YWR: The US$ Crash

A USD$ crash.

It’s one of those things where once you see it, you can’t unsee it.

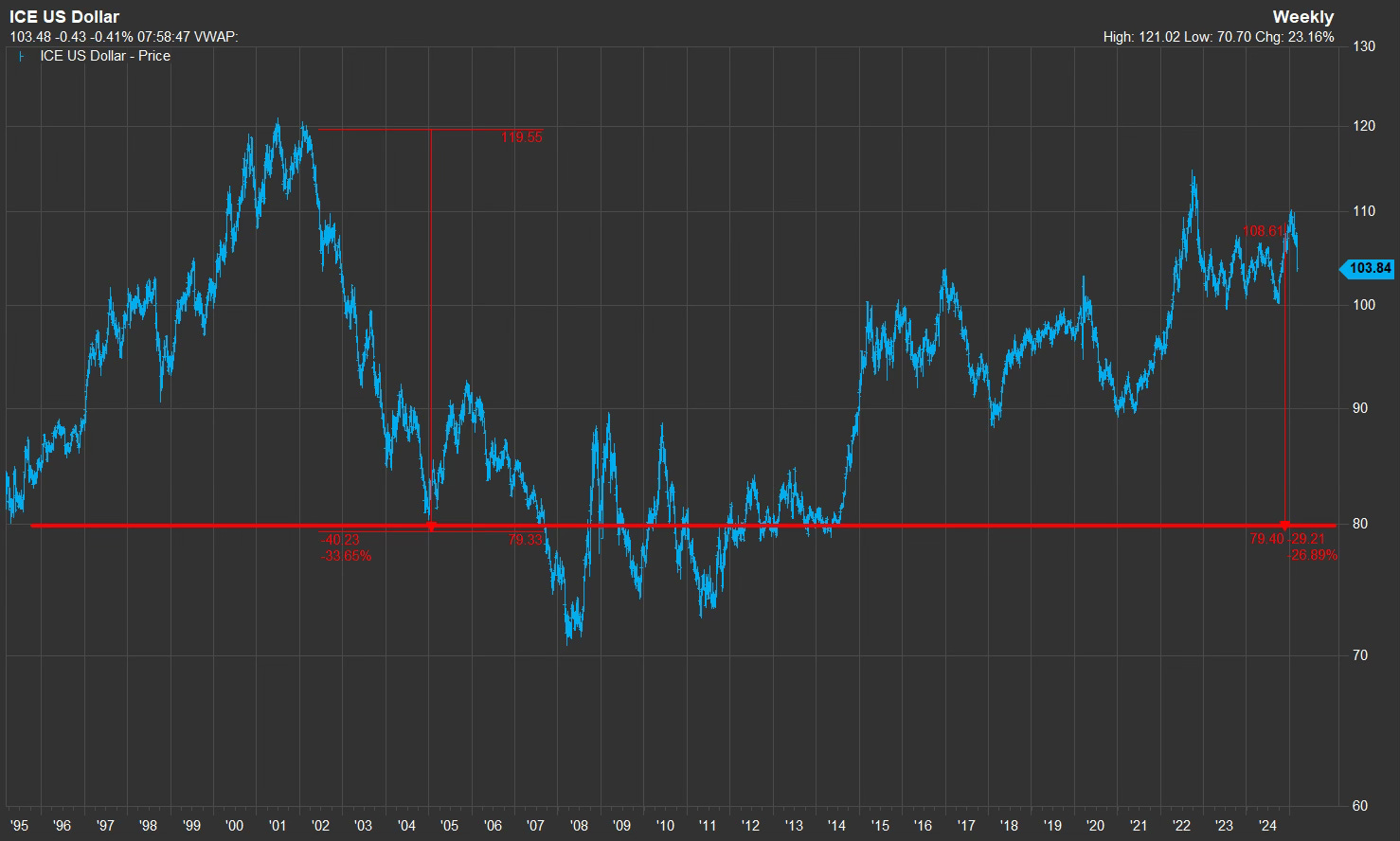

Not ‘97 Thai Bhat, but a 2 year -26% move in the ICE.

A repeat of 2000-2002. The ICE index back to 80.

EUR 1.30 and JPY 110.

It’s hard to imagine the dollar crashing, and FX is notoriously difficult to predict, but let’s review the set up.

Then let’s look at the asset allocation implications.

The Six Set Ups

#1 The Twin Deficits

A Martian would think we were an EM. The US runs persistently high government deficits and trade deficits. The Q4 budget deficit was 2.3% of GDP for 1 quarter!!! That is insane.

The trade deficit is setting records too.

But we all know the counterbalance to trade deficits is foreign investment inflows (Current Account = Capital Account + Financial Account).

Everyone loves to invest in the US. We are a capital sink for the world.

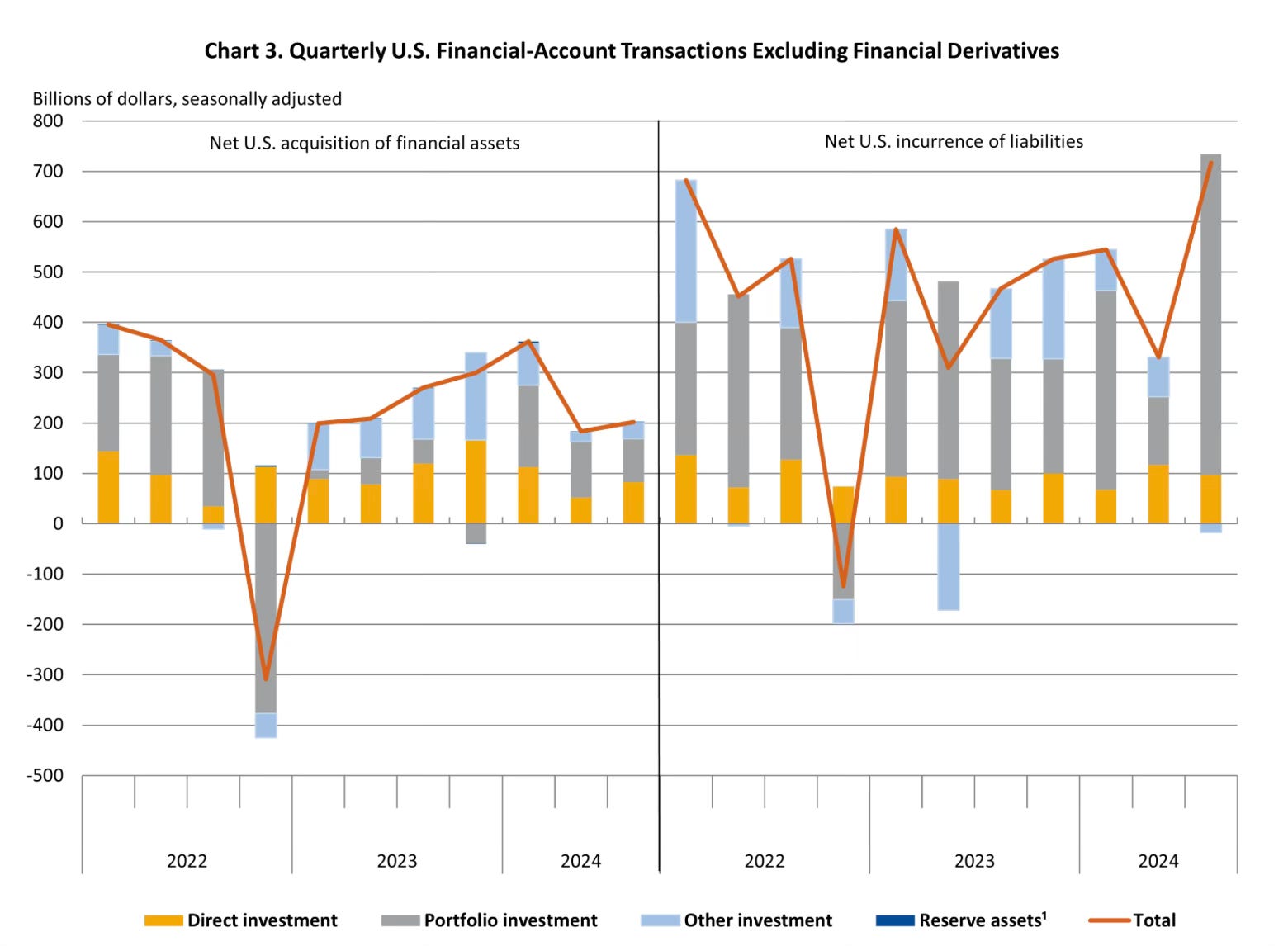

In Q3 there was a $300bn financial inflow into the US. Q4 will be even higher.

In the chart below compare the bar on the far right (investment inflows), to the last bar for the chart on the left (US outbound investment).

We spend money like a drunken sailor, and import everything, but it works because we finance it with our great stock market, world leading alternatives businesses, and stable currency.

Capital markets are our export. Right?

Let’s chip away at that too and see how these investment inflows might reverse. Or, already have.

Stocks

Our beloved stock market is close to the most unattractive it has ever been (2001 being the worst). The S&P 500 is trading on 28x trailing EPS. It sticks out because it is historically expensive vs international markets.

And forward earnings estimate momentum is negative.

Record high valuations, negative earnings momentum, and an overvalued currency? Doesn’t seem great for investment inflows.

#2 Money follows the Juice

Traders follow stimulus. They follow the juice.

To a trader the US looks expensive and depressing. No juice. Maybe even a recession (one of our 5 surprises for 2025).

Europe on the other hand looks good. ESG nonsense is dead and they are talking about defence spending, fiscal stimulus, and reconstruction. Sounds like a lot of money will be kicking around. Better go get some.

Sell your $’s and party in EUR.

Same thing with China. Trillions of RMB in stimulus and property bailouts. A Chinese version of TARP. Plus, it’s a cheap market + underowned.

Sell your $’s, buy RMB and party like it’s S&P 2009.

Especially, if you are Chinese and have $’s sitting in HK.

#3 Mrs Watanabe

We always talk about Mrs Watanabe and how she loves to sell JPY, with 0% yield, to buy US Treasuries and earn 4%. That’s been a great trade, but it’s time to close it out. Japanese 10 year bonds now yield 1.5% and the JPY is historically weak. Japanese tourism flows tell you that.

What happens when Mrs Watanabe, or Toyota, realise it’s attractive to bring $’s back to Japan and get some yield in their home currency for the first time? Especially, if the US$ looks risky.

Mrs Watanabe. Sell your $’s and buy JPY.

#4 Fed Credibility

The Fed is another negative. Last year’s rate cuts hurt their credibility. They jumped the gun and cut rates despite inflation sticky at 3%. The inflation terminator isn’t dead.

Now the Fed is stuck and unsure what to do. Does the economy weaken and bring inflation back to 2%? Or, do all these tariffs mean are we in a stagflation era where we get high inflation and low growth? And what if the US$ weakens?

Ooof. What a headache.

Net, net, the current set up is negative for the $. A Fed which doesn’t know what’s going on and inflation above target.

#5 Economic Warfare

Everyone is pissed off with the US, especially the Canadians. And if you are European, Australian, or Chinese why invest your savings in the US?

If it’s going to be economic warfare why invest in the enemy?

We’re still in the early stages with this, but it’s going to become a consideration in asset allocation decisions. The new ESG.

It’s not good for the US$ brand if everyone hates it.

#6 National Security vs the ‘World is Flat’

The Terminators cannot be built in China. That’s the bottom line. The US has to have strong manufacturing. It’s a national security issue. We have to be able to build our own robots. That’s why Trump says he doesn’t care about the stock market and want’s a weak US$. Longer term this is more important. That’s the change for investors. Maybe there is a Trump put, but it’s with the US$ down 20%.

#7 Mar-A-Lago Accords

We have the set up (#’s 1-6). Now the coup de grace.

Mar-A-Lago

Imagine you’re running a few hundred billion for the KIA or GIC.

You are already worried you over allocated to an expensive market with massive downside. You worry there could be an economic recession. You worry the US is overvalued. You are looking at losses on both the market value of your investments, plus the currency.

Now you read the president’s financial advisors (Steve Miran) are devising how they will force you to shift your US treasury holdings into 100 year bonds with a low yield to payback the US for all the defence spending you enjoyed in the past. Or, maybe a special fee on your interest payment remittances (Restructuring the Global Trading System).

Goodness gracious.

So my question is this.

Given what you’ve seen from Trump in the first 2 months, and every promise he has fulfilled, if you are sitting on billions of $’s in US assets, do you want to wait and see what policies Bessent and Miran announce? Or do you want to get in motion now?

You get moving now. And it’s why I don’t think there will ever be a Mar-A-Lago accord.

A bunch of finance ministers are not going to have dinner in Florid and devalue the US$.

It will happen naturally.

6% Ten Years

My big non-consensus call is that US 10 year yields are going to 6%.

The US$ weakening, investors selling bonds. It’s why I don’t see yields going down, and why they aren’t, even though the equity market is crashing. This is what happens in EM’s.

My one caveat is if the Fed does yield curve control (control the price), which Steve Miran advises.

If we go down that road then the US$ really implodes.

So how do we make money?