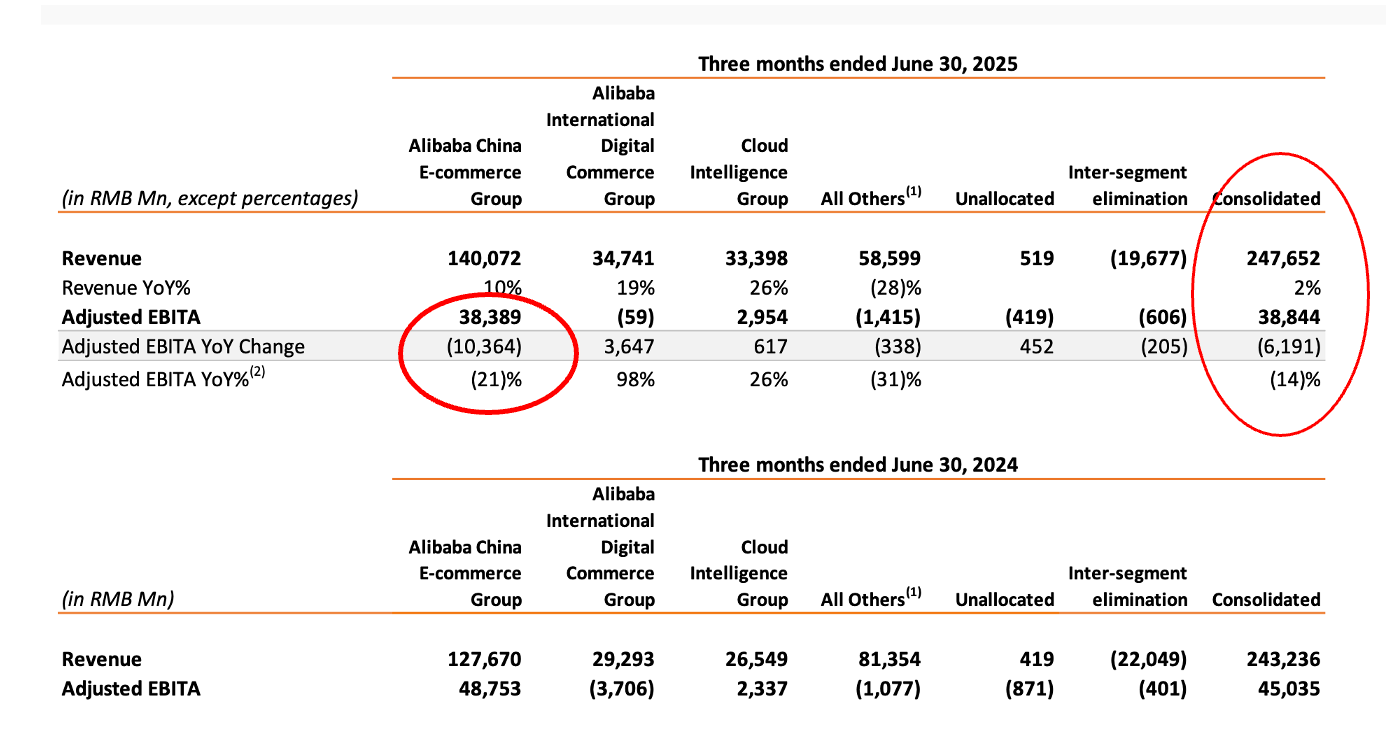

The stock was +13% on 1Q 2026 results (March 2025 year end), which is strange, because they were not good (in my view).

Look below. What do you see?

Revenues +2% yoy, and EBITDA -14%.

Everyone is excited about Alibaba’s growing cloud business, but it hardly makes any money in Cloud compared to the E-Commerce segment, where Alibaba took a big hit to invest in ‘Fast Commerce’.

Basically, Chinese online shopping is super competitive and to keep up with Meituan and JD.Com Alibaba’s Tmall has to deliver products in several hours which required a big surge in costs. So Alibaba’s core business where they make most of the their money is hyper-competitive and declining.

But the stock was +13%. Why?

3 reasons.

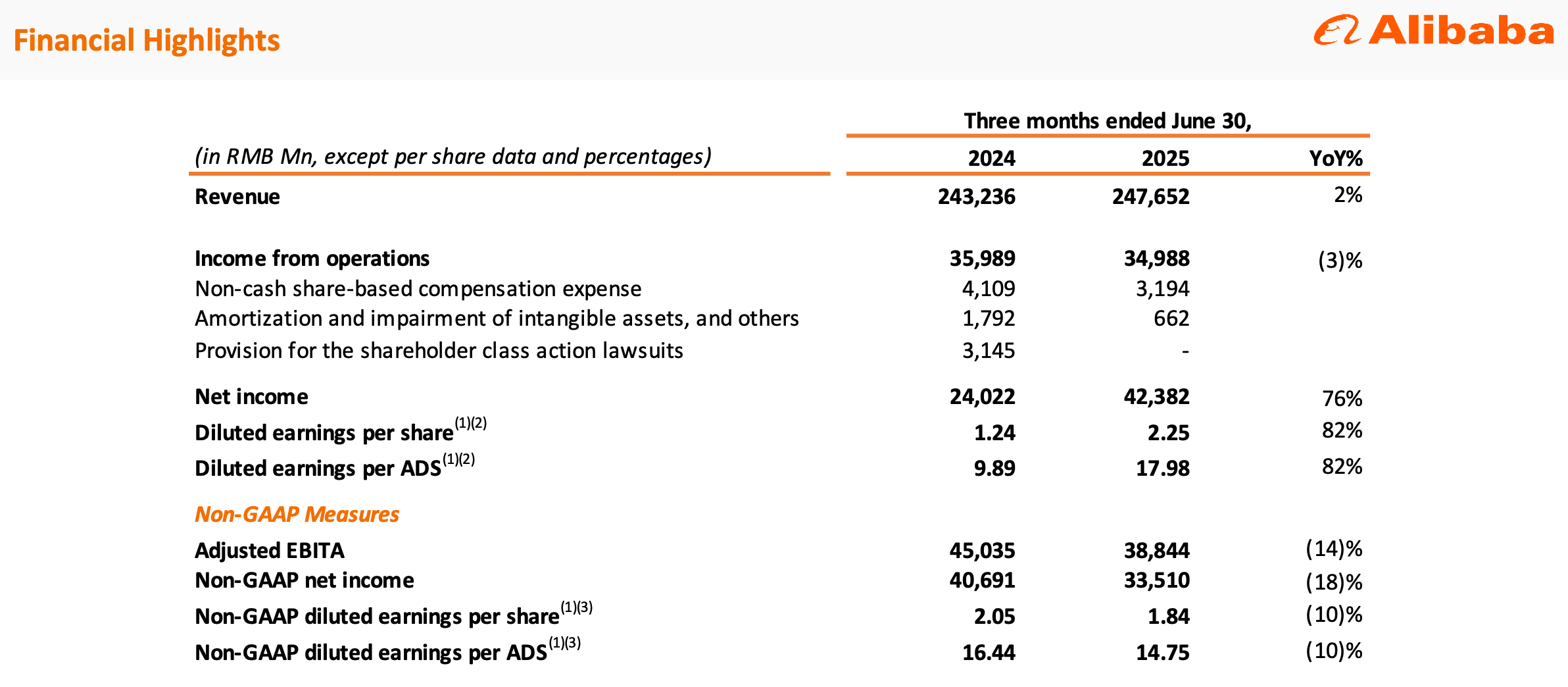

1st. Alibaba saved themselves at the bottom line because they booked 1-off revaluation gains on their many tech investments. So they reported an EPS of RMB 2.25/share which is OK ($2.5 per US ADS). In a bull market we don’t nit pick too much.

Second is that the e-commerce business is ‘growing’ again with revenues +10% yoy. OK..but profits declined so what’s so great?

Third, is the AI narrative. Cloud is only 7.6% of EBITDA, but it’s growing and Alibaba is talking it up. They are also becoming a full stack AI play. They have a Cloud business growing 26%, their own LLM (Qwen) and now a new AI chip under development. They created the optionality to grow into something new. Which the market seems to like.

Alibaba still has $19.3 billion left in its share buyback plan (5.8% of the market cap), but I’m worried that is the end of the buybacks. Future cashflows will be shoved into the AI furnace.

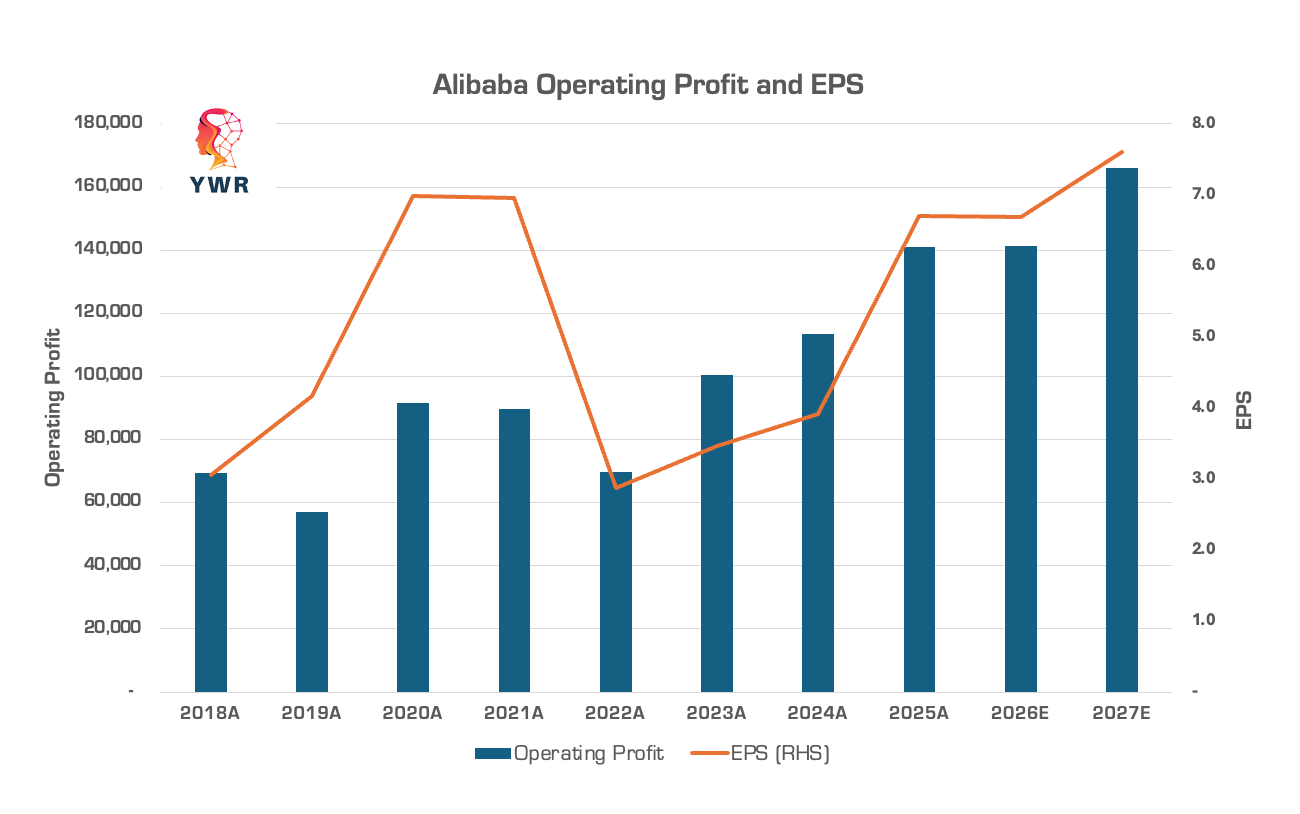

What do we do? The bull market in China is just getting going and Alibaba is now an ‘AI’ play. So we sit tight. Operating profits and EPS should make a new record high in 2027 which means the share price might too.

Baidu:

Ooof. This was bad. Baidu is in a tough spot. Amazingly, the share price is flat. Probably because it’s a bull market and money is flowing into HK tech funds.

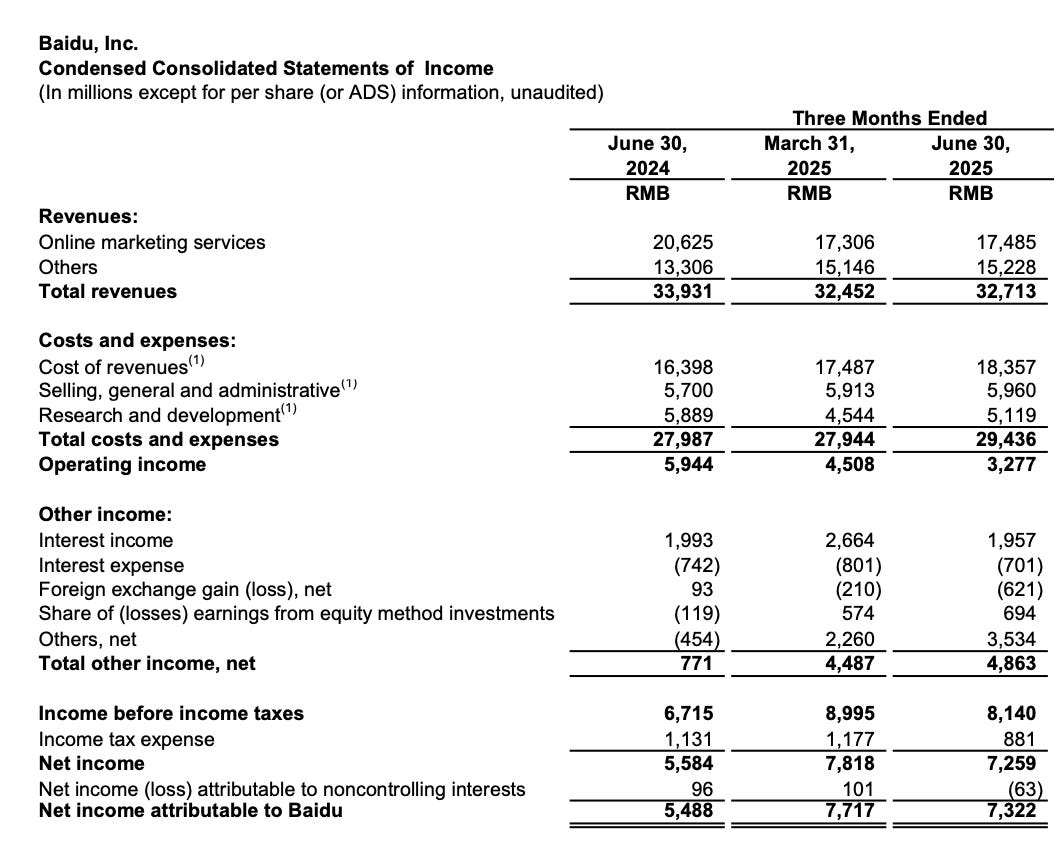

At the revenue line we see the shift from the dying paid search (online marketing services) to the ‘others’ business which is their datacenter and AI businesses.

But as much as Baidu tries to manage costs, the operating income is declining. -45% yoy to RMB 3.2bn.

Like with Alibaba the bottom line was flattered by 1-off revaluation gains on stakes in other tech businesses so reported net income was +33% to RMB 7.3bn.

As we know paid search is getting disrupted because advertisers don’t want to pay for clicks if the only thing clicking is an AI.

So Baidu is growing other businesses like data centers, it’s Ernie LLM and autonomous driving (Apollo Go). Baidu also hopes search will evolve into something even better where instead of searching for links an AI actually books you your dinner or your trip. Baidu is feverishly trying to innovate and discover new AI business models. And some interesting new things are popping up.

For example, online streaming where presenters sell products online is popular in China. Think the Home Shopping Network. Baidu created software where a presenter can create an AI version of themself to stream and sell products online for hours and it turns out the AI versions do a better job than the real person.

These two people below are both fake and they made $7mn selling stuff online for 6 hours.

After the broadcast, Luo Yonghao wrote on Weibo, “To be honest, I was really shocked by the effectiveness of this digital human. The co-host and I (the digital human) exchanged glances and shared jokes similar to yours,” adding, “I felt a bit dazed, but this is reality.”

It’s all very interesting, but in my estimates I have to accept that online marketing service revenues decline another 15% next year, and the 1-off gains will probably be less (still some, but less) which leads to a 40% cut in my 2026 EPS to 5.87. Suddenly, Baidu is no longer cheap.

So what do we do? A risk manager would take me out of this trade. The 3rd quarter will probably look terrible. On the other hand to some degree I think what’s happening to Baidu could happen to a lot of companies. And maybe Baidu are ahead of the game trying to figure out a new business as fast as they can.

But their struggles could also be because they have a weak starting position and they aren’t going to figure out anything which produces meaningful revenue.

I’m not sure. I should probably sell it. But I might not.

Have a good rest of the week.

Erik

Links to the updated models below: