YWR: The World According to Glencore

Today’s YWR Special Event is a 1-1 with Glencore CEO, Gary Nagle

Erik: Gary! Thank you. It’s such a treat to have one of our favorite CEO’s in the YWR Studios.

Gary: You’re welcome. It’s pleasure. Our traders love YWR, and we learn a lot from it, so it’s great to be able to reciprocate.

But 2 things before we get going. Am I sitting in the right place? And I only have 45 min. I need to get to Heathrow for a flight.

Erik: Maybe shift a little to your right, so you aren’t blocking the sign. But then don’t worry. We’ll get you on the Piccadilly in 45 min and you’ll be fine. Let’s get going.

Can I start by saying why we love Glencore?

I feel like you have to be humble and polite, and can’t really say it the way you should. So I want to explain why Glencore is a core Dirty Dividends holding. Kind of set the stage.

Gary: You’re pitching me on Glencore? I’d love to hear that!

Erik: Truth is I actually started out by shorting Glencore back in 2014—2015 when you got over your skis with the physical trading book. But then came the coal deal with Rio Tinto. And that’s when I fell in love.

Our readers might not know the story, but around 2015-2018 Rio Tinto had a French CEO, name Jean Sebastian Jacques, who was a total moron, and at the time overly worried about Rio’s image on the world stage. In 2015 thermal coal prices were just $50/ton and everyone was saying how coal was a dying commodity and the price would go even lower. For J-S the pressure was too much. He also thought it was bad for Rio’s image to own coal mines, so he decided to exit the whole business.

Of course, people in the industry who had seen lots of cycles and who knew what they were doing, like your former CEO Ivan Glasberg, saw a massive opportunity to acquire the world’s best high quality coal assets on the lows. Ivan knew the numbers and saw that despite all the environmental rhetoric in the US and Europe, global coal demand was still growing and as rising demand met with falling supply, there would be a massive price squeeze.

Ivan wasn’t the only one who saw this. Yancoal, and a few PE firms also took coal mines off of Rio Tinto. I think you paid $1.7bn for your package of thermal and met coal,and I joked that some year in the future you would make that back in 1 year. And 2022 was that year. Richards Bay coal prices traded into the $300/ton range and your coal business alone made $19 billion of EBITDA!!!

So in summary, I like that Glencore management is super street smart, commercial and run by sensible South Africans who also own shares themselves. You are owner/operators. No disrespect to you Gary, but I sleep well knowing that with Ivan owning 10%, nothing stupid is going to happen.

I also really like the innovation of having a physical commodity trading operation attached to the mining business. The trading business is now running with lower risk and delivering $3bn/year.

The physical infrastructure associated with that trading business, the ports, smelters, train lines, refineries, etc is hard to replicate, so it has a moat in a way a Morgan Stanley trading business does not. The trading business also gives you great insight into commodity demand, flows and assets for potential acquisitions. You have your fingers in the pie everywhere, and I love it.

And when you have a supernormal year, like in 2022, you buy back 700 million shares and pay out special dividends.

Like I said, you are in the YWR Dirty Dividend portfolio, and Mrs YWR appreciates all the divies last year.

And so I always tune in your results calls as a shareholder, but also to hear Glencore’s view of the world.

Thank you for being here and now I hand it over to you to tell us what you are seeing.

Gary: Wow! Can I record that and play it at the next BOD meeting? But no, I am glad to share what we are seeing.

I put together a few slides for the audience. Is that OK?

I think really the message and the clear indications in the world today is the world is energy hungry.

The world needs energy.

And it doesn't matter how you look at it. You've got your normal economic growth where the world continues to grow and needs energy. But where else is the energy coming from?

You've got electrification of mobility. Clearly the growth in battery electric vehicles, significant growth. You have electrification of residential heating and industrial processes. We've seen a huge move towards that over the last 12 months and continue massive growth in that direction.

And obviously, the other area where we see huge amounts of energy growth, which is outside of the normal energy growth, is data centers, AI, crypto, those sorts of things.

So, I mean, looking at the graph and some the projections out there in terms of energy need the worlds or the energy demand the world will need in order to grow and continue on the trajectory is, we're going is very strong. Absolutely very strong.

And how is that hunger for energy being fed?

Now, a lot of money being spent, as we all know, in renewables, solar, wind turbines, and the like. And huge trillions of dollars have been spent on that. But there's two elements around that.

One, trillions of dollars being spent and it's still not enough to meet the growing demand for energy the world needs.

And number two, and this is where a lot of the world forgets that it's one thing building a solar farm. It's one thing building wind turbines. But these need to be connected to the grid. And the ability to connect them to the grid is massively challenged.

By some estimates, the world needs to spend over the next 16 to 17 years over $11 trillion on grid spending just to be able to connect that power to the grid. Very, very hard ask.

Now the world has to do that. The world needs to grow. The energy demand is there and we need to decarbonize. But it's not going to happen overnight. It's going to be difficult. Funding's needed, capital is needed, materials are needed. And in that time, we're still going to need the power.

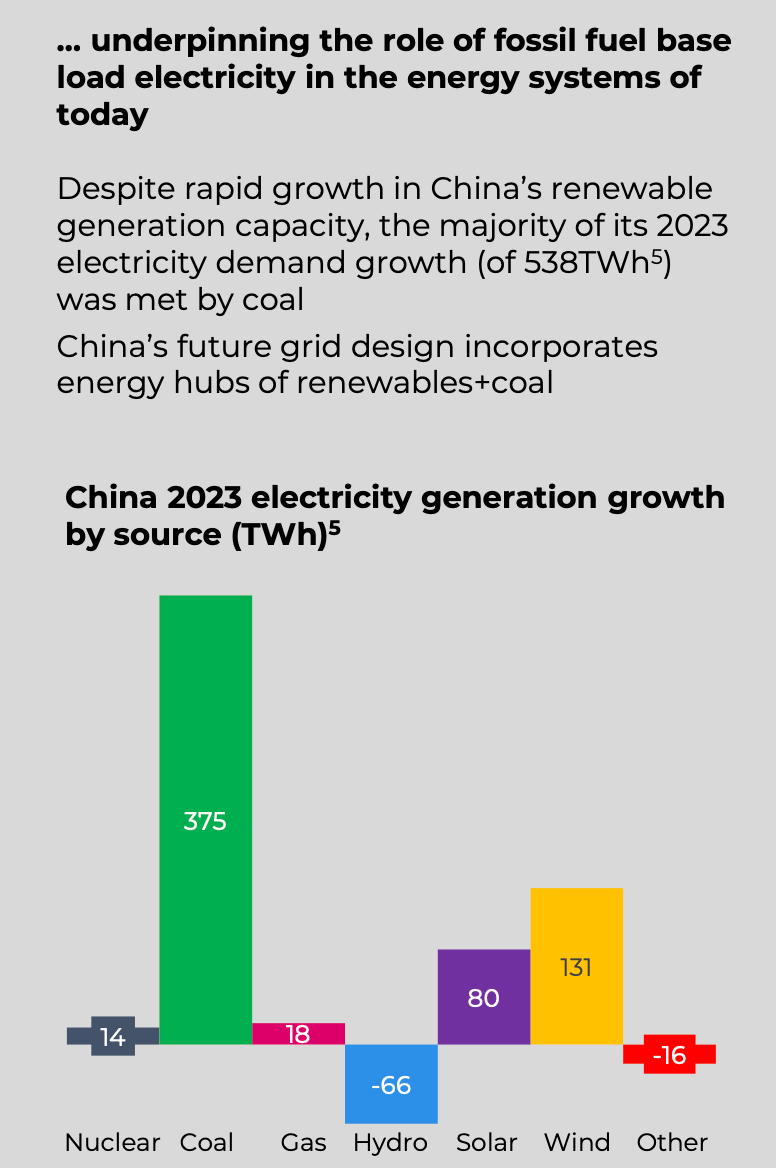

So where will baseload cheap power come from?

It's still going to come from hydrocarbons. It's still going to come from fossil fuels.

And if you look at the far right hand graph, you can see the amount that's still coming from – for power generation from fossil fuels. Now, in the Western world, nobody's building new steam coal mines. We're shutting, as Steve mentioned, 12 mines – at least 12 mines of ours will be shut over the next – between -- well, we've already shut five and we've got another at least seven between now and 2035. No one else is building big steam coal mines. So – and it's the right thing to do, to shut mines, to shut steam coal, and take it out of the world is the right thing to do.

But what does that mean when you've got a demand for power, which translates into demand for fossil fuels, and the supply response is not there because people are shutting mines and not developing new mines?

That's got to be bullish for fossil fuel prices going forward. And we believe our steam coal business, as we run it down responsibly, we prefer a value over volume model that the value of these mines and the margin that these mines will generate over time as we run down that volume will be material in our business. So from an energy perspective, supplying the energy needs of the world today as we transition to a low carbon economy, we are perfectly positioned within our steam coal business.

Erik: And what are you seeing in China? Everyone is afraid that 50% of metal demand comes from China and looking at the stock charts the fear is China is imploding.

But what is the real story?

Gary: Now, everybody last year spoke about China being weak and we all know property was weak.

And you can look at equity markets in China and things have been weak.

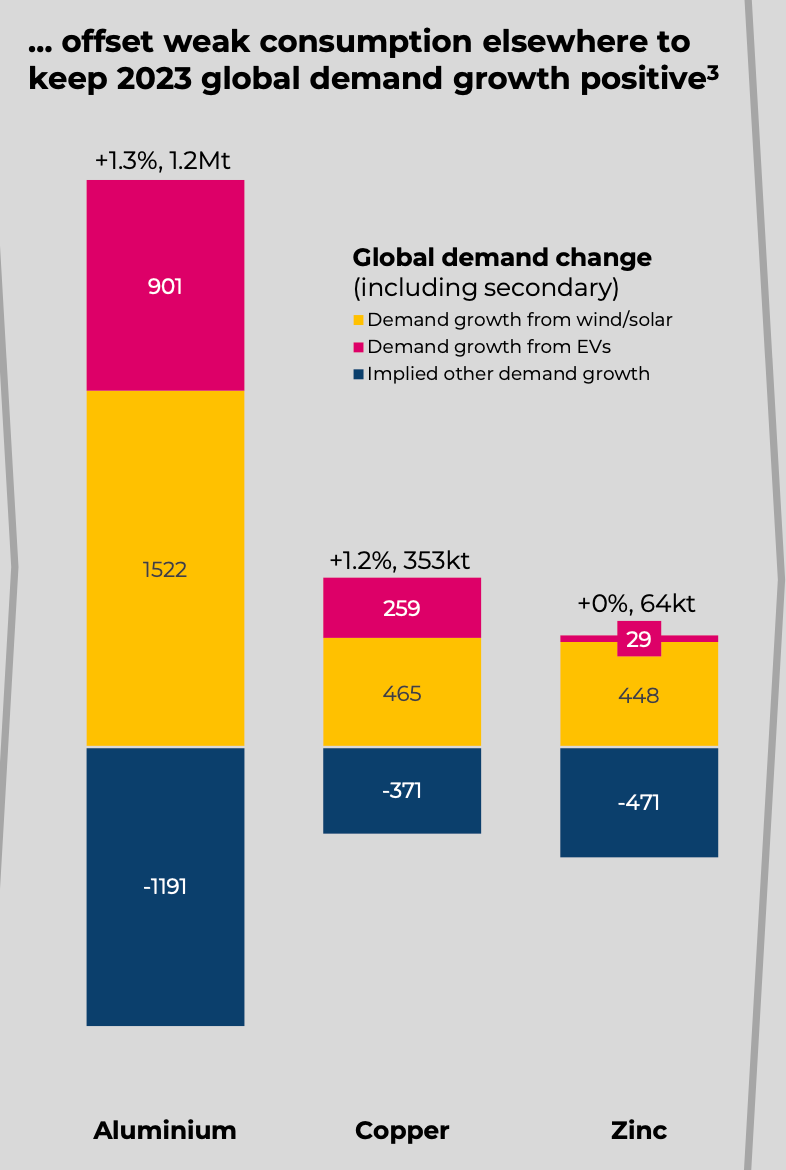

But ultimately we go on what the order book looks like, where we see material flowing. And last year China was strong, particularly in the commodities that we are strong in.

Demand for China – demand for copper in China last year was up between 5% and 6%. You can see it for zinc. You can see it for copper. You can see it for aluminium. Very strong demand from China last year.

And what's driving this demand? It's not – little bit yes, it's property completions. But when you look at the other big growth pillars within the Chinese economy, it's solar installations. It's wind installations. It's battery electric vehicles. This is driving – it's grid spending. This is driving the demand for materials in China.

And we see the order book strong this year again. They continue to buy materials as we transition to a low carbon world.

So in the middle, when you look at global growth of these key commodities that we trade, yes, the blue shows some implied demand weakness in the traditional markets, but that's more than offset by these new demand growth from EVs, from winds, from solar, and the likes. And that's why we've seen growth in China and we expect continued growth in China for demand in these key commodities.

Erik: Now Gary… this is all very exciting, but it leads right to another interesting point.

On the one hand you show the potential growth from all this energy transition demand, but on the other hand, Glencore is not adding any new supply, and you say you won’t add new supply unless prices are higher. And you aren’t the only ones with flat/declining supply. It’s the whole industry.

So how does this demand happen if the metal for it doesn’t exist?

I mean just sticking to Glencore, you look at your forecasts for copper, cobalt, nickel, etc there is no growth through 2026.

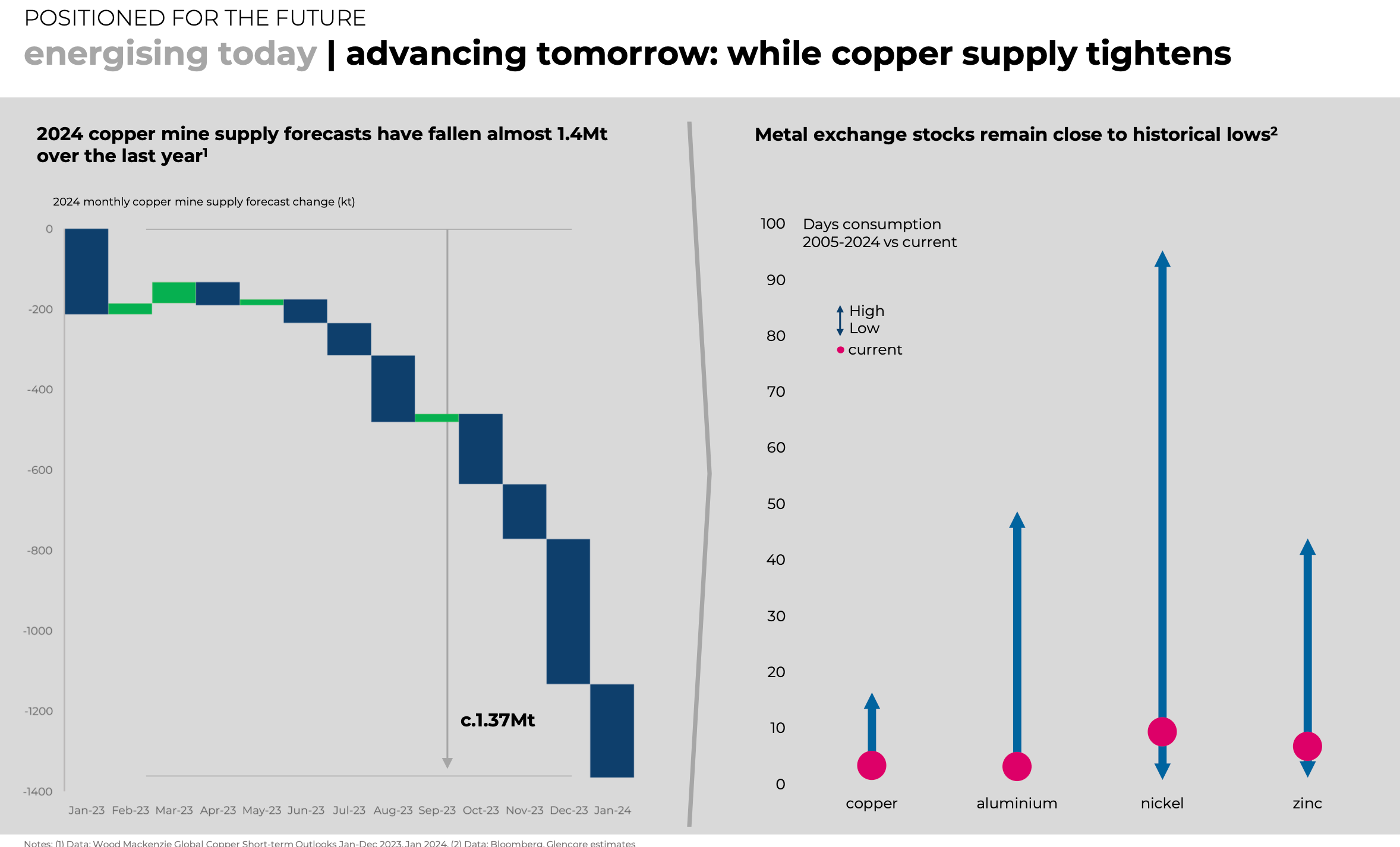

Gary: Are you saying you think there could be another price squeeze? It looks that way to us too. One of the things we keep saying is the market underestimates the challenges of these projects and of delivering new supply.

Let's talk copper supply. When we started 2023 everybody expected, in fact, a surplus in terms of supply to the market.

And the world thought 2024 would also be a surplus because you had the growth of the new big projects, Quellaveco, QB2, Kamoa all those coming on.

But as 2023 progressed, we had issues in Panama (the First Quantum Situation), we had issues in Chile, we had issues in Peru, we had issues in Africa. And ultimately supply would be down over 1.3 million tonnes for the year.

And 2024, again, there are challenges around where copper growth will come from. You now have QB2 at nearly full capacity. Quellaveco is at nameplate capacity. Kamoa is done. Oyu Tolgoy is done. There's nothing more coming.

And so the market looks tight, but the copper price is not reflecting that tightness.

And as Glencore, we would never bring new volumes into a market in anticipation of higher prices. We want to see higher prices first. We need – and we believe the world will have higher prices because of the supply demand deficit. And it's only at that stage where we bring these units into the market.

Erik: Makes sense.

Can we talk about your copper projects in Argentina? Because you said you are really impressed with the new government and you think it might be the best new mining jurisdiction in the world.

Gary: Before we go there, I just want to talk about one other critical mineral and in some parts of the world, steelmaking coal is classified as a critical mineral, particularly in the EU, and they're discussing it to do the same in Canada.

Elk Valley Resources (EVR), which we are acquiring from Teck, is a major producer of hard coking coal, 24 million to 26 million tonnes. And that high quality hard coking coal is absolutely essential in steelmaking and that steel needed for the energy transition, whether it be for the wind turbines, whether it be for the transmission grids, whatever it may be that steel is needed and there's no immediate or short term replacement for hard coking coal. 90% of the global blast furnace fleet is less than 15 years old. It's a very young fleet of blast furnaces, and this will be for a very long time. So the demand for hard coking coal looks very strong over the next short, medium, and long term.

So those are the three pictures of where our business is, a excellent steam coal business that's running down in an energy short world, a unbelievable metals business where the demand is growing and I don't think the world can keep up with that growth, and a soon to be incorporated coking coal business with a very good future for coking coal – for steelmaking coal.

Erik: Love it. No one ever gets bullish on steel, and yet it is doing surprisingly well. It shows up in the YWR Factor Model.

And Argentina? What do you think of the new government?

Gary: Edwards and I, our head of corporate affairs, met with much of – some of the senior government officials from Argentina in, Davos recently. And the message from them is very encouraging, very business friendly. They're looking for investment. They want to give certainty to investors. They want to see investors come and spend their money in the country and be able to take the money out, ultimately, create jobs, create opportunities and do well. So the noise coming out of Argentina is excellent. It's looking like a very exciting country and we have two big projects there.

Now I’m worried I’ve gone over and should be getting to the airport.

Erik: Yes, let’s get you on your way. Terminal 3 or 5?

Gary: 5. I think.

Erik: OK. So turn left out of the studios and walk along the street until you get to the Tube station. The Piccadilly line will take you directly to Heathrow. Just make sure the sign says Terminal 5. Not 4. You’ll be there in 45 min. Thank you again!

Gary: Awesome. It was fun. And WhatsApp me when you are in SA next, so we can meet up.

OK. He’s gone.

Let’s do the post-game on how we make money on this.

Let’s also review the model and a link to Gary’s full presentation.