YWR: The Magic of John Burbank

In personal development there are 2 schools of thought. There’s Dennis Rodman and the Japanese.

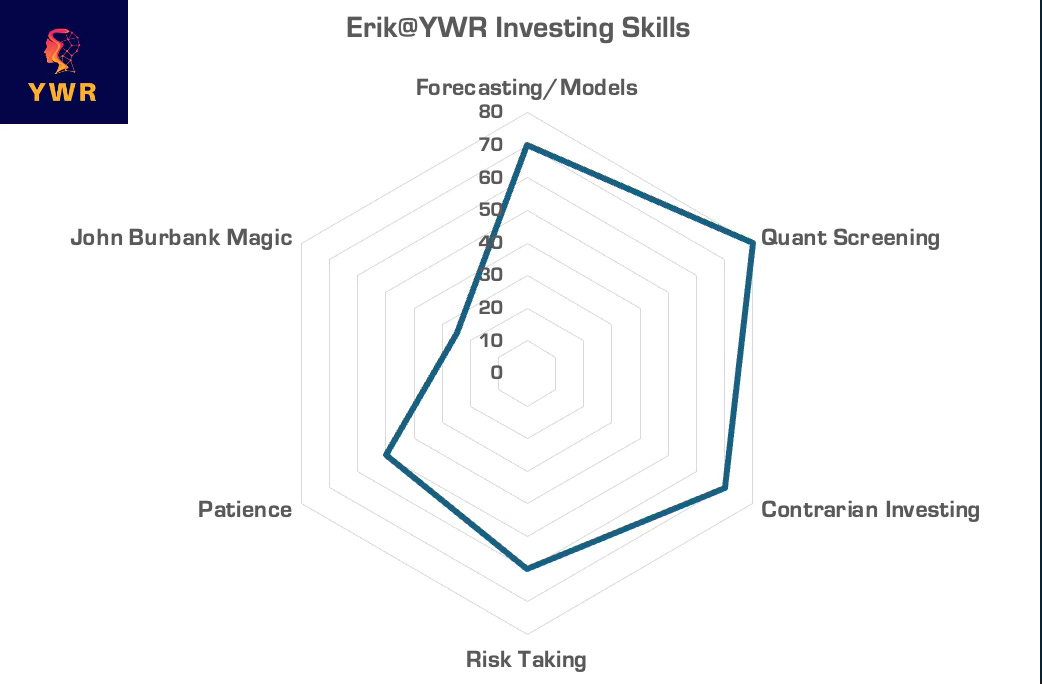

The Rodman path to success is to be freakishly good at one particular skill. Be the best in the world at something, whatever it is. For Dennis it was rebounding. He was notoriously bad at free throws, but found his niche and a spot on the best basketball team ever by learning to rebound better than anyone.

The other path is the Japanese. This is where you have your special skills, but you also improve your weaknesses. When you see someone really good at something, you study what they are doing, then adapt it and incorporate it into your skill set. It’s Kaizen: constant improvement.

I’ve worked with lots of successful people and they each have their super skills which I try to identify and incorporate.

From the first senior analyst I worked with I learned to be better at earnings modelling and forecasting.

From another I learned how to screen and be more systematic in idea generation.

From another PM I learned to be better at sales and how to make friends not customers.

From another I learned to be more contrarian and take more risk.

From another I learned how playing dumb can be smart.

But John Burbank is the hardest. It’s hard to describe what he is doing, let alone how to be 10% more like him.

When you work with him or listen to him talk you can see what I mean. But what do you call that?

Is it perspective, vision, gut instinct? Magic?

How do you become 10% more ‘magical’?

And yet I try.

402 Jackson Street

John’isms

The Institutional Murder of Passport Capital

John’s Rebirth: Investing in Human Capital

New John’isms: Life Force Energy, Government Tech + Golden State Warriors

A John Burbank Idea

402 Jackson Street

I was homesick for California and wanted a job back in San Francisco so after a bit of a search I took a job with a $500mn hedge fund above an art shop on Jackson Street called Passport Capital. They’d been compounding at 25% and a broker friend said he liked the founder.

My job interview with John was a slice of pizza over lunch. You see right away that John is friendly but intense. He asked for a stock idea and I told him about BBVA, a well run Spanish bank with a growing business in Mexico. John’s reaction was why buy BBVA? If Mexico is the attractive growth engine why not just buy that? Or some other bank in Mexico.

And that’s how it went from there. You would have great ideas, but always felt shy speaking your mind with John because you knew he always had some obvious, more brilliant take on the whole thing. He was a natural.

Passport Capital was quirky and that was the essence of its success.

The office itself was the embodiment of this. It was in an old building with squeaky wooden floors. When you opened the front door off Jackson Street there was a long flight of stairs to the 2nd floor where we were open plan. Everytime someone came to visit you would hear them squeaking up the stairs long before they got to the landing. And when they go to the top of the stairs there was no reception. Just analysts on their computers. Eventually, someone would look up and ask you who you wanted to meet.

And the bathroom/kitchen situation. The single toilet for the office was at the end of the kitchen. The bathroom had an accordion sliding door. Yes, there were 3 cans of deodorant above the toilet, but it was still weird when you would slide the door open after using the bathroom and your co-worker would be standing right there making a sandwich.

In the kitchen there were also two coffee jugs. They were essential and prepared without fail first thing in the morning. One was labeled ‘regular’ and the other ‘diesel’. We all drank ‘diesel’. I still call how I like my coffee ‘diesel’.

At 1pm when the markets closed everywhere for the day the traders would play an Alvin and the Chipmunks song if we had made money.

In summary there was nothing ‘institutional’ at all about the set up, but we were crushing it. I loved it.

The fund compounded at 25% year from inception in 2000 to when I joined in 2006. It had a -5% year in 2006 followed by +270% in 2007 when it won Hedge Fund of the Year.

John’isms

Like I said, it’s hard to pin down how he does what he does, but here are a few examples.

In 2000 when he started the fund he said he ‘wanted to get as far away from US tech as possible’ so he invested in India, commodities and China. He was not afraid to be different. In fact he loved it.

He thought it was essential for the perspective and intelligence of the firm that everyone go to both India and China. Even if what you were working on didn’t have anything to do with India or China you needed to join one of the many Passport trips and make sure you knew what was happening there. He didn’t care what it cost. You had to go.

In 2007 one hour after landing in Dubai for the first time he declared ‘We need to have an office here!’ He loved the energy of the place.

You should not get rich on management fees, just performance fees. John thought it was essential to reinvest the management fees back into the business. If you were living off management fees you would get lazy and not take enough risk.

His view was most hedge funds were ‘volatility managers’, not investors.

He disliked the idea of ‘reversion to the mean’. It lacked imagination and appreciation for the magnitude of big changes.