YWR: The South Africanisation of the US

“The US will be the best market for the next 5 years and the next 10 years. Allocating to Europe or China is a waste of time and capital.”

This was from a cocky guy I met at a NYE party who started a hedge fund 2 years ago and told me he “used to run global prop for JP Morgan and Bank of America.”

OK. Whatever. Makes sense. Super consensus though. 97% of global ETF flows went into US stocks in November.

Markets love narratives. Narratives connect the dots. Narratives tell the story.

Well here is a new narrative for Mr. “Global Prop”.. A new narrative for asset allocation.

The South Africanisation of the US.

Peak US Exceptionalism

The thin veneer of Mag7

The impossible trinity of Deficits, Growth and the US$

How we make money

Gobal MAGA

Futuristic Asia

Peak US Exceptionalism

We’ve hit peak US exceptionalism, or at least the concept of it.

The irony is we are all excited and optimistic about Trump’s presidency, but I fear he is inheriting a train smash of accumulated problems. The rot has been going on for years, but Biden was our version of Jacob Zuma. He turbo charged the corruption, the out of control spending and deterioration in rule of law.

The surprise may be that just when markets are at their most optimistic about the US, these problems come home to roost. Trump only has 4 years. The SWAMP strategy will be the same as last time. Delay and run out the clock. In the end Trump’s big achievement will probably be stopping illegal immigration. Bigger changes take persistent work over a decade, and it’s hard to see that happening, even if we start now. The benefits will be years away, while the problems are immediate.

So what does that mean, ‘the South Africanisation of the US’?

Here are the themes:

Rising unemployment

Rising inflation

Rising corruption

Rising crime

Currency weakness

Breakdown in government services

Rise of the lower class

Brain drain

Yes, the US will still be the most amazing country in the world, still the best in lots of things, but your perception of the US will change over the next 5 years. It will seem a little dirtier, and less safe. You will run the math and keep thinking it is too expensive for what you get. And increasingly you will wonder if there are opportunities elsewhere.

South Africans know what I mean.

Ronny Chieng articulates it well. Very funny.

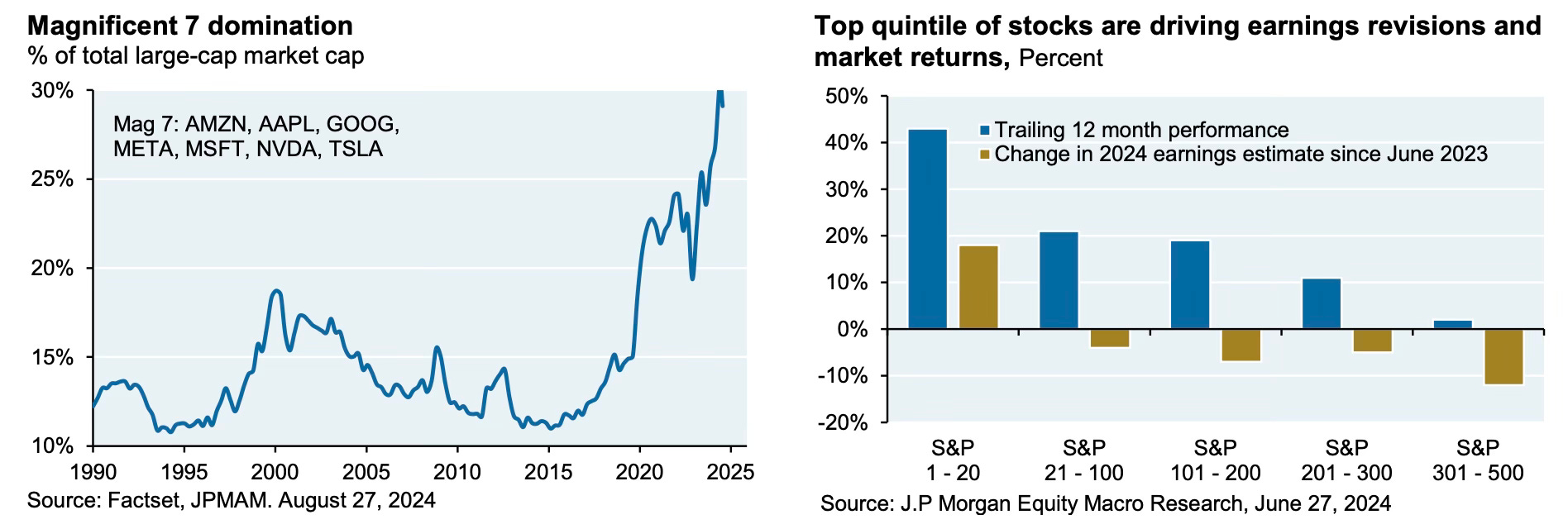

The thin veneer of MAG7.

Much of our perception of US excellence is dominated by stock market returns. The US is the best because its stock market is the best. But this is a thin veneer based on 7 stocks which are 30% of the market. Any problems with these 7 and the US won’t seem so exceptional. These top 7 are driving earnings revisions, growth and performance. Outside the top 20 stocks S&P earnings revisions are negative, which is a concerning sign.

Like the fall of Rome it’s not going to be one thing which takes the tarnish off Mag7. It will be a mix of things, some specific to each company. For example, Apple is running up against the strength of Chinese smart phone competition and struggling to grow sales. Meanwhile, does it make sense that Apple, the most important stock in the world, now trades on 10x sales when sales are stagnant? In the past when Apple was growing it used to trade on 4x sales? It’s the opposite of what it should be and a bad sign.

Google has an accumulation of problems too. It just lost an antitrust case with the DOJ and we will find out the penalties in 2025. The market doesn’t care at all and is optimistic the penalties will be low level fines or inconsequential business changes. Meanwhile, Google has ramped up the spammyness of the search results to try and juice revenues.

But there is another problem brewing, which nobody is talking about, and it’s a problem for Google, Amazon and Microsoft.

A price war in cloud services, everyone’s cash cow.

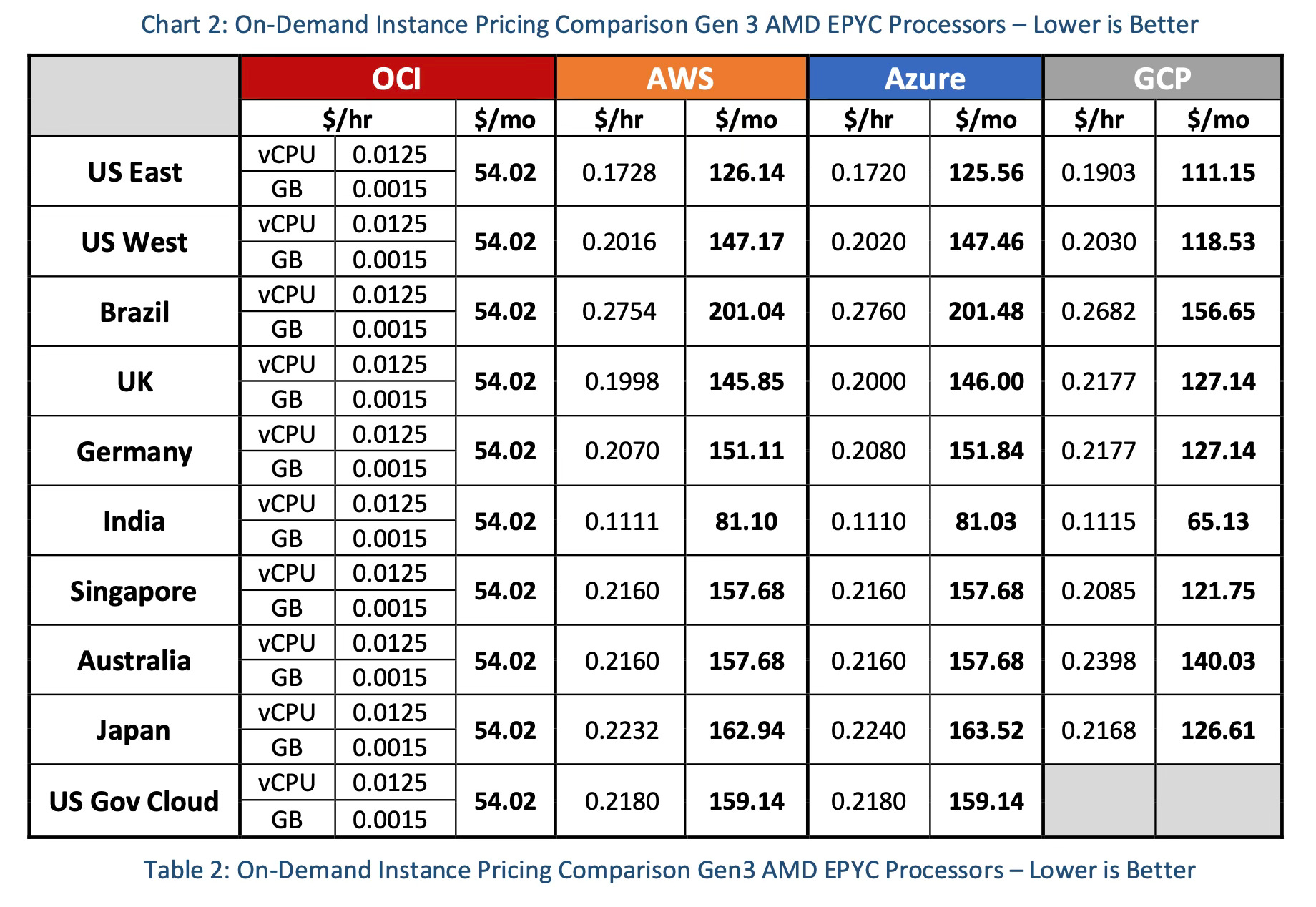

Since 2016 there has been a mutually agreed oligopoly between AWS, Azure and GCP (Google Cloud Platform). They agreed to compete on service, not price. But like with cell phone markets, this equilibrium can get disrupted if a new competitor tries to enter the market. Which is what’s happening with Oracle. Oracle is muscling into the cloud market with innovative products and 50% lower pricing. It’s not a crash tomorrow problem, just more of a gradual revenue problem over time.

It’s also a warning sign for when experts in online sales, guys who are in the weeds of this business, are getting increasingly negative on Amazon.

And did you know there is a free version of Microsoft Office that millions of people are discovering? (https://www.wps.com)

So the signs are all there.

This is classic end of the cycle behaviour. Bezos, Gates and Jobs have moved on and you have unimaginative corporate CEO’s trying to grow profits through financial engineering and turning the screws a little harder. It’s fine, but the problem is the stock market valuations associated with these strategies is too high.

The impossible Trinity of Deficits, Growth and the US$.

The US seems to be achieving the equivalent of walking on water. It runs record government spending deficits to create economic growth, but the currency doesn’t weaken. In fact it strengthens. Inflation is higher than in the past, but not a crisis, and bond yields haven’t broken any key levels. It’s magic.

It’s not magic though. It’s just leads, lags and narratives. Global investors are following the economic growth trend, strong stock market performance and thereby creating huge capital flows which support the dollar.

But they are buying a story which is already over.

Where do we go from here? What’s the new, new?

We’ve stretched the elastic band far enough. If the US is going to keep growing from these elevated levels, then it needs to keep running huge government deficits (6% of GDP), which is eventually going to create a problem in the bond market.

Or, the US government has to cut/moderate spending, which will filter down into the equity market. Either way, if US equity market returns go negative for a few years, and bond returns are negative too, then all of a sudden the US will be under pressure to cut spending, cut growth, and not be so exceptional anymore. Or not exceptional enough to justify the valuations.

It’s a tricky spot.

Global investors will find things look surprisingly interesting elsewhere.

The whole set-up is fragile with a high probability the US$ weakens. This will be a key South Africanisation theme; depreciating currency, higher inflation and higher bond yields.

How do we make money?

But this post isn’t about being negative. It’s about making money. And I don’t want to go too much into the WHY of the South Africanisation themes around crime, unemployment, corruption and the breakdown of government services.

I’m just saying 5 years from now your view will have changed and you won’t think the US is so exceptional anymore. New trends will have emerged and money will be made along the way.

Here are some trends I expect to do well.

Rise of the Lower Class: Companies which provide exceptional value to the low-end consumer will thrive. Their demographic segment is expanding as people drop out of the middle class. Think McDonalds, Costco, and Carnival Cruises. Think video games as a way to entertain yourself without going anywhere (Sony, Tencent, Netease). Dominoes Pizza as a Friday night treat instead of going out. Maybe even appetite suppressants like vaping? How does a family keep up appearances, but still save money? Where are the subtle downshifts?